Learning Outcomes

This article examines trustees' liability for breach through proprietary claims in the SQE1 context, including:

- the distinction between personal and proprietary claims and why proprietary relief is often strategically preferable in exam scenarios

- the circumstances in which a beneficiary may assert a proprietary claim, with emphasis on clean substitutions, identifiable substitutes, and ongoing equitable proprietary interests

- how to differentiate clean substitutions from following assets and to apply the concepts of following and tracing in problem questions

- the core requirements for a successful proprietary claim and how to structure a clear, exam-ready answer using those elements

- the range of proprietary remedies available, including constructive trusts and equitable liens, and the factors guiding election between them

- how mixing, bank account rules, lowest intermediate balance, and multi-beneficiary contributions affect tracing and allocation of recoveries

- the impact of third-party rights, including the protection afforded to a bona fide purchaser for value without notice and the vulnerability of volunteers and recipients with notice

- typical pitfalls and limitation points that can defeat or restrict proprietary claims, such as dissipation, loss of identifiability, and breaks in the tracing chain

SQE1 Syllabus

For SQE1, you are required to understand the circumstances in which a beneficiary may assert a proprietary claim against a trustee for breach of trust, with a focus on the following syllabus points:

- the distinction between personal and proprietary claims for breach of trust

- the requirements for a proprietary claim, including tracing, clean substitutions, and following assets

- the legal consequences of a trustee substituting trust property for another asset

- the remedies available to beneficiaries where trust property has been misapplied or substituted

- election between remedies: claiming the asset (constructive trust) or taking an equitable lien/charge

- tracing into mixed funds and bank accounts, including pro rata sharing and lowest intermediate balance rules

- priority of proprietary claims in insolvency and the impact of assets passing to a bona fide purchaser for value without notice.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is a "clean substitution" in the context of breach of trust?

- Which of the following is required for a beneficiary to assert a proprietary claim against a trustee?

- a) The trustee must be solvent

- b) The beneficiary must have an equitable proprietary interest in the property

- c) The property must have increased in value

- d) The trustee must have acted honestly

- True or false? If a trustee uses trust money to buy a new asset without mixing it with other funds, the beneficiaries can claim the new asset.

- What is the main difference between following and tracing in trust law?

