Learning Outcomes

This article examines proprietary claims against trustees and equitable tracing of trust property in equity, including:

- The distinction between personal and proprietary claims and strategic advantages of proprietary recovery (insolvency, appreciation in value, limitation versus laches)

- Requirements for equitable tracing: initial fiduciary relationship, equitable proprietary interest, and continued identifiability of the property or its traceable proceeds

- Choice of proprietary remedies for substitutions: constructive trust to capture increases in value, and equitable lien or charge where the substitute has fallen in value

- Tracing outcomes in mixed-asset purchases and mixed bank accounts, with core authorities (Re Hallett’s Estate, Re Oatway, Roscoe v Winder) and beneficiary election against a wrongdoing trustee

- Rules for mixtures involving two trusts or an innocent volunteer: pari passu allocation and departures from Clayton’s Case (FIFO) in favour of fairness (Barlow Clowes v Vaughan)

- Limitations on tracing: dissipation, overdrawn accounts, the lowest intermediate balance rule, and the coordinated scheme exception to backwards tracing (Federal Republic of Brazil v Durant)

- Defences and bars to proprietary recovery: bona fide purchaser for value without notice, change of position, and inequitable results involving innocent volunteers (e.g., improvements to pre-owned property)

- Subrogation where misapplied trust funds discharge secured debts

- Structured worked examples illustrating key tracing and proprietary claim scenarios

SQE1 Syllabus

For SQE1, you are required to understand how beneficiaries can recover trust property following a breach of trust through the application of equitable tracing and proprietary remedies, with a focus on the following syllabus points:

- The distinction between personal and proprietary claims against trustees.

- The requirements and rules for equitable tracing.

- How tracing operates where trust funds are mixed with the trustee's own funds or other trust funds.

- The rules for tracing into assets purchased with mixed funds.

- The limits and defences to equitable tracing, such as the bona fide purchaser defence and dissipation.

- The lowest intermediate balance rule and overdrawn accounts.

- The usual bar on backwards tracing and the coordinated scheme exception (Brazil v Durant).

- Allocation rules in mixed claims between two trusts (FIFO/Clayton’s Case and when courts adopt pari passu).

- The availability of subrogation where trust funds discharge secured obligations.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which of the following is a key advantage of a proprietary claim over a personal claim against a bankrupt trustee?

- a) It allows the beneficiary to claim punitive damages.

- b) It gives the beneficiary priority over the trustee's general creditors regarding the specific trust asset or its traceable proceeds.

- c) It is subject to a shorter limitation period.

- d) It does not require proof of a breach of trust.

-

A trustee mixes £10,000 of trust money with £5,000 of their own money in their personal bank account. They then withdraw £8,000 and spend it on a holiday (dissipation). What amount of the remaining £7,000 can the beneficiaries trace in equity?

- a) £2,000

- b) £5,000

- c) £7,000

- d) £10,000

-

What is the primary requirement for equitable tracing to be available?

- a) The trustee must have acted dishonestly.

- b) The property must have increased in value.

- c) There must be an existing fiduciary relationship.

- d) The beneficiary must be a minor.

Introduction

When a trustee breaches their trust obligations, beneficiaries may suffer loss. While beneficiaries always have a personal claim against the wrongdoing trustee for compensation, this may be inadequate if the trustee is insolvent. Equity provides an alternative route through proprietary claims, which focus on recovering the trust property itself or property acquired with it. This involves the process of tracing, which allows beneficiaries to identify trust assets even when they have been mixed with other property or changed form. Understanding proprietary claims and equitable tracing is essential for advising beneficiaries on how to recover misappropriated trust assets.

A proprietary claim is often preferable where:

- The trustee (or recipient) is insolvent and the claimant wants priority to a specific asset or its proceeds.

- The misapplied property has increased in value and the claimant seeks to capture the uplift.

- A personal compensation claim is time-barred but a proprietary claim is still available in equity, subject to laches.

Key Term: Fiduciary relationship

A relationship of trust and confidence where one party (the fiduciary, e.g., a trustee) owes duties of loyalty and utmost good faith to another (the principal or beneficiary). Key Term: Following

The process of identifying the original trust asset as it passes from one person to another. Key Term: Tracing

The process of identifying the value of the claimant's property in other assets which have been substituted for the original property.Test Tip: In SQE-style questions on Tracing trust property in equity, identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

Exam Warning: Do not rely on a familiar phrase from Tracing trust property in equity alone; check whether the facts satisfy every condition, exception, and timing requirement.

