Learning Outcomes

This article outlines the specific rules and practical implications surrounding the use of joint accounts, client’s own accounts, and third-party managed accounts (TPMAs) within legal practice, including:

- Limited application of the SRA Accounts Rules to these account types and the solicitor’s ongoing responsibilities

- Differences between client money in a firm’s client account and money held via joint accounts, client’s own accounts, or TPMAs, and applicable SRA Accounts Rules 2019 in each case

- Client money status of funds in joint accounts and minimum record‑keeping and safeguard requirements

- Requirements when operating a client’s own account (statements, reconciliations, central record of bills) and approaches where five‑week cycles are impracticable

- Appropriateness of TPMAs, including provider due diligence, client understanding and informed consent, statement‑checking requirements, and SRA notification on first use

- Avoidance of improper use of alternative arrangements as banking facilities unconnected to regulated legal services

- Triggers for accountants’ reports and record‑retention obligations when operating joint accounts or client’s own accounts during an accounting period

- Interest arrangements and how they differ when funds are held in a firm’s client account, a TPMA, or a client’s own account

SQE1 Syllabus

For SQE1, you are required to have a working knowledge of how client money is handled outside the firm's main client account. This includes understanding the specific provisions under the SRA Accounts Rules 2019 (the Rules) relating to joint accounts and third-party managed accounts. You will need to be able to identify the circumstances in which these accounts might be used and the different compliance obligations compared to standard client accounts, with a focus on the following syllabus points:

- the definition and operation of joint accounts under Rule 9

- the requirements when operating a client’s own account as signatory under Rule 10

- the requirements for using third-party managed accounts (TPMAs) under Rule 11

- the limited application of the main SRA Accounts Rules to these types of accounts

- the solicitor's continuing duty to safeguard client money and act in the client's best interests even when using these alternative accounts

- the need to obtain bank statements and keep a central record of bills for joint accounts (Rule 8.2 and 8.4 applied through Rule 9), and to obtain statements and reconcile at least every five weeks for a client’s own account (Rule 10 with Rule 8.2 and 8.3)

- the obligation to notify the SRA when first using a TPMA and to obtain regular statements from the provider (Rule 11.2), coupled with rigorous due diligence on the provider’s FCA status

- the prohibition on providing banking facilities (Rule 3.3) and its impact on decisions to retain or route funds via alternative arrangements

- the retention of accounting records for at least six years and when accountants’ reports are required where a firm operates joint accounts or a client’s own account in the period.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which SRA Accounts Rule primarily governs the use of joint accounts held by a solicitor with a client or third party?

- a) Rule 2

- b) Rule 5

- c) Rule 9

- d) Rule 11

-

A solicitor operates a client's personal bank account under a Lasting Power of Attorney. Which of the following SRA Accounts Rules requirements applies? (Select all that apply)

- a) Paying the money into a client account promptly.

- b) Reconciling the account statements at least every five weeks.

- c) Keeping a central record of bills relating to the operation of the account.

- d) Obtaining an annual accountant's report covering the account.

-

Before using a Third-Party Managed Account (TPMA), what must a firm primarily ensure regarding the client?

- a) That the client has sufficient funds to cover the TPMA provider's fees.

- b) That the client understands the arrangement and gives informed consent in writing.

- c) That the client has separate legal advice on the TPMA agreement.

- d) That the TPMA provider is based in England and Wales.

