Learning Outcomes

After reading this article, you will be able to identify impairment indicators under IAS 36, calculate and allocate impairment losses to goodwill and other assets within a cash-generating unit, and explain the measurement and disclosure rules for investment properties under IAS 40. You will also understand annual impairment testing requirements for goodwill, and how to transition between owner-occupied and investment property, ensuring correct presentation in SBR exam scenarios.

ACCA Strategic Business Reporting (SBR) Syllabus

For ACCA Strategic Business Reporting (SBR), you are required to understand the application of impairment reviews for non-current assets, with a particular focus on goodwill emerging from business combinations, as well as the recognition and measurement criteria for investment property. In your revision, pay attention to:

- The recognition and measurement principles for non-current assets, including impairment, reversals, and revaluations.

- The method to test and allocate impairment losses, especially for goodwill and cash-generating units.

- The annual impairment review requirement for non-amortised intangibles and goodwill.

- Classification and measurement of investment property under IAS 40, including the cost and fair value models.

- Procedures for transfers between investment property and other asset classes.

- Disclosure requirements for impairment and investment property.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the recoverable amount of an asset, and when should it be compared to carrying amount?

- True or false? Goodwill is tested for impairment only when indicators exist.

- When an impairment loss arises for a cash-generating unit, in what order should it be allocated to assets?

- What is the main difference between the cost model and the fair value model in IAS 40?

- Give an example of an internal indicator and an external indicator of impairment under IAS 36.

Introduction

IAS 36 and IAS 40 are core standards tested in ACCA SBR, focusing on the correct valuation and reporting of non-current assets. IAS 36 requires entities to review assets for impairment and allocate any loss between goodwill and other assets, generally at annual intervals for certain assets. IAS 40 distinguishes investment property from other non-current assets, permits a choice of measurement model, and regulates transfers between property classes.

Understanding how to identify, measure, and allocate impairment losses, including those affecting goodwill, is essential for preparing group financial statements. Comprehension of IAS 40 is equally important for entities holding property for investment purposes.

Test Tip: When revising Goodwill impairment and allocation, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Impairment of Assets – IAS 36

