Learning Outcomes

This article explains the specific accounting procedures and regulatory requirements for joint accounts, client's own accounts operated by solicitors, and third-party managed accounts (TPMAs). After reading this article, you will understand the key SRA Accounts Rules applicable to these special account types, the solicitor's duties regarding record-keeping and safeguarding money, and the distinctions between these accounts and standard client accounts. This knowledge will enable you to apply the relevant principles to SQE1-style multiple-choice questions concerning these specific account management scenarios. In particular, you will be able to identify when money in each arrangement is “client money,” determine which parts of the SRA Accounts Rules 2019 apply (including Rule 8 record-keeping, Rules 9–11 on special accounts, and Rule 12 on accountants’ reports), set up appropriate controls (statements and reconciliations at least every five weeks, central records of bills), and recognise when to notify or seek guidance from the SRA. You will also be able to evaluate when a TPMA is appropriate, what must be explained to clients before use, and how to monitor TPMA statements alongside internal records.

SQE1 Syllabus

For SQE1, you are required to understand the practical application of the SRA Accounts Rules 2019 to specific types of accounts beyond the standard client and business accounts, with a focus on the following syllabus points:

- The operation of joint accounts under Rule 9, including record-keeping requirements.

- The operation of a client’s own account as signatory under Rule 10, including the limited application of the Rules and record-keeping duties.

- The use and implications of third-party managed accounts (TPMAs) under Rule 11, including the solicitor's obligations to the client and the SRA.

- Distinguishing the accounting treatment and regulatory oversight applicable to joint accounts, client’s own accounts, and TPMAs compared to standard client accounts.

- Understanding the solicitor's overarching duty to safeguard client money and assets, irrespective of the account type used.

- Recognising the obligation to obtain an accountant’s report where client money is held or received, or where joint accounts or clients’ own accounts are operated (Rule 12), and the exemptions for low-risk balances.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which part of the SRA Accounts Rules 2019 primarily governs the operation of joint accounts by solicitors?

- a) Rule 5

- b) Rule 8

- c) Rule 9

- d) Rule 11

-

A solicitor operates a client's personal bank account as a signatory under a Lasting Power of Attorney. Which SRA Accounts Rule specifically addresses the requirements for this scenario?

- a) Rule 7

- b) Rule 10

- c) Rule 11

- d) Rule 13

-

True or False: Money held in a Third-Party Managed Account (TPMA) is considered client money under the SRA Accounts Rules 2019.

-

Which of the following is generally NOT a requirement under the SRA Accounts Rules when a solicitor operates a client's own account as signatory?

- a) Obtaining bank statements every five weeks.

- b) Performing account reconciliations every five weeks.

- c) Paying client money promptly into a client account operated by the firm.

- d) Keeping a central record of bills relating to the account.

Introduction

While most client money is handled through a firm's dedicated client bank account, solicitors sometimes encounter situations requiring different account management approaches. The SRA Accounts Rules 2019 provide specific, albeit limited, requirements for scenarios where solicitors operate joint accounts, act as signatories on a client’s own personal bank account, or where firms utilise third-party managed accounts (TPMAs). Understanding these variations is essential for compliance and protecting client interests. This article examines the rules and practicalities associated with these special account types.

Joint accounts, client's own accounts and TPMAs are set out with the applicable SRA rule and the solicitor's principal accounting duties.

The general prohibition against using client accounts to provide banking facilities to clients or third parties applies across the piece. Payments into and out of any account used must relate to the delivery of regulated services: using a firm’s client account, or any arrangement connected with the firm, as a general conduit for funds (without a proper transaction link) risks breach of the Accounts Rules and the SRA Principles. In practice, this means ensuring any joint account, client’s own account operation, or TPMA is driven by a legitimate substantive legal matter or specified appointment and is supported by appropriate records and internal controls.

Obtaining periodic statements at least every five weeks and keeping accurate, contemporaneous and chronological records are central expectations within Rule 8. For joint accounts and clients’ own accounts, Rules 9 and 10 respectively disapply most of the detailed client account requirements but selectively import elements of Rule 8 (statements, reconciliations, and central records of bills) to ensure adequate oversight. Rule 11 sets the parameters for TPMA use, emphasising clear client understanding and robust due diligence on the provider. Separately, Rule 12 requires an accountant’s report to be obtained for any accounting period in which client money is held or received, or where joint accounts or clients’ own accounts are operated; only low-risk balances meeting specified thresholds may be exempt.

