Learning Outcomes

This article covers indemnities, limitation clauses, and liability caps in commercial contracts, including:

- Distinguishing indemnities, exclusion and limitation clauses, and liability caps, and their legal functions

- Drafting considerations and common pitfalls, with application to SQE2 problem scenarios

- Differentiating third‑party indemnities from direct‑loss indemnities, and their operation as debt versus damages

- When common‑law controls on damages (remoteness, mitigation) apply or are displaced by clear indemnity wording

- UCTA reasonableness and enforceability of exclusions, limitations, and caps, with key statutory factors

- Interaction between caps, indemnities, and carve‑outs; drafting clear aggregate versus per‑claim caps and exceptions

- Drafting exclusions of specified heads of loss (e.g., consequential loss) and how courts classify loss types

- Essential procedural protections for indemnities (notice, conduct of defence, settlement control) and their effect on recoverability

SQE2 Syllabus

For SQE2, you are required to understand how substantive clauses allocate risk, particularly indemnities, limitation clauses, and caps, with a focus on the following syllabus points:

- The nature and function of indemnity clauses in commercial contracts

- The difference between indemnities, exclusion, and limitation clauses

- How limitation clauses and caps operate (including enforceability and drafting pitfalls)

- The legal controls on enforceability (such as Unfair Contract Terms Act 1977)

- Client advice on risk allocation in common contractual scenarios

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the effect of an indemnity clause compared to a warranty?

- What statutory test governs whether a limitation of liability clause in a B2B contract will be enforceable?

- Why do commercial contracts include liability caps, and what factors may undermine their effectiveness?

- If an exclusion clause purports to limit liability for death caused by negligence, is it enforceable under English law?

Introduction

Substantive risk allocation clauses shape the distribution of legal and commercial risk in most business contracts. For SQE2, you must be able to explain what indemnities, limitations, and caps actually achieve, how they are different, and the main legal pitfalls that come up in practice. This article covers their core functions, enforceability, and key issues to watch for.

Key Term: indemnity

A promise to compensate another party for specified losses or liabilities, often on a pound-for-pound basis, typically triggered by a defined event or breach. Key Term: limitation of liability clause

A contract term that restricts or limits a party’s liability for certain breaches or events, often by setting a monetary cap or excluding types of damage. Key Term: liability cap

A specific maximum monetary amount stated in a contract beyond which a party is not liable for claims, usually relating to contractual obligations. Key Term: exclusion clause

Any contractual provision that seeks to exclude a party’s liability for certain events or types of loss. Key Term: Unfair Contract Terms Act 1977 (UCTA)

Legislation that controls the effectiveness of exclusion and limitation clauses in business and consumer contracts under English law.

Indemnities

Indemnity clauses are used to shift risk for defined losses, often in commercial, corporate, and technology contracts. Unlike warranties, indemnities typically require payment of the indemnified amount as a debt, not just damages subject to legal proof of loss. Indemnities may respond to third-party claims, specific breaches, or non-fault events. Precise drafting is essential to define the losses covered and trigger conditions.

In practice, indemnities tend to fall into two broad categories:

- third‑party indemnities (e.g., IP infringement, product liability, regulatory claims), where a third party asserts a claim against the indemnified party and the indemnifier must reimburse or defend; and

- direct loss indemnities (e.g., tax indemnities in share purchase agreements), where the counterparty’s own loss is reimbursed on a specified basis.

The intended remedial character matters. If drafted as a debt claim (e.g., “shall indemnify and keep indemnified against all losses”), recovery is often simpler and may sidestep some common-law damage controls (such as remoteness), unless the clause reincorporates them. If drafted merely as a promise to pay damages, common-law controls will likely apply.

Key drafting variables include:

- Scope of covered “Losses”: define “losses” to include damages, settlement sums, finally awarded costs, reasonable legal and expert fees, and interest, and specify whether internal costs or management time are included.

- Triggers: state precisely what triggers the indemnity (e.g., “any third‑party claim alleging IP infringement” vs “any claim finally determined by a court of competent jurisdiction”).

- Procedures: include notice obligations, control of defence, cooperation, and settlement consent to avoid paying for inflated or avoidable costs.

- Interplay with limitations: specify whether the indemnity sits inside or outside any cap, and whether exclusions of certain heads of loss apply to indemnified sums.

- Exclusions and carve-outs: common carve‑outs include where the claim arises from the indemnified party’s materials, instructions, or misuse.