Introduction

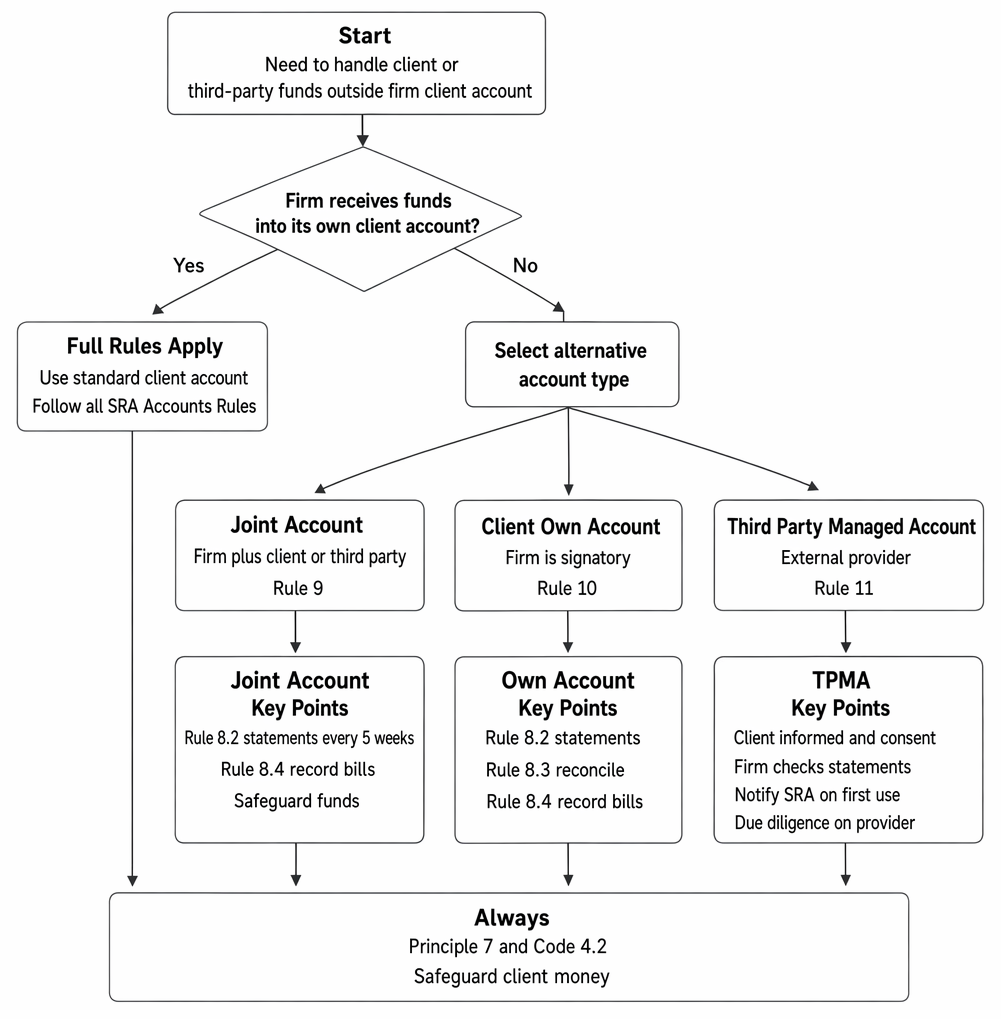

While the core SRA Accounts Rules focus heavily on the operation of a firm's own client bank account, there are specific situations where money belonging to clients or third parties is handled differently. The Rules acknowledge these situations and provide modified requirements for joint accounts (Rule 9), the operation of a client’s own account by the solicitor as signatory (Rule 10), and the use of third-party managed accounts (TPMAs) (Rule 11). Understanding these variations is essential for ensuring compliance and safeguarding funds, even when money does not pass through the firm’s main client account.

SRA Accounts Rules 2019 requirements are set out for a firm’s client account, joint accounts, client’s own accounts and TPMAs.

The starting point remains the definition of client money and the prohibition on using a client account to provide banking facilities unconnected to regulated legal services. Where funds are not held or received by the firm (for example, in a TPMA or the client’s own account), they fall outside the full client account regime, but the professional duties under the SRA Principles and Codes of Conduct continue to apply in full. Consequently, even when the full recording, reconciliation and withdrawal rules do not apply, firms must maintain appropriate oversight, put in place clear terms and safeguards, and keep adequate records so that client money and assets remain safe and are used only for their proper purpose.

Key Term: Joint Account

An account held at a bank or building society in the joint names of a solicitor/firm and a client or third party, to which limited SRA Accounts Rules apply (primarily Rule 9).Test Tip: In SQE-style questions on Understanding third-party managed accounts, identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

Joint Accounts (Rule 9)

A joint account under the SRA Accounts Rules is an account held in the joint names of the solicitor or firm and a client or other third party. A common example is where a solicitor acts as an executor alongside a non-solicitor executor (such as a family member) for a deceased's estate, and they open a joint bank account to manage the estate's funds.

