Learning Outcomes

This article explains how joint accounts operate where a solicitor or firm holds or receives money jointly with a client or other third party, and delineates the precise regulatory framework that applies under the SRA Accounts Rules 2019. It explains the limited operation of Part 2 in this context, anchored in Rule 9.1, and identifies exactly which elements of Rule 8 still bite on joint accounts, namely the mandatory requirements to obtain bank or building society statements at least every five weeks (Rule 8.2) and to keep a readily accessible central record of bills or written notifications of costs (Rule 8.4). It distinguishes joint accounts from both standard client accounts and a client’s own account operated by the solicitor under Rule 10, emphasising the differing reconciliation and record-keeping obligations. It highlights typical risk scenarios, governance controls, and professional duties that continue to apply, including safeguards to prevent misuse of estate or trust funds. It also illustrates how exam questions may test these distinctions, enabling you to analyse SQE1-style MCQs and mini-scenarios accurately and to select the option that reflects the correct rule framework and ethical response.

SQE1 Syllabus

For SQE1, you are required to understand the operation of joint accounts under the SRA Accounts Rules 2019, with a focus on the following syllabus points:

-

Identify the definition and nature of a joint account involving a solicitor/firm and a client or third party.

-

Explain Rule 9.1 SRA Accounts Rules 2019: limited application of Part 2 to joint accounts.

-

State precisely which Rule 8 requirements apply to joint accounts:

- Rule 8.2: obtaining bank/building society statements at least every five weeks.

- Rule 8.4: keeping a readily accessible central record of bills or written notifications of costs.

-

Contrast joint accounts (Rule 9) with:

- Client accounts held solely by the firm (full Part 2 applies).

- A client’s own account operated by the solicitor (Rule 10 applies—including statements and reconciliations).

-

Recognise professional duties that still apply (SRA Principles and Code of Conduct) and practical risk controls (mandates, dual signatures, documentation of purpose) for safe operation.

-

Understand that money in a joint account is still client money, even though most of Part 2 does not apply.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Under SRA Accounts Rules 2019, Rule 9, which specific Rule 8 requirement applies to money held in a joint account?

- a) Rule 8.1 (Separate client ledgers and cash book)

- b) Rule 8.2 (Obtaining bank/building society statements at least every five weeks)

- c) Rule 8.3 (Reconciliations at least every five weeks)

- d) Rule 5.1 (Circumstances for withdrawal from client account)

-

A solicitor holds money in a joint account with an executor client. Which SRA Accounts Rules 2019 requirement regarding records specifically applies to this joint account?

- a) Rule 8.4 (Central record of bills or written notifications of costs)

- b) Rule 7.1 (Accounting for interest)

- c) Rule 3.3 (Prohibition on providing banking facilities)

- d) Rule 5.3 (Sufficient funds for withdrawal)

-

True or false? Money held in a joint account operated by a solicitor and a client is not considered client money under the SRA Accounts Rules 2019.

-

A firm operates a joint account with a client (as co-executor) and is asked to transfer funds to settle the firm’s outstanding fees for an unrelated matter for the same client. Which obligation is most relevant to consider?

- a) Rule 9.1 (Limited application of Part 2 to joint accounts) and the general duty to safeguard client money (Code of Conduct para 4.2)

- b) Rule 3.3 (Prohibition on providing banking facilities)

- c) Rule 5.1 (Circumstances for withdrawal from client account)

- d) Rule 7.1 (Payment of interest)

Introduction

Solicitors and firms may sometimes hold or receive money jointly with a client or another third party. Commonly this arises where a solicitor is appointed as a co-executor of an estate or as a co-trustee alongside a lay person. In such cases, a bank or building society account used for the related monies may be opened in joint names. This is a joint account and differs from the firm’s general client account or separate designated client accounts.

