Learning Outcomes

After reading this article, you will be able to explain why businesses must match the source of finance to the asset's expected life, distinguish between short-term and long-term funding, select suitable finance for various assets, and assess the consequences of poor matching in the context of the ACCA exam.

ACCA Foundations in Financial Management (FFM) Syllabus

For ACCA Foundations in Financial Management (FFM), you are required to understand how businesses match finance to their asset needs and useful lives. In particular, you should focus on:

- The distinction between short-term and long-term finance

- The concept of matching the duration of financing to the life of assets acquired

- Appropriate sources of finance for different types of assets (current vs non-current)

- Risks of inappropriate finance matching (liquidity, refinancing risk, cost)

- Typical examples of asset-finance mismatches and the potential impact on a business

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

A business wants to purchase delivery vans to be used over five years. Which financing method is most appropriate?

- a) Overdraft

- b) Five-year term loan

- c) Trade credit

- d) Retained earnings

-

What is the main risk of using a short-term overdraft for acquiring long-term manufacturing equipment?

-

State one reason why inventory is commonly financed through trade credit rather than a bank loan.

-

True or false? Using a twenty-year mortgage to buy seasonal inventory is an example of poor finance matching.

Introduction

Businesses require finance to acquire assets, both for short-term operations and long-term growth. However, choosing the correct source and term of finance is as important as the finance itself. If the finance term does not match the asset's useful life, the business may face liquidity issues, repayment challenges, or even operational disruption. In this article, you will learn how to select the right type and length of funding for different assets, a critical skill for the ACCA exam.

Test Tip: When revising Matching finance to asset life and needs, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

MATCHING FINANCE TO ASSET LIFE

Asset Types and Funding Needs

Every asset used by a business has a different expected life. These are broadly split into:

- Non-current assets (long-term): Machinery, vehicles, buildings, computers. Used for several years.

- Current assets (short-term): Inventory, receivables, cash. Used or turned over within a year.

The main principle: Finance with a similar timescale to the asset's life.

Key Term: matching principle

The practice of aligning the term of finance with the useful life of the asset it is funding. This ensures repayments end as the asset's benefits are exhausted.

Sources of Finance: Short vs Long Term

Short-term Finance

Used for assets that turn over quickly, such as stock or ongoing expenses.

Key Term: short-term finance

Financing sources due for repayment within one year, typically used to fund working capital needs.

Common types:

- Bank overdraft

- Trade credit from suppliers

- Short-term lines of credit

Long-term Finance

Used for assets with a longer expected benefit, such as equipment or premises.

Key Term: long-term finance

Financing sources repayable over periods longer than one year, suitable for funding long-term investment in non-current assets.

Typical sources:

- Term loans (3–10 years)

- Mortgages

- Hire purchase/leasing

- Issuing shares (equity)

- Retained profits

HOW TO MATCH FINANCE TO NEEDS

General Rules

- Non-current assets (long-term): Use long-term finance.

- Current assets (short-term): Use short-term finance.

This matching provides stability and reduces risk. For example, a five-year machine should be financed by a five-year loan, not an overdraft repayable on demand.

Key Term: working capital

The capital needed to fund the day-to-day operations of a business, covering current assets like inventory and receivables.

Consequences of Poor Matching

Financing long-term assets with short-term finance creates several risks:

- Lenders may call in funds before the asset generates enough cash profit.

- Frequent refinancing may be needed, risking liquidity problems.

- Interest rates on short-term funds may fluctuate. Oppositely, using long-term finance for short-term needs increases total borrowing cost and ties up resources unnecessarily.

Worked Example 1.1

A bakery needs new ovens expected to last eight years. Management considers a one-year bank overdraft vs. an eight-year bank loan.

Which is the better match and why?

Answer:

The eight-year term loan is the correct match for ovens with an eight-year life. This aligns repayments to the period the ovens generate profit, reducing refinancing and liquidity risk. The overdraft may be withdrawn or renewed at higher rates, leading to operational disruption.

Worked Example 1.2

A retailer purchases seasonal inventory using a 15-year mortgage. What is the main problem with this approach?

Answer:

Seasonal inventory turns into sales within months. Using a 15-year loan greatly overextends financing, locking the business into long-term repayments for goods sold long ago. This is inefficient and expensive.