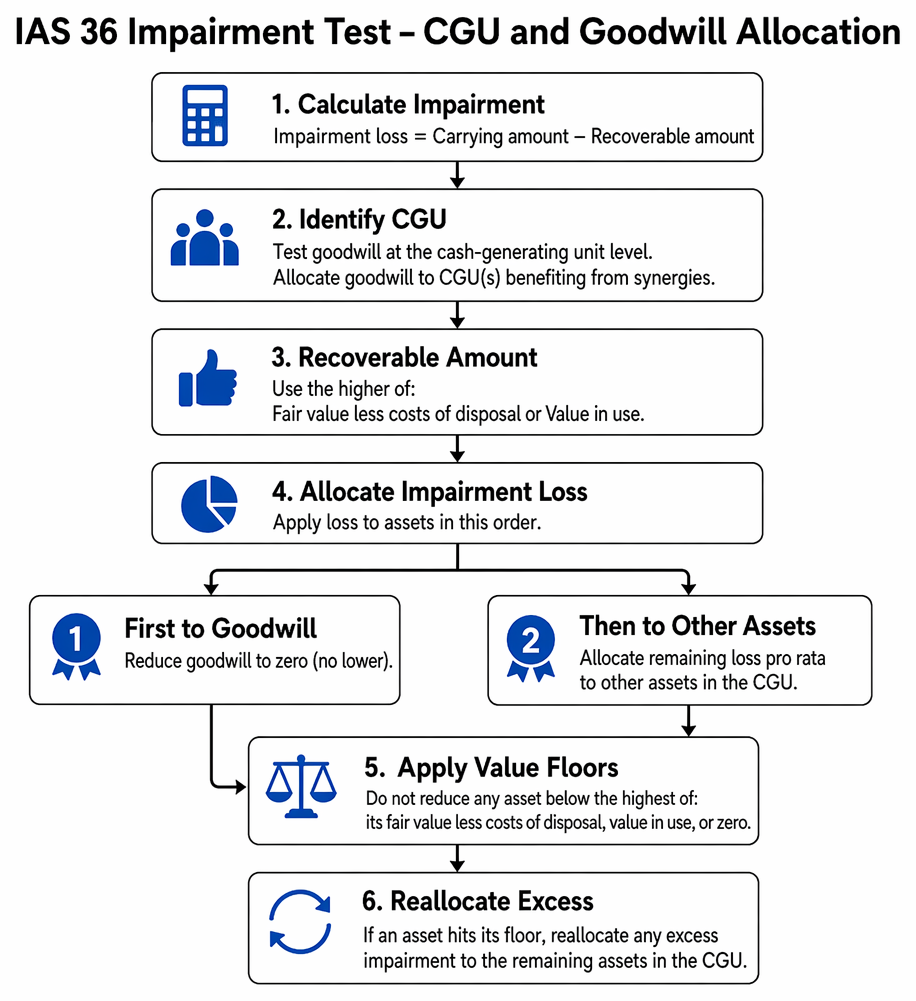

IAS 36 requires entities to ensure that assets are not carried at more than their recoverable amount. An annual impairment review is mandatory for goodwill and non-amortised intangibles, while other assets are tested when indicators suggest possible impairment.

IAS 36 recoverable amount equals the higher of fair value less costs of disposal and value in use.

Indicators of Impairment

IAS 36 distinguishes between external and internal indicators. Common examples include:

- Significant fall in market value (external)

- Adverse changes in market or technology (external)

- Physical damage or obsolescence (internal)

- Asset underperforming compared to previous expectations (internal)

Key Term: Impairment loss

The amount by which the carrying amount of an asset or cash-generating unit exceeds its recoverable amount.

Recoverable Amount

Impairment involves comparing the asset’s carrying amount to its recoverable amount.

Key Term: Recoverable amount

The higher of an asset’s fair value less costs of disposal and its value in use.

Fair value less costs of disposal is the price obtainable from selling the asset in an orderly transaction, less direct outgoing costs.

Value in use is the present value of the estimated future cash flows expected from the asset’s continued use and eventual disposal. The calculations must use reasonable and supportable assumptions and a suitable discount rate.

Cash-Generating Units and Goodwill

Goodwill acquired in a business combination does not generate cash flows independently and is therefore tested for impairment as part of a cash-generating unit (CGU).

Key Term: Cash-generating unit (CGU)

The smallest identifiable group of assets that generates cash inflows largely independent of other assets or groups.

Goodwill is only allocated to CGUs or groups of CGUs that are expected to benefit from the synergies of the combination.

Worked Example 1.1

Scenario: Aspen Ltd acquires Beech Ltd and records $12m of goodwill. After one year, Aspen identifies the following information for Beech’s CGU:

- Carrying amount, including goodwill: $48m

- Recoverable amount: $44m

- The carrying amount of assets: Goodwill $12m, PPE $16m, Inventory $12m, Customer list $8m

Question: How is the impairment loss allocated?

Answer:

Total impairment: $4m ($48m – $44m).

- First, allocate to goodwill: $4m (goodwill cannot fall below zero).

- Remaining: $0m. No further allocation needed.

- Post-impairment carrying amounts: Goodwill $8m, other assets unchanged.

Allocation of Impairment Losses

Impairment for a CGU is allocated first to goodwill, then pro rata to other assets, with each asset not reduced below the highest of its fair value less costs of disposal, value in use, or zero.

Key Term: Goodwill impairment

The reduction of the carrying amount of purchased goodwill to its recoverable amount, with losses recognised in profit or loss. Key Term: Value in use

The present value of the future cash flows expected from an asset’s use and disposal.

Worked Example 1.2

Scenario: A CGU comprises assets: Goodwill $5m, Land $12m (recoverable amount $12m), Plant $9m, Trademark $4m. The CGU’s recoverable amount is $21m. The carrying amount of the CGU (including goodwill) is $30m.

