Learning Outcomes

This article explains how fiscal policy multipliers operate in theory and practice, emphasizing the link between changes in government spending or taxation and resulting movements in aggregate demand and GDP. It clarifies the textbook multiplier formula, the role of the marginal propensity to consume and tax rates, and how leakages such as savings, imports, and debt repayment reduce the effective multiplier observed in real economies. The article analyzes how fiscal deficits accumulate into public debt, focusing on the government budget constraint, the mechanics of interest compounding, and the conditions under which the debt-to-GDP ratio becomes unsustainable. It examines crowding out as a key limitation of deficit-financed stimulus, showing how higher government borrowing can push up interest rates, displace private investment, and dampen long-run growth. The article also reviews how interactions between fiscal policy, monetary policy, and exchange rates influence inflation risk, sovereign credit risk, and currency values, providing a framework to interpret exam questions on fiscal transmission, debt sustainability, and the international consequences of persistent deficits.

CFA Level 1 Syllabus

For the CFA Level 1 exam, you are expected to understand fiscal policy's impact on aggregate demand, the calculation and interpretation of multipliers, and the sustainability issues surrounding government debt, with a focus on the following syllabus points:

- The fiscal multiplier and factors influencing its size

- Debt sustainability and the risks associated with excessive borrowing

- The interaction of fiscal and monetary policy (including crowding out)

- Causes and consequences of sovereign debt crises

- Quantitative concepts such as the government budget constraint and the debt-to-GDP ratio

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- Briefly explain why the fiscal multiplier is usually less than its theoretical maximum in practice.

- If the government increases its deficit in a country with high existing debt levels, what risk does this pose to long-term interest rates?

- Why might an increase in government spending not lead to an equivalent increase in GDP when the economy is at full employment?

- Define the “crowding out” effect in the context of fiscal policy.

Introduction

Fiscal policy—governments’ decisions on spending and taxation—can influence aggregate demand and help stabilize the economy. However, the size and effectiveness of these interventions depend on multiplier effects and the sustainability of public debt. Understanding the mechanisms and limits of fiscal multipliers, and how fiscal deficits accumulate into debt, is essential for both investment and economic analysis.

Key Term: fiscal multiplier

The ratio of the change in aggregate output (GDP) to an initial change in government spending or taxation. It measures the impact of fiscal policy on total economic activity. Key Term: government budget constraint

The requirement that current government spending must be financed either by taxes, borrowing (debt), or newly created money. Key Term: debt-to-GDP ratio

The ratio of a country's total gross government debt to its nominal GDP, widely used as an indicator of fiscal sustainability. Key Term: crowding out

The reduction in private sector investment or consumption caused by increases in government borrowing or spending, especially when resources are fully utilized.Test Tip: When revising Fiscal policy multipliers and debt dynamics, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

The Fiscal Multiplier: Mechanics and Real-World Factors

The fiscal multiplier quantifies how much GDP increases for each unit of additional government spending (or decreases via taxation). In theory, if consumers spend a constant fraction of every additional unit of disposable income received, an increase in spending will trigger a chain reaction of additional consumption—making the multiplier greater than one.

The basic formula for the spending multiplier is:

where:

- c = marginal propensity to consume (MPC)

- t = marginal tax rate

For example, an MPC of 0.8 and a tax rate of 25% yields a multiplier of 1.25, meaning each $1 of new government spending increases GDP by $1.25.

However, real economies seldom match this textbook result. The actual multiplier is often less than one due to several mitigating factors:

- Imports: If part of any additional demand is spent on foreign goods, the marginal propensity to import reduces the domestic multiplier.

- Savings: If increased income is saved instead of spent, the chain effect weakens.

- Taxes and leakages: Higher taxation, indebted households paying down debt, or uncertainty can further reduce induced consumption.

- Slack capacity: Multipliers are typically larger when there is unemployment and unused resources, and smaller when the economy is near or at potential output.

