Learning Outcomes

This article outlines the management of client money and client accounts under the SRA Accounts Rules, including:

- the definition and four categories of client money, with clear distinction from business money, VAT treatment and billing consequences

- the different types of client account (general, separate designated and joint), when each is appropriate and the "available on demand" requirement

- the principle of segregation, prompt deposit of client money, and correct handling of mixed and mis-posted receipts

- rules on opening, naming and operating client accounts, including authorisation controls and the sufficient-funds-for-that-client rule

- when client money must be paid into a client account, the limited exceptions, and how firms that do not operate client accounts must protect funds

- restrictions on withdrawals, the prohibition on using client accounts as banking facilities, and typical examination traps in this area

- procedures for returning client money, managing residual balances, charity payments, and when SRA authorisation is required

- record-keeping, reconciliation and reporting duties, including the role of the COFA and the significance of qualified accountant’s reports

- how firms must account for interest on client money, apply de minimis policies fairly, and use separate designated deposit accounts

- common breaches of the SRA Accounts Rules, how they are identified in exam scenarios, and the steps needed to remedy shortfalls promptly

SQE1 Syllabus

For SQE1, you are required to understand the management of client money and client accounts under the SRA Accounts Rules, with a focus on the following syllabus points:

- the definition and categories of client money

- the distinction between client money and business money

- the requirements for opening and operating client accounts

- the rules for segregation and prompt deposit of client money

- the types of client accounts (general, designated, joint)

- the compliance obligations for recording, returning, and safeguarding client money

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which of the following is client money under the SRA Accounts Rules?

- a) Money received for unpaid disbursements before a bill is delivered

- b) Money received for paid disbursements after a bill is delivered

- c) Money received for the firm's own fees after a bill is delivered

- d) Money held as a trustee for a trust

-

What is the main reason for keeping client money separate from business money?

-

True or false? A solicitor may use a client account to provide banking facilities for a client’s convenience.

-

Which type of account must include the word "client" in its name and be held at a bank or building society in England or Wales?

Introduction

When a solicitor or law firm receives or holds money for a client, strict rules apply to ensure that these funds are protected and not misused. The SRA Accounts Rules set out the requirements for handling client money and operating client accounts. Understanding these rules is essential for SQE1 and for ethical legal practice.

Client money and accounts management under the SRA Accounts Rules is summarised by core definitions, segregation, account types, records and oversight.

The current framework is principles-based. The focus is on safeguarding money, keeping client funds separate, using client money only for its intended purpose, and maintaining effective systems and controls. These obligations apply to authorised bodies, their managers and employees. In practice, managers and the firm’s COFA are expected to ensure there are robust procedures, staff training, regular reconciliations, and prompt remediation of any breaches.

Test Tip: In SQE-style questions on Overview of client money and client accounts, identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

