Learning Outcomes

After reading this article, you will be able to explain the different sources of finance used by companies, including ordinary share issues, preference shares, and retained earnings. You will understand the distinct rights attached to each type, how these sources are presented in the financial statements, and the implications for shareholders and companies from a legal and accounting standpoint.

ACCA Foundations in Financial Management (FFM) Syllabus

For ACCA Foundations in Financial Management (FFM), you are required to understand the forms and implications of company finance. In particular, you should focus your revision on:

- The distinction between equity (ordinary share) capital and preference share capital

- The specific rights of ordinary and preference shareholders

- The criteria for classifying preference shares as debt or equity

- The meaning and role of retained earnings

- How each source of finance is accounted for and disclosed in the statement of financial position

- The impact of each source on dividends, voting rights, and risk for shareholders

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which of the following statements is true regarding retained earnings?

- a) They are a legal reserve of cash available for dividends

- b) They represent accumulated profits not yet distributed

- c) They must be used to fund future asset purchases

- d) They reduce the total equity of a company

-

Ordinarily, which shareholders have both voting rights and the right to residual assets on winding up?

- a) Debenture holders

- b) Ordinary shareholders

- c) Preference shareholders

- d) Directors

-

What is the main difference between redeemable and irredeemable preference shares in terms of classification on the statement of financial position?

-

A company decides not to pay a dividend this year. What is the consequence for its retained earnings?

Introduction

Companies raise finance using a mix of sources, each with legal, economic, and reporting consequences. The main long-term sources for limited companies are the issue of ordinary shares, preference shares, and the retention of earnings. Understanding these sources and their accounting treatment is fundamental for the ACCA exam and practical company analysis.

EQUITY FINANCE: ORDINARY SHARES

Ordinary shares (also called equity shares) form the core of a company’s capital. These shares give holders ownership of the company, full voting rights at general meetings, and a claim on the residual assets after all other obligations have been settled. Ordinary shareholders are entitled to dividends as declared by the company, but these are not guaranteed and may vary year by year.

Key Term: Ordinary shares

Equity instruments issued by a company that give the holder rights to residual assets and profits, usually including voting rights.

PREFERENCE SHARES

Preference shares are another source of company finance. Preference shareholders typically receive a fixed dividend before ordinary shareholders receive any payments. Depending on the type, they may or may not have voting rights and can be redeemable (repayable at a set date or at the company’s option) or irredeemable.

Key Term: Preference shares

Shares that give holders priority over ordinary shareholders for dividends and capital repayment, often at a fixed rate, with limited or no voting rights. Key Term: Redeemable preference shares

Preference shares that the issuing company is obliged to repay at a specified future date or at the shareholder's or company’s option. Key Term: Irredeemable preference shares

Preference shares with no fixed redemption date; they may exist indefinitely and are treated as equity if they carry no mandatory repayment.

Preference shares can be classified as either equity or liabilities in the financial statements, depending on the company’s obligation to repay. If there is a contractual obligation to redeem the shares for cash or another financial asset, they are treated as debt in accordance with accounting standards.

Rights attached to different shares

- Ordinary shares: Voting rights, variable dividends, residual claim on assets.

- Preference shares: Priority fixed dividends, usually non-voting, preferential return of capital.

Worked Example 1.1

A company issues 100,000 $1 irredeemable, non-cumulative 8% preference shares. In the current year, it declares no dividend due to low profits. What rights do the preference shareholders have regarding the unpaid dividend?

Answer:

For non-cumulative irredeemable preference shares, if no dividend is declared, holders lose the right to the current year's dividend. If the shares were cumulative, missed dividends would accrue for future payment.Exam Warning: Be alert: Preference shares that must be repaid (redeemable) are normally classified as liabilities, not equity, for accounting purposes, regardless of their legal name.

RETAINED EARNINGS

Retained earnings are not a source of new external finance but are an internal source. Companies often choose to retain profits rather than pay out all earnings as dividends. These ‘retained earnings’ accumulate as a component of equity in the statement of financial position and can be used to fund company operations, invest in assets, or pay down debt.

Key Term: Retained earnings

The cumulative net profits of a company that have not been distributed as dividends, available for reinvestment or future distribution.

