Learning Outcomes

This article explains how trust property can pass outside a deceased’s estate for succession and tax purposes in the SQE1 FLK2 exam context, including:

- identifying when property is held solely as legal title by a trustee so that it bypasses the deceased’s estate and continues under the trust terms;

- distinguishing legal and equitable ownership and applying that distinction to co-owned land, bare trusts, and will trusts;

- comparing discretionary, interest in possession, bare, excluded property and charitable trusts, and predicting whether their assets fall inside or outside the estate;

- analysing how life interests, IPDIs and discretionary benefits are treated on death for both succession and inheritance tax purposes;

- recognising the duties, powers, and potential liabilities of trustees where a trustee or beneficiary dies, including replacement of trustees and vesting of assets;

- evaluating common SQE1-style problem questions that mix personal, jointly owned and trust assets, and avoiding typical exam traps and misunderstandings;

- assessing the practical implications for personal representatives, creditors and beneficiaries when significant wealth is held on trust outside the estate.

SQE1 Syllabus

For SQE1, you are required to understand the treatment of trust property in the context of wills and the administration of estates, with a focus on the following syllabus points:

- the distinction between legal and equitable ownership in trusts

- how trust property passes outside the estate on death

- the main types of trust relevant to estate planning (e.g. discretionary, interest in possession, bare trusts)

- the duties and powers of trustees

- the impact of trusts on inheritance tax and estate administration

- trusts of land under TLATA 1996 (automatic trust where land is co-owned; legal title as joint tenancy, equitable interests may differ)

- survivorship for beneficial joint tenancies versus tenancies in common

- immediate post-death interests (IPDIs) and when life interests are taxed in the life tenant’s estate

- the “relevant property” regime for discretionary trusts (ten-year and exit charges)

- trustees’ standard investment and care duties under the Trustee Act 2000, and maintenance/advancement powers under the Trustee Act 1925 as amended

- self-dealing and fair dealing rules for trustees, and consequences of breach (including tracing)

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the difference between legal and equitable ownership in a trust?

- Which types of trust property do not fall into a deceased’s estate for distribution by personal representatives?

- What are the main duties of trustees when holding trust property?

- How does a bare trust differ from a discretionary trust in terms of beneficiary rights?

Introduction

When a person dies, not all property they owned or controlled will pass to their personal representatives for distribution under their will or the intestacy rules. Some assets are held on trust and pass outside the estate. For SQE1, you must be able to identify trust property, understand how it is treated on death, and explain the legal consequences for beneficiaries and trustees.

Trust property is a common feature in estate planning and can have significant implications for inheritance tax, asset protection, and succession. This article explains the key legal principles, types of trust, and trustee duties relevant to trust property passing outside the estate. It also highlights the limits of personal representatives’ authority: PRs must collect the deceased’s estate, but they must not interfere with assets held on trust for others. Where the deceased was a trustee, the trust continues according to its terms and replacement trustees are appointed; the trust assets do not vest in the PRs.

Test Tip: In SQE-style questions on Trust property, identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

Exam Warning: Do not rely on a familiar phrase from Trust property alone; check whether the facts satisfy every condition, exception, and timing requirement.