Key Term: joint account

An account held at a bank or building society in the names of two or more parties, one of whom is the solicitor or firm, used to hold money relating to a client matter or trust. Key Term: client's own account

A client's personal bank or building society account for which a solicitor or firm employee has authority to operate as a signatory, often under a power of attorney or deputyship. Key Term: third-party managed account (TPMA)

An account held with an authorised payment institution, regulated by the Financial Conduct Authority (FCA), which holds money for clients involved in transactions handled by a law firm. The law firm does not hold the money itself.Test Tip: In SQE-style questions on Accounting procedures for special account types, identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

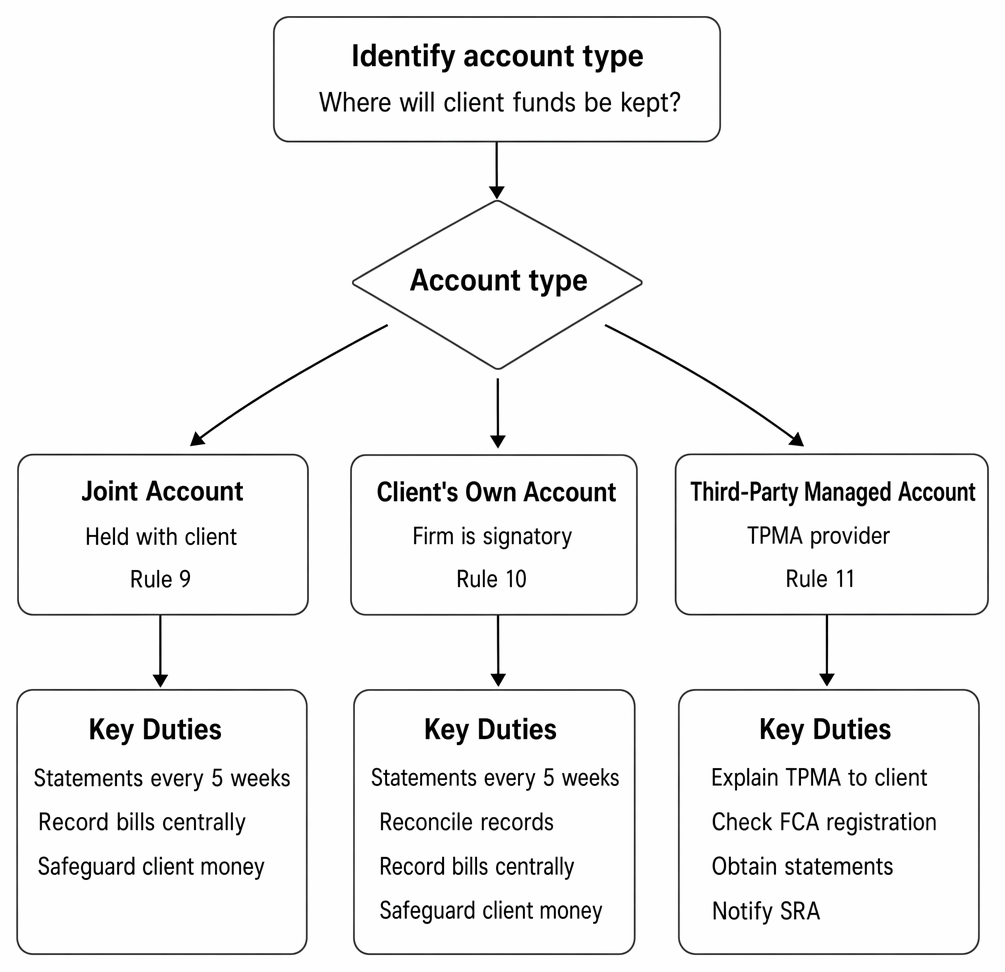

Joint Accounts

A joint account, in the context of solicitors' accounts, is an account held at a bank or building society in the joint names of the solicitor/firm and a client or other third party. A typical example is where a solicitor acts as an executor of an estate alongside a lay executor, and they decide to manage the estate funds through a joint bank account.