Distinguishing Personal and Proprietary Claims

It is important to distinguish between personal and proprietary claims arising from a breach of trust.

A personal claim is brought against the trustee individually. The aim is to compel the trustee to compensate the trust fund for the loss caused by the breach, using their own personal assets. If the trustee is bankrupt, the beneficiaries will rank alongside other unsecured creditors, and recovery may be limited. A personal claim can also be pursued against certain third parties (e.g., knowing receipt or dishonest assistance), but those are typically personal liabilities and do not, by themselves, confer a proprietary interest in assets held by the wrongdoer.

A proprietary claim, conversely, asserts ownership rights over specific assets. The beneficiary claims that the trust property (or property representing it) still belongs beneficially to the trust, even if it is in the hands of the trustee or a third party (unless they are a bona fide purchaser for value without notice). This claim gives the beneficiary priority over the trustee's general creditors in insolvency and allows recovery of the specific asset or its traceable product, including any increase in value. It is not subject to the statutory six-year limitation applicable to most personal claims for breach of trust when brought “to recover trust property or its proceeds” from a trustee, but it remains subject to equitable defences such as laches.

The practical difference is often seen in the remedy sought:

- A constructive trust over the substitute asset to capture gains and assert priority.

- An equitable lien (or charge) to secure repayment of the amount misapplied where the substitute has depreciated.

Key Term: Constructive trust

An equitable mechanism by which the court recognises that a defendant must hold property for the claimant, typically to prevent unjust enrichment or vindicate pre-existing property rights. Key Term: Equitable lien

A proprietary security right affixed to a specific asset, enabling the claimant to force a sale and take the amount due from the proceeds in priority to unsecured creditors.

Equitable Tracing: Core Principles

Equitable tracing is the process used to identify trust property that has been wrongfully mixed with other property or converted into a different form. It allows beneficiaries to follow the value of the trust asset through substitutions.

For equitable tracing to be available, certain conditions must generally be met:

- Fiduciary Relationship: There must have been an initial fiduciary relationship (e.g., trustee-beneficiary). In practice this is rarely contentious in trust breach scenarios.

- Equitable Proprietary Interest: The claimant must have an equitable proprietary interest in the property being traced — a trust beneficiary ordinarily does.

- Traceable Property: The property must still exist in some identifiable form, whether original or substituted, and not have been dissipated.

- Equitable Discretion: Tracing must not produce an inequitable result (especially against innocent volunteers), and undue delay may bar relief via laches.

It is useful to distinguish between 'following' and 'tracing'.

Key Term: Following

The process of identifying the original trust asset as it passes from one person to another. Key Term: Tracing

The process of identifying the value of the claimant's property in other assets which have been substituted for the original property.

Tracing is necessary when the original asset has been replaced by another asset or mixed with other funds. In commercial reality, tracing often occurs across bank accounts. Equity treats a bank account as a fund of value, enabling the identification of contributions and withdrawals by applying presumptions and fair allocation rules.

Tracing into Unmixed Funds

Where a trustee misappropriates trust property and keeps it separate from their own assets, tracing is straightforward.

- If the trustee still holds the original asset, the beneficiaries can simply claim it back (this is 'following').

- If the trustee has exchanged the original asset for a substitute asset (e.g., used trust money to buy shares), the beneficiaries can choose either:

- To claim the substitute asset itself, including any increase in value (using a constructive trust).

- To take an equitable charge (or lien) over the substitute asset to recover the value of the original trust property lost. This is preferable if the substitute asset has decreased in value.

The choice is an election designed to give the beneficiary the better of the two outcomes as against a wrongdoing trustee.

Key Term: Subrogation

An equitable remedy that allows a claimant whose money has discharged another’s secured debt to be placed in the creditor’s shoes and enforce that security to the extent of the discharge.

Worked Example 1.1

A trustee misappropriates £20,000 from the trust fund and uses it to buy a classic car in their own name. The car is now worth £25,000. What proprietary remedy should the beneficiaries seek?

Answer:

The beneficiaries should trace the trust money into the car. As the car (the substitute asset) has increased in value, they should claim ownership of the car itself via a constructive trust, thus capturing the £5,000 increase in value for the trust.

Worked Example 1.2

Assume the same facts as Worked Example 1.1, but the classic car is now only worth £15,000. What proprietary remedy should the beneficiaries seek?