Indemnities are interpreted by reference to the natural meaning of the words used and the overall contract context. Because the benefit typically lies with the indemnified party, precision reduces disputes and the risk of a narrow reading.

Worked Example 1.1

Question: A supplier contract includes: "The Supplier shall indemnify the Customer against all losses arising from any claim that the goods breach third party intellectual property rights." The goods are found to infringe a third party patent. What is the effect of the indemnity?

Answer:

The supplier must reimburse the customer for all losses arising from the claim: damages, settlement amounts, and reasonable legal costs. The customer does not need to prove "remoteness" or other common law damage limits—unless the clause says so. Additional points commonly negotiated around indemnities:

- Defence control: the indemnifier often wants conduct of the defence of third‑party claims it will be funding; the indemnified party will want veto rights over settlements that admit liability or prejudice its business.

- Settlements: parties typically require prior written consent (not to be unreasonably withheld or delayed) for any settlement imposing non‑monetary obligations or reputational harm.

- Mitigation: if the indemnity is framed as a debt, mitigation may not automatically apply; clear wording can import a duty to act reasonably to avoid or minimise loss.

- Regulatory penalties: indemnities for fines or penalties can raise public policy issues. Draft carefully; avoid purporting to indemnify for criminal fines, and consider drafting to cover “reasonable costs and expenses” of responding to investigations rather than fines themselves.

Revision Tip: Indemnities are usually interpreted strictly, with the benefit going to the indemnified party. If the clause is badly drafted, coverage may be narrower than intended.

Limitation and Exclusion of Liability Clauses

Limitation and exclusion clauses aim to reduce the risk of open-ended or disproportionate liability. They can specify an upper limit (a cap), exclude entire categories of damages (e.g., consequential loss), or exclude liability for certain types of event. However, they are subject to legal restrictions.

Key Term: consequential loss

Indirect losses flowing from a breach, as distinguished from direct loss; often excluded through a specific clause.

Exclusions are often structured by categories, for example “loss of profits,” “loss of revenue,” “loss of anticipated savings,” “loss of data,” “loss of goodwill,” and “consequential or indirect loss.” Remember:

- “Consequential or indirect loss” is typically construed as loss falling within the second limb of Hadley v Baxendale (loss not arising naturally but due to special circumstances known to both parties). It does not automatically capture all lost profits.

- Lost profits can be direct or indirect depending on the contract. Profit on the very contract itself is commonly treated as direct; profits on separate downstream contracts may be indirect. If a particular head of loss matters commercially, specify it expressly rather than relying on “consequential loss” wording.

Exam Warning: If a clause seeks to exclude liability for death or personal injury caused by negligence, it is void under UCTA—do not overlook this rule in exam scenarios.

Scope and Structure

Typical structure:

- A general cap on damages (e.g., total contract price)

- Exclusion of indirect or consequential losses

- Exclusion of liability for specific events

- Carve-outs for things like death or personal injury, fraud, or deliberate default

The drafting must be clear and specific. Ambiguity is resolved against the party seeking to rely on the limitation (the “contra proferentem” rule). Avoid vague catch‑alls and define uncertain expressions like “wilful misconduct” or “deliberate default.”

Worked Example 1.2

Question: A contract clause states: "The Supplier’s total liability for any claim arising under the contract shall not exceed £50,000, except for liability that cannot be limited by law." A fire caused by supplier negligence results in loss of life and property damage of £200,000. Is the £50,000 cap effective?

Answer:

The cap is effective only for property damage claim(s); it is void for personal injury or death for which liability cannot be limited under UCTA.