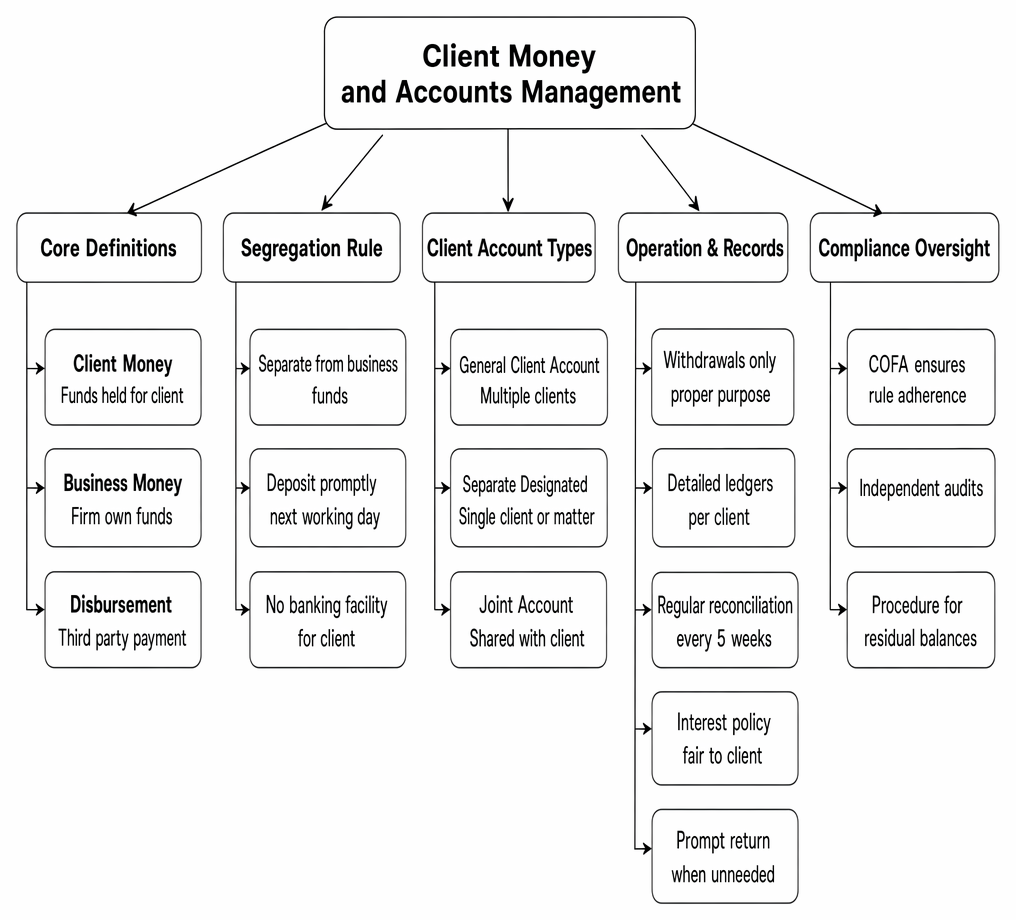

What is Client Money?

Client money is any money received or held by a solicitor relating to regulated legal services for a client, or on behalf of a third party in connection with those services. This includes funds for legal fees and disbursements (before a bill is delivered), settlement proceeds, property sale proceeds, and trust funds.

Key Term: client money

Money held or received by a solicitor relating to regulated services delivered to a client, or on behalf of a third party, or as a trustee, or for unpaid fees and disbursements before a bill is delivered. Key Term: business money

Money belonging to the law firm itself, such as fees received after a bill is delivered or reimbursement for disbursements already paid by the firm. Key Term: disbursement

A payment made by a solicitor to a third party on behalf of a client, such as court fees or search fees. Whether it is client or business money depends on whether it has been billed and paid.

In practice, client money covers four broad categories:

- money held for clients in connection with regulated services (e.g., completion monies, damages, sale proceeds)

- money held on behalf of third parties in relation to regulated services (e.g., stakeholder deposits held for buyer and seller; sender’s order)

- money held when acting as a trustee or in certain specified appointments (e.g., donee of a power of attorney, Court of Protection deputy)

- money in respect of fees and any unpaid disbursements if held prior to delivery of a bill

Conversely, money received in reimbursement for disbursements already paid by the firm, or for fees after a bill has been delivered, is business money and should not be paid into a client account.

The Principle of Segregation

Solicitors must keep client money entirely separate from business money. This is a fundamental requirement of the SRA Accounts Rules. Client money must be paid promptly into a client account and never mixed with the firm's own funds.

Key Term: segregation

The requirement to keep client money separate from business money at all times.

Segregation also entails dealing correctly with mixed receipts. If funds combine client and business elements (for example a single bank transfer covering completion funds and a billed fee), the firm must allocate promptly to the correct accounts, either by splitting the receipt at bank if possible or by transferring the relevant elements straight away from the account first credited to the appropriate account.