Answer:

The beneficiaries should still trace the trust money into the car. However, as the car has decreased in value, they should claim an equitable charge or lien over the car for the £20,000 misappropriated. This allows them to force the sale of the car and recover £15,000 from the proceeds. They retain a personal claim against the trustee for the remaining £5,000 shortfall.

Worked Example 1.3

A trustee uses £100,000 of trust money to discharge a bank’s registered mortgage over the trustee’s own property. The property is unencumbered after payment, then falls in value. Can the beneficiaries claim a proprietary interest?

Answer:

Yes, via subrogation. The trust is subrogated to the bank’s discharged security to the extent of the payment. The beneficiaries can enforce that security interest against the property (up to £100,000), despite the fall in value.

Tracing into Mixed Funds

Tracing becomes more complex when a trustee mixes trust funds with other money, either their own or funds from another trust. Equity has developed specific rules for these situations.

Trustee Mixes Trust Funds with Own Money in Asset Purchase

If a trustee uses a mixture of trust money and their own money to buy an asset (a 'mixed asset'), the beneficiaries have a choice similar to that for clean substitutions:

- Claim a proportionate share of the asset. This is advantageous if the asset has increased in value.

- Claim an equitable lien over the asset for the amount of trust money used. This is advantageous if the asset has decreased in value.

The choice allows the beneficiary to secure the best outcome against the wrongdoing trustee. Authority supports that a proportionate proprietary share is available where the contribution is ascertainable (e.g., Foskett v McKeown).

Worked Example 1.4

A trustee uses £10,000 of trust money and £10,000 of their own money to buy shares worth £20,000. The shares are now worth £30,000. What can the beneficiaries claim?

Answer:

The beneficiaries can trace into the mixed asset (the shares). Since the trust contributed 50% of the purchase price and the shares have increased in value, they should claim a 50% proportionate share, which is now worth £15,000 (£30,000 x 50%).

Worked Example 1.5

Assume the same facts as Worked Example 1.4, but the shares are now worth only £16,000. What should the beneficiaries claim?

Answer:

Since the shares have decreased in value, the beneficiaries should enforce an equitable lien over the shares for the £10,000 of trust money used. This allows them to recover their £10,000 from the sale proceeds in priority to the trustee claiming their share.

Trustee Mixes Trust Funds with Own Money in Bank Account

Where a trustee deposits trust funds into their personal bank account, mixing them with their own money, and then makes withdrawals, specific rules apply to determine what happens to the trust money:

Equitable tracing after breach of trust is outlined by reference to proprietary and personal claims, mixed funds, substitute assets, and defences.

- Presumption of Honesty (Re Hallett's Estate): The trustee is presumed to spend their own money first. Any money remaining in the account up to the amount of the trust fund is considered trust money.

- Beneficiary's First Choice (Re Oatway): If the Re Hallett presumption would prejudice the beneficiaries (e.g., the trustee buys an asset with early withdrawals and dissipates the rest), the beneficiaries can assert a charge over the earlier withdrawal (or asset purchased with it) first. Equity presumes against the wrongdoer, allowing the beneficiary to choose the rule that best preserves the trust fund.

- Lowest Intermediate Balance Rule (Roscoe v Winder): The beneficiaries' claim against the mixed bank account is limited to the lowest balance the account reached after the trust money was paid in but before any subsequent deposits of the trustee's own money. Later deposits by the trustee are not presumed to replace spent trust money unless that intention is clear.

- No Tracing into an Overdrawn Account: If the account is overdrawn at the relevant time, there is no identifiable property to trace into.

- Backwards Tracing Generally Not Permitted: Claimants ordinarily cannot say that trust money used to repay a prior loan now entitles them to claim the asset originally acquired with that loan. However, there is an important exception.

Key Term: Lowest intermediate balance

The minimum balance in a mixed bank account after the trust money is paid in and before any later deposits. A claimant’s proprietary claim is capped at this figure. Key Term: Backwards tracing

An attempt to trace into assets acquired before misapplied funds are paid into an account used to service or repay the acquisition; generally not allowed in equity unless the transactions form part of a coordinated scheme.

A limited exception to the no backwards tracing rule has been recognised where withdrawals and deposits form part of a coordinated scheme to defeat tracing, so that value and asset acquisition are sufficiently linked. In that event, the court may treat the misapplied funds and the asset purchase as part of the same scheme and permit recovery (Federal Republic of Brazil v Durant International [2016] AC 297 (PC)).

