Learning Outcomes

After reading this article, you will be able to:

- Explain the significance of exchange rate behavior and parity when appraising international projects.

- Distinguish between project and parent cash flow viewpoints in foreign investment appraisal.

- Apply exchange rate parity models to forecast future exchange rates for project evaluation.

- Identify implications of exchange rate movements on cash flows, NPV calculations, and group reporting.

ACCA Advanced Financial Management (AFM) Syllabus

For ACCA Advanced Financial Management (AFM), you are required to understand how exchange rate behavior affects multinational investment decisions. In particular, focus your revision on:

- The impact of alternative exchange rate assumptions on the value of a project

- How to forecast project and organisation free cash flows in any specified currency

- Application of parity relationships (purchasing power parity and interest rate parity) and the implications for investment appraisal

- The distinction between project-level and parent-level cash flows in international project evaluation

- The use of forecast exchange rates and parity models for NPV calculations

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the main purpose of applying purchasing power parity (PPP) in international project appraisal?

- Explain the difference between project and parent cash flow viewpoints in the context of overseas investment evaluation.

- Which parity model assumes that forward exchange rates reflect interest rate differentials between two countries?

- True or false? Fluctuations in exchange rates only affect project cash flows if remittances to the parent are blocked.

Introduction

Evaluating overseas projects requires a clear understanding of how foreign exchange rates may impact projected returns. Comparison between the project’s local currency cash flows and what ultimately reaches the parent is essential. Exchange rates rarely remain stable, so future movements and the relationships between inflation, interest rates, and exchange rates must be considered for reliable investment appraisal.

This article examines the distinction between the project and parent viewpoints, outlines how exchange rate and parity models are used for forecasting, and demonstrates practical implications for multinational financial management.

PROJECT VERSUS PARENT CASH FLOWS

When a multinational considers investing in a foreign project, managers must project cash flows from two viewpoints:

- The project's standpoint, using the currency where operations occur

- The parent company's viewpoint, focusing on the currency in which group accounts and shareholder value are measured

Key Term: Project Cash Flows

All expected inflows and outflows generated by the investment, measured in the foreign (host country) currency over the project's life. Key Term: Parent Cash Flows

The net remittances, after conversion and possible restrictions, which the parent receives in its own currency as a result of the foreign investment.

The key challenge is that exchange rates can substantially alter the value of local profits once translated or remitted to the parent.

Main Steps in Foreign Project Appraisal

- Estimate free cash flows in the foreign currency (host country).

- Forecast exchange rates for the relevant years using a suitable parity relationship (PPP or IRP).

- Convert project cash flows into the parent’s currency as they are expected to be remitted.

- Discount parent-currency cash flows at an appropriate rate to estimate project NPV from the group viewpoint.

- Adjust for possible remittance restrictions, additional taxes or costs.

Key Considerations

- Not all foreign cash flows are automatically available to the parent.

- Withholding taxes, exchange control regulations, or blocked remittances may reduce the amounts that can be sent back.

- Timing differences between local cash generation and parent receipt can create additional FX risk.

EXCHANGE RATE FORECASTS AND PARITY MODELS

Uncertainty surrounds future exchange rates. Multinationals need a systematic approach to estimate likely rates to use in project assessment.

Exchange Rate Parity Concepts

Several economic theories guide exchange rate forecasts for investment appraisal.

Key Term: Purchasing Power Parity (PPP)

The theory that exchange rates will adjust over time so that identical goods cost the same in different countries, after conversion, due to inflation differentials. Key Term: Interest Rate Parity (IRP)

The theory that differences in nominal interest rates between two countries will be reflected in their forward exchange rates.

Using PPP to Forecast Future Spot Rates

The expected future spot rate is calculated as:

Where:

- = Expected future spot rate (foreign/base)

- = Current spot rate

- = Foreign (host) country inflation rate

- = Base (parent) country inflation rate

Using IRP for Forward Rates

The expected forward rate () is calculated as:

Where:

- = Interest rate in the foreign country

- = Interest rate in the parent country

Choosing the Appropriate Parity Model

- Use PPP when inflation differentials are expected to drive exchange rates and there is no liquid forward market.

- Use IRP when forward contracts exist and interest rates are the main drivers.

Exchange rate assumptions should be consistent with inflation and discount rate assumptions elsewhere in the appraisal. Always clarify which parity is being used, and the reasons, in any investment report.

Worked Example 1.1

A UK company forecasts the following inflation rates: UK: 4% per annum USA: 7% per annum Current spot rate: $1.50/£1

Calculate the forecast $/£ exchange rate in three years using PPP.

Answer:

Year 1: $1.50 × (1.07/1.04) = $1.54 Year 2: $1.54 × (1.07/1.04) = $1.59 Year 3: $1.59 × (1.07/1.04) = $1.63 Each year, the rate is 'rolled forward' by applying the inflation ratios.

PRACTICAL IMPLICATIONS FOR NPV ANALYSIS

Parity model choice depends on forward market liquidity, applying IRP for available forwards and PPP for expected spot-rate forecasts otherwise.