Since the account is not solely in the name of the firm, it is not a 'client account' as defined by the main Rules. Consequently, most of the detailed requirements in Part 2 of the Rules (e.g., relating to withdrawals, immediate availability) do not apply directly.

However, Rule 9 specifies that certain obligations do still apply:

- Rule 8.2: The firm must obtain bank statements for the joint account at least every five weeks.

- Rule 8.4: The firm must keep a central record of bills or written notifications of costs relating to the matter associated with the joint account.

- The SRA retains powers to require firms to produce documents and information for inspection under the regulatory arrangements. Firms must be able to supply records demonstrating compliance upon request.

Although not explicitly covered by the main client account rules, the overarching SRA Principles, particularly the duty to safeguard client money and assets, remain essential. Firms should implement safeguards, such as requiring joint signatures for withdrawals, to mitigate the risks associated with joint control. In addition, where funds held in a joint account are client money (as they generally will be), the firm should ensure the existence of a clear audit trail for all receipts and payments. Operationally, firms should:

- Obtain and review statements at least every five weeks, ensuring narrative entries tie to the substantive legal matter.

- Maintain centrally accessible records of all bills or written notifications of costs relating to the matter.

- Put in place mandate controls, for example, joint signatory requirements or transaction limits, proportionate to the risks.

- Ensure the arrangement is appropriate for the client’s best interests and not used as a substitute for a proper firm client account where that would be more suitable.

Rule 12 on accountants’ reports also has practical relevance. If, during an accounting period, a firm holds or receives client money or operates a joint account, the firm must obtain an accountant’s report within six months of the period end unless exempt for low balances. The report may need to be delivered to the SRA if it is qualified (i.e., the accountant identifies a risk to client money).

Worked Example 1.1

A solicitor, Priya, is acting as a joint trustee for a family trust alongside the settlor's son, David. They open a joint bank account in both their names to hold trust funds. Priya's firm does not handle any other trust money through this account.

What are Priya's firm's minimum obligations under the SRA Accounts Rules regarding this joint account?

Answer:

Under Rule 9, Priya's firm must ensure it obtains bank statements for the joint account at least every five weeks (Rule 8.2) and keeps a central record of any bills raised concerning the trust administration (Rule 8.4). While other client account rules don't strictly apply, Priya must still comply with the SRA Principles, including safeguarding the trust assets.

Worked Example 1.2

A solicitor opens a joint account with a lay executor to administer an estate. The firm’s review identifies that statements have not been obtained for nearly two months due to a bank delay. What should the firm do to remain compliant?

Answer:

The firm should immediately obtain the latest available statements and put in place steps to avoid recurrence (e.g., online statement access, diarised reminders). It should document the reasons for the delay, record the remedial actions taken, and ensure a central record of any bills is up to date. The regular five‑weekly statement expectation under Rule 8.2 applies; prompt corrective action and records showing money is safeguarded will help demonstrate compliance.

Operating a Client’s Own Account

Solicitors may sometimes operate a client's personal bank or building society account as a signatory. This typically occurs when acting under a Lasting Power of Attorney (LPA) for property and financial affairs or as a court-appointed Deputy for someone lacking mental capacity.

As the account is in the client's name, the money within it is not 'held or received' by the firm in the same way as money in a client account. Therefore, it is not technically 'client money' subject to the full SRA Accounts Rules.

Rule 10 outlines the specific, limited requirements that apply in this situation:

- Rule 8.2: Obtain bank statements at least every five weeks.

- Rule 8.3: Perform reconciliations between the statements and the firm's records of transactions made on the account, at least every five weeks. The reconciliation record should be signed off by a manager or the COFA as part of the firm’s systems and controls.

- Rule 8.4: Keep a central record of bills relating to the work done in operating the account (or other written notifications of costs).

- Rule 30 (records for clients’ own accounts): Specific record-keeping duties apply, including retaining statements/passbooks (or duplicate statements) for at least six years from the last entry. Maintain either a central register of all clients’ own accounts operated or keep records centrally.

