Learning Outcomes

After reading this article, you will be able to identify which costs form part of the initial measurement of property, plant, and equipment (PPE), apply the criteria for capitalisation, and clearly distinguish between capital expenditure and expenses. You will also learn to record PPE acquisition accurately in the accounting records in line with ACCA FA2 exam requirements.

ACCA Maintaining Financial Records (FA2) Syllabus

For ACCA Maintaining Financial Records (FA2), you are required to understand how property, plant, and equipment are recorded in business accounts. This includes knowing what can be included in the cost of these assets and how to classify expenditure correctly. You should focus your revision on:

- The definition of non-current assets and the distinction between current and non-current assets

- Identification and classification of capital (asset) expenditure versus revenue (expense) items

- The components of cost to include when recording PPE in the accounting records

- The correct journal entries to record the acquisition, including any claimable sales tax

- The consequences of incorrect classification of expenditure on the financial statements

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which of the following costs should always be capitalised as part of the initial cost of a machine (assuming sales tax is recoverable)?

- a) Delivery to the business premises

- b) Staff training costs

- c) Routine annual maintenance

- d) Costs of repainting after six months of use

-

True or false? If a new office printer costing £3,000 is recorded as 'Sundry Expenses' rather than as a non-current asset, the reported profit for the period will be understated.

-

What is the correct double entry to record the purchase of an item of factory machinery for $6,000 plus refundable sales tax of $1,200, purchased on credit?

-

Briefly explain why installation costs normally form part of the PPE cost.

Introduction

When a business acquires property, plant, and equipment (PPE)—such as vehicles, machinery, or computers—it is important to decide which costs are included as part of the asset’s value and which are regarded as expenses in the statement of profit or loss. The distinction directly affects reported profit and the financial position of the entity. This article sets out the ACCA FA2 requirements for identifying the direct and attributable costs to capitalise, when to expense costs, and how to apply the correct accounting entries.

Key Term: property, plant, and equipment (PPE)

Tangible items held for use in the production or supply of goods and services, for rental to others, or for administrative purposes, expected to be used for more than one accounting period.Test Tip: When revising Cost components and capitalisation policy, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

COST COMPONENTS OF PROPERTY, PLANT, AND EQUIPMENT

Determining the initial cost of PPE is not limited to its purchase price. Several other directly related costs must be considered.

Purchase Price and Directly Attributable Costs

The initial cost of PPE includes:

- Purchase price (including discounts and rebates)

- Import duties and non-refundable taxes (if applicable)

- Direct costs necessary to bring the asset to its intended location and condition for use

These might include:

- Delivery and handling charges

- Installation and assembly costs

- Site preparation (e.g. preparing a base for machinery)

- Professional fees (such as engineers or architects)

Key Term: directly attributable cost

Expenditure necessary to bring an asset to the location and condition required for it to operate as intended.

Expenditure to be Capitalised vs. Expensed

It is essential to distinguish between capital (asset) expenditure and revenue (expense) expenditure:

-

Capital expenditure increases the value of non-current assets and brings future economic benefit. It is included in the PPE cost and shown on the statement of financial position.

-

Expense (revenue) expenditure relates to the day-to-day running or routine maintenance of assets and is charged to the statement of profit or loss in the period incurred.

Key Term: capital expenditure

Spending on acquiring or improving non-current assets to bring future economic benefit. Key Term: expense (revenue) expenditure

Costs incurred for maintenance, repairs, or operational running that do not increase asset value or useful life, recognised immediately as expenses.

Common Costs and Their Treatment

Included in PPE cost (capitalise):

- Initial purchase price minus trade discounts

- Delivery and insurance while in transit

- Installation and assembly

- Legal and registration fees to acquire title

- Testing and trial run costs (net of proceeds from testing)

Expensed immediately:

- Repairing damage during delivery

- Initial operating losses after the asset is ready for use

- Routine maintenance, servicing, and minor repairs

- Training for staff

Claimable Sales Tax

If the business can recover input sales tax/VAT, only the net (exclusive of sales tax) is capitalised. The recoverable tax is recorded as a receivable from the tax authority.

Worked Example 1.1

A business purchases a machine with the following costs:

- List price: $10,000 (minus $500 trade discount)

- Installation and assembly: $800

- Deliveries to site: $300

- Staff training: $700

- First-year service contract: $400

- Non-refundable sales tax: $1,200

Question: What is the capitalised cost of the machine?

Answer:

- Purchase after discount = $10,000 – $500 = $9,500

- Installation and assembly = $800

- Delivery = $300

- Non-refundable sales tax = $1,200

- Staff training and service contract are not directly attributable; they are expensed.

- Total capitalised cost: $9,500 + $800 + $300 + $1,200 = $11,800

Exam Warning: Be clear on which costs can be included in PPE and which cannot. Costs for staff training and annual servicing are frequently included incorrectly. Only costs directly bringing the asset to useable condition are capitalised.