Key Term: Coordinated scheme exception

Where the factual matrix shows a sufficiently connected, planned sequence of steps designed to acquire an asset and launder value, the court may allow tracing notwithstanding strict chronological mismatches. Key Term: Dissipation

The spending or wasting of trust funds in such a way that they cannot be traced into any substitute asset (e.g., spending on general living expenses, holidays, or paying off unsecured debts).

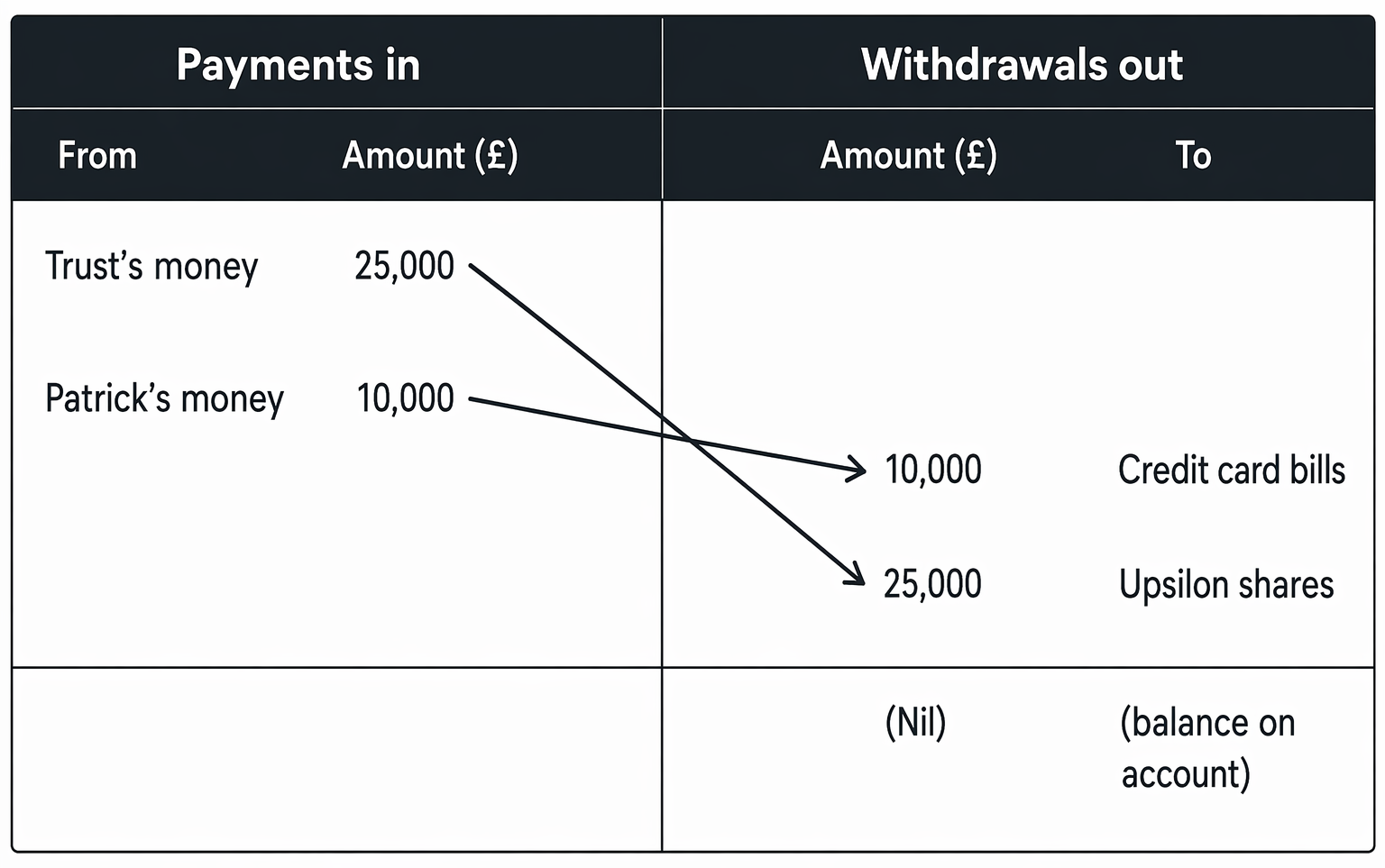

Worked Example 1.6

A trustee pays £5,000 trust money into their bank account, which already contains £2,000 of their own money (Total £7,000). The trustee then withdraws £3,000 for shares and later spends £3,000 on living expenses. £1,000 remains. How can the beneficiaries trace?

