Learning Outcomes

This article outlines the classification of testamentary gifts—specific, general, demonstrative, pecuniary, and residuary—and how each is identified, construed, and fulfilled during estate administration; distinguishes which gifts adeem on the non‑existence or disposal of the subject matter and which remain enforceable as general or demonstrative legacies; examines when a will “speaks” as to property and as to persons, and how these default timing rules and class‑closing principles affect entitlement; discusses statutory and express substitution mechanisms, including anti‑lapse for gifts to issue, and the consequences of lapse for residue and potential intestacy; explains the statutory order of abatement, the incidence of secured and unsecured debts, and the differing treatment of specific, general, demonstrative, and pecuniary gifts where funds are insufficient; reviews the effect of directions such as “free of mortgage” and charging clauses on the burden of liabilities; and analyzes how disclaimer, forfeiture, divorce or dissolution, and witnessing by a beneficiary can defeat or redirect gifts and alter the final composition of the residuary estate.

SQE1 Syllabus

For SQE1, you are required to understand the interpretation of wills and failure of gifts, including the types of gifts—specific, general, demonstrative, pecuniary, and residuary—with a focus on the following syllabus points:

- the different types of gifts in wills: specific, general, demonstrative, pecuniary, and residuary

- how to distinguish between these gift types in practice

- the legal principles governing the interpretation of will clauses

- the main reasons why gifts may fail, including ademption and lapse

- the consequences of failed gifts for estate distribution

- the statutory anti‑lapse rule for gifts to issue and its limits

- the order of abatement and its impact on legacies and devises

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the difference between a specific gift and a general gift in a will?

- What happens if a specific gift is no longer in the testator’s estate at death?

- How is a demonstrative gift treated if the specified fund is insufficient?

- What is the effect of a beneficiary predeceasing the testator on a pecuniary legacy?

Introduction

When interpreting a will, you must identify the type of gift being made, as this determines how the gift is fulfilled and what happens if it fails. The classification of gifts—specific, general, demonstrative, pecuniary, and residuary—affects the rights of beneficiaries and the duties of personal representatives. Understanding these distinctions is essential for SQE1 and for advising clients on estate administration.