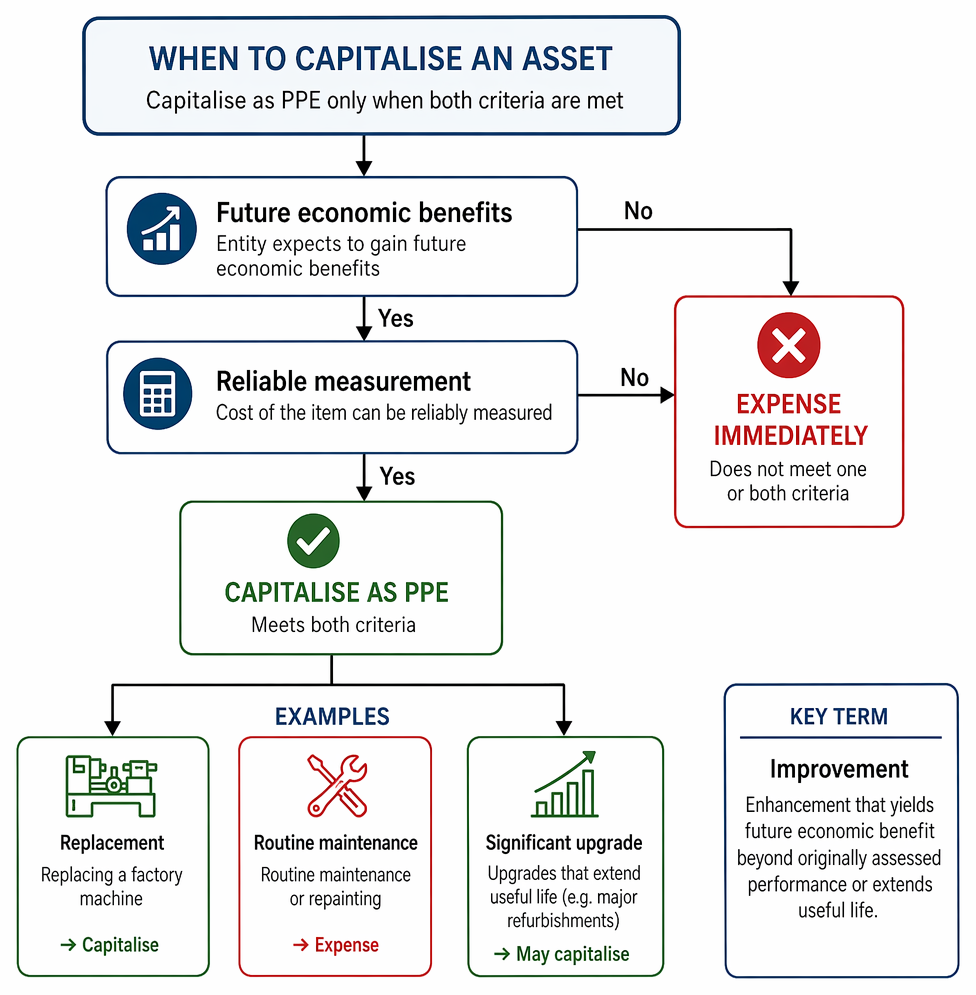

CAPITALISATION POLICY: WHEN TO RECOGNISE AN ASSET

An item is capitalised as PPE only when:

Expenditure is classified as property, plant, and equipment only when future economic benefits are probable and cost is reliably measurable.

- The entity expects to gain future economic benefits

- The cost of the item can be reliably measured

If an expenditure does not meet these criteria, it must be expensed immediately.

Expenses vs. Asset Expenditure: Key Distinctions

Examples:

- Replacing a factory machine is capital expenditure.

- Routine maintenance or repainting is expensed.

- Upgrades that significantly extend useful life (e.g. major refurbishments) may be capitalised.

Worked Example 1.2

A company buys office furniture for $3,000. The invoice is correctly posted to 'Office Equipment.' Later, $600 is spent on repairing scratches, which is wrongly added to the asset account.

Question: What is the effect of this error on profit and asset value?

Answer:

- Capitalising repairs overstates assets and profit (repairs should reduce profit immediately).

- The assets are overstated by $600. Profit is overstated by $600, as the repair should be an expense.

Asset Improvements and Replacements

Subsequent costs to PPE should only be capitalised when they improve or significantly prolong the asset’s life. Routine repairs, servicing, and recurring costs are always expensed.

Key Term: improvement

An enhancement that yields future economic benefit beyond the asset’s originally assessed performance or extends its useful life.

RECORDING PPE ACQUISITION IN THE GENERAL LOGER

When a PPE item is acquired, use the following standard double entry (assuming sales tax is recoverable):

- Debit: PPE (at net cost, excluding recoverable sales tax)

- Debit: Recoverable sales tax (if applicable)

- Credit: Payables (or Cash at bank) for total gross amount

Worked Example 1.3

A business buys a machine for $5,000 plus $1,000 VAT (input tax claimable). Payment is due in 30 days.

Question: Show the correct general ledger entries.

Answer:

- Debit PPE: $5,000

- Debit Sales Tax Receivable: $1,000

- Credit Payables: $6,000

IMPACT OF MISCLASSIFICATION

Misclassifying capital expenditure as an expense will:

- Understate assets on the statement of financial position

- Understate profit (due to immediate expensing)

Misclassifying expenses as asset purchases will:

- Overstate assets

- Overstate profit in the short term (since the cost will only reduce profit through depreciation over time)

Summary

To comply with the ACCA FA2 syllabus, be able to:

- Identify which costs should be included in the cost of PPE

- Apply correct capitalisation policy to new expenditure

- Distinguish asset expenditure from routine expenses

- Record acquisitions in the general ledger with correct treatment of taxes

- Avoid common exam errors by focusing on the nature and purpose of each cost

Key Point Checklist

This article has covered the following key knowledge points:

- Identify all cost components to include in the initial measurement of PPE

- Distinguish capital expenditure from expenses, with real examples

- Understand which subsequent costs to capitalise and which to expense

- Correctly account for recoverable sales tax when acquiring PPE

- Apply the correct double-entry for asset acquisition

- Explain financial statement effects of misclassification

Key Terms and Concepts

- property, plant, and equipment (PPE)

- directly attributable cost

- capital expenditure

- expense (revenue) expenditure

- improvement