ACCOUNTING FOR SOURCES OF FINANCE

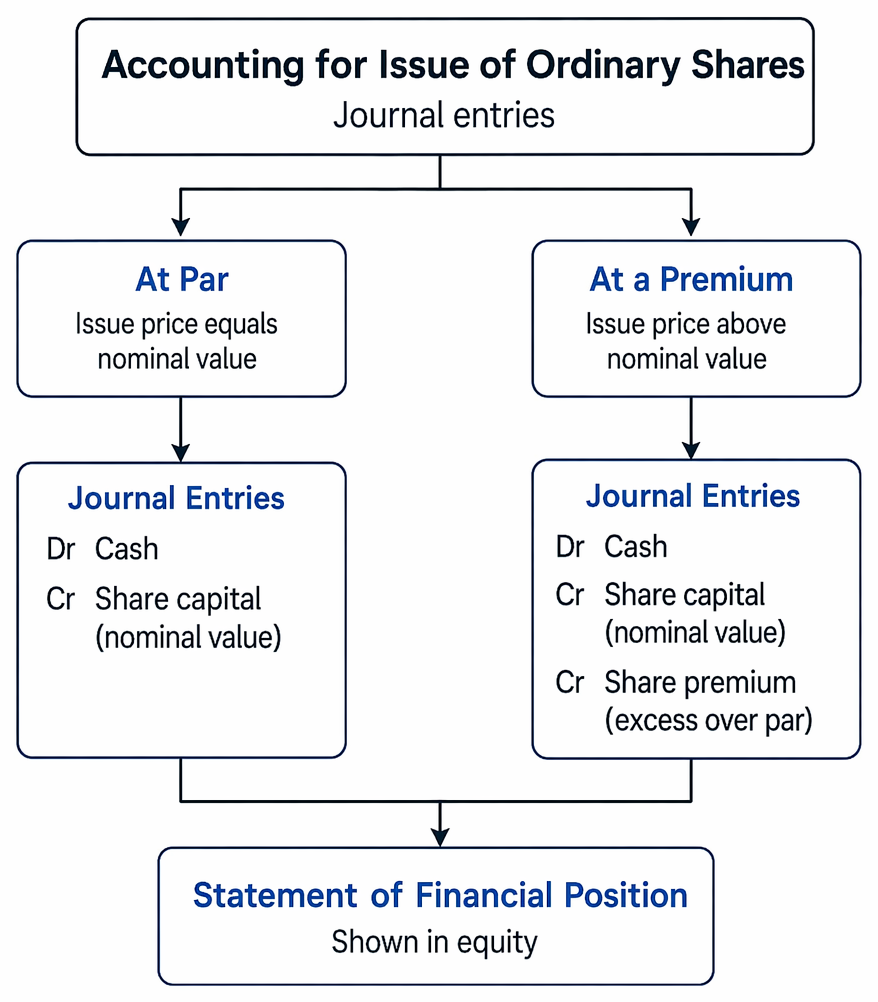

Ordinary share issues at nominal value or premium generate entries to cash, share capital, and, where applicable, share premium.

Ordinary shares

On issue for cash at par:

- Dr Cash

- Cr Share capital (nominal value)

If issued above par (at a premium):

- Dr Cash

- Cr Share capital (nominal value)

- Cr Share premium (excess over par)

The balances appear in equity on the statement of financial position.

Worked Example 1.2

Cranston Ltd issues 50,000 ordinary shares of $1 each at an issue price of $1.50. What are the entries?

Answer:

Dr Cash $75,000 Cr Share capital $50,000 Cr Share premium $25,000 The company raises $75,000, of which $50,000 is share capital and $25,000 is share premium.

Preference shares

Issue of irredeemable preference shares:

- Dr Cash

- Cr Preference share capital

If redeemable:

- Dr Cash

- Cr Financial liability

Preference shares classified as liabilities will result in dividends being treated as an expense (finance cost), reducing profit before tax. If they are irredeemable and the company is not obliged to make payments, dividends are distributions from profit, not expenses.

Retained earnings

Each year:

- Net profit after tax increases retained earnings

- Dividends declared reduce retained earnings

No cash movement occurs when profits are retained, but equity builds up as reserves.

Worked Example 1.3

Furness plc has net profit after tax of $120,000. The directors declare an ordinary dividend of $35,000 and a preference dividend of $10,000. What is the movement in retained earnings?

Answer:

Increase in retained earnings: $120,000 – $35,000 – $10,000 = $75,000.

LEGAL AND PRACTICAL IMPLICATIONS

- Ordinary share issues typically dilute existing shareholders' ownership.

- Preference shares appeal to investors seeking regular income with lower risk but less control.

- Retaining earnings reduces dividend payments but can provide funds for future growth.

- Only distributable profits can be paid out as dividends; capital or share premium cannot be distributed.

Revision Tip: Review the classification criteria for preference shares in practice questions. Focus on whether the company is obliged to pay cash (debt) or not (equity).

Summary

Companies fund their activities by issuing ordinary shares (equity), preference shares (sometimes equity, sometimes debt), and retaining earnings. Each has implications for ownership, control, risk, and how items appear in the statement of financial position and income statement. Recognising these differences is essential for exam success.

Key Point Checklist

This article has covered the following key knowledge points:

- The features and rights of ordinary shares as equity capital

- The main types of preference shares and their characteristics

- How to distinguish redeemable from irredeemable preference shares

- The accounting treatment for ordinary and preference shares in the statement of financial position

- The nature and role of retained earnings as a source of internal finance

Key Terms and Concepts

- Ordinary shares

- Preference shares

- Redeemable preference shares

- Irredeemable preference shares

- Retained earnings