Learning Outcomes

After reading this article, you will be able to explain and apply effective methods for understanding, documenting, and evaluating accounting and internal control systems. You will learn the exam-relevant features, purposes, and differences between internal control questionnaires (ICQs), internal control evaluation questionnaires (ICEQs), and checklists. You will also be able to illustrate how these tools are constructed and used in audit assignments.

ACCA Foundations in Audit (FAU) Syllabus

For ACCA Foundations in Audit (FAU), you are required to understand the main techniques available to auditors for recording and evaluating accounting systems, particularly in the context of assessing internal controls. Revision for this article should focus on:

- Techniques for understanding and documenting accounting systems (narrative notes, flowcharts, organisation charts, questionnaires)

- Techniques used to evaluate accounting systems (ICQs, ICEQs, checklists)

- Construction and purpose of ICQs and ICEQs

- Use of checklists for compliance and system evaluation

- Identifying strengths and weaknesses in controls from completed questionnaires

- Reporting control deficiencies found in evaluation

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which tool is typically used to confirm whether specific controls exist within an accounting system?

- a) Flowchart

- b) ICQ

- c) Analytical procedure

- d) Audit plan

-

State two key differences between an ICQ and an ICEQ in the context of internal control evaluation.

-

When should an auditor use a checklist rather than a questionnaire?

-

True or false? A "Yes" answer in an ICEQ always indicates a control strength.

Introduction

Auditors must achieve a detailed understanding of a client’s accounting systems and internal controls before they can plan effective audit procedures. Several techniques are used for this purpose, and systematic evaluation determines whether controls are robust or need further attention. Three principal evaluation tools—ICQs, ICEQs, and checklists—are frequently examined in ACCA FAU and must be understood for practical and exam success.

Techniques to Understand, Record and Evaluate Systems

Auditors are expected to clarify how an accounting system operates and to assess whether sufficient controls are present and effective. The main steps include understanding the system, recording its structure, and evaluating its strengths and weaknesses.

Techniques to Understand and Record Accounting Systems

Common methods include:

- Narrative notes: Clear descriptions in written form; useful for very simple systems.

- Organisation charts: Visual depiction of reporting lines but lacking operational details.

- Flowcharts: Diagrams showing flow of documents, transactions, and responsibilities; especially effective for complex systems.

- Questionnaires: Systematic series of questions to determine presence and adequacy of controls.

These tools provide the basis for formal evaluation.

Key Term: Flowchart

A diagrammatic representation of an accounting or control system, showing the sequence of transactions, documents, and controls visually.

Evaluation Techniques: ICQs, ICEQs, and Checklists

Once a system is understood and documented, auditors must evaluate its effectiveness using structured tools.

Internal Control Questionnaires (ICQs)

An Internal Control Questionnaire (ICQ) is a structured set of short, focused questions designed to determine what controls exist in the client’s system.

Key Term: Internal Control Questionnaire (ICQ)

A standardised list of questions used to determine whether specific controls exist within an accounting system and to identify control deficiencies.

ICQs focus on features such as authorisation, segregation of duties, documentation, and custody. Each question is drafted so that a "Yes" answer typically confirms a control is present, while a "No" reveals a possible deficiency.

ICQs are commonly used for large, complex systems where reliance on controls is intended. Their systematic, tick-box structure can, however, encourage superficial completion if not actively reviewed.

Construction and Format of an ICQ

- Questions grouped by transaction stage (e.g., ordering, authorisation, custody)

- Space for Yes/No responses, comments, and references

- Direct mapping to control objectives (e.g., "Are goods received independently checked against orders and invoices?")

ICQs are best suited to identifying areas where controls formally exist and flagging gaps for further testing or management communication.

Internal Control Evaluation Questionnaires (ICEQs)

An Internal Control Evaluation Questionnaire (ICEQ) is focused on determining whether the system can prevent or detect specific types of errors or frauds.

Key Term: Internal Control Evaluation Questionnaire (ICEQ)

A document using direct questions to assess the system’s ability to prevent or detect specific risks by focusing on potential errors or frauds.

ICEQs differ from ICQs in structure and logic. Instead of asking if a control exists, they ask if a problem or risk "can" occur (e.g., "Can unauthorized purchases be made?"). A "No" answer is desirable, as it implies appropriate controls stop the risk; a "Yes" answer signals a deficiency to be addressed.

ICEQs are usually shorter, more intuitive for experienced auditors, and are particularly useful following system walkthroughs or flowchart reviews.

Construction and Format of an ICEQ

- Starts with key risk questions (e.g., "Can liabilities be incurred without proper supporting documents?")

- Supplementary sub-questions examine how exposures are monitored

- References to evidence and comments as needed

ICEQs are best for highlighting significant weaknesses and focusing audit effort where risks cannot be eliminated by existing controls.

Checklists

Checklists are pre-prepared lists used to confirm the completion of necessary steps, documentation, or compliance requirements.

Key Term: Checklist

A standardised list used by auditors to confirm that required procedures, steps, or criteria have been applied or completed within an audit area.

Checklists are used in multiple settings:

- Compliance (ensuring all steps of a process are followed)

- Review (verifying that all required disclosures are included)

- Final audit file completion

While efficient, over-reliance on checklists can risk mechanical box-ticking if not combined with auditor judgement.

Worked Example 1.1

Question: You are assigned to evaluate the purchases system at Levenson Ltd. Management claim their process is fully controlled. How would you use ICQs and ICEQs to identify system weaknesses?

Answer:

- Completing an ICQ, you ask if purchase orders are pre-numbered and authorised. A "No" response highlights missing controls that could allow unauthorised orders.