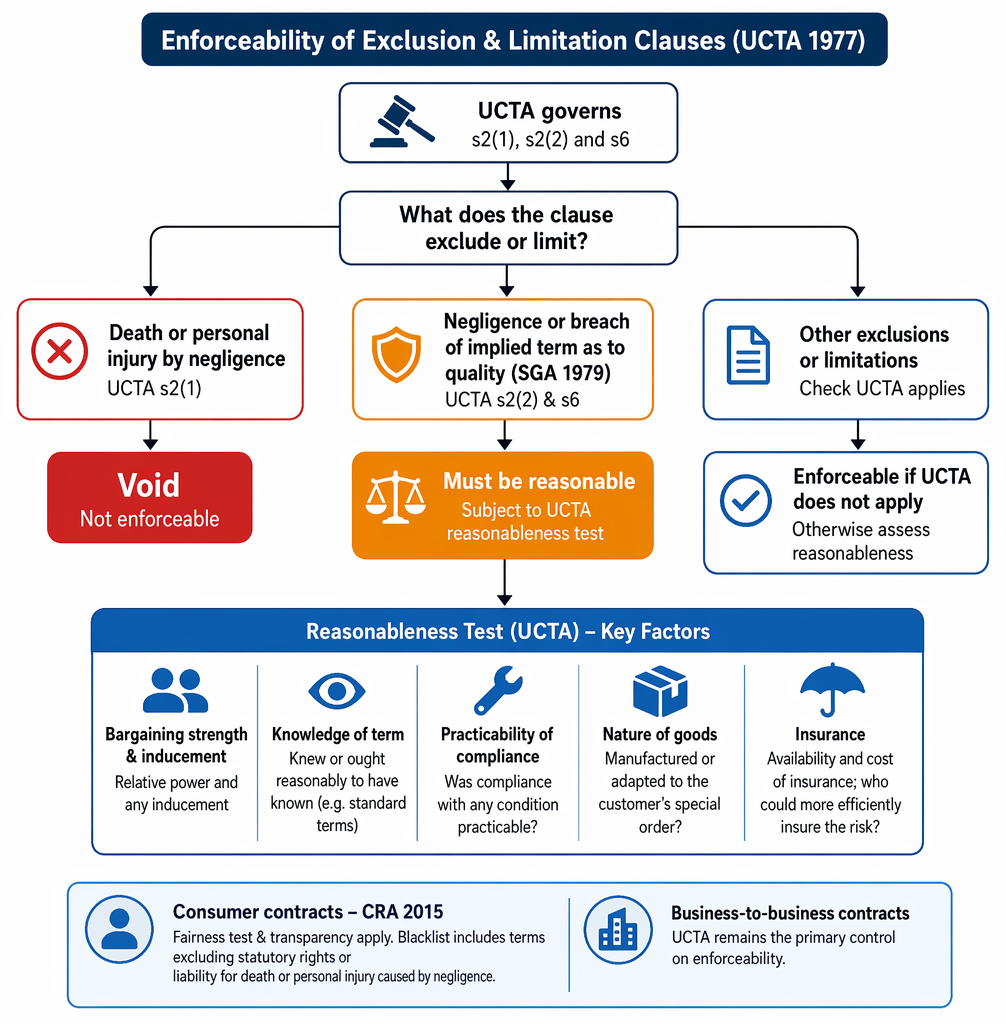

Enforceability and Statutory Controls

The Unfair Contract Terms Act 1977 governs whether exclusion and limitation clauses are enforceable.

Contractual risk-allocation clauses are evaluated by identifying term and parties, confirming incorporation, interpreting wording, applying statutory controls, and advising on redrafting.

- Clauses excluding liability for death or personal injury by negligence are void (UCTA, s2(1)).

- Clauses limiting liability for negligence, or breach of implied term as to quality under SGA 1979, must be reasonable to be enforceable (UCTA, s2(2) and s6).

- “Reasonableness” considers bargaining power, insurance, and what was practical at the time of contract. A key question is whether the term was fair and reasonable having regard to the circumstances which were, or ought reasonably to have been, known to or in the contemplation of the parties when the contract was made.

Reasonableness factors typically include:

- relative bargaining strength of the parties and whether the customer received an inducement to agree to the term;

- whether the customer knew or ought reasonably to have known of the term (especially if in standard terms);

- whether compliance with a condition was practicable;

- whether the goods were manufactured or adapted to the customer’s special order;

- availability and cost of insurance and who could more efficiently insure the risk.

Consumer contracts are separately policed by the Consumer Rights Act 2015 (CRA), which applies a fairness test and transparency requirements; terms excluding statutory rights or liability for death or personal injury caused by negligence are blacklisted in consumer contexts. In business‑to‑business contracts, UCTA remains the primary control.

Key Term: reasonableness test (UCTA)

The statutory standard in UCTA requiring limitation or exclusion clauses to be fair and reasonable in all circumstances, assessed at contract formation.

Worked Example 1.3

Question: A software licence purports to exclude all liability for loss of data, including where caused by the supplier’s own negligence. Is this enforceable?

Answer:

The clause is void if it excludes liability for death or personal injury. For property or economic loss, it will only be effective if reasonable under UCTA.

Revision Tip (Enforceability)

In SQE2 problem questions, always consider: (1) Has the clause been clearly incorporated? (2) Does UCTA apply? (3) If so, can the clause pass the reasonableness test?