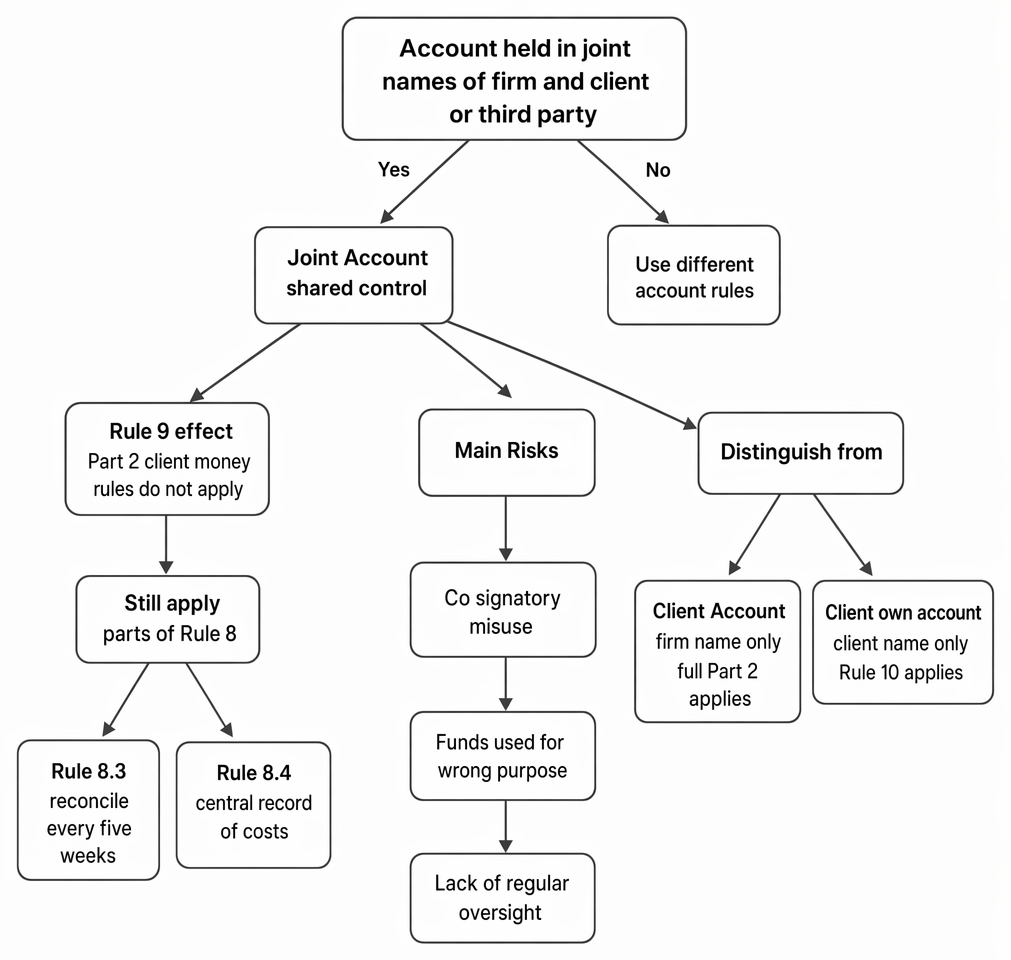

Joint accounts in joint names of firm and client or third party fall within Rule 9, with residual Rule 8 duties.

Joint accounts sit within a modified regulatory framework. The SRA Accounts Rules 2019 recognise that the firm does not have sole control over the funds and, therefore, most of Part 2 (client money and client accounts) is disapplied. Nevertheless, certain financial control and record-keeping obligations still apply. Understanding precisely what applies, and what does not, is essential for compliance and for correctly answering SQE1 MCQs.

Key Term: Joint Account

A bank or building society account held in the joint names of a solicitor/firm and a client or third party (such as a co-executor or co-trustee), used to hold money related to a specific matter (e.g. an estate or trust) where control is shared.

