Learning Outcomes

This article outlines record-keeping obligations under the SRA Accounts Rules, including:

- The core requirements for client ledgers, cashbooks, reconciliations, accountants’ reports, and supporting documentation needed to satisfy Rule 8

- The regulatory purpose of accounting records and how they demonstrate compliance, promote transparency, and protect client money in practice

- The minimum six‑year retention periods for accounting records and the reasons these time limits are tested in SQE1 questions

- The distinct record-keeping obligations for joint accounts and a client’s own account, contrasted with those applicable to general client accounts

- The requirement to obtain five‑weekly bank statements and perform three‑way reconciliations, with emphasis on resolving discrepancies promptly

- The need for a central record of bills and written notifications of costs, and how this links to withdrawals from client account

- The role of the transfers journal in evidencing inter‑ledger movements, including inter‑client and inter‑matter transfers and residual balance clearances

- Common exam traps, such as confusing business and client records, overlooking the five‑week rule, or misunderstanding when accountants’ reports must be delivered to the SRA

SQE1 Syllabus

For SQE1, you are required to understand the record-keeping requirements under the SRA Accounts Rules, with a focus on the following syllabus points:

- the obligation to keep accurate, contemporaneous, and chronological accounting records for client and business money

- the specific records required (client ledgers, cashbooks, reconciliations, bills, etc.)

- the process and timing of bank reconciliations

- the retention period for accounting records

- the purpose and content of accountants’ reports and when they must be delivered to the SRA

- the consequences of inadequate record-keeping for compliance and client protection

- the requirement to obtain statements and reconcile at least every five weeks, and to keep a central record of bills and a transfers journal

- the limited record-keeping that applies when operating joint accounts and a client’s own account, and how those obligations differ from general client account records

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the minimum period for which a law firm must retain client accounting records under the SRA Accounts Rules?

- Which of the following must be included in a law firm’s accounting records?

- a) client ledgers

- b) cashbooks

- c) bank statements

- d) all of the above

- How often must a law firm reconcile its client bank account(s) with its internal records?

- True or false? Only qualified accountants’ reports must be delivered to the SRA.

Introduction

Accurate record-keeping is a central requirement of the SRA Accounts Rules. Law firms must keep detailed, up-to-date records of all financial transactions involving client and business money. These records are essential for demonstrating compliance, protecting client funds, and enabling effective supervision by the SRA. Failure to maintain proper records can result in regulatory action and puts client money at risk. The Rules also demand that firms have systems and controls proportionate to the nature and volume of client transactions, including frequent bank statement reviews and reconciliations, and that managers are accountable for ensuring those systems are operated effectively.

Record-Keeping Obligations under the SRA Accounts Rules

The Purpose of Record-Keeping

The SRA Accounts Rules require law firms to keep client money safe and to demonstrate compliance through proper records. Good record-keeping:

- enables firms to track all receipts and payments for each client

- supports the separation of client and business money

- allows for prompt identification and correction of errors or breaches

- provides evidence for regulatory inspections and accountants’ reports

- ensures client money is available on demand unless a different arrangement is agreed in writing

- supports the detection and clearance of residual balances and helps evidence fair payment of interest where applicable

- underpins effective COFA oversight and timely reporting of material breaches

Required Accounting Records

Firms must keep a range of records to comply with Rule 8 of the SRA Accounts Rules.

SRA Accounts Rules record-keeping obligations are presented by reference to core principles, required records, compliance processes, accountants’ reports, and non-compliance consequences.