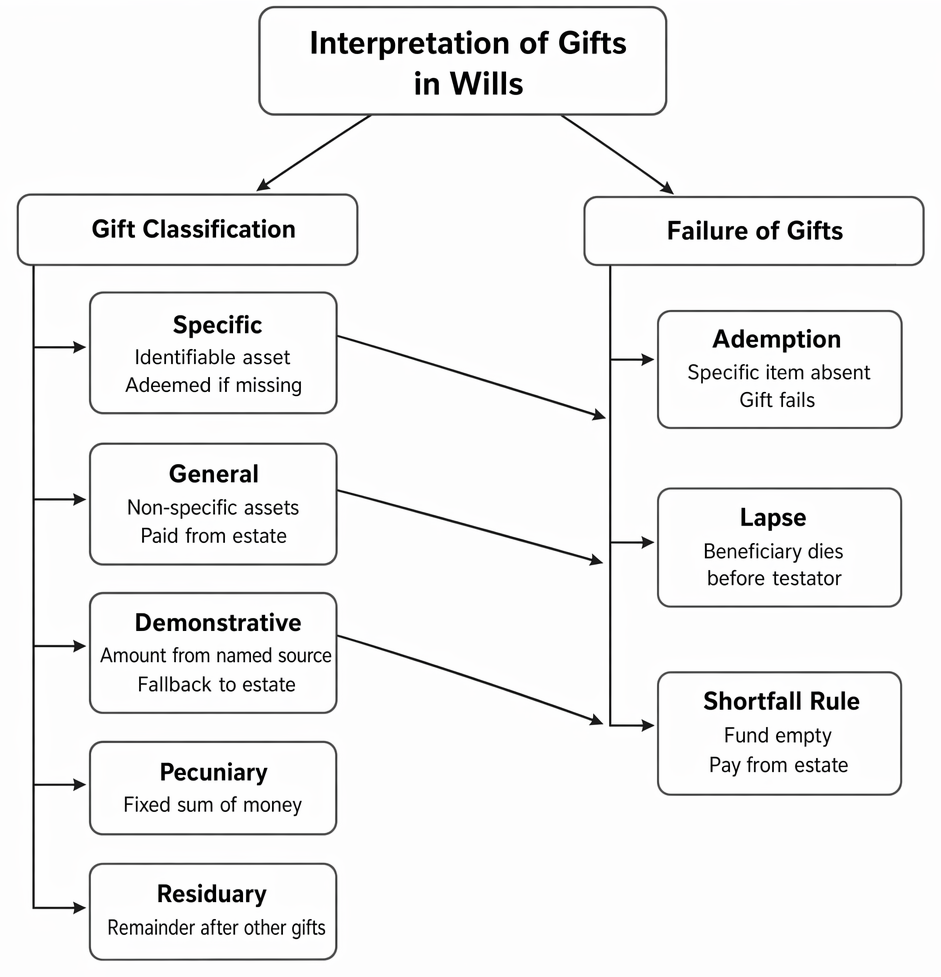

Interpretation of testamentary gifts in wills by classification and principal grounds of failure, including ademption, lapse, and the shortfall rule.

Correct classification also interacts with broader rules of interpretation. Subject to contrary intention, a will “speaks” as to property from the date of death (so descriptions are read in light of the estate at death), but as to people from the date of execution (so class membership is determined by who fits the description when the will was signed, subject to class‑closing rules). How gifts are affected by debts and expenses depends on statutory abatement rules, and failures such as ademption or lapse have distinct consequences for residue and, sometimes, intestacy.

Key Term: specific gift

A gift of a particular, identified item or asset owned by the testator at death, such as “my diamond ring” or “my car”. Key Term: general gift

A gift that can be satisfied from any suitable property in the estate, such as “£5,000 to my niece” or “a car to my brother”. Key Term: demonstrative gift

A gift of a stated amount or property, to be paid from a particular fund or account, but payable from general assets if the fund is insufficient. If the specified fund is insufficient, the balance is paid from the general estate. Key Term: pecuniary gift

A gift of a fixed sum of money, usually payable from the general estate, such as “£10,000 to my friend”. Key Term: residuary gift

A gift of all property remaining in the estate after payment of debts, expenses, and other gifts. Key Term: ademption

The failure of a specific gift because the item is not owned by the testator at death. Key Term: lapse

The failure of a gift because the beneficiary dies before the testator, unless saved by statute or substitution.Test Tip: In SQE-style questions on Types of gifts: specific, general, demonstrative, pecuniary, residuary, identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

Types of Gifts in Wills

Specific Gifts

A specific gift is a testamentary gift of a particular, identifiable asset, distinguished from all other property in the estate. Phrases such as “my Rolex watch,” “the painting by Turner,” or “the 500 shares in X Co plc registered in my name at the date of this will” signal specificity. Correct classification turns on whether the description singles out an identified thing (or quantified part of a particular thing) rather than an amount or type.

If the asset is not in the estate at death, the gift fails (is “adeemed”). Ademption is an automatic consequence for specific legacies and devises; the beneficiary has no claim on the asset’s sale proceeds unless the will provides otherwise. Be careful with descriptions: “a BMW car” is not specific; “my BMW registration number AB12 CDE” is specific.

The way an asset leaves the estate can matter in borderline scenarios (for example, corporate reorganisations or account renumbering), but the core SQE1 principle is that only specific gifts adeem and general/demonstrative gifts do not. Always check for contrary intention in the will.

General Gifts

A general gift is a gift of property described by type or amount, not referring to any particular asset. Examples include “£5,000 to Y,” “a laptop to X,” or “100 shares in X plc to my son.” These gifts are satisfied from the estate’s general assets at death.