Client Accounts: Types and Requirements

A client account is a bank or building society account used exclusively for holding client money. The account must be in England or Wales and must include the word "client" in its name.

Key Term: client account

A bank or building society account, clearly designated as a client account, used solely for holding client money.

There are several types of client accounts:

- General client account: Used for holding money belonging to multiple clients. This is the pooled account most firms operate.

- Separate designated client account: Opened for a specific client or matter, often for large sums or long-term holdings. These are deposit accounts in the client’s name with the firm clearly identified.

- Joint account: Opened jointly with a client or third party, usually for a specific transaction. It is not, strictly, a client account, but certain record-keeping requirements still apply (e.g., obtaining statements every five weeks and keeping a central record of bills relating to it).

Key Term: general client account

The main client account used by a firm to hold money for multiple clients. Key Term: separate designated client account

A client account opened for a single client or matter, with the client's name in the account title. Key Term: joint account

An account held in the joint names of the solicitor and the client or a third party, not strictly a client account but still subject to some SRA requirements.

The client account must be available on demand. This means the firm should operate instant-access client accounts unless a different arrangement is agreed in writing with the client or relevant third party (for example, an agreed notice period deposit where the client benefits from higher interest). Any such agreement should be clear and retained on file.

Some firms may legitimately choose not to operate a client account. This is permitted where the only client money received comprises sums toward the firm’s own fees and unpaid disbursements before billing, and the firm has informed clients in advance where and how the money will be held. Firms may also agree in writing to hold money under alternative arrangements, provided adequate safeguards are in place and records are kept.

It remains the firm’s responsibility to ensure payments into and out of client accounts relate to regulated services. A client account must not be used as a banking facility for clients or third parties.

Receiving and Paying in Client Money

All client money must be paid promptly into a client account. "Promptly" generally means on the day of receipt or the next working day. The only exceptions are:

- Money received for disbursements already paid by the firm (business money)

- Money from the Legal Aid Agency for the firm's costs

- Money held as a trustee or under a specified appointment where other rules apply

- Where an alternative arrangement is agreed in writing with the client

In addition, where a firm holds money for a client over a prolonged period or a large sum is involved, it may be appropriate to open a separate designated client account so that interest can be accounted for more precisely and in full.

Firms should maintain clear narratives linking every receipt to a client, matter, and purpose. Where the purpose changes (for example, net proceeds become a gift to another client), an internal reallocation (inter-client transfer) on the ledgers will be required, even though no bank movement occurs.

Worked Example 1.1

A solicitor receives £5,000 from a client as a deposit for a property purchase and £500 on account of legal fees (no bill delivered yet). What should the solicitor do with these funds?

Answer:

Both amounts are client money and must be paid promptly into a client account. The solicitor cannot pay either sum into the business account.

Worked Example 1.2

A criminal defence firm receives monthly payments from the Legal Aid Agency covering its professional fees and paid disbursements. Must these LAA funds be paid into a client account?

Answer:

No. Payments from the LAA for the firm’s costs may be paid straight into the business account. The firm must still ensure timely payment of any third-party fees covered by the grant and maintain clear records.

Operating and Managing Client Accounts

Client accounts must be held at a bank or building society in England or Wales, and the account name must include the word "client." The firm must keep accurate records for each client, showing all receipts and payments. In addition to segregation, two managerial controls are critical:

- Client money should be available on demand unless a written agreement provides otherwise.

- Withdrawals must be appropriately authorised and supervised, and only made if sufficient funds are held for that specific client or third party.

Withdrawals from a client account can only be made:

- For the purpose for which the money is held (e.g., paying a third party in a transaction)

- On the client's written instructions (or those of the relevant third party)

- With SRA authorisation (e.g., for unclaimed balances exceeding the prescribed limit, see “Returning Client Money” below)

Transfers to pay the firm’s costs can only be made after a bill (or other written notification of costs) has been given, and the sum transferred must match the billed amount covered by funds held for that client. Where anticipated disbursements have been billed but not yet paid, good practice is to retain those amounts in client account until paid.