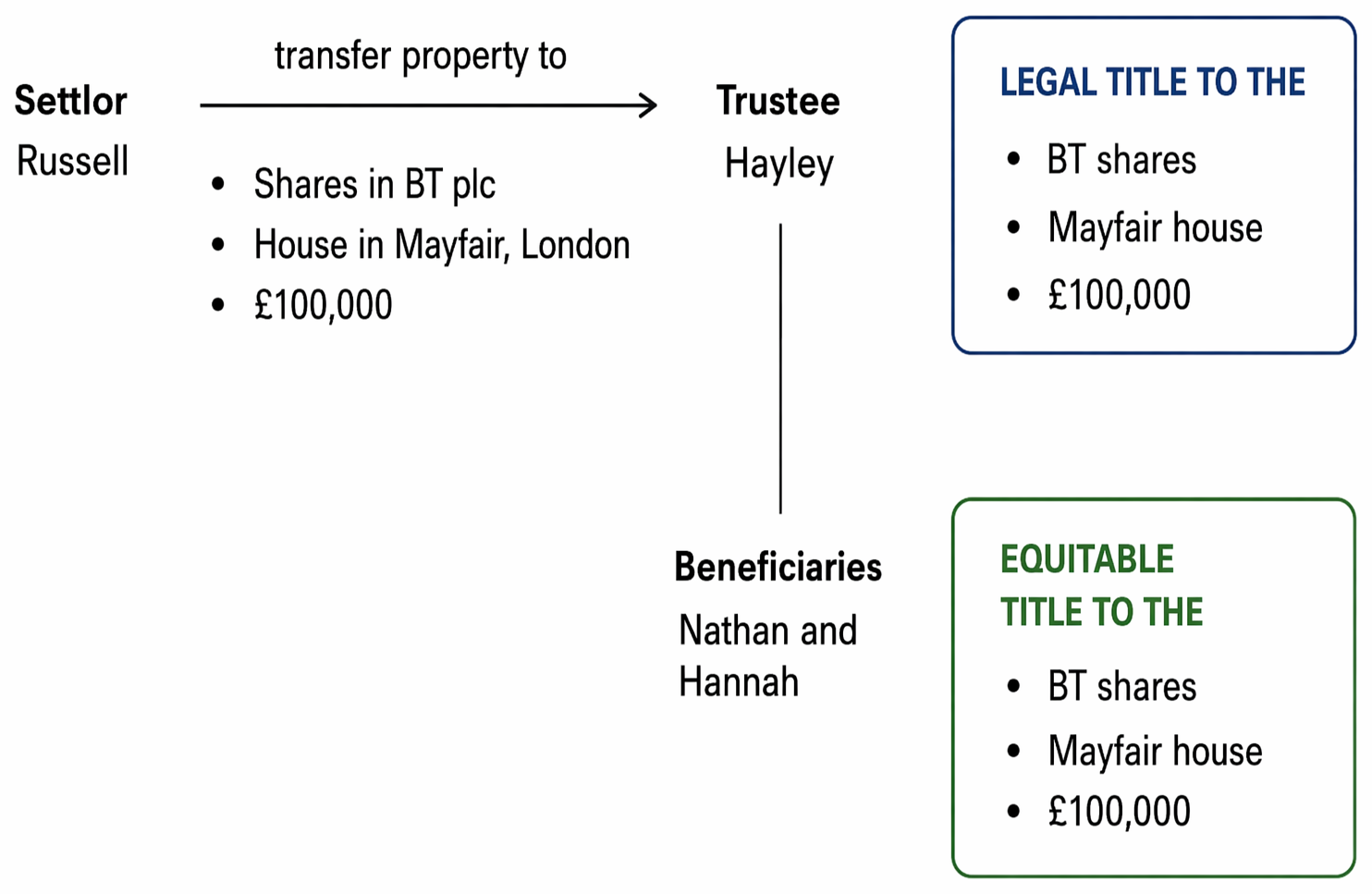

Trust property: legal and equitable ownership

Trust property is characterised by the separation of legal and equitable (beneficial) ownership. The trustee holds the legal title to the property, while the beneficiary holds the equitable interest.

Trust property on death is summarised by reference to trustee title, limited beneficial interests, continuing trusts, trust types, duties, and tax.

Key Term: legal ownership

The right to deal with and control property in law, held by the trustee in a trust arrangement. Key Term: equitable (beneficial) ownership

The right to benefit from property, held by the beneficiary in a trust.

This division means that, on the death of a trustee, the trust property does not form part of their personal estate. Instead, it continues to be held on trust for the beneficiaries, according to the terms of the trust. If a trustee dies, the trust does not fail: a successor trustee can be appointed and the trust property is vested in the new trustee(s), typically by deed; certain assets (e.g. registered land) may vest automatically under statutory provisions, while shares usually require stock transfer formalities.

Where land is co-owned, a trust of land arises automatically by statute.

Key Term: trust of land

A statutory trust arising when land is co-owned; the legal estate is held by the trustees, and beneficial interests are held in equity (TLATA 1996).

Under TLATA 1996, co-owners hold the legal estate as joint tenants. The equitable interests may be held as joint tenants (triggering survivorship) or as tenants in common (each distinct share passes via will/intestacy). These co-ownership trusts are distinct from trust property held by a person as trustee of an express or implied trust.

When does trust property pass outside the estate?

Trust property passes outside the estate when the deceased held it as a trustee (i.e. legal owner only) or as a beneficiary with a limited interest (such as a life interest) that ends on death. In these cases, the property is not available for distribution by the deceased’s personal representatives.

Main scenarios where trust property passes outside the estate

- The deceased was a trustee: Only the legal title is held; the property remains subject to the trust for the beneficiaries.

- The deceased had a life interest (interest in possession): The right to income or use ends on death, and the property passes to the next beneficiary (the remainderman) under the trust.