General gifts do not adeem merely because the testator did not own an item fitting the description when they died. If the estate has sufficient funds or items to satisfy the description, the personal representatives (PRs) purchase or allocate accordingly (for example, buying 100 X plc shares if the testator did not own them).

Demonstrative Gifts

A demonstrative gift is a hybrid: a gift of a sum of money or property, directed to be paid primarily from a specified source, but not limited to that source. “£2,000 from my HSBC account to Z” is demonstrative. If the named fund exists and contains enough, the gift is paid from it. If the fund is insufficient or does not exist, the gift is treated as general to the extent of any shortfall.

Demonstrative gifts do not adeem. They are treated as specific to the extent the named fund exists (relevant for abatement order), and general beyond that. This classification affects the order in which assets are applied to debts and expenses if the estate is strained.

Pecuniary Gifts

A pecuniary gift is a gift of a fixed sum of money. Pecuniary legacies are commonly general (for example, “£10,000 to A”), but may be demonstrative (“£10,000 to be paid from my Nationwide savings account”) or even specific (“the £100 in the safe”).

Where multiple pecuniary legacies exist and the estate is insufficient, they generally abate proportionately unless the will gives one priority. Interest on general pecuniary legacies typically runs from the end of the executor’s year unless the will directs otherwise.

Residuary Gifts

A residuary gift is a gift of the remainder of the estate after all debts, expenses, and other gifts have been paid. Residue is a “sweep‑up” gift and often the largest in economic terms. If there is no effective residuary gift (or it fails), the undisposed property passes under the intestacy rules.

Residuary gifts can be shared among beneficiaries and may be given “subject to” directions, such as payment of debts from residue, which can alter the default incidence of liabilities.

Legal Effects and Consequences of Gift Types

The classification of a gift determines:

- How the gift is fulfilled (from which assets)

- The order in which gifts are satisfied if the estate is insufficient

- What happens if the gift fails (e.g., ademption, lapse, abatement)

- Whether statutory anti‑lapse applies and whether shortfalls are met from general assets

Interpretation baseline rules:

- As to property, a will speaks from death unless the will indicates a contrary intention (for example, “now” or “at present” wording).

- As to people, a will speaks from execution: the identity of the class (e.g., “my nephews”) is determined at the date of the will, subject to class‑closing rules. Classes generally close when at least one member has a vested interest.

Abatement and incidence of liabilities:

-

In a solvent estate (where debts and expenses can be paid in full), the statutory order applies to unsecured debts and expenses. Subject to contrary intention, assets are applied in the following broad order:

- Property undisposed of by will (subject to retaining a fund to meet pecuniary legacies)

- Property specifically given for payment of debts, if any

- Property specifically charged with debts (surplus after charges)

- The pecuniary legacy fund (pecuniary legacies abate rateably)

- Specific legacies and devises (rateably according to value)

-

Secured debts attach to the specific property unless the will shows a contrary intention (for example, “free of mortgage” or an express direction that secured debts are to be paid from residue).

Key Term: abatement

The reduction of legacies when the estate is insufficient to pay all debts, expenses, and legacies in full, following the statutory order of application. Key Term: marshalling

An equitable doctrine allowing a disappointed beneficiary to be compensated from residue where assets within a category not liable to bear a debt were used by PRs to pay that debt.

Worked Example 1.1

A will states: “I give my Rolex watch to my nephew, £5,000 from my Barclays account to my niece, and £10,000 to my cousin.”

Question: How should these gifts be classified?

Answer:

The Rolex watch is a specific gift. The £5,000 from the Barclays account is a demonstrative gift. The £10,000 to the cousin is a general pecuniary gift.

Failure of Gifts

Gifts in wills may fail for several reasons. The main types of failure are ademption and lapse, but disclaimers, forfeiture, divorce/dissolution, witnessing by a beneficiary, uncertainty, and unmet conditions can also defeat gifts.

Ademption

Ademption occurs when a specific gift is no longer in the estate at death. The gift is “adeemed” and the beneficiary receives nothing.