Firms must never use a client account to provide banking facilities for clients or third parties. Payments into and out of the account must relate to legal services.

Exam Warning: Using a client account as a banking facility for a client’s convenience (e.g., paying personal bills or holding funds unrelated to legal work) is a serious breach of the SRA Accounts Rules and may result in disciplinary action.

Worked Example 1.3

The firm receives £120,000 net sale proceeds. The seller asks the firm to pay £10,000 of the proceeds to their child’s school for fees due next month, and the balance to the seller. May the firm do this from the client account?

Answer:

No. The payment to the school is not connected to the legal services provided. Making the payment would treat the client account as a banking facility and would breach the prohibition. The firm should return the proceeds to the client promptly so the client can make their own payment.

Worked Example 1.4

A firm receives a client cheque for £5,000 on account. Relying on it, the firm pays a £2,000 expert fee the same day. The cheque then bounces. What must the firm do?

Answer:

The client account has been used to pay a third party when insufficient cleared funds were held for that client. The firm must immediately replace the shortfall from its business account to remedy the breach and then seek reimbursement from the client.

Returning Client Money

Client money must be returned to the client promptly when there is no longer any proper reason to hold it. Where a related transaction has concluded, prompt distribution is expected. Client money should not be retained “just in case” or for the client’s convenience.

Where the client cannot be traced or the firm cannot obtain instructions, the firm should take reasonable steps to locate the client and return the funds. If still unsuccessful, current SRA provisions allow firms to pay residual client balances of £500 or less to a charity without prior SRA authorisation, subject to appropriate checks, records, and the firm providing an indemnity to the charity. For balances above £500, written authorisation from the SRA is required before withdrawal. Detailed records of the steps taken must be retained.

Worked Example 1.5

A firm concludes a matter leaving £275 on the client ledger. After reasonable attempts over several months, the client cannot be found. What can the firm do?

Answer:

The firm may pay the residual balance of £275 to a suitable charity without prior SRA approval, provided it documents the tracing steps taken, records the payment, and obtains an appropriate charity indemnity against later claims.

Record Keeping and Compliance

Firms must keep detailed, up-to-date records of all client money received, held, and paid out. This includes:

- Separate ledgers for each client and matter, showing business and client sides where appropriate

- Regular reconciliation of client account balances with bank statements at least every five weeks, with differences investigated and resolved promptly

- Obtaining statements for all client and business accounts at least every five weeks

- A central record of all bills and written notifications of costs

- Retention of accounting records for at least six years

A Compliance Officer for Finance and Administration (COFA) is responsible for ensuring compliance with the SRA Accounts Rules.

Key Term: Compliance Officer for Finance and Administration (COFA)

A senior individual in a law firm responsible for ensuring compliance with the SRA Accounts Rules and reporting material breaches to the SRA.

Where a firm holds or receives client money during an accounting period (or operates a joint account or a client’s own account as signatory), it must obtain an accountant’s report for that period. This report must be delivered to the SRA if it is qualified to show a failure to comply with the rules that places client money at risk. Limited exceptions apply (e.g., very low balances or where all client money is LAA funds), but the firm should be ready to demonstrate its systems and controls comply fully.

Prompt remediation is essential. If client money has been wrongly paid into the business account, it must be transferred immediately to the client account on discovery. If client money has been wrongly withdrawn, the firm must promptly replace the funds—usually from the business account—pending rectification.

Interest on Client Money

Firms must account to clients for a fair sum of interest on money held in a client account, unless a different arrangement is agreed in writing. The amount of interest depends on the amount held, the period, and the firm’s policy.

Key Term: interest policy

The firm's written policy explaining how it calculates and pays interest on client money, which must be fair and communicated to clients.