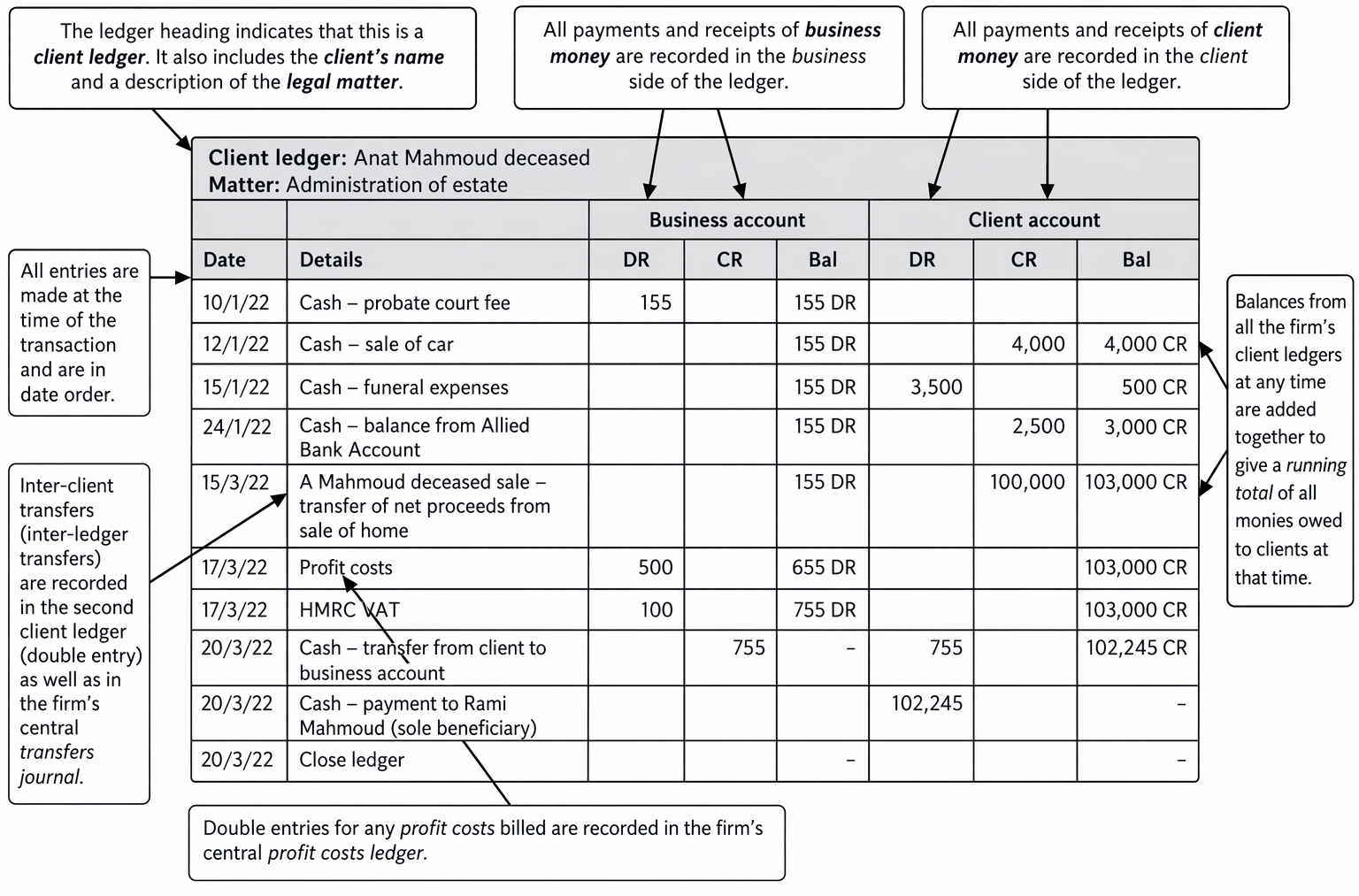

Key Term: client ledger

A record showing all receipts and payments of client and business money for each client and each legal matter, including running balances and sufficient narrative to identify the transaction and its purpose. Key Term: cashbook

A record of all receipts and payments through the firm’s client bank account(s) and business bank account(s), showing running totals and clear cross-references to the ledgers. Key Term: reconciliation

The process of comparing the balances on the firm’s internal records (client ledgers and cashbook) with the balances on bank statements, to identify and resolve any differences. Key Term: accountants’ report

An independent report prepared by a qualified accountant confirming whether the firm has complied with the SRA Accounts Rules, focusing on the handling of client money and the adequacy of accounting records. Key Term: transfers journal

A contemporaneous and chronological record of inter-ledger transfers (for example, inter-client or inter-matter transfers), showing the source and destination ledgers, date, amount, and narrative.

Under the SRA’s guidance “Helping you keep accurate client accounting records”, records must be accurate, contemporaneous, and chronological, and include sufficient narrative to understand the transaction. Each client ledger should identify the client and matter clearly (for example, “Client: A Smith; Matter: Purchase of 1 Property Road”) so that the money held and the transactions recorded can be linked unambiguously to the correct matter.

Types of Records Required

Firms must keep, as a minimum:

- a separate client ledger for each client and each matter

- a cashbook for all client bank accounts

- a cashbook for business bank accounts (strongly recommended)

- bank statements for all accounts

- a central record or file of all bills and written notifications of costs

- records of all inter-client transfers

- records of all reconciliations and supporting documents

In addition to the above, firms should keep:

- a transfers journal capturing all inter-ledger movements (for example, between a sale matter and a will drafting matter for the same client)

- specific records for any separate designated deposit client accounts or deposit columns on the client ledger to track receipts, payments, and interest arising

- schedules of residual balances and actions taken to clear them

- where relevant, a central register of joint accounts and client’s own accounts operated by the firm, together with the five‑weekly statements required for those accounts

Frequency and Process of Reconciliation

Firms must obtain bank statements for all client and business accounts at least every five weeks. Reconciliation of the client bank account(s) with the client ledgers and cashbook must also be completed at least every five weeks. Any discrepancies must be investigated and resolved promptly.

In practice, firms should perform a three-way reconciliation:

- total of the client ledger balances (client side) compared to

- the balance per the client cashbook, and

- the balance per the client bank statement(s)

Reconciling items such as unpresented cheques and uncleared lodgements should be listed and tracked to resolution. The reconciliation statement and supporting schedules should be signed off by an appropriate manager or the COFA, retained, and accompanied by documented explanations and corrective entries where differences are found. Persistent or unexplained differences must be escalated, investigated, and corrected without delay.

