Learning Outcomes

After reading this article, you will be able to explain the purpose of depreciation, describe and apply both straight line and reducing balance depreciation methods, perform relevant calculations, and correctly record depreciation and disposals in the general ledger for property, plant, and equipment (PPE) in accordance with ACCA FA2 requirements.

ACCA Maintaining Financial Records (FA2) Syllabus

For ACCA Maintaining Financial Records (FA2), you are required to understand how tangible non-current assets—property, plant, and equipment—are accounted for in respect of depreciation. This article directly supports your revision of the following syllabus points:

- Define property, plant, and equipment as tangible non-current assets.

- Explain the reason and purpose for depreciation.

- Distinguish between straight line and reducing (diminishing) balance depreciation methods.

- Calculate depreciation charges using both methods, including for part years.

- Record depreciation and accumulated depreciation in the general ledger.

- Account for disposals of tangible non-current assets, including calculation and recording of gains or losses on disposal.

- Present PPE and accumulated depreciation in the financial statements.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- A delivery van has a cost of $12,000, an estimated useful life of 4 years, and a residual value of $2,000. What is the annual depreciation charge using the straight line method?

- A machine is depreciated using the reducing balance method at 25% per year. Its current carrying amount is $8,000. What is the depreciation charge for this year?

- True or false? All non-current assets, including freehold land, must be depreciated each year.

- What double entry records the annual depreciation charge?

- Briefly describe how a profit or loss on disposal of PPE arises and where it is reported.

Introduction

Property, plant, and equipment (PPE) are tangible non-current assets held for long-term use within a business. As these assets are used over multiple periods, their cost must be allocated across the expected useful life to accurately reflect their consumption and comply with the accruals concept. Depreciation ensures that financial statements present a fair view of profit and financial position by spreading the cost of PPE over the periods benefiting from their use. Exam questions frequently test your knowledge of depreciation definitions, calculation methods, double-entry bookkeeping entries, and understanding of disposals.

Key Term: depreciation

A systematic allocation of the depreciable amount of a tangible non-current asset over its useful life. Key Term: carrying amount

The value of a non-current asset shown in the statement of financial position; calculated as original cost less accumulated depreciation.Test Tip: When revising Depreciation methods and calculations, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Purpose of Depreciation

Depreciation applies to all non-current assets with a finite useful life, such as buildings, vehicles, and machinery. Its main aim is to allocate the asset’s cost—less any estimated residual value—across the years that benefit from its use, in line with the accruals concept.

Assets such as land, unless subject to depletion, are not depreciated. The annual depreciation charge is typically estimated, as the asset’s actual useful life and final value may only be known when it is disposed of.

Key Term: useful life

The period over which an asset is expected to be available for use by the entity. Key Term: residual value

The estimated amount an entity expects to receive for an asset at the end of its useful life, after deducting expected costs of disposal.

Depreciation expense is not a cash flow and does not set aside funds for asset replacement.

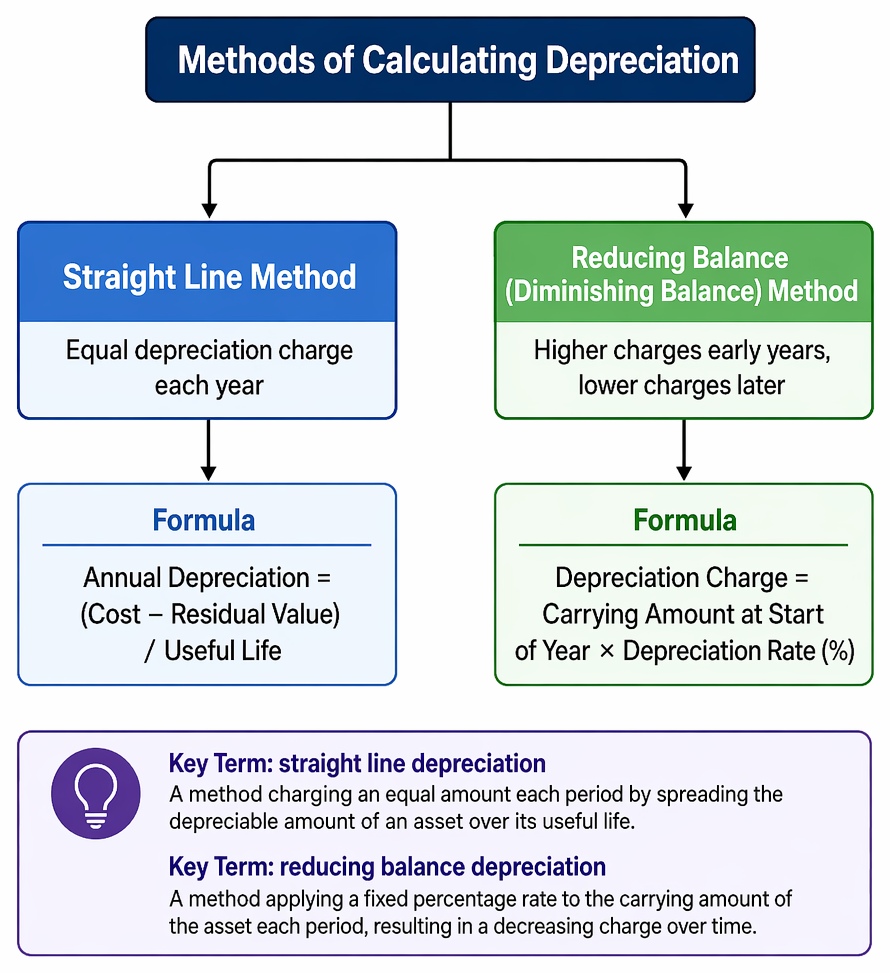

Methods of Calculating Depreciation

Two main methods are commonly used in practice:

Property, plant and equipment depreciation links method choice and period charge to expense recognition, accumulated depreciation, and carrying amount presentation.