Because the account is not solely controlled by the firm, it is not treated as a 'client account' for the full application of the Rules. Rule 9.1 specifies that only limited provisions of the Rules apply, specifically:

- Rule 8.2: Obtaining bank statements at least every five weeks.

- Rule 8.4: Keeping a readily accessible central record of bills or written notifications of costs relating to the matter.

Although the joint account is not a firm client account, money in it is still client money. The firm must therefore set proportionate safeguards and maintain oversight, even though detailed client ledger postings and five‑week reconciliations under the client account regime do not apply. Good practice includes:

- ensuring the account mandate requires joint signatures for withdrawals or transfers, minimising the risk of unilateral payments

- agreeing, in writing, clear roles, authority limits and payment approval procedures between joint holders

- obtaining and reviewing statements at least every five weeks and retaining them with the firm’s central records for at least six years, alongside the central record of bills and written notifications of costs

- keeping internal matter records that explain transfers and payments made from the joint account and demonstrate ongoing compliance with the firm’s overarching duties to safeguard money.

Where a firm operates a joint account during an accounting period, this can trigger the obligation to obtain an accountant’s report for that period (unless the firm is exempt under the small balances or Legal Aid Agency exceptions). Even though the funds are not in the firm’s client account, the SRA expects firms to be able to demonstrate that obligations under Rule 9 (and the SRA Principles and Codes) have been met.

SRA Principle 7 (acting in the best interests of each client) and the SRA Code of Conduct (Paragraph 4.2 for solicitors / 5.2 for firms – safeguarding client money and assets) remain of utmost importance. This means the solicitor must take reasonable steps to protect the money in the joint account, for example, by:

- documenting the client’s objectives and linking each payment or transfer to the regulated legal services being delivered

- ensuring that the joint account is not used to provide a general banking facility for the client or third party

- considering deposit protection implications for large balances and, where appropriate, discussing options that do not compromise availability on demand.

Worked Example 1.1

Farah, a solicitor, is appointed as a co-executor of Mr Khan's estate alongside Mr Khan's daughter, Aisha (who is not a solicitor). They decide to open a joint bank account in both their names to receive estate funds and pay liabilities. Farah's firm does not handle the money through its own client account. What are Farah's primary obligations under the SRA Accounts Rules regarding this joint account?

Answer:

Under Rule 9, Farah must ensure she obtains bank statements for the joint account at least every five weeks (Rule 8.2) and that records of any bills related to the estate administration are kept (Rule 8.4). Although the full client account rules do not apply, she still has professional duties to safeguard the estate money and act in the best interests of the estate beneficiaries. She should consider practical safeguards like requiring joint signatures for withdrawals.

Worked Example 1.2

A firm opens a joint account with a litigation client to hold settlement funds pending apportionment between multiple claimants. The other joint holder is a lay representative chosen by the claimants. The lay representative requests a transfer to a claimant’s personal account before the agreed apportionment schedule is finalised. What should the solicitor do?

Answer:

The firm should refuse any transfer that is not justified by the regulated legal services being delivered and the agreed apportionment. The joint account must not be used to provide a banking facility. The solicitor should ensure the mandate requires joint authorisation for withdrawals, obtain and review statements every five weeks, keep a central record of bills, and document decisions in the matter file. Payments should only be made in accordance with the agreed legal framework and client instructions consistent with acting in each client’s best interests.

Operating a Client's Own Account (Rule 10)

Sometimes a solicitor or authorised employee might operate a client's personal bank account as a signatory. This typically occurs under a power of attorney (e.g., Lasting Power of Attorney for property and financial affairs) or when appointed as a deputy by the Court of Protection for someone lacking mental capacity.

Key Term: Client's Own Account

A client's personal bank or building society account which a solicitor or firm operates as a signatory (e.g., under a power of attorney or as a Court of Protection deputy), subject to specific requirements under SRA Accounts Rule 10.