Rule 9: Limited Application of Part 2

Rule 9.1 of the SRA Accounts Rules 2019 provides that Part 2 (client money and client accounts) generally does not apply to money held or received in a joint account. This reflects the shared control and the practicalities of operating an account that is not in the firm’s sole name. The usual client account rules—for example, deposits into client account, withdrawals, and reconciliations—are drafted for accounts controlled by the firm alone and hence are not normally suitable where the firm is only one of the joint signatories.

However, Rule 9.1 requires compliance with specified elements of Rule 8 (client accounting systems and records) to ensure there is still adequate oversight and transparency. The firm remains subject to the SRA Principles and the SRA Code of Conduct, including the obligation to safeguard money and assets entrusted by clients and others. In short: while the heavy machinery of the client account rules is switched off for joint accounts, targeted controls remain on.

Applicable Requirements under Rule 8

Under Rule 9.1, the following requirements apply to a joint account:

-

Rule 8.2 (Obtaining bank/building society statements)

- You must obtain statements for the joint account at least every five weeks. This supports ongoing oversight where control is shared and ensures that transactions and balances can be checked against the solicitor’s own records and the matter’s records (e.g., estate accounts, trust records).

-

Rule 8.4 (Central record of bills)

- You must keep a readily accessible central record of all bills or other written notifications of costs relating to work done on the matter connected to the joint account. This contributes to transparency about the firm’s charges and supports accountability to beneficiaries or other interested parties.

Notably, Rule 8.3 (five-weekly reconciliations) does not apply to joint accounts under Rule 9.1. Reconciliations are a requirement for accounts controlled by the firm (e.g., general client account or a client’s own account under Rule 10), but joint accounts are carved out from this obligation. That said, as a matter of good practice, firms often perform regular internal checks by comparing joint account statements to their matter records.

Key Term: Rule 9 (Joint accounts)

The SRA Accounts Rule that disapplies most of Part 2 to money held or received jointly with clients or third parties, while still requiring compliance with Rule 8.2 (statements) and Rule 8.4 (central record of bills). Key Term: Bank/building society statements (Rule 8.2)

Statements for the joint account must be obtained at least every five weeks to maintain oversight of activity and balances. Key Term: Central record of bills (Rule 8.4)

A single, accessible record of bills or written notifications of costs for the matter connected to the joint account, supporting transparency and auditability.

Worked Example 1.1

A solicitor, acting as co-executor with the deceased's daughter, manages an estate via a joint bank account in both their names. The daughter instructs the solicitor to pay a personal debt of hers directly from the joint estate account. The will contains no authority for such a payment.

Answer:

No. The funds belong to the estate and must be used for proper administration purposes (e.g., paying estate debts and expenses, and distributing to beneficiaries). Paying the daughter’s personal debt would misuse estate funds and breach fiduciary duties, regardless of the limited application of Part 2 to the joint account. The solicitor must refuse the instruction and explain the correct use of the estate funds.

Worked Example 1.2

A firm is joint signatory to an account with a lay co-trustee for a family trust. The co-trustee prefers to manage statements and only forwards summaries sporadically. The firm does not receive full bank statements regularly.

Answer:

The firm must obtain bank/building society statements for the joint account at least every five weeks (Rule 8.2). Where the other signatory holds original statements, the firm should arrange provision of duplicate statements or copies sufficient to comply. The firm should confirm this arrangement in writing and maintain the statements in its records.

Worked Example 1.3

A solicitor is asked to move funds from a joint executor account to pay the firm’s outstanding fees on a different, unrelated matter for the same client. There is no bill or written notification of costs relating to the estate matter authorising such a payment.

Answer:

The solicitor should not do this. Using estate funds for an unrelated matter is improper and may breach fiduciary duties and the duty to safeguard client money (Code of Conduct para 4.2). Rule 9.1 reminds the firm that the joint account sits outside the usual client account regime, but it does not grant carte blanche to repurpose the funds. The firm must ensure a bill or written notification of costs exists for the estate matter and only pay appropriate estate costs from the estate account.

