Learning Outcomes

After reading this article, you should be able to explain the objective and procedures of impairment reviews under IAS 36, apply the key models and recognition rules for investment property under IAS 40, and account for transfers between PPE, investment property, and inventory. You will be able to distinguish impairment from revaluation, select and justify measurement models for investment property, and identify how to handle changes in use.

ACCA Strategic Business Reporting (SBR) Syllabus

For ACCA Strategic Business Reporting (SBR), you are required to understand both the principles and detailed application of impairment of assets and investment property accounting. This article addresses the following syllabus points:

- Evaluate and apply the recognition, derecognition and measurement of non-current assets including impairments and revaluations

- Evaluate and apply the accounting treatment of investment properties including classification, recognition, measurement and change of use

- Distinguish between the cost and fair value models for investment property

- Apply the impairment review process to individual assets and cash-generating units

- Assess the impact of transfers between investment property, PPE and inventory

- Explain relevant disclosures for impaired assets and investment property

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What triggers a mandatory impairment review under IAS 36?

- Which model under IAS 40 requires fair value gains and losses to be recognised in profit or loss?

- When can a property be transferred from PPE to investment property?

- Explain how to measure an asset initially upon transfer from inventory to investment property held under the fair value model.

- Which costs are included in determining the recoverable amount under IAS 36?

Introduction

IAS 36 Impairment of Assets ensures that non-current assets are not carried above their recoverable amount, protecting users from overstated values. IAS 40 Investment Property sets out how to account for properties held for rental income or capital appreciation, allowing a choice of measurement models and prescribing rules for classification and transfer. Both standards require sound judgement on asset use and value, with direct consequences for both profits and assets in financial statements.

Key Term: impairment

The reduction in an asset’s carrying amount to its recoverable amount when its carrying amount exceeds what is recoverable through use or sale. Key Term: recoverable amount

The higher of an asset’s fair value less costs of disposal and its value in use.

Impairment of Assets (IAS 36)

implies an entity must review at each reporting date whether indicators of impairment exist. For certain assets (goodwill and intangible assets with indefinite useful lives), an annual impairment test is required regardless of indicators. Other assets are reviewed for impairment only when indicators exist.

Indicators of impairment include:

- Significant decline in market value

- Adverse changes in technology, market or legal environment

- Internal evidence of obsolescence or physical damage

- Economic underperformance of the asset

Calculation of Impairment Loss

Impairment occurs if an asset’s carrying amount exceeds its recoverable amount.

Key Term: value in use

The present value of future cash flows expected from an asset, discounted at a suitable rate. Key Term: fair value less costs of disposal

The price that would be received from selling an asset, less the direct costs of disposal, in an orderly transaction.

The recoverable amount is the higher of:

- Fair value less costs of disposal

- Value in use

The impairment loss is the carrying amount less the recoverable amount. This is recognised immediately in profit or loss unless the asset was previously revalued through other comprehensive income (such as under the revaluation model), in which case the loss is offset against revaluation surplus to the extent available.

Exam Warning: Where an item was previously revalued, impairment losses must first reduce the revaluation surplus for that specific asset before affecting profit or loss.

Cash-Generating Units

If an asset does not generate largely independent cash flows, impairment must be assessed at the cash-generating unit (CGU) level.

Key Term: cash-generating unit (CGU)

The smallest group of assets generating cash inflows from continuing use that are largely independent from other assets.

Goodwill is always tested for impairment within the CGU to which it belongs. Any impairment loss in a CGU is allocated first to goodwill, then to other assets pro rata by carrying amount.

Worked Example 1.1

An entity has equipment with a carrying amount of $250,000. Due to market changes, the expected cash flows (discounted at 8%) total $200,000, and the asset could be sold for $180,000 after $10,000 of selling costs.

What is the impairment loss, if any?

Answer:

The recoverable amount is the higher of:

- Value in use: $200,000

- Fair value less costs of disposal: $180,000 - $10,000 = $170,000 Therefore, recoverable amount = $200,000 Impairment loss = $250,000 - $200,000 = $50,000

Reversal of Impairment

If the recoverable amount of an asset increases in a future period, the impairment loss may be reversed (except for goodwill). The increase is recognised in profit or loss and cannot increase the asset’s carrying amount above what it would have been had no impairment been recognised.

Investment Property (IAS 40)

IAS 40 defines investment property as property held (by owner or lessee under a right-of-use asset) to earn rentals, for capital appreciation, or both. It does not include owner-occupied property (IAS 16), property held for sale (IAS 2), or property under construction for third parties (IFRS 15).

Recoverable amount assessment determines whether an impairment loss is recognised and whether any loss first reduces revaluation surplus.

Key Term: investment property

Land or building (or part) held to earn rental income, for capital appreciation, or both, rather than for use in production or supply of goods or administration.

