Learning Outcomes

This article covers money laundering offences and compliance duties in legal and financial services practice, including:

- The principal POCA offences (s.327–s.329), criminal property, and knowledge/suspicion thresholds

- The stages and methods of laundering in legal practice (placement, layering, reintroduction)

- When and how to make SARs, the MLRO’s role, DAML consent, response and moratorium periods

- The distinction between regulated sector duties (failure to disclose, tipping off) and general duties outside the sector

- Customer due diligence: identification, verification, beneficial ownership, ongoing monitoring, and risk-based EDD for PEPs/high-risk jurisdictions

- Defences and exemptions: authorised disclosure, privileged circumstances/legal professional privilege, and adequate consideration

- Communication risks and the offences of tipping off and prejudicing investigations, with practical guidance on client interactions

- Recordkeeping, training, and internal AML policies under the Money Laundering Regulations 2017 and supervisory expectations

- The MLRO’s responsibilities for internal reporting, NCA liaison, staff training, and transactional controls

- Application of these rules to realistic fact patterns to manage risk and proceed lawfully

SQE2 Syllabus

For SQE2, you are required to understand the legal framework for money laundering from a practical standpoint, with a focus on the following syllabus points:

- The main criminal offences relevant to money laundering under UK law.

- The legal and regulatory duties imposed on solicitors and firms regarding money laundering prevention.

- The requirements for suspicious activity reporting, including timing, procedure, and correct recipients.

- The scope of customer due diligence and identification obligations.

- The role of defences, including privileged circumstances and adequate consideration.

- The offences of tipping off and prejudicing an investigation, and the scope of exceptions.

- The application of anti-money laundering procedures to typical legal practice scenarios.

- The distinction between regulated sector duties and general duties under POCA (including the mental state threshold for disclosure).

- The role and responsibilities of the MLRO (nominated officer) within firms.

- The consent (“DAML”) process, moratorium period, and practical transaction controls.

- Risk-based due diligence, including enhanced due diligence for politically exposed persons and high-risk jurisdictions.

- Recordkeeping and training obligations under the Money Laundering Regulations 2017, and interaction with Terrorism Act reporting.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which of the following is NOT a principal money laundering offence under English law?

- a) Concealing

- b) Arranging

- c) Failing to keep client ledgers

- d) Acquisition, use, or possession

-

In which situation must a solicitor make a suspicious activity report?

- a) They have mere curiosity about a client’s transactions.

- b) They know or suspect that a client is engaged in money laundering.

- c) A client refuses to pay their bill.

- d) A client withdraws from a proposed transaction for legitimate reasons.

-

Which defence may excuse a solicitor from the duty to make a suspicious activity report?

- a) The information is covered by legal professional privilege

- b) The solicitor believes the client is honest

- c) The client is located abroad

- d) The client has paid upfront

-

True or false? Tipping off is always an offence, even when the solicitor is seeking further information from a client about the origins of funds.

Introduction

Money laundering law is a core SQE2 topic. Candidates must understand how money laundering offences apply in practice and what duties are imposed on solicitors and financial service professionals. Key focus areas are the principal criminal offences, regulatory obligations, reporting requirements, and common defences. The Proceeds of Crime Act 2002 (POCA) sets out the principal offences and the reporting regime, while the Money Laundering, Terrorist Financing and Transfer of Funds (Information on the Payer) Regulations 2017 (MLR 2017) require firms to implement systems, policies, customer due diligence, training, and internal reporting procedures to prevent misuse of legal services for laundering. The National Crime Agency (NCA) administers the suspicious activity reporting process, including requests for consent to proceed with transactions. Understanding how privilege interacts with reporting duties, and how to avoid tipping off or prejudicing investigations, is central to compliant practice.

Key Term: criminal property

Criminal property is any asset, including money, derived from or representing the benefit of criminal conduct, whether in the UK or elsewhere. For overseas conduct, the test is whether the conduct would be criminal if it occurred in the UK. Property remains criminal even after conversion or mixing if it still represents the benefit of criminal conduct. Key Term: money laundering

Money laundering is the process of concealing, converting, arranging, acquiring, using, or possessing criminal property so as to give it the appearance of lawful origin or to facilitate its use.Test Tip: In SQE-style questions on Money laundering, identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

Exam Warning: Do not rely on a familiar phrase from Money laundering alone; check whether the facts satisfy every condition, exception, and timing requirement.

