Learning Outcomes

This article explains discounted cash flow valuation using residual income and economic value added, including:

- Defining residual income (RI), economic value added (EVA), and market value added (MVA) in precise, exam-relevant terms.

- Distinguishing RI from accounting net income and articulating why RI better reflects economic profit for equity holders.

- Computing residual income from net income, book value of equity, and required return on equity, and interpreting positive or negative results.

- Applying single-stage and multistage residual income valuation models to derive the fundamental value of equity.

- Relating EVA to NOPAT, total capital, and WACC, and evaluating how EVA links to MVA and shareholder value creation.

- Comparing residual income and EVA approaches with dividend discount and free cash flow models, noting advantages and limitations of each.

- Identifying when RI- and EVA-based models are most appropriate, given a firm’s dividend policy, earnings quality, and reliability of book values.

- Assessing the impact of key drivers—ROE, growth, and capital charges—on model outputs and valuation conclusions.

- Recognising common exam pitfalls, including misuse of accounting income as a cash flow and failure to adjust accounting data for economic reality.

CFA Level 2 Syllabus

For the CFA Level 2 exam, you are expected to understand the concepts and application of discounted cash flow valuation, focusing on residual income and economic value added, with a focus on the following syllabus points:

- Define and interpret residual income, economic value added, and market value added

- Describe the uses and limitations of residual income models

- Compute and interpret fundamental value using the single-stage and multistage residual income models

- Explain the fundamental drivers of residual income and their impact on equity valuation

- Compare and contrast residual income, dividend discount, and free cash flow models

- Adjust accounting data for EVA calculation and interpret its meaning

- Identify the appropriateness of RI and EVA models in various equity valuation scenarios

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the difference between accounting net income and residual income?

- A company has net income of $56 million, equity of $380 million, and a required return on equity of 11%. What is its residual income?

- True or false? Economic value added (EVA) incorporates both a cost of debt and a cost of equity in its calculation.

- In what circumstances is a residual income valuation model preferable to a dividend discount model?

Introduction

Discounted cash flow (DCF) valuation methods form the backbone of equity valuation for the CFA curriculum. While dividend discount and free cash flow models are commonly used, they are often impractical for firms without dividends or with unpredictable cash flows. The residual income and economic value added approaches provide effective alternatives, particularly when company dividends do not reflect real performance, or when free cash flow is negative for an extended period. These approaches measure true economic profit by charging equity investors or all capital providers for the required returns on the capital supplied.

Key Term: residual income

The net income of a firm less a capital charge for equity, calculated as net income minus equity charge (book value of equity × required return on equity). Key Term: economic value added (EVA)

An after-tax measure of a firm’s economic profit, calculated as net operating profit after tax (NOPAT) minus a charge for total capital (weighted average cost of capital × total capital). Key Term: market value added (MVA)

The difference between the market value of a firm’s capital and the book value of capital supplied by investors, representing cumulative value created over the firm’s life.

RESIDUAL INCOME AND ECONOMIC INCOME

Residual income quantifies whether a company’s profits have sufficiently compensated equity shareholders for their invested capital, considering the opportunity cost of equity. Accounting net income includes only debt costs (interest expense), ignoring the expected return required by equity holders.

Residual income can be calculated as:

- Residual Income (RI) = Net income – Equity charge

Equity charge = Beginning book value of equity × Required return on equity

A positive residual income means the firm generated returns above the required threshold. A negative value suggests the shareholders' capital could have earned more elsewhere at comparable risk.

Key Term: equity charge

The cost assigned to equity capital, calculated as book value of equity multiplied by the required return on equity.

ECONOMIC VALUE ADDED (EVA) AND MARKET VALUE ADDED (MVA)

EVA extends the residual income concept to all providers of capital. It deducts not just the cost of debt but also the required return on equity.

- EVA = NOPAT – (Weighted average cost of capital × capital employed)

Market value added (MVA) summarises the value created for all capital providers since the firm’s inception, calculated as market value of debt and equity minus invested capital.

Worked Example 1.1

A company reports net income of $20 million, has $150 million in equity, and the required return on equity is 9%. Calculate residual income.

Answer:

Equity charge = $150m × 9% = $13.5m Residual income = $20m – $13.5m = $6.5m

Worked Example 1.2

Alliance Ltd. has EBIT of $80m, a tax rate of 25%, total capital of $600m, and a WACC of 10%. Compute the company’s EVA.

Answer:

NOPAT = $80m × (1 – 0.25) = $60m Capital charge = $600m × 10% = $60m EVA = $60m – $60m = $0

Worked Example 1.3

Question: A firm has a market value of equity of $1.2bn, market value of debt $400m, and has total invested capital on its balance sheet of $1.3bn. What is its MVA?

Answer:

MVA = ($1.2bn + $400m) – $1.3bn = $300m

THE RESIDUAL INCOME VALUATION MODEL

The fundamental value of equity using the residual income model is calculated as:

- Fundamental value = current book value of equity + present value of expected future residual income.

In mathematical form, with as current book value and as forecast residual income for year :

where is the required return on equity.

Key Term: fundamental value

The value of an asset calculated as the present value of all expected future cash flows, discounted at an appropriate required rate of return.

Worked Example 1.4

Question: Carson Ltd. has a book value of $20 per share. ROE is projected at 13%, required return on equity is 10%, and the growth rate of equity is 4%. What is the fundamental value per share using the single-stage constant growth residual income model?

Answer:

Residual income per year = $20 × (0.13 – 0.10) = $0.60 Fundamental value = $20 + $0.60/(0.10 – 0.04) = $20 + $10 = $30 per shareExam Warning: A frequent mistake is to use accounting net income directly in a DCF model as if it was a cash flow. Only residual income represents true economic profit after considering the equity holders' required return.

