Learning Outcomes

After reading this article, you will be able to explain and apply the core parity relationships governing exchange rate behavior: Purchasing Power Parity (PPP), Interest Rate Parity (IRP), and the Fisher Relationship. You will be able to compute expected future spot and forward exchange rates using these formulas, interpret the economic logic behind the relationships, and identify potential deviations in practice. You should be able to discuss their application in international investment appraisal and recognize common exam pitfalls.

ACCA Advanced Financial Management (AFM) Syllabus

For ACCA Advanced Financial Management (AFM), you are required to understand the theoretical and practical basis of exchange rate forecasting and how parity relationships inform financial decisions involving foreign currencies. This knowledge is fundamental when appraising international investments and managing currency risk.

- Explain and apply the Purchasing Power Parity (PPP) theory for forecasting exchange rates

- Explain and apply the Interest Rate Parity (IRP) theory in relation to spot, forward, and expected future exchange rates

- Describe and use the Fisher Relationship to distinguish between real and nominal interest rates

- Calculate expected spot and forward exchange rates using parity relationships

- Discuss reasons for deviations from theoretical parity conditions in practice

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which of the following best describes Purchasing Power Parity (PPP)?

- a) The relationship between spot rates and interest rates

- b) The relationship between price levels and exchange rates

- c) A method for hedging currency risk

- d) The pricing of international derivatives

-

If interest rates in Country X are 6% and in Country Y are 3%, and the spot rate is 2 X$/Y$, according to IRP, what should the 1-year forward rate be? Briefly explain your calculation.

-

True or false? The Fisher Relationship is used to separate the effects of inflation from nominal interest rates when analyzing investment returns across countries.

-

Outline one reason why actual future spot rates may deviate from those forecasted under PPP or IRP.

Introduction

Understanding how exchange rates move and the principles that connect them to inflation and interest rates is key for any financial manager working with cross-border investments. Exchange rate parity relationships establish the theoretical links between interest rates, inflation rates, and currency movements, providing a framework for predicting exchange rates and pricing international financial contracts. In practice, these relationships underpin the calculation of expected cash flows and risk in international project appraisal.

This article covers the three main parity theories—Purchasing Power Parity (PPP), Interest Rate Parity (IRP), and the Fisher Relationship—used to analyze and forecast exchange rates and returns in international finance.

Key Term: Purchasing Power Parity (PPP)

The theory that the exchange rate between two currencies should adjust so that equivalent goods cost the same in each country, accounting for inflation differentials. Key Term: Interest Rate Parity (IRP)

The principle that the difference between forward and spot exchange rates is equal to the interest rate differential between two countries, preventing arbitrage opportunities. Key Term: Fisher Relationship

The formula that links nominal interest rates, real interest rates, and inflation, stating that nominal rates reflect both expected inflation and real required returns.

THE PARITY RELATIONSHIPS

Exchange rate parity decision rules link inflation data to PPP, interest differentials to IRP, and nominal-real consistency to the Fisher relationship.

Purchasing Power Parity (PPP)

PPP provides a long-term view of exchange rate determination. The core logic is that differences in inflation rates will cause exchange rates to adjust so that identical baskets of goods cost the same across countries. If domestic inflation exceeds foreign inflation, the domestic currency is expected to depreciate.

