Learning Outcomes

By the end of this article, you will be able to explain the distinction between asset and expense items, describe the asset expenditure budgeting process, and evaluate investments using the payback period and accounting rate of return (ARR) methods. You will be able to apply these methods to real scenarios, interpret their results, and discuss their advantages and limitations for decision-making in ACCA exam contexts.

ACCA Management Accounting (MA) Syllabus

For ACCA Management Accounting (MA), you are required to understand how businesses plan, control, and appraise asset expenditure. This article focuses on:

Investment appraisal items are classified by future occurrence, incrementality, project dependence, and cash basis to determine relevance.

- Defining and distinguishing between asset and expense items

- Outlining the stages of asset expenditure budgeting and investment appraisal

- Explaining and applying the payback period method (including discounted payback)

- Explaining and applying the accounting rate of return (ARR) method

- Identifying relevant cash flows for investment appraisal

- Interpreting payback and ARR outcomes for investment decisions

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the difference between asset and expense items in a business context?

- How is the payback period calculated, and what decision rule is typically used?

- Define accounting rate of return (ARR) and explain how it is different from payback period.

- Which costs are considered relevant when evaluating future cash flows for investment appraisal?

Introduction

Asset budgeting and investment appraisal are key processes that help organisations plan long-term investments in non-current assets. These decisions involve significant capital and have lasting financial impact. Two common methods for evaluating such investments—the payback period and accounting rate of return (ARR)—provide simple metrics to rank and select projects.

Both methods require careful identification of relevant cash flows, as well as an understanding of the broader budgeting process. This article will guide you through essential definitions, calculation methods, and the interpretation of results, ensuring you are equipped for ACCA exam questions on these topics.

Distinguishing Asset and Expense Items

Investments in business either create non-current assets or are recognised as expenses. The distinction determines both their accounting treatment and their inclusion in investment appraisal.

Key Term: Asset item

Expenditure on non-current assets expected to benefit the business over several periods, such as machinery, vehicles, or property. Key Term: Expense item

Expenditure on items consumed within the current period, including day-to-day running costs like wages, utility bills, and repairs.

Asset purchases are shown as non-current assets in the statement of financial position and depreciated over their useful lives. Expenses are charged directly to profit or loss in the period incurred.

The Asset Expenditure Budgeting Process

Businesses use asset expenditure budgets to plan, authorise, and control large capital investments over several years. This process involves multiple decision points:

- Forecasting needs—Identify necessary asset replacements, expansions, and new investments.

- Project identification—Select potential projects that align with business strategy.

- Appraisal—Evaluate the financial and non-financial merits of each project.

- Selection and approval—Choose projects based on appraisal results and strategic priorities.

- Implementation—Purchase assets and monitor progress against the plan.

- Review and control—Compare actual against budgeted expenditure and investigate variances.

Good investment decisions rely on reliable forecasts and objective appraisals.