Introduction

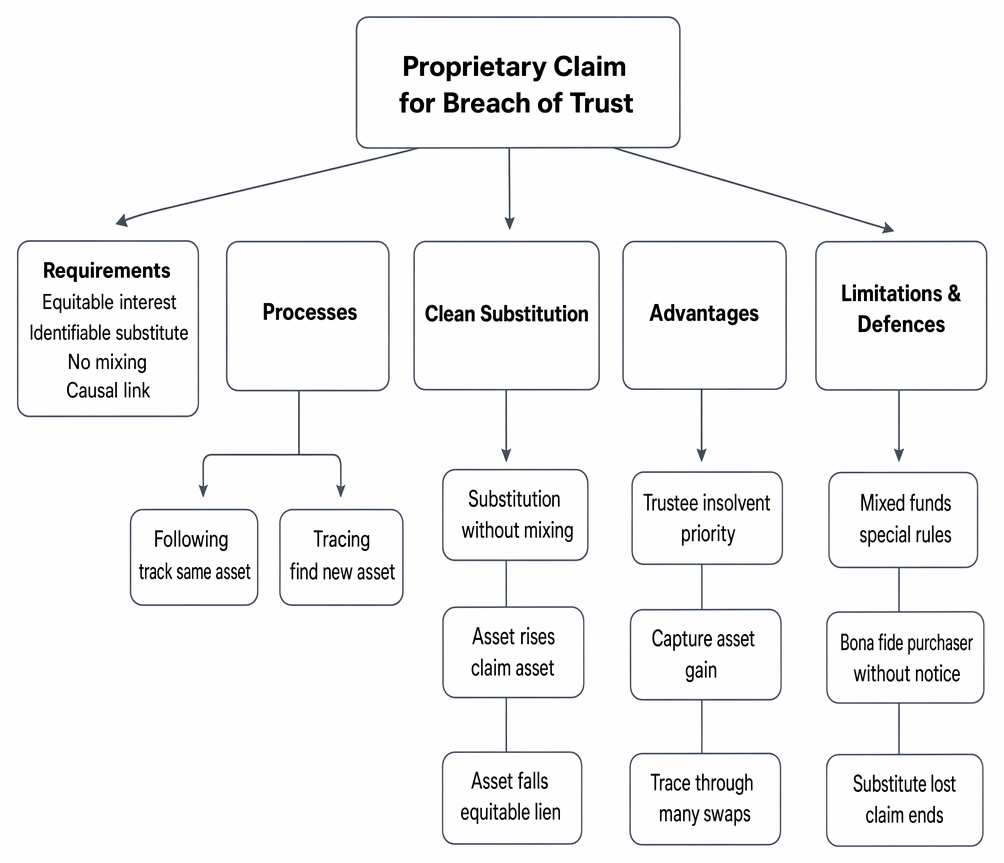

When a trustee breaches trust by misapplying trust property, beneficiaries may seek to recover their loss through a personal claim or, in some cases, a proprietary claim. Proprietary claims are especially important where the trustee is insolvent or the trust property has been substituted for another asset. This article explains the principles of proprietary claims, focusing on clean substitutions and the process of following assets, and outlines how beneficiaries can trace and recover property in these situations.

Proprietary claims for breach of trust are summarised by reference to requirements, following, tracing, clean substitutions, remedies, and defences.

A proprietary claim targets specific property. If the misapplied property (or its substitutes) is still identifiable and has not passed to a bona fide purchaser for value without notice, beneficiaries can assert proprietary rights and recover the asset itself or secure a charge over it. By contrast, a personal claim seeks compensation from the trustee’s general assets and competes with unsecured creditors.

Key Term: proprietary claim

A claim by a beneficiary to recover specific property (or its substitute) in which they have an equitable proprietary interest, rather than a claim for compensation from the trustee personally.

Proprietary claims engage the equitable rules of following and tracing. Following tracks the same asset as it changes hands. Tracing identifies the substitute acquired with misapplied funds and connects it back to the beneficiary’s equitable interest. In practice, beneficiaries often have a choice of proprietary remedy: claim the substitute asset by way of a constructive trust, or take an equitable lien (charge) for the amount misapplied. Which remedy is more advantageous depends on whether the substitute has gained or lost value.

Key Term: constructive trust

An equitable remedy by which a court treats specific property as held for the beneficiaries, allowing them to claim the asset itself and any increase in its value. Key Term: equitable lien

A proprietary security interest that gives the beneficiary a charge over an asset to secure repayment of the misapplied trust money, typically used where the substitute has decreased in value.Test Tip: In SQE-style questions on Clean substitutions and following assets, identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

Proprietary Claims: Overview

A proprietary claim allows a beneficiary to assert rights over specific property, rather than merely seeking compensation from the trustee’s personal assets. This is particularly valuable if the trustee is bankrupt or the substituted property has increased in value.

Beyond choosing between remedies, note these core consequences:

- an increase in the value of the substituted asset belongs to the beneficiaries if they claim the asset

- a decrease in value can be addressed by taking an equitable lien for the amount of trust money used

- proprietary rights generally take priority over unsecured creditors in the trustee’s insolvency

- proprietary rights can be asserted against volunteers and recipients with notice, but will be defeated by a bona fide purchaser for value without notice

Key Term: bona fide purchaser for value without notice

A person who acquires legal title to property for value and without notice of any prior equitable interest. This purchaser takes free of the beneficiaries’ equitable proprietary rights.

Clean Substitutions

A clean substitution occurs when a trustee uses trust property to acquire a new asset, without mixing the trust property with other funds. The new asset is directly traceable to the original trust property.

Key Term: clean substitution

The exchange of trust property for a new asset, where the new asset is acquired solely using trust property and remains identifiable.

If a trustee sells trust shares and uses the proceeds to buy a car, the car is a clean substitution for the original shares. The beneficiaries may claim the car, or, if the car has decreased in value, may claim a charge over it for the amount of trust money used.

The availability of a proprietary claim does not depend on the trustee’s honesty. It depends on the beneficiaries’ equitable proprietary interest and the asset’s identifiability. If the substitute asset is held by the trustee or by a volunteer, the beneficiaries can recover it; if it has been passed to a bona fide purchaser for value without notice, the proprietary claim is lost and the beneficiaries must look to personal remedies.