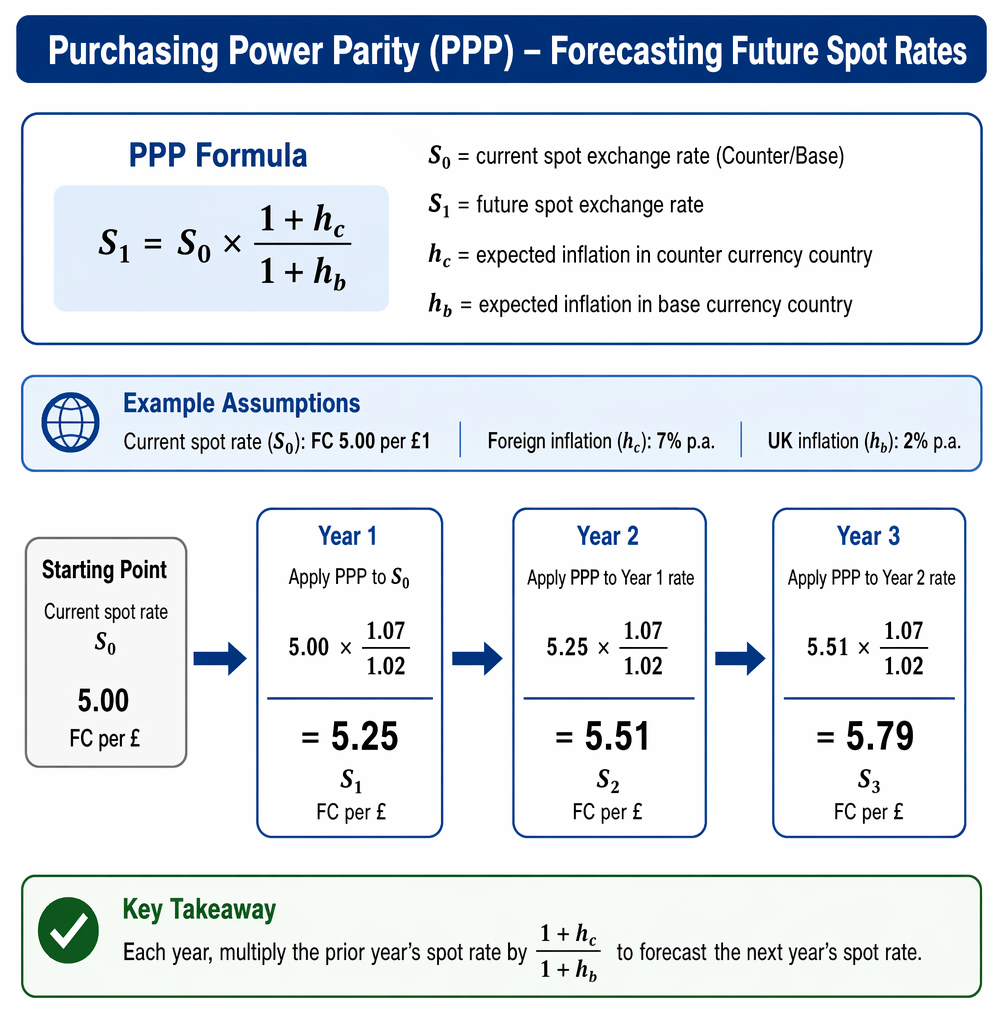

The PPP formula for forecasting the future spot rate () is:

where:

- = current spot exchange rate (quoted as Counter currency/Base currency)

- = expected inflation rate in the counter currency country

- = expected inflation rate in the base currency country

Interest Rate Parity (IRP)

IRP links interest rates and exchange rates under the assumption that capital will flow freely to exploit any arbitrage. If risk-free interest rates are higher in one country, its currency is expected to depreciate relative to a currency with lower rates, as the forward rate adjusts to offset the interest advantage.

The IRP formula for calculating the forward rate () is:

where:

- = risk-free interest rate in counter currency country

- = risk-free interest rate in base currency country

The Fisher Relationship

The Fisher Relationship separates the nominal required rate of return into real and inflationary components:

where:

- = nominal (money) interest rate

- = real interest rate

- = expected inflation rate

This allows you to convert between real and nominal rates when dealing with cash flows affected by inflation.

Worked Example 1.1

A company is evaluating a 3-year project in a foreign country. The current spot rate is FC 5.00 per £1. UK inflation is expected to be 2% per annum and the foreign country's inflation rate is expected to be 7% per annum for each of the next three years. Calculate the expected spot rates for years 1, 2, and 3 using PPP.

Answer:

Year 1:

Year 2:

Year 3:

Each year, apply the PPP formula to the prior year’s calculated rate.

Worked Example 1.2

Suppose the spot rate is $1.50/£, the risk-free $ interest rate is 4%, and the risk-free £ interest rate is 6%. According to IRP, what is the 1-year forward rate?

Answer:

The forward rate is lower than spot, reflecting higher UK interest rates.

Worked Example 1.3

A UK investor seeks a 5% real after-tax return on an overseas project. Inflation in the foreign country is 9%. What nominal rate should the investor use?

Answer:

Use the Fisher Relationship:

So,

nominal required return.

Exchange Rate Behavior in Practice

While the parity relationships are powerful tools for forecasting and analysis, actual exchange rate movements may differ from theoretical forecasts. Factors include capital flows, government intervention, speculative activity, transaction costs, and non-traded goods.

- PPP tends to hold in the long term, but short-term rates are affected by capital flows, speculative positions, and government policy.

- IRP assumes perfect capital mobility and no transaction costs; deviations can occur due to capital controls or differential tax treatments.

- Fisher Relationship provides a reliable method to separate inflation impacts from real returns, critical for correct project appraisal and comparability.

Exam Warning: When calculating expected spot rates for cash flow conversion in investment appraisal, ensure you use the correct parity relationship for the data given—PPP for inflation rates, IRP for interest rates. Mixing up formulas is a common source of error and will lead to incorrect project NPVs.

Revision Tip: Always express exchange rates and inflation rates on a consistent basis (e.g., annually, continuously). Clearly state which country's inflation/interest rate is in numerator/denominator, and whether the quote is direct or indirect.

Summary

Exchange rate parity relationships—PPP, IRP, and the Fisher Relationship—form the core theoretical basis for forecasting exchange rates and analyzing returns in an international context. Command of these relationships allows accurate conversion of foreign cash flows, correct hedging of currency risk, and adjustment for inflation in project evaluation. Awareness of practical deviations and clear formula application are essential for ACCA AFM exam success.

Key Point Checklist

This article has covered the following key knowledge points:

- Define and use the PPP, IRP, and Fisher Relationship formulas in practice

- Calculate expected spot and forward rates based on inflation and interest rate differentials

- Convert between real and nominal rates for international project appraisal

- Recognize circumstances where parity conditions may not hold in the short term

- Avoid confusion between parity relationships in exam calculations

Key Terms and Concepts

- Purchasing Power Parity (PPP)

- Interest Rate Parity (IRP)

- Fisher Relationship