Learning Outcomes

This article explains the fundamental techniques of equity valuation using residual income and asset-based models in an exam-oriented way. It clarifies how asset-based approaches derive a company’s fundamental value from the fair value of assets minus liabilities, and highlights the adjustments required when book values differ from economic values, including treatment of intangibles, off-balance-sheet items, and contingent liabilities. It explains how residual income models build value from current book value plus the present value of future residual income, emphasizing the link between net income, the equity charge, and economic profit. The article details how to calculate and interpret fundamental value estimates, determine whether a stock appears under- or overvalued relative to market price, and recognize the special case where value equals current book value when return on equity matches the required return. It also discusses when each model is most appropriate, typical limitations created by accounting quality and forecasting uncertainty, and classic CFA Level 1 exam traps, such as relying on unadjusted book values, miscomputing the equity charge, or ignoring the implications of residual income that is persistently zero or negative.

CFA Level 1 Syllabus

For the CFA Level 1 exam, you are expected to understand and apply key equity valuation models as part of fundamental analysis, with a focus on the following syllabus points:

- Explaining the rationale for using residual income and asset-based valuation models

- Calculating and interpreting fundamental value estimates using these approaches

- Evaluating when to use each model and recognizing their major limitations

- Comparing fundamental value to market price and analyzing differences for investment decision making

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- Which scenario is most suitable for using an asset-based valuation model?

- True or false? The residual income model requires reliable forecasts of future book value and return on equity.

- Briefly explain what a positive residual income means in fundamental equity valuation.

- Under what key condition will fundamental value equal current book value when using a residual income approach?

Introduction

Equity valuation is the process of estimating the fair value of a company’s shares using various fundamental approaches. Two important models for the CFA exam are the asset-based model and the residual income model. These techniques can complement dividend and free cash flow models, especially when companies lack stable dividends or when comparables are unavailable. Understanding when and how to apply these models is essential for exam success and for practical investment analysis.

Key Term: fundamental value

The estimated fair or economic value of a share or company, based on fundamentals rather than current market price.

Asset-Based Valuation Models

Asset-based models estimate fundamental value by calculating the fair value of a company’s assets minus its liabilities. The resulting value reflects what shareholders would theoretically receive if the company were liquidated today under orderly (not forced sale) conditions.

Key Term: asset-based valuation model

A valuation approach that determines a company’s value as the sum of its assets less its liabilities, based on current fair values.

This approach is especially relevant for firms with:

- Tangible, separable assets (e.g., investment holding companies, property firms)

- Liquidation scenarios or distressed situations

- Minimal intangible assets or off-balance-sheet exposures

Adjustments are required for assets and liabilities not carried at fair value. For example, inventory and property may need to be revalued, and intangible assets or contingent liabilities should be assessed and added/subtracted as needed.

Worked Example 1.1

A holding company owns properties valued at $120 million and listed equities (fair value) of $40 million. The company has long-term debt of $35 million and other liabilities totaling $10 million. What is the asset-based value of equity?

Answer:

Asset-based value = ($120m + $40m) – ($35m + $10m) = $115m.Exam Warning: Do not simply use book values from the balance sheet in an asset-based model. Adjust to fair value wherever possible for both tangible and intangible items.

Revision Tip: Asset-based models are most logical when assets can be measured objectively. Avoid this approach for companies with substantial intangible value or operating assets that are difficult to value individually.

Residual Income Valuation Models

Residual income models estimate fundamental value as current book value plus the present value of future value created above the cost of equity capital. This approach emphasizes economic profit (value above required return), not just accounting earnings.

Key Term: residual income

The income in excess of that required by shareholders, calculated as net income minus an equity charge (cost of equity × beginning book value).

The basic formula for fundamental value () using the residual income model is:

Where:

- = current book value per share

- = residual income in period

- = required return on equity

Key steps:

- Forecast net income and book value for each period.

- Compute required equity charge as cost of equity × opening book value.

- Residual income = net income – equity charge.

Key Term: equity charge

The required return on beginning period equity capital (cost of equity × book value), representing shareholders’ opportunity cost.

A positive residual income means the company is generating economic profit, i.e., management is adding value above investor expectations. If residual income is zero, fundamental value equals book value.

The residual income model is most useful when:

- Companies do not pay dividends or have irregular payout policies

- Free cash flow cannot be reliably estimated

- Book value is meaningful and accounting quality is high

Worked Example 1.2

Suppose XYZ Corp has book value per share of $50. Next year’s forecasted net income is $7. Required return on equity is 10%. What is the residual income for the next year?

Answer:

Equity charge = 10% × $50 = $5. Residual income = $7 – $5 = $2.

If the company’s residual income is expected to remain at $2 indefinitely, what is the present value of residual income using a perpetuity formula?

Answer:

Value of residual income perpetuity = $2 / 0.10 = $20.