Straight Line Method

This method assumes the asset will be consumed evenly over its useful life and results in an equal depreciation charge each year.

The formula is:

Annual Depreciation = (Cost – Residual Value) / Useful Life

Reducing Balance (Diminishing Balance) Method

This approach assumes that the asset is used more heavily in earlier years, so higher depreciation is charged in early years and lower charges in later years. The depreciation rate is applied to the asset’s carrying amount at the start of each period.

The formula is:

Depreciation Charge = Carrying Amount at Start of Year × Depreciation Rate (%)

Key Term: straight line depreciation

A method charging an equal amount each period by spreading the depreciable amount of an asset over its useful life. Key Term: reducing balance depreciation

A method applying a fixed percentage rate to the carrying amount of the asset each period, resulting in a decreasing charge over time.

Calculating Depreciation for Part Years

Assets may be acquired or disposed of part-way through an accounting year. In such cases, depreciation must be charged for the period in which the asset was held by the entity, usually on a monthly or prorated basis.

Some entities charge a full year’s depreciation in the year of acquisition and none on disposal; others apply a strict pro rata calculation. Be led by the question's instruction in the exam.

Recording Depreciation in the General Ledger

Each year, depreciation is recorded as an expense in the statement of profit or loss and credited to an accumulated depreciation account, which is deducted from the asset’s cost in the statement of financial position to show its carrying amount.

Double-entry:

- Debit: Depreciation expense (in SPL)

- Credit: Accumulated depreciation (in SFP)

Accumulated depreciation is a cumulative balance, increased each year by the depreciation charge.

Presenting PPE in Financial Statements

In the statement of financial position, each class of PPE is usually shown at cost, less accumulated depreciation, to give carrying amount. In the statement of profit or loss, depreciation is included among operating expenses.

Disposal of Property, Plant, and Equipment

When a non-current asset is sold, scrapped, or part-exchanged, the following steps must be completed:

- Remove the asset’s cost from the relevant asset account.

- Remove related accumulated depreciation.

- Record the proceeds received (cash or other asset).

- Calculate the profit or loss on disposal as the difference between carrying amount and proceeds received.

The resulting profit or loss is shown in the statement of profit or loss.

Key Term: profit or loss on disposal

The difference between the disposal proceeds and the carrying amount of a non-current asset at the date of its disposal.

Worked Example 1.1

Worked Example 1.1

A company purchases equipment for $18,000. The estimated useful life is 6 years, with a residual value of $3,000. Calculate the annual depreciation charge using the straight line method.

Answer:

The depreciable amount is $18,000 – $3,000 = $15,000. Annual depreciation = $15,000 ÷ 6 years = $2,500 per year.

Worked Example 1.2

A business purchases machinery for $10,000 on 1 January, using reducing balance depreciation at 30%. What is the depreciation charge for Year 1 and the carrying amount at the end of Year 2?

Answer:

Year 1 depreciation: $10,000 × 30% = $3,000; carrying amount = $7,000. Year 2 depreciation: $7,000 × 30% = $2,100; carrying amount = $4,900.

Worked Example 1.3

An entity buys a delivery van for $12,000 (estimated useful life: 4 years, residual value: $2,000). After three years, the asset is sold for $3,500. Depreciation is calculated straight line. Calculate profit or loss on disposal.

Answer:

Annual depreciation = ($12,000 – $2,000) ÷ 4 = $2,500 per year. Accumulated depreciation after 3 years = $2,500 × 3 = $7,500. Carrying amount at disposal = $12,000 – $7,500 = $4,500. Proceeds = $3,500; loss on disposal = $4,500 – $3,500 = $1,000.Exam Warning: Failing to use the method specified in a question or omitting residual value in calculations is a common source of lost marks. Always check for part-period adjustments if the asset is acquired or disposed mid-year.

Summary

Depreciation allocates the cost of PPE over its useful life and is necessary for accurate financial reporting and compliance with the accruals concept. Two main methods are examined: straight line (equal annual charges) and reducing balance (declining annual charges). Depreciation is recorded annually via double entry. Accurate calculation and presentation, including accumulated depreciation and disposals, are essential for ACCA FA2 exam success.

Key Point Checklist

This article has covered the following key knowledge points:

- Define depreciation, carrying amount, useful life, and residual value.

- Explain why depreciation is necessary for non-current assets (except land).

- Calculate depreciation using straight line and reducing balance methods, with adjustments for partial periods.

- Record depreciation and accumulated depreciation in general ledger accounts.

- Account for disposals, including calculation and recording of gains or losses on disposal.

- Present PPE and related balances correctly in financial statements.

Key Terms and Concepts

- depreciation

- carrying amount

- useful life

- residual value

- straight line depreciation

- reducing balance depreciation

- profit or loss on disposal