Worked Example 1.1

A trustee sells trust-held shares for £30,000 and uses the entire sum to purchase a painting. The painting later appreciates to £40,000. Can the beneficiaries claim the painting?

Answer:

Yes. The painting is a clean substitution for the original trust property. The beneficiaries may claim the painting itself, including any increase in value. If multiple clean substitutions occur in sequence (for example, trust funds buy Asset A, which is sold to buy Asset B, then sold to buy Asset C), beneficiaries can continue to trace through each substitution so long as the chain remains clear and the assets are identifiable.

Worked Example 1.2

A trustee transfers trust money to buy a car, then sells the car and uses the proceeds to buy a boat. Can the beneficiaries claim the boat?

Answer:

Yes. The beneficiaries can trace the trust money through the car to the boat, provided each substitution is clear and the property remains identifiable. Where a clean substitution has decreased in value, beneficiaries can protect themselves by taking an equitable lien (charge) for the amount misapplied rather than claiming the asset itself. This ensures they recover the full sum used, if necessary from sale proceeds, without being exposed to market loss.

Worked Example 1.3

A trustee misapplies £10,000 of trust funds to buy a car, which later falls in value to £7,000. What are the beneficiaries’ options?

Answer:

The beneficiaries may claim a charge over the car for £10,000 (the amount misapplied), allowing them to recover the loss from the sale proceeds.

Following and Tracing Assets

When trust property is misapplied, beneficiaries may need to identify its location or substitute. Two related concepts are used:

Key Term: following

The process of tracking the same asset as it moves from one person to another. Key Term: tracing

The process of identifying a new asset that has been substituted for the original trust property, allowing the beneficiary to assert a claim over the substitute.

Following is used when the property itself is transferred. Tracing is used when the property is exchanged for something else. Both are essential for establishing a proprietary claim.

Successful tracing in equity requires:

- an existing equitable proprietary interest (beneficiaries under a trust satisfy this)

- the misapplied property (or its substitute) to be identifiable

- no break in the chain caused by dissipation (for example, money spent on a holiday with no enduring traceable product)

- no transfer to a bona fide purchaser for value without notice

Special rules apply to mixed funds and bank accounts. In equity, where trust money is mixed with a trustee’s own money, courts may presume the trustee spends their own money first, protecting the beneficiaries’ entitlement to trace into any remaining balance or identifiable purchase. Beneficiaries also have a “first charge” over identifiable assets bought with mixed funds, ahead of the trustee’s claim.

In bank accounts, if misapplied trust money is paid into an overdrawn account, the deposit is immediately dissipated to reduce the overdraft and cannot be traced further. If the account remains in credit, tracing will consider the lowest intermediate balance: if the balance falls below the amount misapplied and later increases, the beneficiaries’ claim is limited to that lower figure.

Worked Example 1.4

A trustee transfers £60,000 of trust money into a personal bank account with a £20,000 existing credit balance. The trustee then withdraws £20,000 to purchase a sculpture and later spends the rest on holidays. The sculpture is now worth £30,000.

Answer:

The beneficiaries can assert a first charge over the sculpture to secure £20,000 (the amount of trust money used to buy it). The rest of the trust money was dissipated on holidays and cannot be traced. Any uplift in the sculpture’s value belongs to the beneficiaries if they elect to claim the sculpture itself by constructive trust rather than a lien. Where mixed funds from different trusts are used to buy one asset, each trust shares in the asset or its proceeds proportionately to its contribution.

Worked Example 1.5

A trustee uses £15,000 from Trust A and £5,000 from Trust B to buy a car. The car is sold for £10,000 after the trustee’s insolvency. How should the beneficiaries recover?

Answer:

Each trust recovers proportionately from the £10,000 sale proceeds. Trust A takes £7,500 and Trust B takes £2,500, reflecting their contributions.

Requirements for a Proprietary Claim

To bring a proprietary claim for a clean substitution, the following must be established:

- The claimant has an equitable proprietary interest in the original trust property.

- The property has been substituted for another asset (cleanly, without mixing).

- The substituted asset is identifiable.

- There is a sufficient connection between the original trust property and the substitute.