TYPICAL MATCHES FOR COMMON ASSETS

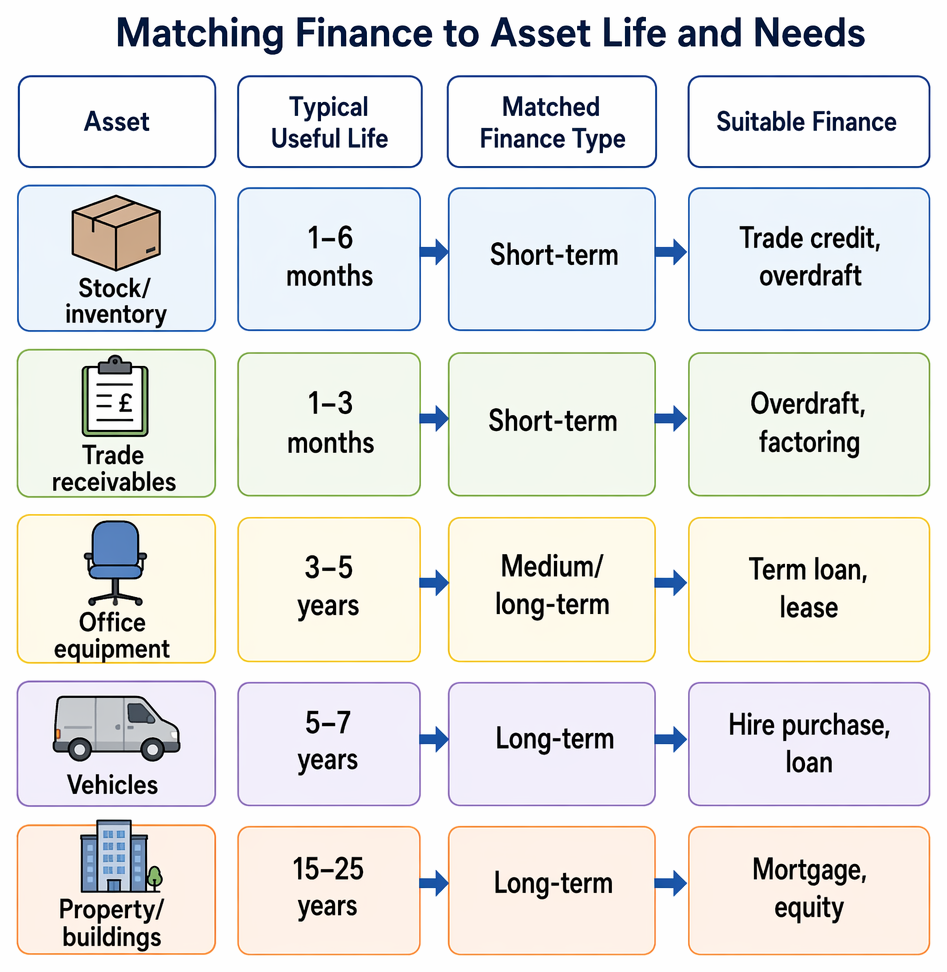

Mismatched financing terms create refinancing and liquidity exposure for long-term assets, and unnecessary cost and reduced flexibility for short-term needs.

| Asset | Typical Useful Life | Matched Finance Type | Suitable Finance |

|---|---|---|---|

| Stock/inventory | 1–6 months | Short-term | Trade credit, overdraft |

| Trade receivables | 1–3 months | Short-term | Overdraft, factoring |

| Office equipment | 3–5 years | Medium/long-term | Term loan, lease |

| Vehicles | 5–7 years | Long-term | Hire purchase, loan |

| Property/buildings | 15–25 years | Long-term | Mortgage, equity |

Exam Warning: Examiners often ask about consequences of mis-matching finance and asset life. Always relate the financing period to the asset’s useful life.

BENEFITS OF EFFECTIVE MATCHING

Appropriate matching of finance and asset life offers several benefits:

- Lower risk of cash shortfalls

- Repayments end when the asset no longer generates returns

- Easier financial planning and budgeting

- Avoids excessive total interest costs

Summary

Choosing finance for asset acquisition is not just about obtaining funds, but ensuring the finance's term matches the asset’s expected use. This reduces risk, supports business stability, and is a key exam point.

Key Point Checklist

This article has covered the following key knowledge points:

- The importance of matching the term of finance to the useful life of assets

- The distinction between short-term and long-term finance

- Common sources of finance for different business assets

- Risks and problems caused by poor matching of finance and asset life

- Recognition of standard asset-finance combinations for ACCA exam scenarios

Key Terms and Concepts

- matching principle

- short-term finance

- long-term finance

- working capital