Principal Money Laundering Offences

Money laundering is the process of hiding, converting, or cleaning criminal property to give it the appearance of lawful origin. UK law contains several main offences relating to money laundering.

Key Term: suspicion (money laundering context)

A state of mind where there is a possibility, which is more than fanciful, that relevant facts exist—less than actual knowledge or belief. It is a low threshold and can arise from a constellation of red flags.

Main Offences

The principal offences under the Proceeds of Crime Act 2002 are:

- Concealing, disguising, converting, transferring, or removing criminal property (POCA s.327).

- Arranging to facilitate the acquisition, retention, use, or control of criminal property (POCA s.328).

- Acquiring, using, or possessing criminal property (POCA s.329).

A person may be guilty if they know or suspect the property is criminal property. “Criminal property” is defined broadly in POCA s.340 and includes real and personal property and intangible assets. The offences cover acts in the UK or overseas where the predicate conduct is criminal by UK standards. Attempts, conspiracy, and assisting or encouraging the commission of these offences are also criminal.

Concealing includes disguising the nature, origin, location, disposition, or ownership of property. Arrangements often capture professional involvement where a transaction is structured so that criminal property is put beyond reach or mixed with legitimate assets (e.g., holding funds in client accounts to facilitate their onward movement). Acquisition and possession can be as simple as accepting cash or goods when there is suspicion that they represent a criminal benefit, even if the person did not participate in the predicate offence.

Key Term: placement

The introduction of criminal property into the financial system (e.g., depositing cash or buying monetary instruments). Key Term: layering

Series of transactions intended to obscure the origin, ownership, or control of criminal property, often via multiple accounts, entities, or jurisdictions. Key Term: reintroduction

Making laundered money appear legitimate by returning it to the economy as apparently clean assets (often called “legitimisation”).

Worked Example 1.1

Scenario: A solicitor helps a client transfer money from a sale which the client describes as “quick cash from a friend.” The solicitor is not told the source but sees several cash deposits from unknown individuals. Should the solicitor be concerned about a money laundering offence?

Answer:

Yes. If the solicitor suspects that the money may be criminal property, proceeding with transactions could constitute an arrangement offence if they facilitate the use or control of criminal property. They should halt the transaction, escalate internally to the MLRO, and consider a SAR.

Application Stages of Money Laundering

The three classic stages are placement (introducing illegal funds into the system), layering (obscuring the origin through multiple transactions), and reintroduction (placing funds into legitimate assets or businesses). Legal professionals are most likely to be involved at the layering or reintroduction stages, for example, when handling property transactions or managing client funds.

In practice, professionals should watch for methods commonly used to launder funds in legal contexts: rapid transfers between multiple accounts or jurisdictions, unexplained third-party payments, requests to pay refunds to different accounts, unusual overpayments with immediate requests for return, and using legal accounts to hold funds without a genuine transaction.

Duty to Report Suspicion

Solicitors and regulated firms must report to the National Crime Agency (NCA) or their firm’s Money Laundering Reporting Officer (MLRO) when they know, suspect, or have reasonable grounds to suspect money laundering. In the regulated sector (which includes independent legal professionals when participating in specified transactional work), failure to disclose such suspicion can itself be an offence (POCA s.330 for employees; s.331 for nominated officers). Outside the regulated sector, there is no general failure-to-disclose offence, but anyone seeking the consent defence must make an authorised disclosure.

Key Term: suspicious activity report (SAR)

A formal report filed with the NCA (or internally to the MLRO) when there are grounds to suspect money laundering or terrorist financing. A SAR seeking consent to proceed with a transaction is commonly referred to as a DAML SAR. Key Term: MLRO (nominated officer)

The senior individual designated to receive internal disclosures, assess suspicions, decide whether to file SARs with the NCA, and guide transactional conduct pending consent. The MLRO must be accessible, independent in decision-making, and responsible for AML training and procedures. Key Term: regulated sector

Firms and professionals carrying on specified activities (e.g., transactional legal work such as property or business sales, managing client assets, opening accounts) subject to enhanced duties under POCA and MLR 2017, including failure-to-disclose offences and tipping off restrictions.