Retention of Records

All accounting records must be retained securely for at least six years from the date of the last entry. This includes ledgers, cashbooks, bank statements, bills, reconciliations, and supporting documentation. Where records are electronic, they should be stored in a format that cannot be altered and be reproducible quickly in printed form. Firms should maintain records centrally and ensure they can readily demonstrate compliance to the SRA on request.

For joint accounts and client’s own accounts operated by the firm, the Rules require that statements (or duplicate statements) be obtained at least every five weeks and retained in an accessible form for at least six years. Where electronic statements are relied upon, they must be saved in a durable, non-editable format.

Accountants’ Reports

Most firms must obtain an accountants’ report within six months of the end of each accounting period if they have held or received client money, or operated a joint account or a client’s own account as signatory. Only qualified reports (those showing a significant breach or risk to client money) must be delivered to the SRA. Firms holding only small amounts of client money or only Legal Aid Agency money may be exempt.

The reporting accountant exercises professional judgment, with a focus on risks to client money and whether the firm’s records and reconciliations meet Rule 8. Typical matters reviewed include the completeness and timeliness of ledger postings, the adequacy and frequency of reconciliations, whether client money is segregated and available on demand, and whether withdrawals from client account are properly supported (for example, by a bill or written notification of costs and clear instructions). Firms should ensure their records and reconciliations are in order throughout the year; the accountant’s report is not a substitute for robust ongoing compliance.

Worked Example 1.1

A law firm receives client money for a conveyancing matter. What records must the firm keep, and how often must it reconcile its client account?

Answer:

The firm must keep a client ledger for the matter, a cashbook for the client account, and retain all bank statements. It must reconcile the client account with its internal records at least every five weeks, investigating and correcting any differences.

Worked Example 1.2

A firm’s accountant discovers that the client ledger balances do not match the client account bank statement at the five-week reconciliation. What should the firm do?

Answer:

The firm must promptly investigate and resolve the discrepancy before signing off the reconciliation. If the difference cannot be resolved, the firm’s COFA should be informed, and the SRA may need to be notified if client money is at risk.

Worked Example 1.3

You are preparing the five-week reconciliation. The bank statement shows £1,000,000 in the client account. The client cashbook shows £999,500. The total of client ledger balances shows £999,500. There is a list of unpresented cheques totalling £500. How should you document and sign off this reconciliation?

Answer:

Record a three-way reconciliation showing the ledger total (£999,500) agrees to the cashbook (£999,500). Reconcile the bank statement (£1,000,000) by listing reconciling items, including £500 of unpresented cheques, to explain the difference. Retain the reconciliation, schedules of reconciling items, and supporting documents. Ensure a manager/COFA signs and dates the reconciliation and that reconciling items are tracked to resolution at the next reconciliation.

Worked Example 1.4

Your firm operates a joint account with an executor on a probate matter and is also signatory on a client’s own account under a lasting power of attorney. What record-keeping and reconciliation obligations apply?

Answer:

For both the joint account and the client’s own account, obtain bank statements at least every five weeks and retain them. For the client’s own account, complete reconciliations at least every five weeks. Keep a central record of any bills or written notifications of costs relating to these accounts. Retain the records in an accessible form for at least six years.Exam Warning: If a firm fails to keep accurate, contemporaneous, and chronological records, or does not reconcile its client account at least every five weeks, this is a breach of the SRA Accounts Rules. Such breaches must be corrected promptly and may result in regulatory action. Repeated failures to retain bank statements or reconciliation evidence, use of client account as a banking facility, or inability to demonstrate segregation and availability of client money on demand are all red flags.

Revision Tip: For SQE1, memorise the required records, the five-week reconciliation rule, and the six-year retention period. These are frequent exam topics. Also remember the need for a central record of bills and a transfers journal, and that only qualified accountants’ reports are delivered to the SRA.

Key Point Checklist

This article has covered the following key knowledge points:

- Law firms must keep accurate, up-to-date, and chronological accounting records for all client and business money.

- Required records include client ledgers, cashbooks, bank statements, bills, reconciliation statements, and a transfers journal for inter-ledger movements.

- Reconciliation of client bank accounts with internal records must be done at least every five weeks, and differences must be investigated and corrected promptly.

- All accounting records must be retained securely for at least six years and be reproducible quickly if electronic.

- Most firms must obtain an accountants’ report within six months of the end of each accounting period; only qualified reports must be delivered to the SRA.

- Limited record-keeping applies to joint accounts and a client’s own account operated by the firm (five-week statements and, for the client’s own account, five-week reconciliations).

- Failure to comply with record-keeping obligations is a breach of the SRA Accounts Rules and may result in regulatory action.

Key Terms and Concepts

- client ledger

- cashbook

- reconciliation

- accountants’ report

- transfers journal