Lapse

Lapse occurs when a beneficiary predeceases the testator. Unless the will provides otherwise, the gift fails and falls into residue or, if the gift is of residue, into intestacy. A statutory anti‑lapse rule can save gifts to “issue.”

Key Term: statutory substitution (anti‑lapse)

Where a gift is to a child or other issue of the testator who predeceases leaving living issue, the gift passes to those living issue unless the will excludes the rule.

Other failure scenarios:

- Witnessing by a beneficiary or their spouse/civil partner: the will remains valid, but the gift to that person fails.

- Divorce/dissolution: does not revoke the will, but gifts to and appointments of the former spouse/civil partner are treated as if that person had predeceased.

- Forfeiture: a killer cannot benefit from the victim’s estate; limited statutory relief may be available except in cases of murder.

- Disclaimer: a beneficiary may disclaim a gift, causing it to pass as though they had predeceased (often into residue).

Worked Example 1.2

A testator leaves “my painting by Turner to my daughter.” Before death, the painting is sold and not replaced.

Question: What is the effect on the gift?

Answer:

The gift is adeemed. The daughter receives nothing, as the painting is no longer in the estate.

Worked Example 1.3

A will leaves “£2,000 to my friend Sam.” Sam dies before the testator. The will does not provide for substitution.

Question: What happens to the gift?

Answer:

The gift lapses. The £2,000 falls into residue.

Worked Example 1.4

T leaves “£20,000 to my son P.” P dies before T, leaving two children alive at T’s death. The will is silent on substitution.

Question: Does the gift fail?

Answer:

The gift is saved by statutory substitution (anti‑lapse) because the gift was to issue. P’s living children take the £20,000 in place of P, unless the will expressly excludes the rule.

Demonstrative Gifts and Insufficient Funds

If a demonstrative gift cannot be fully satisfied from the specified fund, the shortfall is paid from general assets. If the fund does not exist at all, the gift is treated as a general pecuniary gift. To the extent the named fund exists at death, the gift is treated as specific for abatement purposes; any balance is treated as general.

Worked Example 1.5

A will leaves “£30,000 to D to be paid from my Halifax savings account.” At death, the Halifax account contains £8,000, the general estate contains £25,000, and the will also gives a specific painting and a residuary gift.

Question: How is D’s gift fulfilled and which assets bear debts first?

Answer:

£8,000 is paid from the Halifax account. The remaining £22,000 is a general pecuniary legacy and is paid from general assets (subject to abatement with other pecuniary legacies if funds are insufficient). For unsecured debts, undisposed property is applied first, then the pecuniary legacy fund rateably, and only thereafter specific gifts are reached.

Worked Example 1.6

A will gives “my cottage to A free of mortgage.” The cottage is subject to a mortgage of £50,000.

Question: How is the mortgage treated?

Answer:

The “free of mortgage” wording shows contrary intention. The mortgage must be discharged from residue (or other assets directed), so A takes the cottage unencumbered. Without such wording, A would take subject to the mortgage.

Worked Example 1.7

A will gives “£10,000 to F from my HSBC current account.” The account was closed before death and the will contains no contrary intention.

Question: Does the gift fail?

Answer:

No. The gift is demonstrative and is payable from general assets when the specified fund does not exist. It does not adeem.

Demonstrative Gifts and Insufficient Funds (continued)

If a demonstrative gift cannot be fully satisfied from the specified fund, the shortfall is paid from general assets. If the fund does not exist at all, the gift is treated as a general pecuniary gift. To the extent the specified fund exists, the demonstrative legacy is treated as specific for abatement; any shortfall abates with the pecuniary legacy fund.

Revision Tip: For SQE1, be careful to distinguish between specific and general gifts. Only specific gifts are subject to ademption. Demonstrative gifts are not adeemed if the fund is missing—they become general gifts.

Further Interpretation Principles and Administration Consequences

Will speaks from death (property) and from execution (persons):

- Property descriptions are read in light of the estate at death (subject to contrary intention), so general legacies can be met by buying assets if needed.