Fundamental value = Current book value + Value of residual income Fundamental value = $50 + $20 = $70 per share.

Exam Warning (Residual Income)

The reliability of the residual income model depends on accurate estimates for book value and clean, consistent accounting policies. Material accounting distortions or aggressively capitalized costs can undermine the model’s usefulness.

Revision Tip (Residual Income)

Remember: If forecast ROE equals the cost of equity in all periods, fundamental value equals current book value.

Limitations of Asset-Based and Residual Income Models

Both models carry important assumptions and limitations:

- Asset-based models may ignore valuable intangibles or undervalue ongoing businesses.

- Residual income models are sensitive to accounting choices and require careful adjustment for off-balance-sheet items, asset write-downs, and conservative or aggressive accounting practices.

- Projections of future income and book value often become unreliable beyond a few years.

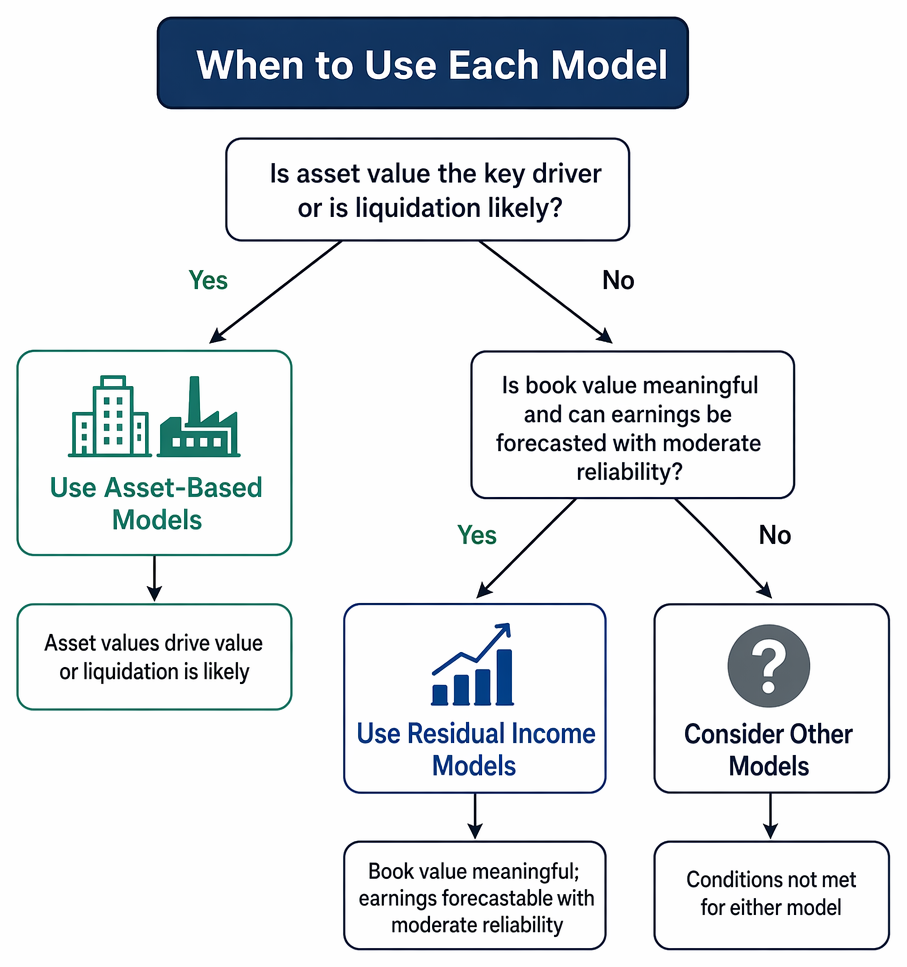

When to Use Each Model

Fundamental value combines current book value with discounted residual income, and residual income reflects net income minus the equity charge.

- Asset-based models work best for firms where asset values are the key driver or where liquidation is likely.

- Residual income models are preferred when a company’s value is not captured by dividend or cash flow models, but book value is meaningful, and earnings can be forecasted with moderate reliability.

Summary

Residual income and asset-based valuation models are important alternatives to dividend- and cash-flow-based approaches. Asset-based models focus on a “floor value” assuming orderly liquidation, while residual income models highlight value created above required equity returns. Knowing when to apply each and understanding required adjustments is tested regularly in CFA exams.

Key Point Checklist

This article has covered the following key knowledge points:

- Define and explain fundamental value and its distinction from market price

- Describe and apply the principles of asset-based valuation models for equity

- Understand residual income models, including calculation and interpretation

- Identify suitable circumstances for each model and recognize key limitations

- Adjust accounting book values to reflect fair value in both models when necessary

Key Terms and Concepts

- fundamental value

- asset-based valuation model

- residual income

- equity charge