Practical Operation and Risks

Operating a joint account involves shared control and therefore presents unique practical risks and compliance obligations:

-

Control and mandate

- Agree, document, and maintain clear operating mandates (e.g., dual signatures for significant withdrawals). Written protocols should specify the purpose of the account, who can authorise transactions, and how statements and records are shared.

-

Oversight via statements

- Obtain bank/building society statements at least every five weeks (Rule 8.2). This is mandatory and underpins oversight. Where the other signatory handles the account day-to-day, ensure duplicates or copies are provided to the firm on the required schedule.

-

Recording costs

- Maintain a central record of bills and written notifications of costs (Rule 8.4) for the matter linked to the joint account. This enables transparency and supports estate/trust accounting.

-

Use limited to the proper purpose

- Funds must be used for the proper purpose of the matter. Although Rule 3.3 (prohibition on providing banking facilities) relates to client accounts rather than joint accounts, the professional obligation to safeguard client money and use it only for legitimate case-related purposes applies. Payments benefitting a lay co-signatory personally, or unrelated firm fees, are improper.

-

Distinguish correctly

- Do not confuse a joint account with:

- The firm’s general client account or separate designated client accounts: full Part 2 applies.

- A client’s own bank account operated by the solicitor (Rule 10): statements and reconciliations apply, and additional specific duties arise.

- Do not confuse a joint account with:

-

Records retention and audit trail

- Keep statements, mandates, and expense records in an accessible form. Although full reconciliation under Rule 8.3 is not required for joint accounts, periodic internal checks comparing statements to matter records are prudent to detect anomalies.

-

Professional duties

- SRA Principles and Code of Conduct apply, including acting in best interests, safeguarding client money and assets, accounting properly for monies, and keeping records clear and complete. Where concerns arise (e.g., withdrawals without proper purpose), escalate promptly and take corrective action.

Exam Warning: Do not confuse a joint account (Rule 9) with a client’s own account operated by the solicitor (Rule 10).

-

Joint account (Rule 9): Part 2 generally does not apply. Rule 8.2 (statements) and Rule 8.4 (central record of bills) do apply. Rule 8.3 (reconciliations) does not apply.

-

Client’s own account (Rule 10): You must comply with Rule 8.2 (statements), Rule 8.3 (reconciliations), and Rule 8.4 (central record of bills). Further, you are operating the client’s account as signatory and must safeguard funds accordingly.

Revision Tip: Focus on the exceptions in Rule 9.1. Memorise which Rule 8 requirements apply to joint accounts:

- Rule 8.2 (obtain statements at least every five weeks).

- Rule 8.4 (keep a central record of bills).

Recognise that money in a joint account is client money, but most of Part 2 does not apply due to shared control. Expect MCQs to probe this distinction and the correct application of Rule 8.2 and 8.4.

Key Point Checklist

This article has covered the following key knowledge points:

-

Joint accounts are bank/building society accounts held in the joint names of a solicitor/firm and a client or third party, used for specific matters (e.g., an estate or trust).

-

Under SRA Accounts Rules 2019, Part 2 generally does not apply to money in joint accounts (Rule 9.1).

-

The firm must still:

- Obtain bank/building society statements at least every five weeks (Rule 8.2).

- Keep a readily accessible central record of bills or written notifications of costs (Rule 8.4).

-

Rule 8.3 (five-weekly reconciliations) does not apply to joint accounts under Rule 9.1.

-

Professional duties still apply: act in the best interests of the client, safeguard money and assets, and ensure proper use of funds for the matter’s purpose.

-

Distinguish a joint account (Rule 9) from:

- A client account (full Part 2 applies).

- A client’s own account operated by the solicitor (Rule 10 applies, including statements and reconciliations).

-

Document mandates, require dual signatures where appropriate, and maintain clear records to mitigate risks in shared control.

Key Terms and Concepts

- Joint Account

- Rule 9 (Joint accounts)

- Bank/building society statements (Rule 8.2)

- Central record of bills (Rule 8.4)