Learning Outcomes

This article outlines pre‑contract inspection and survey considerations in property transactions, including:

- Caveat emptor and buyer responsibility for investigating physical condition; risk allocation and impact on pre‑exchange due diligence

- Distinction between personal inspection and professional survey; scope, limitations, and what each can and cannot achieve

- Mortgage valuation versus buyer‑commissioned survey; limitations of valuations for buyer protection

- RICS Home Survey Levels 1, 2, and 3, suitability by property age, construction, condition, and the buyer’s plans; former “HomeBuyer Report” terminology

- Specialist and supplementary reports (structural engineer’s, damp/timber, drainage, asbestos) and circumstances favouring a newbuild structural defects insurance policy

- Newbuild 10‑year structural warranties (e.g. NHBC Buildmark) and interaction with surveys and lender requirements

- Surveyor’s duties, inspection scope and limitations, potential liability for negligent reports, terms of engagement, and professional indemnity insurance

- Indicators of third‑party rights discoverable on personal inspection (for example, persons in actual occupation, obvious easements) that may bind the buyer

SQE1 Syllabus

For SQE1, you are required to understand pre‑contract personal inspection and professional survey considerations in property transactions, with a focus on the following syllabus points:

- The caveat emptor principle and its application to physical defects in property transactions.

- The purpose and limitations of personal inspection by the buyer.

- The different types of RICS survey reports (Levels 1, 2, and 3) and their suitability for various properties.

- The solicitor’s duty to advise on inspections and surveys.

- The consequences of failing to identify defects before exchange.

- The distinction between a lender’s mortgage valuation and a buyer‑commissioned survey.

- When specialist reports or a newbuild structural defects insurance policy are appropriate.

- How inspection may reveal evidence of overriding interests (for example, actual occupation, obvious easements).

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

What is the legal principle that places the risk of undiscovered physical defects on the buyer before exchange of contracts?

- a) Privity of contract

- b) Caveat emptor

- c) Duty of care

- d) Misrepresentation Act 1967

-

Which RICS survey type is most appropriate for an older property with visible signs of disrepair?

- a) Mortgage valuation

- b) Condition Report (Level 1)

- c) HomeBuyer Report (Level 2)

- d) Building Survey (Level 3)

-

True or false? The seller is always legally obliged to disclose all physical defects in the property to the buyer before exchange of contracts.

Introduction

When buying property, the buyer is expected to investigate the physical state of the building and land before becoming contractually bound. The seller’s duty to disclose is limited, and the buyer must rely on their own inspection and professional advice. This article explains the caveat emptor principle, the importance of personal inspection, and the main types of survey reports available, all of which are essential for SQE1 Property Practice.

Buyer inspection, survey selection, and responses to defects before exchange of contracts in accordance with caveat emptor.

A prudent buyer’s approach is two‑pronged: a careful personal inspection complemented by an appropriate professional survey. The solicitor’s role is to advise on both, ensuring the client understands what each will and will not cover, and how findings might affect price, timing, mortgage funding, and the decision to proceed.