Debt Trajectories and Sustainability

When government expenditures exceed revenues, the difference is the deficit; the accumulation of deficits across years increases the public debt. The relationship is summarized in the government budget constraint:

where:

- The primary deficit is the difference between spending and revenues, excluding interest costs.

- Interest payments are determined by both the level of existing debt and borrowing costs.

Over time, debt grows both from new deficits and from compounding interest. The debt-to-GDP ratio is a key indicator: If debt grows faster than nominal GDP, the ratio rises, potentially undermining debt sustainability.

If investors fear that high and rising debt jeopardizes a government’s ability to repay, they may demand higher yields or even refuse to lend, triggering a sovereign debt crisis.

Worked Example 1.1

A government finances a $100 billion stimulus package entirely with new borrowing. If GDP grows by only $50 billion in response, what is the fiscal multiplier? What happens to the debt-to-GDP ratio if GDP was initially $2,000 billion and public debt was $800 billion?

Answer:

The multiplier is $50B / $100B = 0.5. Debt rises from $800B to $900B, GDP rises to $2,050B, so the debt-to-GDP moves from 40% to approximately 43.9%.

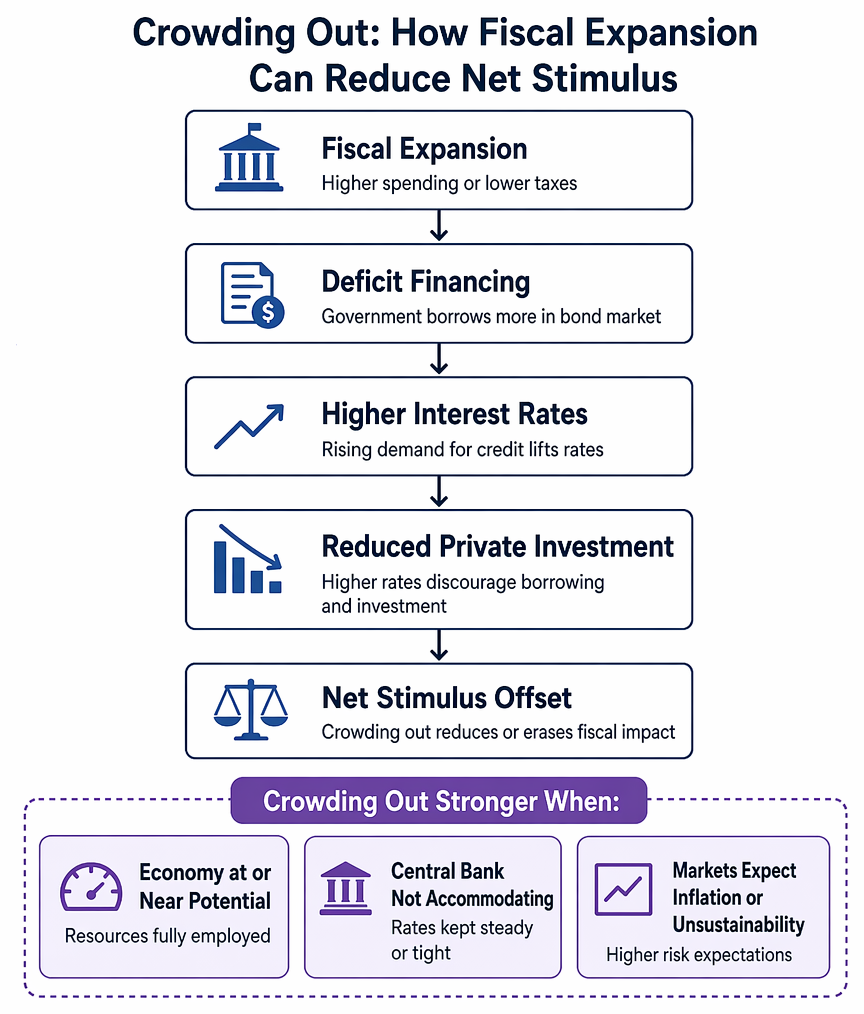

Limitations of Fiscal Policy: Crowding Out and Long-Run Risks

Fiscal expansion—higher government spending or lower taxes—can be effective, especially in deep recessions. But, as the economy approaches full capacity, fiscal stimulus risks being “crowded out”:

Public debt dynamics show how primary balances, interest costs, and nominal GDP determine debt ratios, sustainability, and sovereign default risk.