- The deceased was a beneficiary of a discretionary trust: No fixed entitlement; the trust property remains under the control of the trustees for the benefit of the class of beneficiaries.

- Life policy proceeds written in trust or assigned: The insurer pays trustees/beneficiaries directly; proceeds do not vest in the PRs.

- Pension death benefits under discretionary schemes: Trustees exercise discretion (often guided by a nomination); benefits are paid outside the estate.

Key Term: interest in possession

A right to receive income or benefit from trust property for life or a fixed period, but not to the capital. Key Term: remainderman

The person entitled to trust property after the end of a prior interest, such as a life interest.

Contrast with absolute beneficial ownership: if the deceased had an absolute equitable interest (e.g. as the sole beneficiary under a bare trust), that interest usually forms part of the estate and is distributable by the PRs.

Clarifying equitable entitlements

Some life interests are “qualifying” for tax purposes and result in the fund being taxed in the life tenant’s estate on death.

Key Term: immediate post-death interest (IPDI)

An interest in possession that arises on a person’s death (typically under their will). For IHT, an IPDI is treated as a qualifying interest in possession.

Where the deceased had an IPDI (for example, a spouse given a right to income from residue under a will trust), the interest ends on death and the trust capital passes to the remainderman under the trust; however, for IHT the settled fund is taxed as if part of the deceased life tenant’s estate, typically payable out of the trust fund.

Types of trust relevant to estate planning

Trusts are used in estate planning to control the timing and manner of asset distribution, protect vulnerable beneficiaries, and manage tax liabilities. The main types encountered in SQE1 are:

Discretionary trusts

In a discretionary trust, trustees decide how and when to distribute income or capital among a class of beneficiaries. No beneficiary has a fixed entitlement.

Key Term: discretionary trust

A trust where trustees have discretion over which beneficiaries receive trust property and in what amounts.

For succession, discretionary trust property is not part of any individual beneficiary’s estate: the trustees retain control and exercise their powers. For IHT, discretionary trusts are generally within the “relevant property” regime, subject to periodic (ten-year) and exit charges rather than being taxed in any beneficiary’s estate.

Key Term: relevant property

Settled property without a qualifying interest in possession; subject to ten-year and exit charges under IHTA 1984.

Discretionary pensions and many death-in-service schemes operate similarly: trustees decide recipients and amounts, often guided by a nomination letter that is persuasive but not binding.

Interest in possession trusts

Here, a beneficiary (the life tenant) has a right to income or use of trust property for life, with capital passing to another beneficiary (the remainderman) on their death. This is common in will trusts that provide for a spouse during life, then pass capital to children.

Where an interest arises at death under a will, it is typically an IPDI and, for IHT, the trust fund is taxed in the life tenant’s estate. The property itself passes outside the estate for succession purposes (the PRs do not distribute it), flowing instead to the remainderman under the trust terms.

Bare trusts

A bare trust gives the beneficiary an absolute right to both income and capital. The trustee’s role is purely administrative.

Key Term: bare trust

A trust where the beneficiary is absolutely entitled to the trust property and can demand its transfer at any time.

If the deceased had an absolute beneficial interest under a bare trust, that equitable interest forms part of the estate and is distributable by the PRs (subject to any trust administration needed to effect transfer). For minors, the bare trust continues until majority, at which point the beneficiary can call for the property.

Excluded property trusts

These are trusts set up by non-UK domiciled individuals to hold non-UK assets, often for inheritance tax planning. Subject to the detailed rules on domicile and UK residential property interests, such property is “excluded” from the UK estate for IHT purposes. Succession follows the trust terms and the PRs have no claim to the trust property.

Charitable trusts

Charitable trusts are established for charitable purposes and benefit from special tax treatment, including exemption from inheritance tax. As with any trust, legal title passes to trustees; charitable assets do not vest in the PRs of a deceased trustee or donor.

Trustee duties and powers

Trustees are responsible for managing trust property for the benefit of the beneficiaries. Their main duties include:

- Acting in accordance with the trust instrument and the law

- Acting impartially between beneficiaries

- Exercising reasonable care and skill (Trustee Act 2000)

- Keeping trust property separate from their own assets

- Providing information and accounts to beneficiaries

Key Term: trustee

The person or persons holding legal title to trust property and responsible for managing it for the beneficiaries. Key Term: beneficiary

The person or persons entitled to benefit from trust property.

Trustees have powers to invest, insure, and sell trust property, subject to the trust instrument and statutory requirements. They may be personally liable for losses caused by breach of trust.