As the money is in the client's own account and not held or received by the firm, it isn't technically 'client money' under the main definition, and the account isn't a 'client account'. Therefore, the full Accounts Rules do not apply. However, Rule 10.1 imposes specific obligations on the solicitor/firm operating the account:

- Rule 8.2: Obtaining bank statements at least every five weeks.

- Rule 8.3: Performing reconciliations at least every five weeks (comparing bank statements to the firm's records of transactions made).

- Rule 8.4: Keeping a readily accessible central record of bills or written notifications of costs associated with operating the account.

These requirements reflect the heightened fiduciary duties owed when operating a client’s own account. Practical points include:

- maintaining an internal schedule of payments, with supporting invoices and the authority under which each payment is made

- recording bills and written notifications of costs centrally for any professional charges related to operating the account

- ensuring that the solicitor only makes payments consistent with the client’s best interests and the scope of the authority (for example, under the terms of the power of attorney or Court of Protection order)

- keeping documentary evidence of decisions, especially where discretionary payments are made for a client lacking capacity, to show how best interests were assessed

- promptly correcting any errors and recording how they were identified and remedied.

The SRA guidance acknowledges that obtaining statements and performing reconciliations every five weeks might not always be practicable (e.g., if the bank only issues quarterly statements). In such cases, the firm will not be in breach provided it takes reasonable steps to ensure the client's money is safe and records the steps taken. Reasonable steps might include:

- requesting more frequent interim statements or online access for periodic downloads

- preparing internal reconciliations using the latest available data and noting any limitations due to statement frequency

- documenting risk assessments and oversight measures adopted to protect funds.

Where a solicitor operates a client’s own account during an accounting period, this can trigger the obligation to obtain an accountant’s report for that period, even if the firm does not otherwise hold client money. Firms should also retain statements and central records for at least six years.

When the firm receives payment for its fees arising from work on the matter, normal billing and receipt entries are made in the firm’s accounting system. Crucially, the firm should not draw funds from a client’s own account for fees unless a bill or written notification of costs has been delivered and there is clear authority to do so; the central record under Rule 8.4 should cross‑refer to that bill.

Exam Warning: Do not confuse operating a client's own account (Rule 10) with holding client money in a separate designated client account (which is a client account subject to the full Rules, except perhaps for the interest calculation method). The key difference is ownership and control of the account itself.

Worked Example 1.3

A solicitor is appointed as Court of Protection deputy and operates a separate deputyship current account for the protected party. The bank only issues statements quarterly. How should the solicitor comply with Rule 10’s five‑week requirements?

Answer:

The solicitor should take reasonable steps to protect the client’s money, such as arranging online access to download transaction histories at least every five weeks, performing internal reconciliations against those downloads, and documenting why formal bank statements are not available more frequently. They should retain the quarterly statements when received, keep a central record of bills, and ensure payments are made only in the client’s best interests and within the deputy’s authority.

Third-Party Managed Accounts (TPMAs) (Rule 11)

Rule 11 permits firms, as an alternative to using their own client account, to enter into arrangements with a client for client money related to that client's matter to be held and managed by an independent third party.

Key Term: Third-Party Managed Account (TPMA)

An account held and operated by a third-party payment service provider (regulated by the Financial Conduct Authority), not the law firm, to hold money relating to a client's matter under an agreement between the firm, the client, and the provider (Rule 11).

Money held in a TPMA is not held or received by the law firm and therefore falls outside the definition of client money and the main SRA Accounts Rules. This can reduce the firm's administrative burden (e.g., no need for reconciliations or accountants' reports relating to that money). However, a firm must not use TPMAs to avoid its wider ethical and regulatory obligations.

Using a TPMA imposes specific obligations on the firm under Rule 11:

-

the firm must not itself receive or handle the money (Rule 11.1(a))

-

the firm must take reasonable steps before accepting instructions to ensure the client understands the arrangement, including:

- the contractual terms with the TPMA provider

- how TPMA fees will be paid and by whom

- the client's right to terminate the TPMA agreement and dispute payment requests (Rule 11.1(b))

-

the firm must obtain regular statements from the TPMA provider and check they accurately reflect transactions (Rule 11.2)

-

the firm must notify the SRA when it first uses a TPMA provider.