A typical policy addresses:

- when interest will be paid (often at the end of the matter)

- the rate or method of calculation

- any de minimis provisions (e.g., no interest if the amount calculated is below a small threshold)

- separate designated deposit client accounts: where used, all bank interest arising on those accounts is credited for the client’s benefit

Where client money is held in a general client account, the firm may keep any interest the bank pays on that account beyond the fair sums paid to clients. Where a separate designated account is used for a client, interest paid by the bank should be accounted to that client in full. Firms should explain these arrangements clearly at the outset, ensure fairness, and keep appropriate records. Any interest payable can be sent directly to the client, credited to their account, or (with agreement) offset against amounts due to the firm.

Worked Example 1.6

A firm holds £300,000 for eight weeks for a corporate client. It agrees in writing to place the funds in a separate designated deposit client account earning a higher rate. How should interest be treated?

Answer:

Interest earned on the separate designated account belongs to the client and should be accounted to the client in full. The firm should record the deposit and interest receipt on the client ledgers and pay or credit the interest in accordance with its policy and the client’s instructions.

Mixed Receipts

If a payment includes both client money and business money (e.g., a single cheque for fees and completion funds), the firm must allocate the funds promptly to the correct accounts. Usually, the whole amount is paid into the client account, and the business money is transferred to the business account as soon as possible. Alternatively, if paid first into the business account (for example due to online instructions supplied), the client element must be transferred immediately to the client account. The key is “prompt allocation” and accurate recording.

Worked Example 1.7

A client sends a cheque for £1,200: £1,000 for completion of a purchase (client money) and £200 for billed fees (business money). How should the firm handle this?

Answer:

The cheque should be paid into the client account. The £200 for fees must be transferred promptly to the business account, leaving only client money in the client account.

Worked Example 1.8

A client makes a bank transfer of £5,400 which lands in the business account in error. It includes £5,000 net sale proceeds and £400 to settle a billed fee. What should be done?

Answer:

Promptly transfer £5,000 from the business account to the client account (to correct the mis-posting) and retain £400 in the business account for the billed fee. Record the transfers and ensure both ledgers reflect the correct allocation.

Key Point Checklist

This article has covered the following key knowledge points:

- Client money is any money held or received by a solicitor on behalf of a client, third party, or as a trustee, or for unpaid fees/disbursements before a bill is delivered.

- Client money must be kept separate from business money and paid promptly into a client account.

- Client accounts must be held at a bank or building society in England or Wales and include the word "client" in the account name.

- Client money in a client account should be available on demand unless an alternative written agreement provides otherwise.

- There are different types of client accounts: general, separate designated, and joint accounts.

- Withdrawals from client accounts are strictly limited to proper purposes and must never be used as a banking facility.

- Client money can only be withdrawn if sufficient funds are held for that specific client or third party; client ledgers must not be overdrawn.

- Firms must keep accurate records for each client, obtain statements and reconcile client accounts at least every five weeks, and retain records for at least six years.

- An accountant’s report is required where client money is held/received or joint/client’s own accounts are operated as signatory; qualified reports must be delivered to the SRA.

- Interest must be paid to clients on money held, according to a fair written policy; de minimis thresholds and separate designated accounts should be applied fairly.

- Client money must be returned promptly when there is no longer a proper reason to hold it; residual balances under £500 may be paid to charity subject to conditions, larger amounts require SRA authorisation.

- Mixed receipts must be allocated promptly to the correct accounts, and any mis-posted funds must be corrected immediately.

- Payments from the Legal Aid Agency for the firm’s costs can be paid into the business account.

- Breaches (e.g., bounced cheques, wrong postings) must be remedied immediately, usually by transferring money from the business account to the client account to make up any shortfall.

Key Terms and Concepts

- client money

- business money

- disbursement

- segregation

- client account

- general client account

- separate designated client account

- joint account

- Compliance Officer for Finance and Administration (COFA)

- interest policy