Learning Outcomes

After reading this article, you will be able to describe methods for understanding, recording, and evaluating accounting systems, especially narrative notes and flowcharts. You will learn to explain their uses, strengths and weaknesses, and to apply these methods to support audit planning and internal control assessment.

ACCA Foundations in Audit (FAU) Syllabus

For ACCA Foundations in Audit (FAU), you are required to understand the common techniques auditors use to understand, record, and evaluate systems of accounting and internal control. In particular, you should focus your revision on:

- Techniques auditors use to gain knowledge of accounting systems, including narrative notes and flowcharts

- Methods of documenting system understanding in audit working papers

- The strengths and limitations of narrative notes and flowcharts as documentation tools

- How flowcharts can be applied and interpreted in practical audit scenarios

- The importance of proper documentation in assessing internal controls and identifying deficiencies

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which method provides a visual diagram of the flow of documents and procedures in a system?

- a) Narrative notes

- b) Organisation charts

- c) Flowcharts

- d) Internal control questionnaires

-

Give one key advantage and one disadvantage of using narrative notes to document a system.

-

What is the main purpose of using flowcharts in documenting accounting systems?

-

True or false? Narrative notes are always sufficient for documenting complex accounting systems.

Introduction

To assess and test internal controls effectively, auditors must first obtain a clear understanding of the client’s accounting systems. This involves not only gaining knowledge but also recording that knowledge in a form that supports the audit process. Understanding and documentation are essential for risk assessment and audit planning, and ACCA candidates must be able to select and justify appropriate methods.

Two primary techniques used in practice are narrative notes and flowcharts. Each offers a different approach to capturing and communicating how transactions are processed and how internal controls operate within a system.

Techniques for Understanding Accounting Systems

Before documenting a system, auditors use techniques such as:

- Interviews with client staff

- Walk-through tests (following a transaction through the system)

- Inspection of client documentation

- Observation of client procedures

Key Term: Walk-through test

A walk-through test involves following a transaction through the system to understand how procedures and controls operate in practice.

These methods help auditors establish how processes actually work in practice—highlighting key controls, authorisations, and potential weaknesses.

Documenting Systems: Narrative Notes and Flowcharts

Accurate documentation is critical for planning and evidence. The two most common forms are narrative notes and flowcharts.

Documentation method choice assigns simple routine processes to narrative notes and complex multi-department systems requiring control visualisation to flowcharts.

Narrative Notes

Narrative notes are written descriptions outlining how a particular accounting system operates. They typically set out, in logical order, the sequence of events from initiation of a transaction to its final entry in the accounting records.

Key Term: Narrative notes

Narrative notes are written descriptions that detail the stages, people involved, and controls applied within an accounting or control system.

Narrative notes are particularly useful for simple, linear systems, or when documenting specific parts of a process.

Strengths:

- Simple to prepare for small or straightforward systems

- Clearly identifies responsibilities and steps

Limitations:

- Can become lengthy, repetitive, and hard to follow for complex systems

- Difficult to spot missing steps or weaknesses at a glance

- Time-consuming to update if changes are made

Exam Warning: Narrative notes are not always sufficient for larger or complex systems; explain when a flowchart would give clearer documentation.

Flowcharts

Flowcharts are diagrammatic representations of accounting processes, showing the flow of documents, operations, checks, and authorisations across different departments.

Key Term: Flowchart

A flowchart is a diagram using standard symbols to show the flow of documents, activities, checks, and information within a system.

Flowcharts are especially useful for visualising complex or multi-department processes and for highlighting internal controls, segregation of duties, and the sequence of processing.

Advantages:

- Easier to interpret complex systems at a glance

- Highlights control points, segregations of duties, and information flows

- Helps identify missing or duplicate steps

Disadvantages:

- Preparing high-quality flowcharts requires training and familiarity with standard symbols

- Complex systems may lead to crowded or difficult-to-read charts

- Less suitable for explaining unusual or rare transactions, where narrative is clearer

Test Tip: In exam answers, link the documentation method to the nature of the system: simple routine processes often suit narrative notes, while complex multi-department systems usually suit flowcharts.

Standard Flowchart Symbols (for Manual Systems)

Some standard symbols widely used in auditing include:

- Rectangle: Process or operation (e.g., calculation, preparation)

- Diamond: Check or verification point

- Line: Flow of documents (vertical for same department, horizontal for transfer)

- Dotted line: Flow of information (not actual document)

- Cylinder: Permanent file/document archive

Flowcharts should always be supplemented by brief supporting notes if the system includes non-routine or unusual transactions.