- Persons are determined at execution; where classes are involved (e.g., “my nephews”), class‑closing rules ensure administration is practicable. Wording can expressly fix the class (e.g., “living at my death”).

Interest and income on legacies:

- General pecuniary legacies generally carry interest from the end of the executor’s year unless the will provides otherwise.

- Income arising on specific gifts between death and assent typically belongs to the specific legatee; residue income belongs to residuary beneficiaries subject to the PRs’ duties.

Abatement detail and marshalling:

- Pecuniary legacies abate rateably if the retained fund is insufficient. Specific gifts abate last and rateably according to value.

- If PRs pay a debt from assets that (as between beneficiaries) should not have borne it, a disappointed beneficiary can seek marshalling from residue.

Contrary intention:

- The statutory order can be displaced by express will directions, including directions to pay debts out of residue, or stating property is “free of mortgage.”

Insolvent estates:

- If the estate cannot pay debts in full, beneficiaries receive nothing. Secured creditors are paid to the extent of their security; unsecured creditors are paid in statutory priority, abating rateably within each class.

Summary Table: Types of Gifts

| Type | Example | Main Features | Failure (if any) |

|---|---|---|---|

| Specific | “my gold ring to X” | Identified asset; only that item | Adeemed if not in estate |

| General | “£1,000 to Y” | Not tied to any asset; paid from general assets | Not adeemed |

| Demonstrative | “£2,000 from my HSBC account to Z” | Paid from fund, then general assets if needed | Not adeemed; shortfall paid |

| Pecuniary | “£5,000 to A” | Fixed sum of money | Not adeemed |

| Residuary | “rest of my estate to B” | All remaining assets after other gifts | Fails if no beneficiary |

Key Point Checklist

This article has covered the following key knowledge points:

- The main types of testamentary gifts are specific, general, demonstrative, pecuniary, and residuary.

- Specific gifts are of identified assets and are subject to ademption if the asset is not in the estate at death.

- General gifts are satisfied from any suitable property and are not adeemed.

- Demonstrative gifts are paid from a specified fund, but if the fund is insufficient, the balance is paid from general assets; to the extent the fund exists, the demonstrative legacy is treated as specific for abatement.

- Pecuniary gifts are fixed sums of money; multiple pecuniary legacies abate proportionately where funds are insufficient unless a priority is expressed.

- Residuary gifts dispose of the remainder of the estate after all other gifts and debts; failure of a residuary gift leads to intestacy for the undisposed property.

- Gifts may fail by ademption (specific gifts) or lapse (beneficiary predeceases the testator), but statutory anti‑lapse can save gifts to issue.

- The statutory order of abatement governs the incidence of unsecured debts and expenses; secured debts attach to the asset unless the will shows contrary intention (e.g., “free of mortgage”).

- Marshalling can compensate a beneficiary where assets within a category not liable to bear a debt were used by PRs to pay that debt.

- Will speaks from death for property and from execution for persons, subject to class‑closing rules and any contrary intention in the will.

Key Terms and Concepts

- specific gift

- general gift

- demonstrative gift

- pecuniary gift

- residuary gift

- ademption

- lapse

- statutory substitution (anti‑lapse)

- abatement

- marshalling

Demonstrative Gifts and Insufficient Funds (continued)

If the named fund exists but is too small, pay the demonstrative gift from that fund first (treated as specific for abatement), then meet the balance as a general pecuniary legacy from other assets. If no fund exists, treat the entire demonstrative gift as a general pecuniary legacy. Where multiple pecuniary legacies compete, they abate rateably unless the will provides for priority.

Residuary Gifts (continued)

The residuary gift covers all property not otherwise disposed of. If a residuary beneficiary predeceases the testator and there is no substitution, their share passes under the intestacy rules. Directions such as “subject to payment of debts from residue” or “free of mortgage” can alter the default incidence of liabilities, thereby affecting the amount available as residue. Where all earlier gifts fail, residue may enlarge; where multiple earlier gifts and liabilities exhaust assets, residue may be nil.