Due diligence on the provider is essential. The SRA expects the TPMA provider to be regulated by the Financial Conduct Authority (FCA) either as:

- an authorised payment institution; or

- a small payment institution that has adopted voluntary safeguarding arrangements to the same level as an authorised payment institution.

A firm should verify the provider’s FCA registration, review their safeguarding and complaints procedures, and evaluate the interest and fee arrangements. The firm must also assess whether using a TPMA is in each client’s best interests for the specific matter and ensure the TPMA is linked to the delivery of regulated legal services, not used as a general banking facility.

Client engagement is central to compliance: clients must be informed in a way they can understand and must give informed consent. In practice, firms should provide transparent written information addressing:

- how funds will be held and the mechanics of the TPMA in the client’s matter

- the allocation of TPMA fees and who will bear them

- the client’s rights to terminate and to dispute payment requests

- the differences in regulatory protections compared to funds held in a firm’s client account, including the provider’s complaints route.

Even though the firm does not hold the money, ongoing oversight is required. Firms should:

- obtain and review TPMA statements regularly and reconcile them to internal matter records to confirm accuracy

- maintain internal records sufficient to demonstrate that all TPMA transactions relate to regulated legal services delivered by the firm

- monitor whether continued use of the TPMA remains appropriate for the client’s best interests.

On first use of a TPMA, firms must notify the SRA using the SRA’s TPMA notification form, providing details such as the firm’s name and SRA number, the TPMA provider’s name, the provider’s FCA authorisation number, and the date the firm plans to start using a TPMA. Subsequent changes in provider or material changes in arrangements should be documented and, where appropriate, updated with the SRA.

Interest arising on TPMA-held monies is dictated by the TPMA’s terms and the provider’s safeguarding arrangements. The firm must ensure the client understands those arrangements and who receives any interest. Because TPMA funds are not held or received by the firm, the firm’s obligation to account for interest under Rule 7.1 does not directly apply; instead, the firm’s duty is to ensure the arrangement is fair and in the client’s best interests, and that the client has been properly informed about the TPMA’s interest and fee terms.

Critically, the firm still has overarching duties under the SRA Principles (e.g., acting in the client's best interests – Principle 7) and the Code of Conduct (safeguarding client money and assets – para 4.2/5.2). This means the firm must conduct due diligence to ensure the TPMA provider is suitable, regulated, and that the arrangement is appropriate for the client and the specific matter. The SRA guidance emphasizes that the TPMA must not simply be used as a banking facility unconnected to the legal services being provided.

Worked Example 1.4

A law firm specializing in high-volume, low-value debt recovery considers using a TPMA provider to handle the receipt of collected debts from debtors and payment out to their creditor clients, aiming to reduce administrative costs associated with running a traditional client account. What must the firm do before implementing this system?

Answer:

Before using the TPMA, the firm must (under Rule 11 and associated guidance):

- Conduct due diligence on the TPMA provider to ensure it is FCA-regulated and suitable.

- Obtain informed, written consent from each client before using the TPMA for their matter, ensuring clients understand the terms, fees, termination rights, and regulatory differences compared to a firm's client account.

- Notify the SRA that it is using a TPMA provider (when first doing so).

- Ensure the arrangement is genuinely linked to the debt recovery service and not just providing a banking facility.

- Establish internal systems to obtain and check regular statements from the TPMA provider (Rule 11.2).

Worked Example 1.5

A firm proposes to route all conveyancing deposits through a TPMA to avoid operating a client account, and offers to hold surplus funds for clients between transactions for convenience. Is this acceptable?

Answer:

No. Using a TPMA to hold surplus funds “for convenience” or for purposes unconnected to regulated legal services risks breaching the prohibition on providing banking facilities. TPMA use must be linked to the delivery of regulated services in the specific matter, must be appropriate for the client’s best interests, and requires informed client consent, provider due diligence, SRA notification on first use, and regular statement checks.