The Caveat Emptor Principle

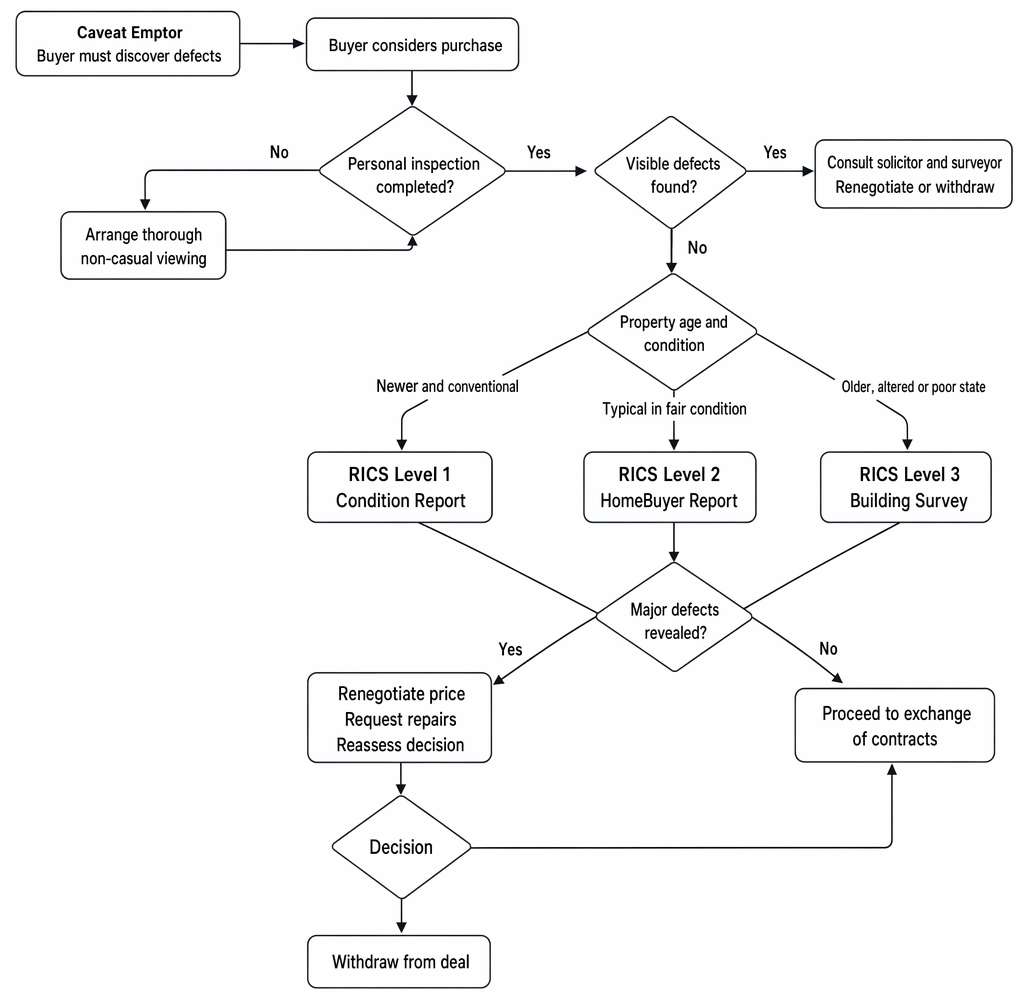

The starting point for physical defects in property transactions is caveat emptor—let the buyer beware. The buyer is responsible for discovering any issues with the property before exchange. If defects are found after exchange, the buyer will usually have no remedy unless the seller has actively concealed them or made a misrepresentation.

Key Term: Caveat Emptor

The common law rule that the buyer is responsible for identifying physical defects in property before exchange. The seller is generally not obliged to disclose such defects.

Caveat emptor applies to the property’s physical condition (for example, damp, subsidence, rot, roof failure). It does not permit a seller to mislead: if specific questions are asked (for example, through the Property Information Form (TA6)), the seller must answer honestly and accurately; misleading answers can give rise to misrepresentation remedies. However, the primary risk remains with the buyer to commission appropriate inspections before exchange. Contractual boilerplate rarely shifts this risk.

Caveat emptor also reinforces the need to consider visible signs of third‑party rights. Some rights bind a buyer even if not registered, where they are obvious on a reasonably careful inspection or where a person is in actual occupation. A diligent physical inspection can therefore protect against both physical and legal surprises.

Personal Inspection

A buyer should always be advised to carry out a careful personal inspection of the property before exchange. This is more than a casual viewing; it involves looking for obvious (patent) defects such as cracks, damp, missing tiles, or signs of water ingress. The buyer should also check boundaries, access, and look for evidence of third-party occupation or rights of way.

However, a personal inspection by a layperson is limited. Many defects—especially structural or hidden (latent) issues—will not be apparent without professional knowledge or intrusive investigation.

Key Term: Personal Inspection

A careful on‑site viewing by the buyer, aimed at spotting obvious defects and red flags: signs of damp, movement, roof disrepair, poor drainage; boundary anomalies; apparent rights of way; and indications of third‑party occupation.

Beyond the fabric of the building, a short, common‑sense checklist for a personal inspection includes:

- Boundaries: do fences and hedges align with the agent’s particulars and title plan? Are there encroachments, broken walls, or shared access points?

- Access: is the property directly abutting a publicly maintainable highway or is there a verge or strip between? A visible grassed strip may indicate a potential “ransom strip” requiring legal confirmation of rights.

- Occupation: are any parts occupied by someone other than the seller (for example, lodgers or a neighbour storing items)? Ask specifically; persons in actual occupation may have rights.

- Use patterns: worn tracks or footpaths may signal a long‑used right of way that could amount to a legal easement and be obvious on inspection.

Worked Example 1.1

A buyer views a 1920s house and notices a musty smell but sees no visible damp. After completion, extensive rot is discovered under the floorboards. Can the buyer claim against the seller?

Answer:

No. Under caveat emptor, the buyer was responsible for investigating the property’s condition before exchange. The seller had no duty to disclose the hidden defect unless specifically asked or unless they actively concealed it.

Worked Example 1.2

On inspection of a cottage’s garden, the buyer notices a well‑worn footpath used by neighbours as a shortcut to a lane. No right of way is noted on the register. Post‑completion, the neighbours continue to use the path and claim a prescriptive right. Is the buyer likely bound?