Question: Calculate the impairment allocation.

Answer:

Impairment loss: $9m ($30m – $21m).

Apply $5m to goodwill (reduced to zero).

Remaining $4m allocated pro rata to Plant and Trademark, observing asset floors:

- Land is at recoverable amount. No allocation.

- Plant ($9m): ($9m/$13m) × $4m = $2.77m (rounded).

- Trademark ($4m): ($4m/$13m) × $4m = $1.23m (rounded).

- Post-impairment: Plant $6.23m, Trademark $2.77m.

Allocation to Assets with Value Floors

When any individual asset's fair value less costs of disposal or value in use is higher than remaining carrying amount after initial allocation, excess impairment must be reallocated to other assets in the CGU.

Exam Warning: In group scenarios, only the portion of goodwill recognised in consolidated accounts is impaired when applying the proportionate share method for non-controlling interest. Never allocate impairment loss to assets below their recoverable amount or zero.

Reversal of Impairment Losses

An entity must assess at each reporting date whether a previously recognised impairment loss (except those relating to goodwill) may have decreased. Any reversal is immediately recognised in profit or loss and cannot increase the asset’s carrying amount above what it would have been if no impairment had occurred. Goodwill impairment losses cannot be reversed.

Investment Property – IAS 40

IAS 40 applies to property held to earn rent or for capital appreciation, not for use in production or sale in the ordinary course of business.

Key Term: Investment property

Property (land or building, or part) held to earn rentals or for capital appreciation or both, rather than for use in production, or for sale in the ordinary course of business.

Recognition and Initial Measurement

Investment property is recognised at cost, including transaction costs, on initial recognition.

Measurement Models

After recognition, IAS 40 allows a choice between:

- Cost model: Carry at cost less accumulated depreciation and impairment (apply IAS 16 rules, but no revaluation permitted).

- Fair value model: Carry at fair value each reporting date. Changes in fair value are recognised in profit or loss, and no depreciation is charged.

Selection must be applied to all investment properties (except those that cannot be reliably measured at fair value).

Change of Use and Transfers

Property can be transferred into or out of investment property only when change of use occurs. Use fair value at the date of change for measurement.

Worked Example 1.3

Scenario: Maple Ltd changes the use of an office building (previously owner-occupied, carrying amount $950,000) to investment property on 1 March. The property’s fair value at that date is $1,200,000. Company applies the fair value model.

Question: What entries are required at the transfer date?

Answer:

- Carrying amount uplifted to $1,200,000.

- $250,000 ($1,200,000 – $950,000) is a revaluation gain. Recognise this in other comprehensive income (applying IAS 16 up to transfer date).

- Subsequent fair value changes go to profit or loss.

Disclosure Requirements

Entities must disclose their adopted model, amounts recognised in profit or loss attributable to changes in fair values, and a reconciliation between the carrying amounts at the beginning and end of the period.

Summary

IAS 36 ensures assets are not carried above recoverable amount and provides a systematic approach for allocating and reversing impairment losses—with annual mandatory review for goodwill. IAS 40 requires investment properties to be initially measured at cost, then allows a choice of fair value (with gains/losses in profit or loss) or cost models, with restrictions on transfers and clear disclosure rules. Goodwill impairment must be tested at least annually and losses are not reversible.

Key Point Checklist

This article has covered the following key knowledge points:

- Identify when to perform an impairment review under IAS 36.

- Calculate recoverable amount and recognise impairment losses.

- Allocate impairment losses to goodwill and other assets of a CGU.

- Understand the restriction on reversing goodwill impairment losses.

- Distinguish investment property from other asset types per IAS 40.

- Apply the cost and fair value models, and record transfers between asset classes.

- Note required disclosures under IAS 36 and IAS 40.

Key Terms and Concepts

- Impairment loss

- Recoverable amount

- Cash-generating unit (CGU)

- Goodwill impairment

- Value in use

- Investment property