Worked Example 1.6

A firm selects a TPMA provider that is based outside England and Wales but is registered as an authorised payment institution on the FCA register. Does the provider’s location matter?

Answer:

The provider’s physical location is not determinative. The SRA expects the TPMA provider to be regulated by the FCA and to have appropriate safeguarding arrangements. The firm must verify the provider’s FCA authorisation, ensure the arrangement is suitable for the client’s matter, obtain informed client consent, and meet Rule 11’s statement and notification requirements.

Worked Example 1.7

TPMA statements show a payment that the client disputes. The firm believes the payment was properly requested under the retainer. How should the firm proceed?

Answer:

The firm must follow the TPMA’s dispute resolution mechanism and the client’s rights to dispute payment requests. It should provide clear evidence linking the request to regulated services delivered, explain the retainer basis, and ensure communications are transparent. The firm must maintain oversight, keep accurate records, and act in the client’s best interests, including pausing further requests if necessary until the dispute is resolved.

Summary

| Feature | Joint Account (Rule 9) | Client's Own Account (Rule 10) | TPMA (Rule 11) |

|---|---|---|---|

| Account Holder | Firm/Solicitor + Client/Third Party | Client | Third-Party Provider |

| Operator | Joint (or potentially Sole by agreement) | Solicitor/Firm (as signatory) | Third-Party Provider |

| Is it Client Money? | Yes | No (not held/received by firm) | No (not held/received by firm) |

| Is it a Client A/c? | No | No | No |

| Key Rules Applied | 8.2 (Statements), 8.4 (Bills Record) | 8.2 (Statements), 8.3 (Reconciliation), 8.4 (Bills Record) | 11.1 (Client Consent/Info), 11.2 (Statements Check) |

| SRA Notification | No | No | Yes (on first use) |

| Accountant Report | Usually Included (if firm holds client money elsewhere) | Usually Included (if firm holds client money elsewhere) | Excluded (money not held by firm) |

| Safeguarding Duty | Yes (Principles/Code) | Yes (Principles/Code) | Yes (Principles/Code + Due Diligence on Provider) |

Additional summary points:

- Money in a joint account remains client money; safeguards and oversight must be proportionate even though the account is not a firm client account.

- Operating a client’s own account requires statements and reconciliations at least every five weeks; where impracticable, reasonable steps and records are essential.

- TPMA money is not held or received by the firm, but the firm remains responsible for ensuring suitability, client understanding and consent, SRA notification on first use, and regular statement checking.

Key Point Checklist

This article has covered the following key knowledge points:

- Joint accounts (Rule 9) are held with clients/third parties; only limited SRA Accounts Rules apply (mainly obtaining statements and recording bills).

- Money in a joint account is client money; firms must implement mandate safeguards (e.g., joint signatures), maintain oversight and retain statements and central records.

- Operating a client's own account (Rule 10) as signatory (e.g., under PoA or as deputy) requires statements, reconciliations and a central record of bills; where five‑week cycles are impracticable, reasonable protective steps must be taken and documented.

- Where a firm operates joint accounts or a client’s own account during an accounting period, this may trigger an accountant’s report requirement unless an exemption applies.

- Third-Party Managed Accounts (TPMAs) (Rule 11) involve an external FCA‑regulated provider holding funds; this money is not client money held by the firm.

- Using TPMAs requires prior informed client consent, due diligence on the provider (including FCA status and safeguarding arrangements), and SRA notification on first use.

- Firms using TPMAs must still obtain and check statements from the provider and maintain internal records linking all TPMA transactions to regulated legal services.

- TPMA use must not provide a banking facility; all arrangements must be in the client’s best interests and appropriate for the specific matter.

- Interest obligations differ depending on where funds are held; firms must ensure clients understand TPMA interest and fee terms and that arrangements are fair.

- Overarching duties to safeguard client money and act in the client's best interests apply even when using alternative accounts; clear documentation and oversight are essential.

Key Terms and Concepts

- Joint Account

- Client's Own Account

- Third-Party Managed Account (TPMA)