Failure to report is a separate criminal offence for those working in the regulated sector, even if the predicate criminal property is not handled directly. The mental element is broader than for the principal offences: liability can arise where a person knows, suspects, or has reasonable grounds to suspect that another is engaged in money laundering, based on information received in the course of business.

Procedure and Timing

Reports must be made promptly, ideally before the relevant transaction takes place. If a transaction is urgent or cannot be delayed, a report should be made as soon as practicable. Firms should have clear internal reporting routes to ensure disclosures reach the MLRO—reporting to a line manager does not suffice. If the MLRO is away, an authorised deputy must be designated to receive internal reports.

Where a transaction might involve criminal property, the solicitor may make an authorised disclosure seeking consent to proceed. If a SAR is submitted to obtain consent, the “moratorium” regime applies: the NCA has an initial response period (typically seven working days). If consent is refused within that period, the moratorium extends up to 31 calendar days. During the moratorium, the transaction must not proceed. If consent is granted or the initial period expires without refusal, proceeding is generally permissible for the specific act reported.

Solicitors must not inform the subject of a report (“tipping off”), as this is itself an offence unless an exception applies. Enquiries to verify instructions or source of funds before making a SAR are usually permissible, but caution is required once a SAR is submitted.

Worked Example 1.2

Scenario: While acting in a residential property purchase, a solicitor receives £95,000 in cash from a new client for the deposit. The client refuses to provide satisfactory evidence of identity. What must the solicitor do before proceeding?

Answer:

The solicitor should decline to proceed, report the matter to the firm’s MLRO, and may need to make a suspicious activity report if they suspect money laundering. Accepting cash from an unknown source is a red flag. If consent to proceed is required, no step should be taken until the NCA response window is observed.

Worked Example 1.3

Scenario: A firm’s MLRO submits a DAML SAR in relation to a client’s instruction to transfer sale proceeds abroad. When can the firm lawfully complete the transfer?

Answer:

If the NCA grants consent within the initial seven working days, the firm may proceed. If the NCA refuses consent, the firm must not proceed during the statutory moratorium (up to 31 calendar days). If the NCA does not respond within the initial period, the defence against money laundering applies and the firm may proceed with the reported act.