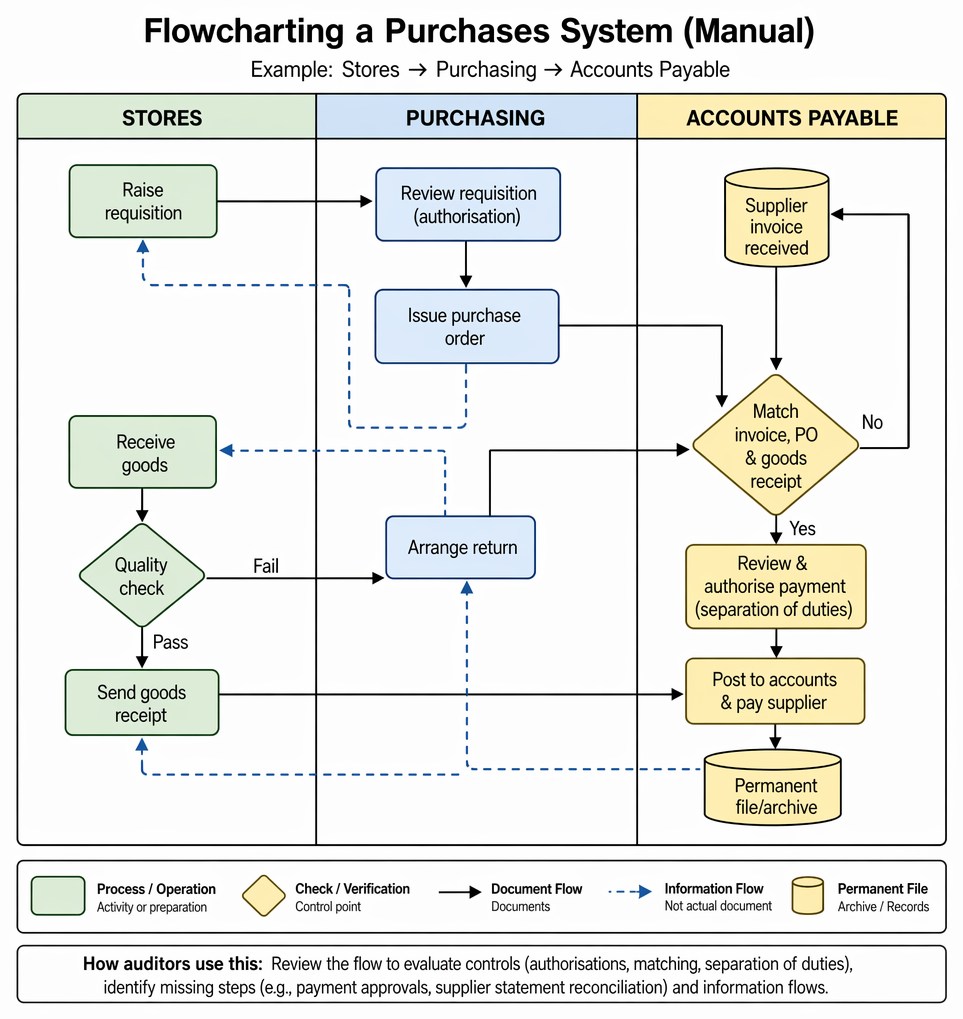

Worked Example 1.1

A company operates a purchases system where ordering is initiated by a requisition, reviewed by purchasing, and goods received are subject to quality checks before invoices are approved and posted. The system involves three departments: Stores, Purchasing, and Accounts Payable.

Question: How could an auditor use a flowchart to document and evaluate this purchases system?

Answer:

- The auditor draws columns for each department and uses standard symbols to map each stage: stores raise requisition, purchasing reviews and generates purchase order, goods are received and checked, invoice and receipt documents are matched and reviewed by Accounts Payable for approval and posting.

- Reviewing the flowchart, the auditor checks for key controls (e.g., authorisations, matching documents, separation of duties).

- Any steps missing—such as approval of payments or reconciliation of supplier statements—are more easily identified visually than in narrative notes.

Worked Example 1.2

A small consultancy has a straightforward sales system where invoices are issued by the financial controller after services are completed, and the managing director reviews monthly sales totals.

Question: Should the auditor use narrative notes or a flowchart here, and why?

Answer:

- Narrative notes are often sufficient for small, simple systems like this, as the process can be described fully in a few sentences.

- Using a flowchart may not add value and could overcomplicate a simple process.

Using Documentation to Evaluate Controls

Once the system is documented—whether by narrative, flowchart, or both—the auditor evaluates whether controls are adequate to prevent or detect errors and fraud.

The documentation helps answer:

- Are controls (e.g., authorisations, reconciliations) built into each key step?

- Is segregation of duties maintained?

- Are supporting documents retained at each stage?

- Where are potential control weaknesses or gaps?

Deficiencies or missing controls identified during evaluation can then be targeted for testing or further enquiry.

Exam Warning: Do not only describe the system; use the documentation to identify control points, missing controls, and possible weaknesses.

Revision Practice

Familiarize yourself with standard flowchart symbols and practice drawing simple process diagrams. In the exam, you may be asked to interpret a flowchart or identify strengths and weaknesses in a given diagram.

Summary

Documenting accounting systems is essential for effective audits. Narrative notes suit simple processes but can quickly become cumbersome for larger systems. Flowcharts provide a visual, efficient method for capturing and evaluating complex processes, making it easier to identify control points and weaknesses. Auditors must choose the appropriate documentation method to ensure accurate understanding and effective evaluation of internal controls.

Key Point Checklist

This article has covered the following key knowledge points:

- The purpose and techniques for understanding, recording, and evaluating accounting systems

- The use, strengths, and limitations of narrative notes in system documentation

- The use, strengths, and limitations of flowcharts for documenting complex systems

- Identification and explanation of standard flowchart symbols and features

- The role of documentation in supporting system evaluation and internal control assessment

Key Terms and Concepts

- Walk-through test

- Narrative notes

- Flowchart