These obligations reflect the unique position of operating a client’s own money directly. Firms need to maintain clear internal records of instructions, payments to third parties, and any fees charged for management of the account. The SRA acknowledges that obtaining statements and performing reconciliations every five weeks might be impractical in some deputyship or attorney situations (for example, where a bank cannot provide timely statements or there are temporary mandate restrictions). Where that occurs, the firm should take reasonable steps to ensure the money is safe (e.g., interim records, transaction logs, confirmations from the bank) and document those steps, alongside prompt remedial action.

Operational points to consider:

- Keep written authority (e.g., LPA or court order), the scope of powers, and any restrictions readily accessible and aligned to the account mandates.

- Separate routine bill payments from discretionary decisions, recording the basis of decisions taken in the client’s best interests.

- Keep the firm’s costs records separate and maintain the central record under Rule 8.4.

- Avoid using the client’s own account as a general banking facility beyond legitimate needs for the appointment—payments must be tied to the proper management of the client’s affairs.

Rule 12 applies here too. If the firm operates a client’s own account as signatory during an accounting period, the firm must obtain an accountant’s report within six months of the period end unless eligible for exemption due to low balances. Where client money is not held in the firm’s client account, many detailed Rule 8 client account controls do not apply; however, the firm must still demonstrate adequate systems and oversight for clients’ own accounts.

Exam Warning: Do not confuse operating a client's own account with holding client money in the firm's client account. The full SRA Accounts Rules do not apply to the former, only the specific requirements outlined in Rule 10. Money in the client's own account belongs entirely to the client.

Worked Example 1.3

A solicitor is appointed as deputy for a person lacking capacity. The deputyship account is operated by the solicitor’s team. During a busy period, the five‑week reconciliation is missed by nine days, though all transactions are properly recorded and the account remains in credit. How should the firm respond?

Answer:

The firm should complete the reconciliation immediately, sign it off, investigate the cause of delay, and document remedial steps (e.g., scheduling, cover arrangements, and online statement access). While the Rules expect reconciliations at least every five weeks (Rule 8.3), the SRA accepts occasional slippage where reasonable steps have been taken to safeguard the money and the firm promptly rectifies the issue and records it. The central record of bills (Rule 8.4) and retention of statements/passbooks (Rule 30) should be up to date.

Third-Party Managed Accounts (TPMAs)

Some firms may choose not to operate their own client accounts, instead using a TPMA provider. Rule 11 permits this arrangement.

Money held in a TPMA is not client money under the SRA Accounts Rules because it is held by the TPMA provider, not the law firm. Therefore, the main body of the Accounts Rules does not apply to funds within the TPMA. However, firms using TPMAs have specific obligations under Rule 11 and the SRA Principles:

- Rule 11.1(a): The firm must not receive or hold the client's money itself for matters handled via the TPMA.

- Rule 11.1(b): The firm must take reasonable steps to ensure the client understands the TPMA arrangements, including fees, who bears them, and the client's right to terminate the agreement or dispute payments. This must be explained before accepting instructions.

- Rule 11.2: The firm must obtain regular statements from the TPMA provider and ensure they accurately reflect all transactions. Internal records should allow cross-checking against provider statements to show that funds are being managed according to instructions.

- Due diligence: The firm must ensure the TPMA provider is appropriately regulated by the FCA (authorised or small payment institution) and has safeguarding arrangements for client funds. Firms should assess how money is safeguarded and what protections apply (note that TPMA funds may not benefit from deposit guarantee schemes applicable to banks; safeguarding rules under payment services regulation are designed to protect customer funds).

- Best interests & safeguarding: The firm must be satisfied that using a TPMA is appropriate for the client and that the client's money will be safe, having regard to Principle 7 (act in the client’s best interests) and the duty to safeguard money and assets.

- SRA notification: Firms must notify the SRA when they start using a TPMA provider, giving details of the provider and their FCA authorisation number, and keep that notification up to date.

Using a TPMA can reduce a firm's administrative burden and potentially lower risk, as the handling of client money is managed externally. However, the firm retains responsibility for ensuring the arrangement is suitable and properly explained to the client. Considerations when deciding to use a TPMA:

- Whether the firm’s client account would be preferable (for example, where the firm already has robust systems and controls and the matter is straightforward).

- Whether the TPMA’s terms appropriately deal with interest, fees, dispute mechanisms, and termination rights.

- How quickly statements can be obtained and whether they provide sufficient detail for oversight.