Further enforceability points:

- Misrepresentation: a clause restricting liability for misrepresentation (e.g., non‑reliance wording) must satisfy the reasonableness test under the Misrepresentation Act 1967, s3.

- Negotiated vs standard terms: heavy use of standard terms and lack of prominence in presentation can undermine reasonableness; clear, prominent caps linked to insurance are more defensible.

- Fundamental breach: English law does not automatically invalidate limitations for “fundamental breach”; enforceability turns on construction and statutory controls.

Liability Caps

A cap is a contractual limit on a party’s aggregate liability. Caps are used in almost all modern commercial contracts and are usually set by reference to price, insurance, or other commercial factors. However, caps typically do not apply to certain types of liability, such as fraud or death/personal injury.

Drafting pitfalls include:

- Failing to exclude liability for uncapped risks (like fraud or deliberate breach)

- Not clarifying if the cap is aggregate or applies per claim

- Ambiguous cap wording being construed against the drafter

The best practice is for the cap to operate as a “ceiling” for all claims except for specifically identified exceptions (e.g., deliberate wrongdoing). Consider specifying:

- whether the cap is aggregate for all claims “arising under or in connection with” the contract;

- whether any sub‑caps apply to specific risks (e.g., data loss up to a separate lower figure);

- what period the cap applies to (e.g., per 12‑month contract year) and whether it resets on renewal;

- whether indemnified liabilities are within or outside the cap.

Worked Example 1.4

A clause states: "The maximum liability per claim shall not exceed the contract price." Is this an aggregate cap or a per claim cap?

Answer:

"Per claim" caps the maximum liability for each separate claim. There is no overall aggregate cap unless expressly provided.

Exam Warning (Liability Caps)

If the contract covers activities over a long period (e.g., a service agreement), check that the cap cannot be circumvented by splitting claims or by claims arising in different periods.

Direct vs indirect loss: why it matters for caps and exclusions

Because exclusions often target “consequential or indirect loss,” caps frequently become the main protection against direct heads of loss (e.g., wasted expenditure directly caused by breach). Clarity over whether lost profits are excluded or merely capped is important. If your commercial intention is to limit, not exclude, a particular head (e.g., loss of data), say so expressly and align with well‑signposted sub‑caps.

Worked Example 1.5

Question: A SaaS provider excludes “consequential or indirect loss” and “loss of revenue,” and caps total liability at 100% of annual fees. The customer’s claim is for lost subscription revenue from its own customers due to a two‑day outage. Is that loss excluded?

Answer:

Not necessarily. Loss of the customer’s own revenue may be a direct loss arising naturally from the outage in this context. “Consequential or indirect loss” typically covers Hadley v Baxendale second‑limb loss, not all lost revenue. If the parties intend to exclude such revenue loss, it should be expressly listed; otherwise the claim may be capped (not excluded).

Aggregation and “related claims”

Defining when multiple demands amount to one “claim” can prevent cap‑avoidance by claim‑splitting. Common approaches:

- series‑of‑related‑claims wording (e.g., “all claims arising from the same or similar acts, omissions, events or series of related events are deemed one claim”);

- “per incident” vs “per claim” language (ensure “incident” is defined if used);

- time‑boxed caps (e.g., per contract year), with aggregation across the year.

Worked Example 1.6

Question: A consultancy contract states: “Supplier’s liability in any 12‑month period shall not exceed the Fees paid in that period. All claims arising out of the same or related facts shall be one claim.” The client suffers five similar defects across three projects within one year. How does the cap apply?

Answer:

If the defects arise from “same or related facts,” the claims aggregate into one claim and share a single cap equal to the fees in that 12‑month period. If they are unrelated, each may have its own cap, but all remain subject to the annual cap if drafted that way.

Indemnities and caps: interaction

Whether indemnified sums count toward the cap is a matter of drafting. Clauses often state “the cap applies to all liabilities, whether in contract, tort, breach of statutory duty, misrepresentation, restitution or otherwise,” and then list carve‑outs (e.g., fraud, death/personal injury). If indemnities are intended to be uncapped (e.g., IP indemnity), the cap must expressly exclude those indemnities. Conversely, if parties wish to cap indemnities, they should say so, and avoid ambiguous carve‑outs that could lift the cap unintentionally.