Answer:

Potentially yes. An unregistered legal easement arising by prescription can bind a purchaser if it is obvious on a reasonably careful inspection. The visible track was a red flag the buyer should have investigated pre‑exchange.

Professional Surveys

Because personal inspection is limited, buyers should be advised to commission a professional survey before exchange. A survey is carried out by a qualified surveyor and provides an expert assessment of the property’s condition. This is distinct from a mortgage valuation, which is for the lender’s benefit only and does not protect the buyer.

Key Term: Mortgage Valuation

A basic assessment for the lender to confirm the property is suitable security for the loan. It does not provide advice on the property’s condition for the buyer. Key Term: Survey

A professional report prepared for the buyer, assessing the property’s condition and highlighting defects, repairs, and risks.

A buyer should not rely on a mortgage valuation as a substitute for a survey. Valuations are often brief, sometimes “drive‑by” or desktop, and primarily answer whether the lender’s security is adequate. They rarely include detailed comment on building pathology, repair options, or costings, and any duty of care is owed to the lender. Where the property is older, altered, non‑standard, or shows signs of distress, a proper survey is essential.

For newbuilds and newly converted properties, a traditional survey before the building is complete is rarely practicable or useful. Instead, lenders typically require a 10‑year structural defects insurance policy; a separate snagging inspection can be arranged close to completion.

Key Term: Structural defects insurance policy

A 10‑year warranty (for example, NHBC Buildmark) covering certain defects in design and construction. Typically, the builder is responsible for non‑structural defects during an initial period (often two years), with structural cover provided for the remainder. Widely required by lenders on properties less than ten years old.

RICS Home Survey Levels

The Royal Institution of Chartered Surveyors (RICS) sets out three main types of survey, each suited to different properties and buyer needs.

Key Term: Condition Report (Level 1)

The most basic survey, providing a summary of the property’s condition using a traffic-light system. Suitable only for newer, conventional properties in good condition. No advice or valuation is included. Key Term: HomeBuyer Report (Level 2)

A more detailed survey, identifying significant defects and providing advice on repairs and maintenance. Suitable for conventional properties in reasonable condition. May include a valuation if requested. Sometimes also referred to as “RICS Home Survey – Level 2.” Key Term: Building Survey (Level 3)

The most comprehensive survey, with a thorough inspection and detailed report on construction, defects, repairs, and risks. Recommended for older, larger, or altered properties, or where major works are planned. Sometimes also referred to as “RICS Home Survey – Level 3.”

Key differences in scope are practical. Level 1 and Level 2 are visual, non‑intrusive inspections. Level 3 is also typically non‑destructive, but it is more exhaustive: it assesses condition in more depth, explains probable causes, recommends remedial options and priorities, and may discuss future maintenance and budgetary implications. None of the levels routinely test services (electrics, gas, heating) or open up structures without express agreement.

Choosing the Right Survey

The appropriate survey depends on the property’s age, type, and condition, as well as the buyer’s intentions. For example, a Level 1 report is not suitable for an old or obviously neglected property. A Level 3 survey is advisable for properties with signs of disrepair, non-standard construction, or where the buyer plans significant alterations.

If purchasing a flat, expect any survey to focus on the demised premises; the surveyor will often exclude the wider structure and common parts, emphasising the need to review landlord/management information for major works risk. Where the flat is in an older block, a Level 2 (or Level 3, if there are concerns) can still be appropriate to assess condition within the limitations of access.

Specialist follow‑ups are common: a Level 2 or 3 may recommend reports by a structural engineer (movement or roof structure), damp/timber specialist (rot or infestation), CCTV drainage survey (suspected defects), or asbestos survey in non‑domestic premises. These should be commissioned before exchange wherever findings materially affect value, safety, or future cost.

In SQE1, you may be asked to recommend the appropriate survey for a given property. Always consider the property’s age, condition, and the buyer’s plans. Recommending an inadequate survey is a common error.

Worked Example 1.3

A client is buying a Grade II listed, 18th‑century cottage with later extensions and intends to knock through and reconfigure. What survey is appropriate?

Answer:

A Level 3 Building Survey. The property is old, altered, and listed, and significant works are planned. A Level 3’s depth of analysis and repair advice is required; it can also flag where listed building consent and building control are likely to be relevant to the proposed alterations.

Worked Example 1.4

A buyer is purchasing a newbuild flat off‑plan with completion due in six months. The developer offers an NHBC Buildmark warranty. Should the buyer commission a survey before exchange?

Answer:

Typically no. Before construction is finished, a survey adds little. The key protection is the 10‑year structural defects warranty required by most lenders. The buyer may consider a snagging inspection shortly before completion to identify minor defects for the developer to rectify.