Cash Flow Conversion Methods

There are two primary methods for converting foreign project cash flows into the parent’s currency:

-

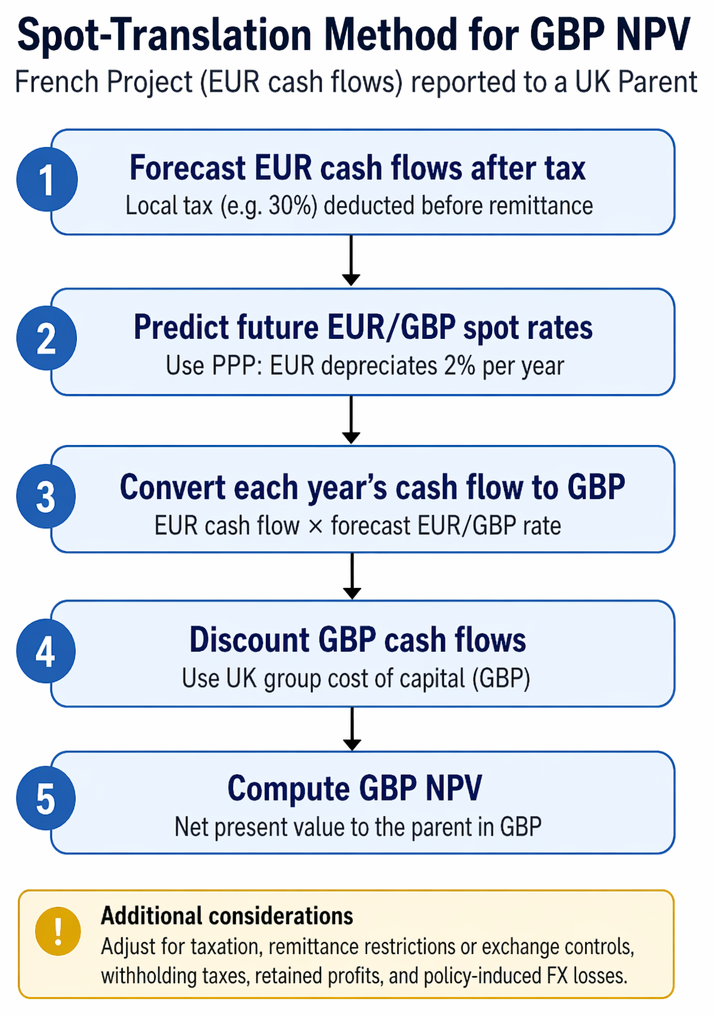

Spot-translation method:

- Forecast local currency cash flows.

- Use parity model (usually PPP) to predict future spot rates for expected remittances.

- Convert and discount at the parent’s required return, reflecting home-currency risk.

-

Local-currency NPV method:

- Discount local currency flows at an appropriate rate for host-country risk.

- Convert the resulting present value to the parent’s currency at the current spot rate.

Both methods should yield the same NPV if assumptions (including the parity model used and the risk profile) are consistent.

Additional Factors

- Adjust for any taxation (double-taxation treaties may limit additional tax) in either country.

- Allow for any remittance restrictions or exchange controls blocking or delaying parent currency inflows.

- Consider the impact of withholding taxes, mandatory retained profits, and policy-induced FX losses.

Worked Example 1.2

Question: A German parent is evaluating a French project. All operational cash flows are in euros, but the group reports in GBP. The euro is expected to depreciate against GBP 2% per year, matching relative inflation. Local tax at 30% is deducted before remittance; all profits are immediately paid to the parent. How does the group assess the GBP NPV?

Answer:

- Forecast euro project cash flows after tax.

- Apply expected exchange rate (using PPP with 2% annual depreciation) to each year’s euro cash flow.

- Convert to GBP, yielding annual parent cash flows.

- Discount at the UK group’s cost of capital (in GBP), after confirming that project risk is similar to existing group risk.

CHALLENGES AND COMMON ERRORS

Exam Warning: A common error is to discount local currency cash flows at the home country rate before converting at forecast rates—this results in inconsistent risk adjustment. Only discount in the currency you have used for cash flows, at a rate reflecting your risk assumptions for that currency.

Revision Tip: Always double-check that exchange rate forecasts are consistent with your inflation or interest rate assumptions elsewhere in your calculation.

Summary

International project appraisal requires careful conversion of project cash flows to the parent’s currency, reflecting expected exchange rate movements. Parity models (PPP and IRP) provide a rational basis for forecasting rates in line with inflation or interest rate assumptions. NPV calculations must account for cash flow restrictions, taxation, and use a consistent discount rate in the measurement currency.

Key Point Checklist

This article has covered the following key knowledge points:

- Explain the difference between project and parent cash flow viewpoints in international investment

- Identify and apply parity models (PPP and IRP) for exchange rate forecasting

- Convert local currency project cash flows to parent currency using forecast rates

- Select a consistent discount rate matching the currency and risk profile used

- Recognise potential issues such as remittance restrictions, double taxation, and witholding taxes in NPV analysis

Key Terms and Concepts

- Project Cash Flows

- Parent Cash Flows

- Purchasing Power Parity (PPP)

- Interest Rate Parity (IRP)