- The government often finances higher deficits by borrowing in the bond market.

- Rising demand for credit can drive up market interest rates.

- Higher rates can discourage private investment, offsetting some or all of the stimulus.

The crowding out effect is more pronounced when:

- The economy is at or near potential GDP (resources are fully employed)

- The central bank is not accommodating the fiscal expansion (i.e., keeps interest rates steady or tight in response to deficits)

- Financial markets are expecting inflation or fiscal unsustainability

Worked Example 1.2

Suppose a government announces a large deficit-financed infrastructure plan. If investors expect higher future inflation or risk, what effect could this have?

Answer:

If deficits are perceived as unsustainable, investors may demand higher yields to compensate for credit and inflation risk. This can raise borrowing costs across the economy, further increasing the cost of government debt and amplifying crowding out.Exam Warning: Be alert for questions where the multiplier is less than one due to leakages (saving, imports, taxes) or where higher interest rates reduce the net stimulus. You may also face questions on how rising debt ratios can destabilize government finances, even when deficits are modest.

Debt and Deficits: Long-Term Considerations

While countercyclical deficits are a core tool of stabilizing fiscal policy, persistent structural deficits lead to accumulating public debt. If debt grows faster than GDP, maintaining stable fiscal conditions becomes difficult.

High debt levels carry risks, such as:

- Higher future tax or spending adjustment needs

- Loss of fiscal credibility

- Pressure on the central bank to monetize debt, risking higher inflation

Key Term: structural deficit

The portion of the budget deficit not caused by temporary cyclical factors, but by the government’s baseline policies and obligations.

Sustainable fiscal policy typically requires that the primary deficit as a percentage of GDP be kept within a level compatible with long-term GDP growth rates and borrowing costs.

Worked Example 1.3

Country Z has debt equal to 100% of GDP. Its interest rate on debt is 4%, and nominal GDP grows at 2%. What primary surplus is needed (as a percentage of GDP) to stabilize the debt-to-GDP ratio?

Answer:

The country needs a primary surplus equal to (interest rate – GDP growth rate) × (debt-to-GDP): (4% – 2%) × 100% = 2%. Thus, a primary surplus of at least 2% of GDP keeps the debt ratio stable.

Fiscal Policy, FX, and the International Dimension

Fiscal deficits can affect currency values. Persistent deficits or unsustainable debt undermine investor confidence, leading to currency depreciation or crisis. In contrast, fiscal tightening may improve a country’s international standing and support its currency.

Countries with flexible exchange rates may experience exchange rate adjustments that help absorb fiscal shocks. However, if deficits are monetized, or if debt levels become very high, both inflation risk and currency risk increase.

Summary

Fiscal policy multipliers explain how government actions influence economic output. In practice, the actual impact depends on the MPC, leakages to taxes, savings, and imports, available economic slack, and private sector confidence. Persistent deficits raise the debt-to-GDP ratio, and debt trajectories hinge on growth and borrowing costs. Crowding out, higher interest rates, and FX market reactions constrain effective fiscal expansion—especially when debt is high or markets lose confidence.

Key Point Checklist

This article has covered the following key knowledge points:

- Fiscal policy multipliers measure the response of GDP to changes in spending or taxation

- The multiplier effect is reduced by leakages: savings, taxes, and imports

- Crowding out limits fiscal effectiveness, especially near potential GDP or with tight monetary policy

- Persistent deficits raise debt-to-GDP ratios, bringing debt sustainability into focus

- The stability of the debt-to-GDP ratio depends on the relationship between growth and borrowing costs

- High public debt raises long-term risks, including potential sovereign crises and FX devaluation

Key Terms and Concepts

- fiscal multiplier

- government budget constraint

- debt-to-GDP ratio

- crowding out

- structural deficit