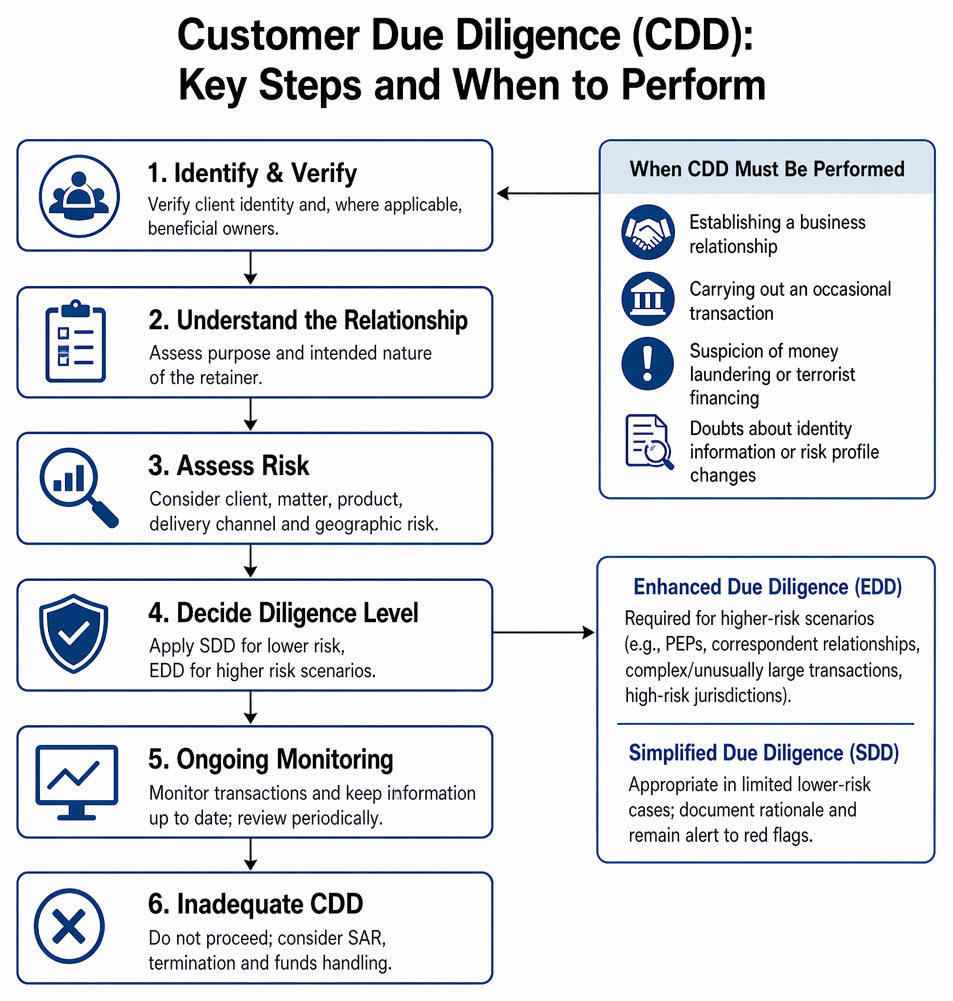

Customer Due Diligence

Firms subject to the Money Laundering Regulations 2017 must perform “customer due diligence” (CDD) at the outset of new business relationships or high-value transactions. CDD is risk-based and must be proportionate to the client, matter, product, delivery channel, and geographic risk.

Knowledge or suspicion triggers privilege review, authorised disclosure steps, transaction controls, and client confidentiality obligations pending NCA consent decisions.

Key Term: customer due diligence (CDD)

The process of identifying and verifying a client’s identity and, where applicable, any beneficial owner of client funds or entities, assessing the purpose and intended nature of a relationship, and conducting ongoing monitoring to ensure transactions are consistent with the client’s risk profile.

CDD procedures include verifying the identity of clients, understanding the purpose of the retainer, and monitoring transactions for suspicious activity. For trusts or companies, firms must verify the identity of beneficial owners.

Key Term: beneficial owner

The individual(s) who ultimately own(s) or control(s) a client or asset. For companies, this commonly includes persons with over 25% ownership or control or significant influence; for trusts, settlors, trustees, protectors (if any), beneficiaries, and other persons exercising control.

In what circumstances must CDD be conducted?

- Establishing a business relationship (e.g., starting a transactional retainer).

- Carrying out an occasional transaction within scope of the Regulations.

- When suspicion of money laundering or terrorist financing arises.

- When doubts emerge about previously obtained identity information, or the client’s risk profile changes.

When must CDD be conducted?

- Usually before establishing the relationship or undertaking the transaction. Limited exceptions permit completion during the course of establishing the relationship, but identity verification must occur as soon as practicable and before any cash movement that could facilitate laundering.

- Information must be kept up to date and reviewed periodically, particularly for long-running matters.

- For trusts and other legal entities, firms must ascertain the legal form and ownership/control structure, and obtain evidence of beneficial owners and controllers. Public registers (e.g., PSC register for UK companies, trust registration where applicable) may assist but do not replace verification.

Enhanced due diligence (EDD) is required for higher-risk scenarios, including dealings with politically exposed persons (PEPs), correspondent relationships, complex or unusually large transactions without apparent economic purpose, and clients from high-risk jurisdictions. EDD may involve senior management approval, obtaining source of funds and source of wealth information, and increased monitoring. Simplified due diligence (SDD) may be appropriate in limited lower-risk cases, but firms should document rationale and remain alert to red flags.