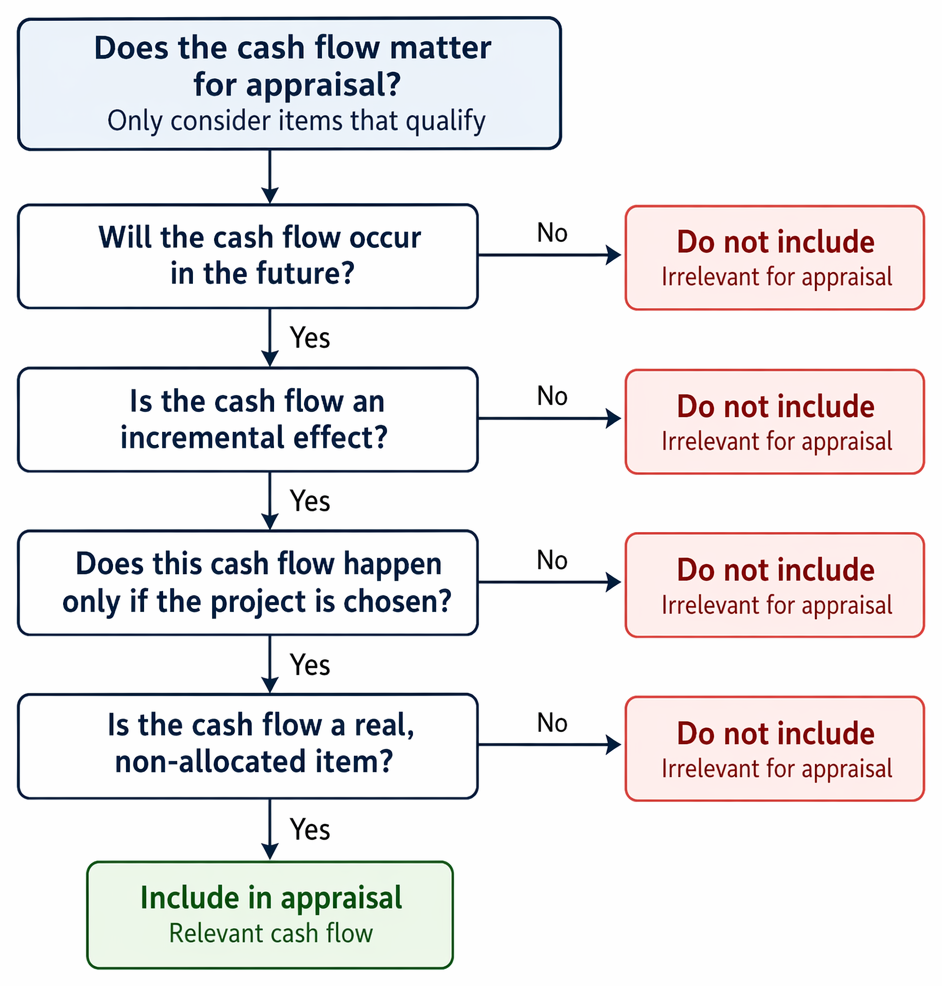

Relevant Cash Flows for Investment Appraisal

Only certain future costs and benefits should be included in investment appraisal calculations.

Key Term: Relevant cash flow

A future, incremental cash inflow or outflow that will occur only if the project goes ahead.

Common examples of relevant cash flows:

- Initial investment outlay (purchase price of an asset)

- Additional operating cash inflows (e.g. increased sales)

- Additional operating cash outflows (e.g. higher maintenance)

- Incremental costs directly resulting from the decision (supervisor costs, extra insurance, etc.)

- Cash disposal proceeds of an asset (e.g. estimated scrap or sale value)

Non-relevant items (not included):

- Sunk costs (past expenditures)

- Non-cash items (depreciation, notional charges)

- Allocated overheads not directly increased by the investment

Worked Example 1.1

A company must decide whether to buy a new machine for $120,000. It will generate extra sales revenues of $60,000 per year for three years, incur additional running costs of $15,000 per year, and require a one-off installation cost of $8,000. A consultant's $3,000 feasibility study has already been paid. The expected scrap value after three years is $10,000.

Question: What are the relevant cash flows for investment appraisal?

Answer:

The relevant cash flows include:

- Initial outlay: $120,000 + $8,000 (installation) = $128,000 outflow at time 0

- Operating inflows: $60,000 per year (years 1–3)

- Operating outflows: $15,000 per year (years 1–3)

- Scrap value: $10,000 inflow at end of year 3 The consultant’s fee is a sunk cost and not included.

The Payback Period Method

The payback period is a simple measure of how quickly an investment returns its original cost.

Key Term: Payback period

The length of time required for an investment’s net cash inflows to equal its initial outlay.

To calculate:

- List cumulative net cash flows each period.

- Find when cumulative inflows equal the investment cost.

- If payback occurs part-way through a year, prorate accordingly.

Projects with shorter payback periods are generally preferred, especially when rapid liquidity is important.

Worked Example 1.2

Project Alpha has the following expected cash flows:

| Year | Cash Flow ($) |

|---|---|

| 0 | (50,000) |

| 1 | 15,000 |

| 2 | 18,000 |

| 3 | 17,000 |

| 4 | 14,000 |

Question: Calculate the payback period.

Answer:

Cumulative inflows:

- End of Year 1: $15,000

- End of Year 2: $33,000 ($15,000 + $18,000)

- End of Year 3: $50,000 ($33,000 + $17,000) Payback occurs at exactly 3 years.

Worked Example 1.3

A project costs $40,000 and produces annual cash inflows of $12,000 for 5 years.

Question: What is the payback period?

Answer:

$40,000 / $12,000 = 3.33 years (3 years and 4 months).Exam Warning: The payback method ignores all cash flows occurring after payback. Selecting projects solely by payback may result in choosing investments that are not profitable overall.

Discounted Payback Period

The discounted payback period extends the payback method by including the time value of money. Each year’s cash flows are discounted before calculating cumulative totals.