Answer:

Applying Re Hallett, the trustee is presumed to spend their own £2,000 first. The first £3,000 withdrawal (for shares) would consist of £2,000 trustee money and £1,000 trust money. The second £3,000 withdrawal (living expenses) would be entirely trust money. The remaining £1,000 would be trust money. This leaves the trust tracing £1,000 into the shares and £1,000 in the account balance, with £3,000 dissipated. However, applying Re Oatway, the beneficiaries can claim a charge over the shares first. The £3,000 withdrawal for shares can be claimed entirely as trust money. The £3,000 spent on living expenses would then be £2,000 trustee money and £1,000 trust money. The remaining £1,000 is trust money. This allows the trust to trace £3,000 into the shares and £1,000 into the account balance, with only £1,000 dissipated. This is the better result for the beneficiaries.

Worked Example 1.7

A trustee pays £20,000 of trust money into an account with an opening balance of £5,000. The trustee then spends £23,000 on various expenses. The balance falls to £2,000. Later, an unrelated client pays £10,000 into the account. What can the beneficiaries claim?

Answer:

The trust’s claim is limited to the lowest intermediate balance of £2,000. The later £10,000 deposit is not presumed to replenish the trust unless there is clear evidence of an intention to do so. The beneficiaries can claim a proprietary right in the £2,000 balance and must sue personally for any shortfall.

Worked Example 1.8

A trustee obtains a short-term loan to buy luxury jewellery on Monday. On Wednesday, the trustee transfers misapplied trust money into the account and repays the loan on Thursday. Can the beneficiaries claim the jewellery under backwards tracing?

Answer:

Ordinarily, no. However, if the evidence shows a coordinated scheme linking the loan, the purchase and the later use of trust funds as part of an overall plan to acquire and retain the jewellery while concealing the source of value, the court may permit tracing into the jewellery notwithstanding the time sequence (Brazil v Durant).

Worked Example 1.9

A trustee pays £10,000 of trust money into a personal account which is already £500 overdrawn and then draws cash which is spent on a holiday. Can the beneficiaries trace into the account?

Answer:

No. An overdrawn balance represents a debt to the bank; there is no identifiable property into which the beneficiaries can trace. The money is dissipated, leaving only a personal claim against the trustee.

Trustee Mixes Funds from Two Trusts or Trust and Innocent Volunteer

Where a trustee mixes funds from two separate trusts, or mixes trust funds with money belonging to an innocent third party (an 'innocent volunteer'), the rules favouring the beneficiary against the wrongdoing trustee do not apply between the two innocent parties.

- Mixed Asset Purchase: If funds from two trusts (or a trust and an innocent volunteer) are used to buy an asset, the parties share ownership of the asset proportionately (pari passu) according to their contributions. They share any increase or decrease in value rateably.

- Mixed Bank Account: If funds from two trusts (or a trust and an innocent volunteer) are mixed in a bank account from which withdrawals are made:

- Clayton's Case Rule (First In, First Out - FIFO): Traditionally, the first money paid into the account is presumed to be the first money paid out.

- Pari Passu Distribution: Courts may depart from FIFO if it is impractical or unjust, and instead divide the remaining funds or assets purchased proportionately between the innocent parties (Barlow Clowes v Vaughan). This is now often preferred, especially where the chronology is arbitrary or records are poor.

Key Term: FIFO

“First in, first out”: the earliest funds paid into a mixed account are deemed the first withdrawn (Clayton’s Case). Key Term: Pari passu

“Rateably” or in proportion: each contributor takes a share corresponding to their contribution, often preferred where FIFO is unfair.

Worked Example 1.10

£10,000 from Trust A and £20,000 from Trust B are paid into a single bank account. £15,000 is used to buy shares; £15,000 is dissipated. How should the shares be allocated?

Answer:

On FIFO, if Trust A’s funds arrived first, the £15,000 share purchase would be attributed to Trust A and B sequentially, which can be arbitrary. A court is likely to adopt a pari passu approach: Trust A contributed one-third, Trust B two-thirds; the beneficial interests in the shares should be 1/3 and 2/3 respectively.