If adequate CDD cannot be performed, the firm must not proceed with the transaction and should consider making a suspicious activity report. The firm must also consider whether to terminate the retainer and whether to retain or return funds in accordance with legal and regulatory guidance.

Worked Example 1.4

Scenario: A company client is controlled by an individual who is a senior government official in a foreign state. The company proposes acquiring UK commercial property using multiple offshore entities. What due diligence steps are required?

Answer:

Treat the client as a PEP and apply EDD: obtain senior management approval to proceed, verify the ownership chain and beneficial owners, obtain robust evidence of source of funds and source of wealth, and increase monitoring. If verification proves inadequate or suspicions arise, halt and escalate to the MLRO and consider a SAR.

Defences and Privileged Circumstances

A limited number of defences excuse a solicitor or person from liability for a principal money laundering offence.

Key Term: authorised disclosure

A formal notification made to the NCA or MLRO prior to (or as soon as practicable after) a transaction to report suspicion of money laundering and seek consent to proceed (a DAML). Where consent is granted or time limits expire without refusal, this can operate as a defence to principal offences for the specific act disclosed. Key Term: legal professional privilege

A rule that protects confidential communications between legal advisers and their clients concerning legal advice or contemplated litigation from disclosure. Privilege does not apply to communications made with the intention of furthering a criminal purpose (the “crime/fraud exception”). Key Term: privileged circumstances

Information received by a professional legal adviser in privileged circumstances (e.g., in connection with providing legal advice or litigation) may be exempt from mandatory disclosure, provided the communication is not in furtherance of a criminal purpose. This can operate as a defence to failure-to-disclose offences in the regulated sector. Key Term: adequate consideration

A defence for those who acquire, use, or possess criminal property for value and in good faith, provided there is no knowledge or suspicion of illegality. For professionals, fees and disbursements for genuine services at normal rates may qualify.

Making an authorised disclosure or reporting suspicion before the act is committed is generally a defence. Solicitors must ensure the disclosure is properly made and documented, that they await consent or expiry of the relevant period, and that they restrict communications to avoid tipping off.

Legal professional privilege and privileged circumstances are narrow shields. They excuse disclosure duties only for genuinely privileged communications and do not protect communications intended to facilitate a crime. Firms should record the rationale for relying on privilege and consider seeking independent guidance where privilege is borderline.

Adequate consideration most commonly arises where the solicitor receives payment for legitimate work without suspicion that the funds are tainted. The fee must reflect fair value; excessive or unusual payments undermine the defence. Even where adequate consideration applies, ongoing duties under MLR 2017 to conduct CDD and monitor risks remain.

Other statutory defences include lack of training for failure-to-disclose offences in the regulated sector, where the person was not provided with the training required by their employer’s AML policies. This defence is limited and does not excuse wilful blindness.

Worked Example 1.5

Scenario: A solicitor’s client pays legal fees from an account that is later found to contain proceeds of crime. The fees were reasonable and for genuine legal work. Is the solicitor criminally liable?

Answer:

If fees are for legitimate services at usual rates and there is no suspicion of crime at the time payment is received, the solicitor may rely on the defence of adequate consideration. If suspicion did exist, the defence would not apply and a SAR should have been made before accepting payment.

Tipping Off and Prejudicing Investigations

Revealing that a suspicious activity report has been made, or that an investigation is ongoing, risks prejudicing investigations and is itself a criminal offence—commonly called “tipping off.” Exceptions are limited. Under POCA, tipping off (s.333A) applies to persons in the regulated sector who disclose that a SAR has been made or that an investigation is contemplated or underway, where the disclosure is likely to prejudice the investigation. Separately, prejudicing an investigation (s.342) applies to any person who makes a disclosure or takes steps (e.g., concealing, falsifying, or destroying documents) likely to prejudice a money laundering investigation.

Enquiries made directly of a client about their source of funds before making a SAR are not usually tipping off. However, warning a client after a SAR has been submitted or implying that authorities are investigating can amount to an offence. Permitted disclosures may include communications within a corporate group for AML purposes, certain inter-institution disclosures in limited circumstances, and disclosures made in connection with legal advice or proceedings, provided there is no intention to further a criminal purpose.