- Using an ICEQ, you would ask, "Can purchases be made without evidence of approval?" If "Yes", this directly indicates the system exposes the company to unauthorised purchases, regardless of whether existing controls are claimed.

- The ICQ helps you spot absent formal controls; the ICEQ highlights if controls are effective at preventing risks.

Worked Example 1.2

The sales returns process at Proline Co. lacks written procedures. As an auditor, how could a checklist help preserve audit quality here?

Answer:

- You prepare or use a sales returns checklist listing steps such as collecting returns forms, checking goods received, authorising credit notes, and updating the sales ledger.

- By following the checklist, you can confirm that every necessary task has been completed and documented, reducing risk of omitted controls and supporting your audit file.

Exam Warning: Completing questionnaires or checklists mechanically without considering actual system operation can miss disguised deficiencies. Always review responses for inconsistencies and investigate "No" answers or unclear justifications.

Revision Tip: When constructing ICQs and ICEQs, frame questions clearly and tailor them to the client’s processes. For exam questions, state both the control objective and example question.

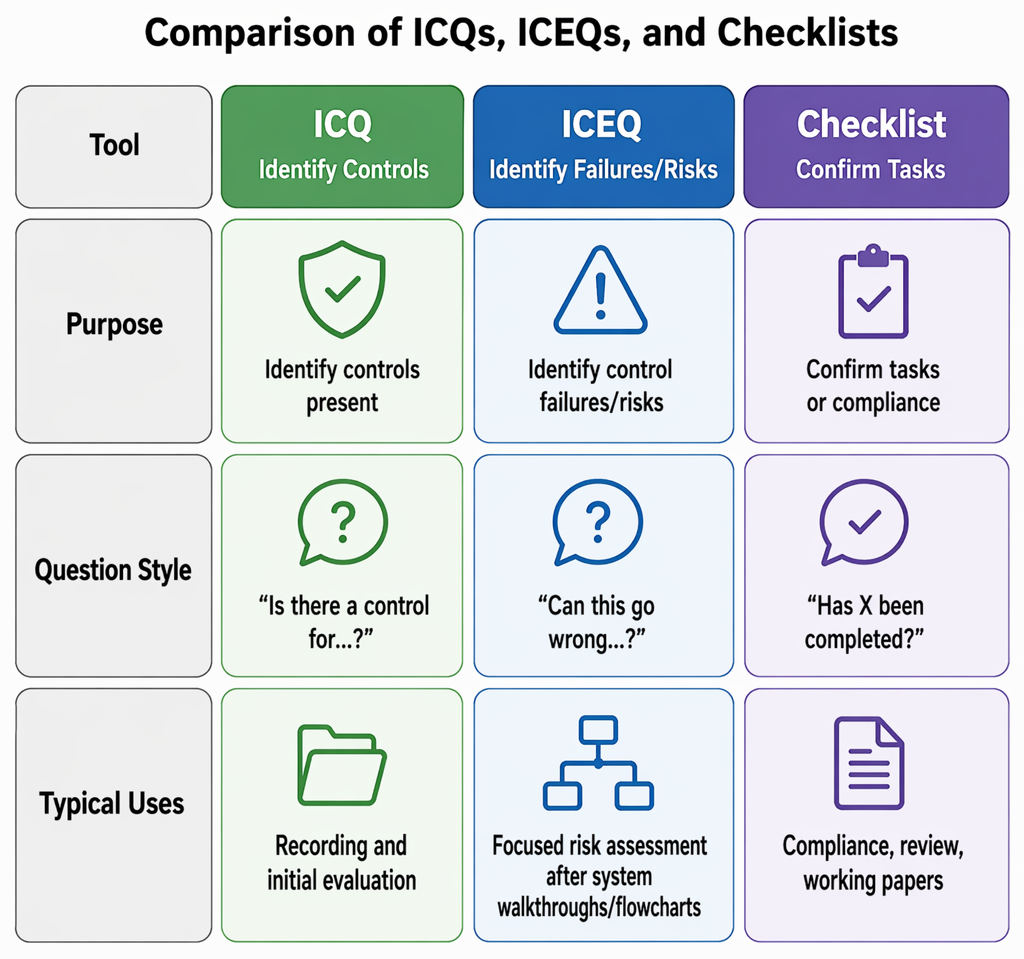

Comparison of ICQs, ICEQs, and Checklists

Evaluation objectives are mapped to ICQs, ICEQs, and checklists according to control existence, risk occurrence, and compliance review purposes.

| Tool | Purpose | Question Style | Typical Uses |

|---|---|---|---|

| ICQ | Identify controls present | "Is there a control for...?" | Recording and initial evaluation |

| ICEQ | Identify control failures/risks | "Can this go wrong...?" | Focused risk assessment after system walkthroughs/flowcharts |

| Checklist | Confirm tasks or compliance | "Has X been completed?" | Compliance, review, working papers |

Summary

Auditors use ICQs, ICEQs, and checklists to systematically and consistently evaluate and document accounting and internal control systems. ICQs focus on confirming controls exist, ICEQs focus on whether errors or frauds can occur, and checklists support standardized completion of audit tasks. Effective use—and understanding which tool to use for what purpose—is essential for audit quality and assurance.

Key Point Checklist

This article has covered the following key knowledge points:

- The main techniques for understanding and documenting accounting systems

- Definition, format, and application of internal control questionnaires (ICQs)

- Definition, structure, and use of internal control evaluation questionnaires (ICEQs)

- The purpose and use of checklists in audit assignments

- Key differences between ICQs, ICEQs, and checklists

- Typical exam requirements relating to system evaluation tools

Key Terms and Concepts

- Flowchart

- Internal Control Questionnaire (ICQ)

- Internal Control Evaluation Questionnaire (ICEQ)

- Checklist