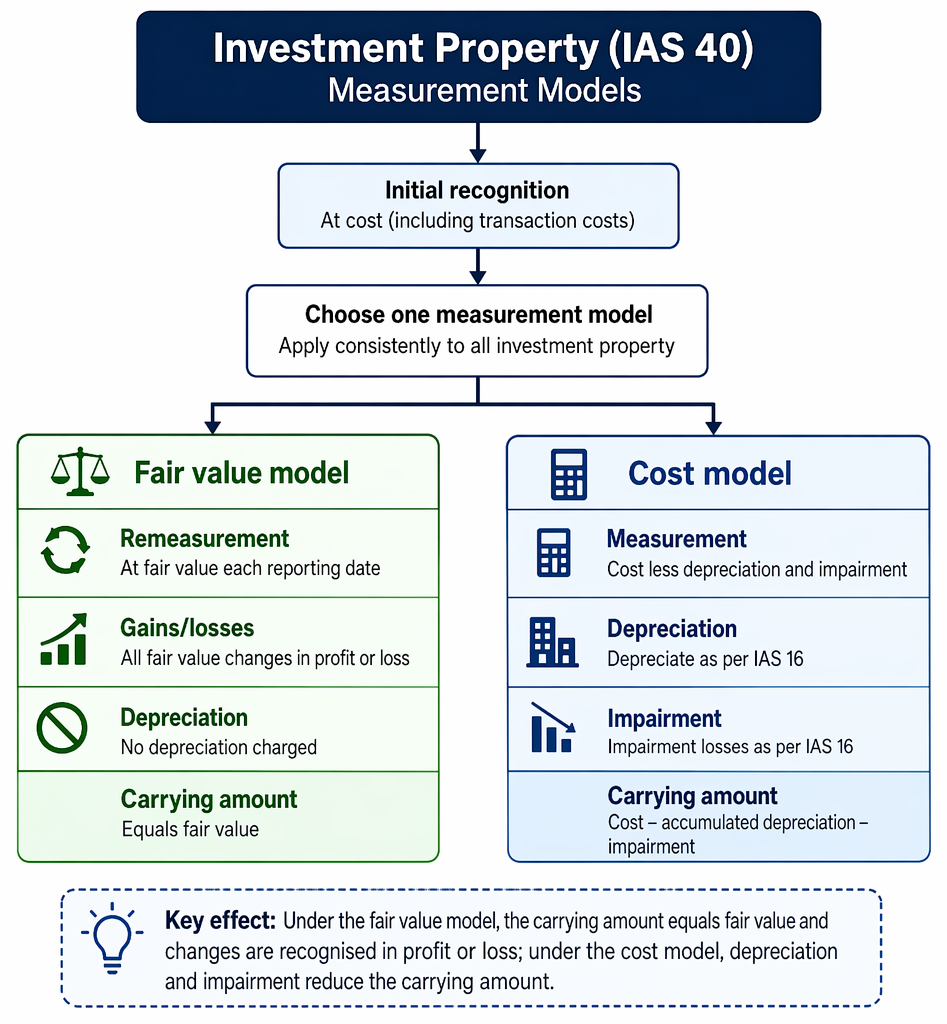

Measurement Models

After initial recognition at cost (including transaction costs), an entity must choose either the fair value model or the cost model, applying the choice consistently to all investment property.

- Fair value model: Investment property is remeasured at fair value at each reporting date. All fair value gains or losses are recognised in profit or loss. No depreciation is charged.

- Cost model: The property is carried at cost less accumulated depreciation and impairment as per IAS 16.

Key Term: fair value model (IAS 40)

A measurement model under which all investment properties are remeasured at fair value at each reporting date, with changes recognised in profit or loss. Key Term: cost model (IAS 40)

A measurement model under which investment properties are carried at cost less depreciation and impairment.

Worked Example 1.2

An entity owns an office building acquired for $600,000. By year-end, its fair value is estimated at $680,000. The entity applies the fair value model.

How is the property accounted for at year-end?

Answer:

Carrying amount is updated to $680,000. The $80,000 gain is recognised in profit or loss, and no depreciation is charged.

Transfers of Property

Transfers to or from investment property can only occur when there is a change in use, as evidenced by:

- Commencement of owner occupation or vice versa

- Commencement of development with a view to sale (inventory)

- Ending owner occupation (now earns rentals or held for appreciation)

On transfer:

- From PPE to investment property (fair value model): Measure at fair value at transfer date. Any difference from carrying amount is treated as a revaluation under IAS 16.

- From inventory to investment property (fair value model): Measure at fair value at transfer. Any difference is recognised in profit or loss.

Worked Example 1.3

A company transfers a warehouse previously held as inventory (cost $200,000, carrying amount $190,000) to investment property, adopting the fair value model. Fair value at transfer is $210,000.

What is the accounting treatment?

Answer:

The asset is remeasured to $210,000 on transfer. The difference ($210,000 - $190,000 = $20,000) is recognised as a gain in profit or loss.

Transfers Between Models

- If a property ceases to meet the definition of investment property (e.g., becomes owner-occupied), normal rules for PPE apply from transfer date.

- If an investment property carried at fair value is transferred to owner-occupied property, the fair value at transfer becomes its deemed cost under IAS 16.

Disclosure Requirements

Entities must disclose which measurement model is applied, the amount of rental income and direct operating expenses, reconciliation of carrying amount at start and end of period, and, for properties at cost, their fair value.

Exam Warning: If a property is partially owner-occupied and partially held for investment, only the investment-portion may be classified under IAS 40. Significant judgement is required in mixed-use cases.

Summary

IAS 36 prohibits carrying non-current assets above the amount recoverable from use or sale. Impairment reviews are based on the higher of fair value less costs of disposal and value in use. Investment property is classified by intention and can be measured either at fair value through profit or loss or at cost less depreciation, applied consistently. Transfers between property categories require a validated change in use and have specific rules for measurement at the date of transfer.

Key Point Checklist

This article has covered the following key knowledge points:

- Distinguish between indicators and triggers for separate asset impairment reviews under IAS 36

- Calculate and allocate impairment losses and reversals, including at CGU level

- Select and apply either the cost or fair value model for investment property under IAS 40

- Recognise measurement and disclosure consequences of model selection

- Account for changes in use and transfers between PPE, investment property, and inventory

Key Terms and Concepts

- impairment

- recoverable amount

- value in use

- fair value less costs of disposal

- cash-generating unit (CGU)

- investment property

- fair value model (IAS 40)

- cost model (IAS 40)