Key Term: tipping off

The criminal offence of informing a person that a report or investigation into money laundering has occurred, potentially prejudicing the case. Applies in the regulated sector. Key Term: prejudicing an investigation

The offence of taking steps to obstruct or undermine a money laundering or terrorist financing investigation, including destroying relevant evidence or making disclosures likely to prejudice investigative actions. Applies to any person.

The mental element requires knowledge or suspicion that disclosure would likely prejudice an investigation. Practitioners should document the rationale when providing general explanations to clients for transactional delays that do not reveal a SAR or investigative actions.

Worked Example 1.6

Scenario: After making a suspicious activity report, a solicitor is contacted by the client asking why their transaction has been delayed. Can the solicitor explain the cause?

Answer:

The solicitor must not disclose the existence of a SAR or NCA involvement. Only a generic response about regulatory compliance or process delays is appropriate. Communications should be limited and documented to avoid any risk of tipping off.

Worked Example 1.7

Scenario: A solicitor suspects that the counterparty’s lawyer has made a SAR, causing a delay in completion. The solicitor is confident their own client’s funds are legitimate. Can they tell their client that delays may be due to a SAR by the other side?

Answer:

If the solicitor does not know or suspect that disclosure would be likely to prejudice an investigation, they may explain the probable cause of delay in general terms. They should avoid confirming that a SAR exists and ensure the explanation is not likely to prejudice an investigation. Document the reasoning.

Penalties and Regulatory Supervision

Money laundering offences carry significant penalties. Principal offences under POCA (concealing, arranging, acquiring/using/possessing) carry maximum sentences of up to 14 years’ imprisonment and/or an unlimited fine. Failure to disclose in the regulated sector can lead to imprisonment (up to two years) and/or a fine. Tipping off carries up to two years’ imprisonment and/or a fine. Prejudicing an investigation carries up to five years’ imprisonment and/or a fine.

Regulatory bodies expect firms to implement training, maintain records, and appoint a qualified MLRO. Firms must:

- Adopt risk-based internal AML policies, controls, and procedures.

- Conduct and document CDD (including beneficial owner identification) before acting, and update information during the relationship.

- Keep records of CDD and SARs/disclosures for at least five years after the end of the relationship or completion of the transaction.

- Provide regular and appropriate AML training to all relevant staff and supervise compliance effectively.

Failing to have suitable procedures, or failing to adequately train staff, can result in professional sanctions and prosecution of both the firm and its responsible individuals. The SRA can impose disciplinary measures, and managers (including the MLRO, COLP, and COFA) may be personally accountable for serious breaches. Robust supervision and documented decision-making are essential to demonstrate compliance.

Key Point Checklist

This article has covered the following key knowledge points:

- The main criminal money laundering offences under English law are concealing, arranging, and acquisition, use, or possession of criminal property.

- Solicitors and relevant staff must make prompt suspicious activity reports when there is knowledge, suspicion, or reasonable grounds to suspect money laundering.

- Customer due diligence and identification procedures are mandatory before acting for clients in the regulated sector, with enhanced measures for higher risk scenarios.

- Authorised disclosures and legal professional privilege (including privileged circumstances) can excuse disclosure duties in certain circumstances, subject to the crime/fraud exception.

- Tipping off and prejudicing investigations are separate criminal offences with limited exceptions; caution is required in communications with clients.

- The MLRO has central responsibility for receiving internal reports, filing SARs, liaising with the NCA, training staff, and guiding transactional conduct pending consent.

- Failure to comply with anti-money laundering procedures can result in professional and criminal sanctions, including imprisonment and fines.

- Firms must maintain AML policies, recordkeeping for five years, and ongoing monitoring to manage risk throughout the client relationship.

Key Terms and Concepts

- criminal property

- money laundering

- suspicion (money laundering context)

- placement

- layering

- reintroduction

- suspicious activity report (SAR)

- MLRO (nominated officer)

- regulated sector

- customer due diligence (CDD)

- beneficial owner

- authorised disclosure

- legal professional privilege

- privileged circumstances

- adequate consideration

- tipping off

- prejudicing an investigation