Key Term: Discounted payback period

The time taken for cumulative discounted cash inflows to recover the initial investment.

Discounted payback always results in a longer period than traditional payback.

Worked Example 1.4

Project Beta requires a $30,000 outlay and generates $10,000 per year for 4 years. The discount rate is 10%.

Question: What is the discounted payback period?

| Year | Cash Flow | Discount Factor (10%) | Discounted CF | Cumulative |

|---|---|---|---|---|

| 0 | (30,000) | 1.000 | (30,000) | (30,000) |

| 1 | 10,000 | 0.909 | 9,090 | (20,910) |

| 2 | 10,000 | 0.826 | 8,260 | (12,650) |

| 3 | 10,000 | 0.751 | 7,510 | (5,140) |

| 4 | 10,000 | 0.683 | 6,830 | 1,690 |

Answer:

Payback occurs during year 4. Amount still to recover at end of year 3: $5,140. Discounted cash flow in year 4: $6,830. Fraction required: $5,140 / $6,830 ≈ 0.75 years (9 months). Discounted payback period is 3.75 years.

Accounting Rate of Return (ARR) Method

ARR is another measure used to compare investment projects. Unlike payback, it is based on accounting profit as a percentage of investment.

Key Term: Accounting rate of return (ARR)

The average annual accounting profit from a project divided by its average or initial investment cost, usually expressed as a percentage.

Calculation steps:

- Estimate average annual profit (after depreciation, but before interest and tax, unless stated).

- Divide by the average (or initial) investment.

- Multiply by 100 to get a percentage.

ARR Decision Rule: Accept projects where ARR exceeds the required minimum rate (the “hurdle rate”).

Worked Example 1.5

A business invests $80,000 in equipment with a 4-year life and nil residual value. Expected annual profits after depreciation are: Year 1 – $7,000; Year 2 – $8,500; Year 3 – $9,500; Year 4 – $7,500.

Question: Calculate the ARR using the average investment approach.

Answer:

- Average profit = (7,000 + 8,500 + 9,500 + 7,500) / 4 = $8,125

- Average investment = ($80,000 + $0) / 2 = $40,000

- ARR = ($8,125 / $40,000) × 100% = 20.3%

Exam Warning (ARR)

ARR uses accounting profit rather than cash flows, and the treatment of depreciation can vary. Always follow the exam’s instructions for profit calculations.

Comparison: Payback, Discounted Payback, and ARR

| Criteria | Payback Period | Discounted Payback | ARR |

|---|---|---|---|

| Measure based on | Cash flows | Discounted cash flows | Accounting profits |

| Includes time value? | No | Yes | No |

| Focus on | Liquidity/risk | Liquidity & time value | Profitability/return |

| Simplicity | Very simple | Requires discounting | Simple |

| Main drawback | Ignores later flows | Ignores post-payback flows | Ignores cash/timing |

Revision Tip: In exam calculations, clearly show step-by-step working, especially for partial-year payback and the ARR formula.

Advantages and Limitations

Payback Period Advantages:

- Simple to compute and explain

- Highlights liquidity and quick recovery of funds

- Useful where investment risk or technology changes rapidly

Payback Period Limitations:

- Ignores cash flows after payback point

- Does not consider overall profitability

- Ignores time value of money (unless using discounted version)

ARR Advantages:

- Easy to relate to familiar profit measures

- Uses financial statements’ data

- Can aid in comparison with target returns

ARR Limitations:

- Based on profits, not actual cash flows

- Dependent on accounting policies (e.g. depreciation)

- Ignores timing of income

- No consideration of time value of money

Summary

Effective investment decisions support long-term goals and financial security. The payback period method measures how quickly an investment is repaid, while ARR gauges profitability as a percentage return on capital. Both methods are straightforward and rely on simple data, but they also have significant limitations. Understanding their use, calculation, and drawbacks is essential for ACCA exam success and for professional practice in budgeting and capital appraisal.

Key Point Checklist

This article has covered the following key knowledge points:

- Distinguish asset from expense items in investment appraisal

- Summarise the asset expenditure budgeting process stages

- Define and calculate relevant cash flows for project appraisal

- Calculate and interpret the payback period and discounted payback

- Define and compute the accounting rate of return (ARR)

- Recognise the advantages and limitations of payback and ARR methods

Key Terms and Concepts

- Asset item

- Expense item

- Relevant cash flow

- Payback period

- Discounted payback period

- Accounting rate of return (ARR)