The statutory duty of care under the Trustee Act 2000 requires trustees to exercise such care and skill as is reasonable in the circumstances, taking into account any special knowledge they have or hold themselves out as having. Professional trustees are held to a higher standard. Trustees typically must act jointly and unanimously unless the trust instrument permits majority decisions.

Trustees cannot generally delegate discretions but may delegate administrative functions and, subject to conditions, certain investment decisions. An individual trustee may execute a limited power of attorney (up to 12 months) to delegate their functions, while remaining responsible for the attorney’s acts.

Investment, maintenance, and advancement

Trustees must consider suitability and diversification when investing trust funds. Beyond investment, trustees often exercise statutory powers to support beneficiaries:

Key Term: power of maintenance

Trustees’ power to apply trust income for a beneficiary’s maintenance, education, or benefit and to accumulate surplus income (TA 1925, s31, as amended). Key Term: power of advancement

Trustees’ discretionary power to advance capital to a beneficiary with an interest in capital, up to their presumptive share (TA 1925, s32, as amended).

Under s31 (as amended), income may be applied for beneficiaries (including minors) and surplus accumulated; at 18, beneficiaries with vested interests become entitled to income (unless postponed by the instrument). Under s32 (as amended by the Inheritance and Trustee Powers Act 2014), trustees may advance up to the whole of a beneficiary’s presumptive share of capital (not merely half, as was previously the default), subject to protecting prior interests (e.g. obtaining a life tenant’s consent where required by the instrument).

Self-dealing and fair dealing

Trustees must avoid conflicts. A trustee purchasing trust property engages in prohibited self-dealing; such transactions are voidable at the beneficiaries’ instance regardless of the trustee’s good faith. By contrast, the “fair dealing” rule permits a trustee to buy a beneficiary’s equitable interest, but only on full disclosure, fair price, and without abuse of position.

Key Term: self-dealing

A trustee’s purchase of trust property; presumptively improper and voidable at the beneficiaries’ election.

Appointment and number of trustees

Trusts do not fail for want of a trustee. If a trustee dies or retires, successors can be appointed under the trust instrument or statute (commonly TA 1925, s36). For trusts of land, at least two trustees (or a trust corporation) are typically required to give a valid receipt for capital money; there may be up to four trustees. Vesting of trust property in new trustees commonly occurs by deed, with special formalities for shares.

Accountability and remedies

Breaches of trust expose trustees to personal liability to restore the trust fund (account or equitable compensation). Trustees must segregate trust property and keep accurate records; beneficiaries can seek disclosure to hold trustees to account. Where misapplied property can be identified, beneficiaries may trace and assert proprietary claims to regain priority over other creditors.

Worked Example 1.1

A is the sole trustee of a trust holding a portfolio of shares for B and C. A dies. Does the share portfolio pass to A’s personal representatives for distribution under A’s will?

Answer:

No. The shares are held on trust. Only the legal title was held by A as trustee. On A’s death, the trust property does not form part of A’s estate. The trust continues, and a new trustee must be appointed to hold the shares for B and C.

Worked Example 1.2

D has a life interest in a trust fund, with E as remainderman. D dies. What happens to the trust fund?

Answer:

D’s right to income ends on death. The trust fund passes to E (the remainderman) under the trust terms. The fund does not form part of D’s estate for distribution by D’s personal representatives.

Worked Example 1.3

F was a member of an occupational pension scheme with discretionary death benefits. F dies leaving a nomination in favour of their partner. Do the scheme death benefits pass via F’s PRs?

Answer:

No, in a discretionary scheme the trustees decide who receives the benefit. The nomination is usually persuasive but not binding. The lump sum is paid directly to the chosen recipient(s) and does not pass through the PRs or form part of the estate for succession.

Worked Example 1.4

G holds £50,000 in a bare trust for minor H. G dies. Does the £50,000 fall into G’s estate?

Answer:

No. G held only legal title. H is absolutely entitled. The funds remain trust property for H and do not pass to G’s PRs. A replacement trustee will be appointed to hold the legal title until H reaches majority, when H can demand transfer.

Tax and practical implications

Trust property passing outside the estate is not available to pay the deceased’s debts or for distribution under the will or intestacy rules. It may also be excluded from the deceased’s estate for inheritance tax purposes, depending on the type of trust and the deceased’s interest.

However, if the deceased had a fixed entitlement to trust property (e.g. an absolute interest or a vested share), that interest will usually form part of their estate.