Worked Example 1.5

A client is buying a 1950s semi-detached house in average condition and asks whether a Level 1 Condition Report is sufficient.

Answer:

No. For a property of this age, a Level 2 HomeBuyer Report is the minimum recommended. A Level 1 report is only suitable for newer homes in good condition.Exam Warning: In SQE1, you may be asked to recommend the appropriate survey for a given property. Always consider the property’s age, condition, and the buyer’s plans. Recommending an inadequate survey is a common error.

The Surveyor’s Role and Liability

Surveyors owe a duty of care to their client to exercise reasonable skill and care in inspecting the property and preparing the report. If a surveyor negligently fails to identify a defect that should have been discovered, the buyer may have a claim for losses suffered.

Surveyor liability turns on scope and foreseeability. Terms of engagement define what the surveyor will do, any exclusions (for example, no lifting of floor coverings or furniture; no testing of services; no access to unsafe areas), and any reliance the buyer can place on the report. Reports are commonly non‑intrusive; they will often state that further opening‑up or specialist inspection is needed to assess suspected issues.

Where a buyer relies only on a lender’s valuation, a duty of care to the buyer will rarely arise because the valuer’s client is the lender. There are, however, situations in which a valuer may owe a duty to an intending purchaser of a modest residential property who is foreseeably going to rely on the valuation without commissioning an independent survey. That underlines the importance of suitable instructions and scope.

If survey findings materially affect value or prompt a price renegotiation, the buyer’s solicitor must ensure that any change in price or discovery of defects is reported to the lender in line with the lender’s instructions. A lender may reduce the advance or impose a retention until specified remedial works are completed.

Revision Tip: Always advise clients to check the surveyor’s terms of engagement and ensure the surveyor has professional indemnity insurance. Survey reports are usually non-intrusive and may not cover inaccessible areas.

Worked Example 1.6

A buyer instructs a Level 2 survey on a 1930s house. The report fails to mention significant roof sagging visible from ground level. Months later, extensive roof repairs are required. Is there a potential claim?

Answer:

Potentially yes. If a reasonably careful surveyor conducting a Level 2 inspection should have noted the visible sag and advised further investigation, the omission may be negligent within the agreed scope. Loss would be measured by the cost attributable to the negligent omission, subject to causation and any valid limitations in the terms of engagement.

Summary Table: RICS Home Survey Levels

| Feature | Level 1: Condition Report | Level 2: HomeBuyer Report | Level 3: Building Survey |

|---|---|---|---|

| Purpose | Basic overview; urgent issues | Detailed defects; repair advice | Full structural analysis |

| Suitability | Newer, conventional homes | Standard homes in fair condition | Older, large, altered, or poor |

| Inspection Depth | Visual, non-intrusive | More extensive visual inspection | Thorough, includes concealed areas |

| Valuation Included | No | Optional | No (unless requested) |

Practical points linking inspection, surveys, and other due diligence

A coherent pre‑exchange strategy joins the dots:

- Personal inspection highlights red flags to be explored through title, enquiries, and the survey (for example, visible rights of way, signs of occupation, boundary discrepancies).

- The survey can uncover structural and serviceability issues that trigger specialist reports and feed into price negotiations or conditions of mortgage funding (for example, retentions pending damp‑proofing or roof replacement).

- Where works have been carried out without obvious consents, survey comments should prompt legal checks for planning permission, building regulations compliance, and certificates (or a plan to regularise and manage risk). Indemnity insurance is not a substitute for addressing physical risk.

- For newbuilds and conversions, verify the warranty provider, its coverage, and exclusions; ensure the policy will be assignable to successors and acceptable to the lender. Consider a snagging list pre‑completion.

Key Point Checklist

This article has covered the following key knowledge points:

- The buyer is responsible for investigating the property’s physical condition before exchange (caveat emptor).

- Personal inspection can reveal obvious defects and signs of third‑party rights but is limited.

- Professional surveys are essential for identifying hidden or structural issues.

- Mortgage valuations are for the lender and do not protect the buyer.

- RICS surveys: Level 1 (Condition Report), Level 2 (HomeBuyer), Level 3 (Building Survey).

- The solicitor must advise on the importance and suitability of different survey types.

- Surveyors owe a duty of care but survey reports have limitations.

- Newbuilds usually rely on a 10‑year structural defects insurance policy; a snagging inspection near completion can be valuable.

- Material defects and price renegotiations must be reported to the lender; funding can be reduced or made conditional.

- Careful inspection may reveal evidence of overriding interests (for example, obvious easements, actual occupation).

Key Terms and Concepts

- Caveat Emptor

- Personal Inspection

- Mortgage Valuation

- Survey

- Condition Report (Level 1)

- HomeBuyer Report (Level 2)

- Building Survey (Level 3)

- Structural defects insurance policy