Worked Example 1.11

A charity (an innocent volunteer) receives £50,000 wrongly distributed by personal representatives and uses it to refurbish a building it already owns, increasing amenity but not saleable value. Can the beneficiaries of the estate assert a lien on the building?

Answer:

Generally, no. For improvements to pre-owned property by an innocent volunteer, equity often refuses a proprietary remedy where it would be inequitable (e.g., forcing a sale). The claimant typically has a personal restitutionary claim against the recipient (subject to defences such as change of position). This approach accords with the reasoning seen in Re Diplock-type scenarios.

Defences to Tracing

Even if tracing is possible, certain defences may prevent the beneficiary from recovering the property:

- Bona Fide Purchaser for Value Without Notice (BFPFVWN): Equity's darling. If a third party buys the legal title to the trust property (or its traceable product) for valuable consideration, in good faith, and without actual, constructive, or imputed notice of the beneficiary's interest, the beneficiary's equitable interest is extinguished. Tracing stops here.

- Dissipation: As noted, if the trust property or its traceable proceeds have been dissipated (e.g., spent on a holiday, general living expenses, or used to pay unsecured debts), there is no asset left to trace into. The proprietary claim fails, though a personal claim against the trustee remains.

- Inequitable Result: Tracing may be denied if it would produce an unfair result, particularly against an innocent volunteer. For example, if an innocent volunteer uses trust money to make improvements to their existing property which do not necessarily increase its sale value (or where forcing a sale would be highly unfair), the court may refuse a proprietary claim (often illustrated by Re Diplock-style reasoning).

- Change of Position: An innocent volunteer who receives trust property in good faith and subsequently changes their position relying on the receipt (e.g., spends the money in an extraordinary way they wouldn't otherwise have done) may have a defence against a personal claim for restitution, and potentially a reason why a proprietary remedy would be inequitable in the circumstances.

- Laches/Delay: Equitable proprietary claims are subject to laches; undue delay that prejudices the defendant may bar relief.

- Overdrawn Accounts: No proprietary tracing is possible where the relevant account is in overdraft at the trace point.

Key Term: Bona fide purchaser

A purchaser who gives value, acts in good faith, and acquires the legal estate without notice (actual, constructive or imputed) of the equitable interest; takes free of that interest. Key Term: Change of position

A defence available primarily to an innocent recipient of mistakenly paid money (or trust property) who has subsequently altered their position in reliance on the receipt, making it inequitable to require full repayment.

Worked Example 1.12

Trust money is used to buy a watch which is then sold to a retail buyer who pays full price, takes legal title and has no notice. Can the beneficiaries claim the watch from the buyer?

Answer:

No. The buyer is a bona fide purchaser for value of the legal estate without notice; the equitable interest is extinguished on transfer and tracing stops. The beneficiaries may pursue the proceeds in the seller’s hands (if identifiable) or bring personal claims against the wrongdoer.

Key Point Checklist

This article has covered the following key knowledge points:

- Beneficiaries can bring personal claims (for compensation) or proprietary claims (to recover assets) against trustees for breach of trust.

- Proprietary claims offer advantages, especially if the trustee is insolvent or the trust property has increased in value.

- Equitable tracing allows beneficiaries to identify trust property even when mixed or substituted, provided a fiduciary relationship existed and the property is identifiable.

- Following tracks the original asset; tracing tracks its value into substitutes.

- Beneficiaries may elect between a proportionate proprietary share or an equitable lien over mixed assets purchased by a wrongdoing trustee.

- Specific rules apply when tracing into mixed funds, depending on whether the funds are mixed with the trustee's own money (Re Hallett, Re Oatway) or with funds of another innocent party (Clayton's Case, Pari Passu).

- The lowest intermediate balance rule limits claims on mixed bank accounts; no tracing into overdrawn accounts.

- Backwards tracing is generally prohibited, subject to the coordinated scheme exception (Brazil v Durant).

- Subrogation may provide a proprietary response where trust money discharges a secured debt.

- Defences to tracing include the bona fide purchaser for value without notice, dissipation of the property, change of position, and where tracing would lead to an inequitable result (especially against innocent volunteers), plus laches.

Key Terms and Concepts

- Fiduciary relationship

- Following

- Tracing

- Constructive trust

- Equitable lien

- Bona fide purchaser

- Lowest intermediate balance

- FIFO

- Pari passu

- Backwards tracing

- Coordinated scheme exception

- Subrogation

- Dissipation

- Change of position