If these requirements are met, the beneficiary may claim the substitute asset or, if it has decreased in value, may claim a charge (equitable lien) over it for the amount of trust money used. Where mixing has occurred, proprietary relief remains possible, but the rules of equitable tracing apply, including assumptions about spending order, pro rata sharing, and limitations imposed by bank account balances.

Proprietary claims may be asserted against the trustee and against third-party recipients except a bona fide purchaser for value without notice of the beneficiaries’ interest. Volunteers and recipients with notice are vulnerable to proprietary recovery and may be required to yield up the asset or recognise the beneficiaries’ charge.

In choosing the form of proprietary relief, beneficiaries should consider:

- whether the substitute has appreciated or depreciated

- whether there are multiple contributors (pro rata sharing)

- whether a sale is anticipated (a lien can be more practical if immediate sale is likely)

- the priority impact in insolvency (a proprietary interest outranks unsecured creditors)

Advantages of Proprietary Claims

Proprietary claims are especially useful if:

- The substituted asset has increased in value (the beneficiary can claim the full value).

- The trustee is insolvent (the beneficiary can recover the asset ahead of unsecured creditors).

- The property has passed through several substitutions, provided each is clean and traceable.

- The beneficiaries wish to protect their recovery against further dealing by the trustee (a proprietary interest binds successors except bona fide purchasers without notice).

Proprietary relief is often strategically superior to a personal claim because it can capture market gains and avoid dilution with unsecured creditor claims. Beneficiaries should avoid double recovery by electing the remedy that yields the best outcome (claim the asset or take a lien), but not both.

Limitations and Defences

A proprietary claim may fail if:

- The substituted asset cannot be identified.

- The property has been mixed with other funds (in which case different tracing rules apply).

- The property has been transferred to a bona fide purchaser for value without notice (who takes free of the beneficiary’s interest).

- The property has been dissipated (spent on services or consumables leaving no enduring asset), breaking the chain of traceability.

In equity, relief is discretionary and responsive to fairness. Although an innocent volunteer is generally subject to proprietary recovery of traceable assets, there may be circumstances—such as improvements to a modest home funded innocently—where the court adjusts or declines relief to avoid an inequitable outcome. These are exceptional and fact-sensitive; the usual route is a proportionate charge over the improved asset rather than personal liability of the volunteer.

Key Term: lowest intermediate balance

A rule applied to mixed bank accounts: if the account balance falls below the amount misapplied and later increases, the traceable claim is limited to the lowest intervening balance.Exam Warning: If trust property has been mixed with other funds, or passed to a bona fide purchaser for value without notice, the beneficiary’s proprietary claim may be lost or limited. Always check whether the asset is still identifiable and whether any defences apply.

Summary Table: Proprietary Claims and Clean Substitutions

| Scenario | Beneficiary’s Remedy |

|---|---|

| Clean substitution, asset increased value | Claim the substituted asset |

| Clean substitution, asset decreased value | Claim a charge (lien) for original sum |

| Asset mixed with other funds | Apply tracing rules for mixed funds |

| Asset transferred to bona fide purchaser | No proprietary claim |

Key Point Checklist

This article has covered the following key knowledge points:

- Proprietary claims allow beneficiaries to recover specific property or its substitute following a breach of trust.

- A clean substitution occurs when trust property is exchanged for a new asset without mixing with other funds.

- Beneficiaries can follow or trace trust property into substituted assets, provided the asset is identifiable.

- If the substituted asset increases in value, the beneficiary may claim the asset; if it decreases, they may claim a charge for the original amount.

- Proprietary claims may be lost if the asset is mixed or transferred to a bona fide purchaser for value without notice.

- Tracing through mixed funds involves equitable rules, including pro rata sharing and the lowest intermediate balance in bank accounts.

- Beneficiaries can elect between claiming the asset (constructive trust) and taking an equitable lien; choose the remedy that produces the best financial outcome.

- Proprietary claims provide priority over unsecured creditors in insolvency but cannot be asserted against a bona fide purchaser without notice.

Key Terms and Concepts

- proprietary claim

- clean substitution

- following

- tracing

- constructive trust

- equitable lien

- bona fide purchaser for value without notice

- lowest intermediate balance