Worked Example 1.7

Question: A limitation clause says: “Supplier’s aggregate liability shall not exceed £500,000, save for death/personal injury, fraud, and the indemnity at clause 12 (IP Claims).” An IP claim leads to a £900,000 settlement. Is the supplier’s exposure capped?

Answer:

No. The IP indemnity is expressly carved out from the £500,000 cap, so the supplier is exposed to the full settlement amount, subject to any defence/settlement controls in clause 12 and general enforceability.

Drafting Best Practice

Clear, precise wording is essential. Best practice includes:

- Stating if caps apply “in aggregate” or “per claim”

- Excluding non-excludable liability (e.g., fraud)

- Defining what is and is not included in the cap (interest, legal costs, etc.)

- Ensuring the cap does not operate as an unlawful penalty

To reduce ambiguity and drafting risk, follow these additional techniques drawn from modern legal drafting guidance:

- Use simple, active language: “X shall pay…” rather than passives that obscure who must act. Passive constructions can create uncertainty about who bears obligations and can backfire in litigation.

- Avoid “and/or.” Where you really mean “any or all of,” say exactly that; otherwise specify the precise combinations.

- Be careful with “subject to.” If you add an extra obligation, prefer “without prejudice to clause…” so you do not unintentionally subordinate or displace an earlier protection. For example, a cap “subject to” a later indemnity carve‑out might inadvertently nullify the intended protection if used carelessly.

- Draft loss exclusions as clear lists, tailored to the transaction. If “loss of profits” is to be excluded, state whether that is all loss of profits or profits on separate downstream contracts only. Consider adding “whether direct or indirect” if that reflects the intention.

- Define “Claim,” “Losses,” “Related Claims,” and “Contract Year” to support how caps and exclusions operate.

- Clarify the treatment of interest and legal costs: specify if pre‑judgment interest and recoverable costs are included in or outside the cap.

- Ensure prominence and legibility of limitations in standard terms. Reasonableness under UCTA is aided by clarity, prominence, and a fair alignment with insurance cover and price.

Procedural protections for indemnities and claims

- Include detailed claims procedures for indemnities: prompt notice; opportunity to take over the defence; consent for settlements; cooperation; and cost control. Lack of control can increase quantum and invite disputes.

- Include time limits for bringing claims, aligned with applicable limitation periods, and any contractual time bars.

- Align liability allocation with insurance: consider an obligation to maintain specified insurance with limits consistent with the cap; identify the insured risks and impose evidence-of-insurance requirements. Tying the cap to insurance levels can support UCTA reasonableness.

Worked Example 1.8

Question: A supplier’s standard terms include: “The Supplier excludes liability for consequential loss and loss of profits and caps liability at £25,000. The Supplier maintains £5m public liability insurance.” A customer claims £300,000 of direct wasted expenditure on a failed project. Is the cap likely reasonable?

Answer:

The cap may be vulnerable. Although the supplier holds substantial insurance, the cap is set very low relative to likely project losses and to the insurance maintained. Under UCTA reasonableness, factors such as disparity between the cap and foreseeable losses, bargaining power, and insurance availability may render the cap unreasonable. Clarity and prominence help, but the level must still be fair in context.

Key Point Checklist

This article has covered the following key knowledge points:

- Indemnity clauses are a contractual promise to compensate for specific losses. They differ from warranties/damages in practical and procedural effect.

- Indemnities should be drafted with clear triggers, scope of “Losses,” defence and settlement control, and explicit interaction with caps and exclusions.

- Limitation and exclusion clauses restrict or exclude liability, but are controlled by the Unfair Contract Terms Act and reasonableness.

- “Consequential loss” generally means second‑limb loss under Hadley v Baxendale; specify important heads of loss expressly rather than relying on labels.

- Liability caps are specific monetary limits and must be drafted with care to cover intended claims, clarifying aggregate vs per‑claim operation and related‑claims aggregation.

- Excluding or limiting liability for death/personal injury caused by negligence is void under English law; other exclusions are subject to a reasonableness test.

- Reasonableness factors include bargaining power, clarity and prominence, practicability of compliance, and the ability to insure. Caps aligned with realistic risk and insurance are more defensible.

- Use clear, modern drafting: avoid passives and “and/or,” use “without prejudice to” (not “subject to”) when adding obligations, and define key terms to support the cap/exclusions framework.

Key Terms and Concepts

- indemnity

- limitation of liability clause

- liability cap

- exclusion clause

- Unfair Contract Terms Act 1977 (UCTA)

- consequential loss

- reasonableness test (UCTA)