Inheritance tax treatment differs between trust types and interests:

- Interests in possession created on death (IPDIs) are taxed in the life tenant’s estate on their death. Although the PRs do not administer the trust property, the trust fund is aggregated for IHT as if the life tenant owned it. The tax is normally borne by the trust fund.

- Discretionary trusts fall within the relevant property regime. No IHT is charged on any beneficiary’s death, but trustees may face ten-year charges and exit charges.

- Bare trust assets are treated as belonging to the beneficiary for IHT. If the beneficiary dies while absolutely entitled, the assets are part of their death estate.

- Excluded property held in certain offshore trusts (where the settlor was non-UK domiciled and the assets are non-UK situs, subject to anti-avoidance rules for UK residential property) is outside the UK IHT estate.

Jointly owned property, life interests in trust property, and gifts with reservation of benefit may be included in the death estate for IHT purposes even though they do not pass to the PRs for succession. For example, a deceased’s beneficial interest in a joint tenancy is brought into account for IHT (though the property passes by survivorship), and an IPDI trust fund is taxed in the life tenant’s estate. By contrast, life policy proceeds written in trust and discretionary pension death benefits are typically outside the IHT estate because the deceased had no beneficial entitlement immediately before death.

Exam Warning

In SQE1 questions, check whether the deceased held property as a trustee, as a life tenant, or as an absolute beneficiary. Only property held as a trustee or as a limited beneficiary (e.g. life interest) passes outside the estate. Absolute interests in trust property usually fall into the estate. For tax, remember that an IPDI fund is taxed in the life tenant’s estate, while discretionary trust property is not; life policy proceeds and discretionary pension benefits paid to others are generally outside the IHT estate.

From a practical standpoint, assets passing outside the estate can provide beneficiaries with immediate funds without waiting for a grant (for example, life policy proceeds written in trust or discretionary pension benefits). Conversely, PRs must fund IHT due before a grant without relying on such trust assets, unless beneficiaries agree to assist.

Revision Tip

Focus on the distinction between legal and equitable ownership, and be able to identify when trust property is excluded from the estate for administration and tax. Be precise about IPDIs versus discretionary trusts, and the consequences for IHT.

Worked Example 1.5

J’s will leaves residue on trust: income to spouse K for life, remainder to their children. J dies; later K dies. Is the trust fund part of K’s estate for IHT?

Answer:

Yes, if K’s life interest was an IPDI, the trust fund is taxed as part of K’s estate for IHT on K’s death (the tax is borne by the trust fund). For succession, K’s interest ends and capital passes to the children under the trust, outside K’s estate administration.

Worked Example 1.6

Trustees hold a rental property on trust for L for life, remainder to M. The trustees propose selling the property to one trustee at market value. Is this permissible?

Answer:

No. A trustee purchasing trust property is prohibited self-dealing. Even if the price is market value and the sale is open, beneficiaries can set aside the transaction. Only exceptional court-sanctioned circumstances could permit it.

Key Point Checklist

This article has covered the following key knowledge points:

- Trust property passes outside the estate when the deceased held only legal title (as trustee) or a limited beneficial interest (e.g. life interest).

- Legal ownership is held by trustees; equitable ownership is held by beneficiaries.

- Co-ownership of land creates a trust of land by statute; survivorship applies to beneficial joint tenancies, distinct shares under tenancies in common pass via will/intestacy.

- Main types of trust relevant to estate planning are discretionary trusts, interest in possession trusts (including IPDIs), bare trusts, and excluded property trusts.

- Discretionary trusts are subject to the relevant property regime (ten-year and exit charges); IPDI funds are taxed in the life tenant’s estate on death.

- Life policy proceeds written in trust and discretionary pension death benefits are paid outside the estate and are generally outside the IHT estate.

- Trustees have duties to manage trust property for beneficiaries (including care, investment, segregation, impartiality, accounting) and may be personally liable for breach of trust; prohibited self-dealing is voidable.

- Trusts do not fail on a trustee’s death; replacement trustees can be appointed and trust property vested in them; shares often require specific transfer formalities.

- Trust property passing outside the estate is not available for distribution by personal representatives and is generally not available to meet the deceased’s personal debts.

Key Terms and Concepts

- legal ownership

- equitable (beneficial) ownership

- trust of land

- interest in possession

- immediate post-death interest (IPDI)

- remainderman

- discretionary trust

- relevant property

- bare trust

- power of maintenance

- power of advancement

- self-dealing

- trustee

- beneficiary