- The firm’s internal records—while the TPMA holds the money, the firm should maintain records matching the TPMA statements to the matter ledger or equivalent.

Where a firm uses a TPMA for a matter, it must still comply with other regulatory requirements, including anti-money laundering duties and acting with integrity. If client circumstances change and a TPMA ceases to be suitable, the firm should inform the client and agree how funds should be managed going forward, which may include transitioning to a firm client account or another provider.

Worked Example 1.4

A firm specialising in low-volume conveyancing decides to use a TPMA to handle client funds instead of operating its own client account. Before taking on a new purchase matter for Mr Jones, the solicitor explains the TPMA system.

What key information must the solicitor ensure Mr Jones understands before proceeding?

Answer:

The solicitor must take reasonable steps to ensure Mr Jones understands (i) the contractual terms, including who pays any TPMA fees, and (ii) his right to end the TPMA agreement or dispute payment requests made by the firm via the TPMA (Rule 11.1(b)). The solicitor should also explain that the regulatory protections differ from those applying to money held in a firm's own client account.

Worked Example 1.5

A firm using a TPMA provider for a corporate transaction notices discrepancies between its internal records and the TPMA statements. The latest statement is delayed and shows an unexpected fee deduction. What should the firm do?

Answer:

The firm should promptly obtain an updated TPMA statement, reconcile it with internal records, and query any discrepancies with the provider. It should confirm the fee basis with the client and the TPMA contract, ensure the client understands any deductions, and document all steps taken. If issues persist, the firm should consider whether the TPMA remains appropriate, and inform the SRA if there is a material concern about safeguarding or provider reliability. The firm must ensure statements are obtained regularly (Rule 11.2) and maintain records evidencing accurate oversight.

Summary

| Feature | Joint Account (Rule 9) | Client's Own Account (Rule 10) | TPMA (Rule 11) |

|---|---|---|---|

| Account Holder(s) | Firm/Solicitor + Client/Third Party | Client | TPMA Provider (FCA Regulated) |

| Is it 'Client Money'? | Yes | No (not held by firm) | No (not held by firm) |

| Is it a 'Client Account'? | No | No | No |

| Main Applicable Rules | Rule 9 (referencing parts of Rule 8) | Rule 10 (referencing parts of Rule 8 & Rule 30) | Rule 11 |

| Key Firm Duties | Obtain statements (8.2), Record bills (8.4) | Obtain statements (8.2), Reconcile (8.3), Record bills (8.4), Record keeping (30) | Inform client (11.1b), Check provider, Obtain statements (11.2), Notify SRA |

| SRA Principles Apply? | Yes (esp. Safeguarding) | Yes (esp. Safeguarding) | Yes (esp. Safeguarding, Client's Best Interests) |

Beyond these core features, remember Rule 12 on accountants’ reports: if client money is held or received during an accounting period, or if the firm operates a joint account or a client’s own account as signatory, an accountant’s report must be obtained within six months of the end of the period (subject to exemptions for small average and maximum balances).

Key Point Checklist

This article has covered the following key knowledge points:

- Joint accounts are held by the firm/solicitor with another party; they are not client accounts, but specific rules (Rule 9) regarding statements and records of bills apply.

- Operating a client's own account as signatory (e.g., under an LPA or Deputyship) means the money is not held by the firm. Specific rules (Rule 10) apply regarding statements, reconciliation, and bills, and records must be retained centrally or in a central register.

- Third-Party Managed Accounts (TPMAs) involve an FCA-regulated provider holding funds. The money is not client money under the SRA Rules. Rule 11 requires client understanding, provider checks, and SRA notification, and firms must obtain regular statements from the TPMA.

- The overarching SRA Principles, especially safeguarding client assets and acting in the client’s best interests, apply regardless of the account type. Do not use client accounts or special arrangements as general banking facilities.

- Firms must maintain appropriate systems and controls for all account types they operate or interact with, including obtaining statements at least every five weeks, performing reconciliations where required, and keeping a central record of bills.

- Under Rule 12, obtain an accountant’s report for any accounting period in which client money is held or received, or a joint account or client’s own account is operated, unless an exemption applies for low balances.

Key Terms and Concepts

- joint account

- client's own account

- third-party managed account (TPMA)