FUNDAMENTAL DRIVERS AND APPLICATIONS

Residual income and EVA models are especially useful for valuing firms that pay little or no dividends or have unpredictable cash flows, provided earnings quality is high. They are most appropriate when accounting book values are reliable. Key determinants are:

- Book value accuracy

- Sustainable ROE in excess of required return

- Stable, predictable earnings

Key Term: sustainable ROE

An estimate of the long-run return on equity a firm can maintain, often based on projected profit margins, asset turnover, and gearing.

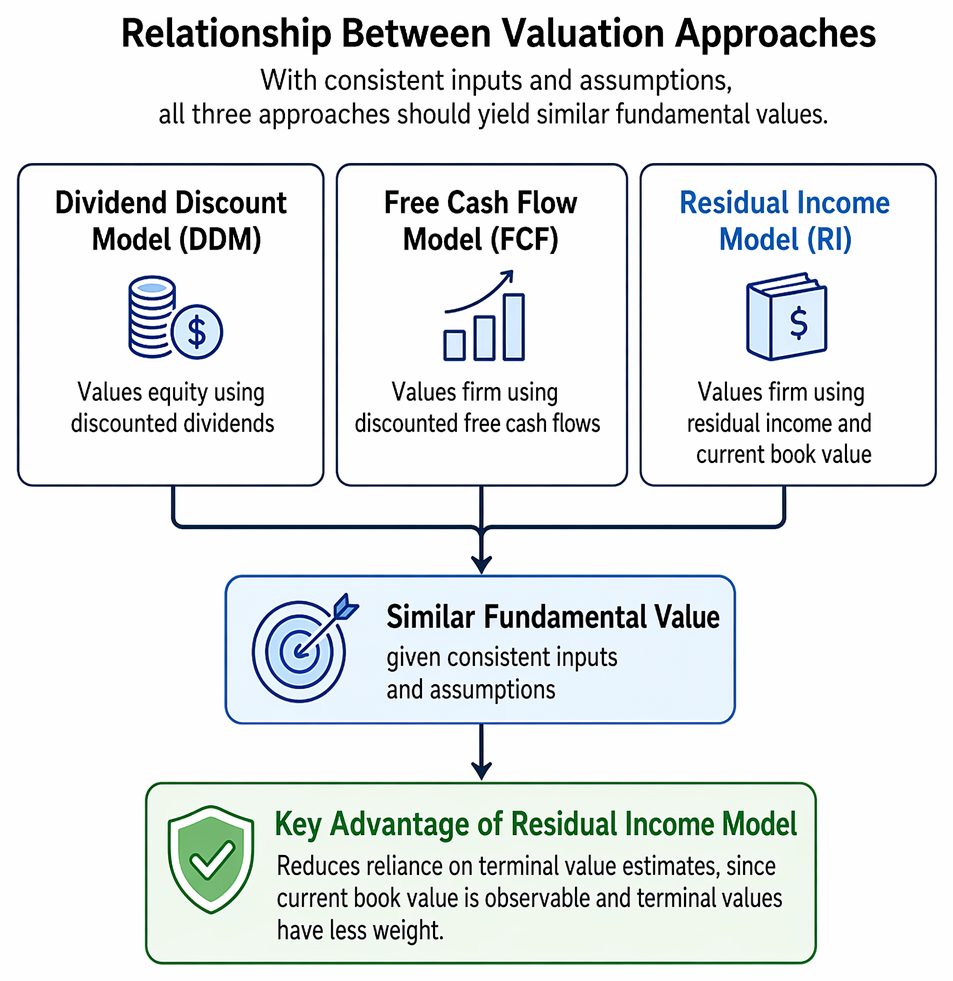

COMPARING VALUATION APPROACHES

The relation between DDM, free cash flow, and residual income models is straightforward. With consistent inputs and assumptions, all three should yield similar fundamental values. The residual income model reduces reliance on somewhat arbitrary terminal value estimates required in DDM and FCF models, since current book value is observable and terminal values have less weight.

Residual income derives from net income less the equity charge, with outcomes classified by return on equity relative to required return.

Key Term: terminal value

The estimated value assigned to all future cash flows beyond the forecast horizon in a valuation model.

LIMITATIONS OF RESIDUAL INCOME AND EVA MODELS

Despite their flexibility, residual income and EVA models require careful adjustments to accounting numbers. Analysts should adjust for:

- Off-balance sheet assets/liabilities

- Goodwill amortization, nonrecurring items

- Differences between economic and accounting depreciation or R&D expenditure

- Clean surplus relation violations

Key Term: clean surplus relation

The accounting requirement that all changes in book equity, except for capital transactions, are reflected in the income statement.Revision Tip: Clean, comparable accounting book values and accurate expected ROE estimates are critical to reliable RI and EVA model results.

Summary

Residual income and economic value added models evaluate economic profit by subtracting a capital charge from net income or operating profit. These approaches are extremely useful for valuing companies with erratic dividends or negative free cash flow, provided book values and forecast earnings are reliable. Residual income models place less emphasis on uncertain terminal values versus typical DCF techniques, which can reduce forecast sensitivity and model risk.

Key Point Checklist

This article has covered the following key knowledge points:

- Residual income is net income less a charge for equity capital

- Economic value added extends RI to all capital, using after-tax operating profit minus WACC × capital

- Residual income models compute fundamental value as book value plus discounted future RI

- RI and EVA are most useful when dividends or cash flows are unreliable/unobservable

- Key model inputs are book equity, expected ROE, required return, and accounting adjustments

- Models are particularly sensitive to earnings quality and book value reliability

Key Terms and Concepts

- residual income

- economic value added (EVA)

- market value added (MVA)

- equity charge

- fundamental value

- sustainable ROE

- terminal value

- clean surplus relation