Learning Outcomes

This article explains discounted cash flow valuation using free cash flow to the firm (FCFF) and free cash flow to equity (FCFE) models, including:

- distinguishing FCFF and FCFE in terms of definition, cash flow claimants, and valuation focus;

- identifying when each model is appropriate given leverage, dividend policy, and capital structure stability;

- deriving FCFF and FCFE from net income, EBIT, EBITDA, and cash flow from operations by making the correct exam-relevant adjustments for non-cash charges, investments in fixed and working capital, interest, and net borrowing;

- applying single-stage and multistage DCF models to convert projected FCFF or FCFE into firm value and equity value, including using WACC or the required return on equity as appropriate;

- assessing how changes in leverage, recapitalizations, dividends, share repurchases, and debt issuance or repayment affect FCFF and FCFE and, consequently, equity valuation;

- evaluating the key assumptions, strengths, limitations, and common CFA Level 2 exam pitfalls associated with FCFF- and FCFE-based valuation;

- using sensitivity analysis to see how valuation estimates respond to changes in free cash flow growth, discount rates, and capital structure assumptions.

CFA Level 2 Syllabus

For the CFA Level 2 exam, you are required to understand how discounted cash flow models are applied to equity valuation, with specific focus on free cash flow approaches; as part of your revision for this topic, ensure you can address the learning objectives below, with a focus on the following syllabus points:

- Distinguish between FCFF and FCFE, and select the appropriate model for a given company or scenario

- Explain and perform the adjustments required to calculate FCFF and FCFE from net income, EBIT, EBITDA, or CFO

- Calculate firm and equity valuation using single-stage and multistage DCF models

- Explain the effects of capital structure, dividends, share repurchases, and changes in financial gearing on FCFF and FCFE

- Use sensitivity analysis to assess valuation outcomes

- Compare the strengths and limitations of DCF methods for valuation

- Evaluate the suitability of FCFF/FCFE approaches versus dividend discount or residual income models in different contexts

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

Use the following information to answer Questions 1–4.

Alpha Components is a listed manufacturer. The analyst has compiled the following information for the most recent year (all figures in millions, except per-share data):

- Net income = 120

- Depreciation and amortization = 30

- Interest expense = 25

- Tax rate = 25%

- Capital expenditures = 60

- Proceeds from sale of equipment = 10

- Increase in non-cash working capital = 8

- Long-term debt issued = 40

- Long-term debt repaid = 12

- Cash flow from operations (CFO) reported under US GAAP = 150

- Shares outstanding = 50 million

- Market value of debt = 300

- Required return on equity = 11%

- Weighted average cost of capital (WACC) = 9%

- Expected long-run growth in free cash flow (both FCFF and FCFE) = 3% per year, constant

Assume no preferred stock.

-

Using the most direct approach from net income, Alpha’s free cash flow to the firm (FCFF) for the year is closest to:

- a) 109

- b) 121

- c) 133

- d) 146

-

Using the given information and a constant-growth FCFF model, Alpha’s total firm value (value of debt + equity) is closest to:

- a) 1,838

- b) 2,217

- c) 2,433

- d) 2,738

-

Under the same assumptions, using a constant-growth FCFE model, the implied value of equity per share is closest to:

- a) 26

- b) 31

- c) 36

- d) 41

-

Alpha announces a plan to repay a large portion of debt over the next five years, materially reducing leverage while keeping the business risk profile and operating performance unchanged. Which valuation approach is most appropriate for the analyst to emphasize?

- a) FCFE model using the current capital structure and constant-growth assumption

- b) FCFE model based on detailed forecasts of net borrowing and FCInv each year

- c) FCFF model using WACC and a constant-growth assumption

- d) Price multiples (P/E and P/B) rather than any free cash flow model

Introduction

Discounted cash flow (DCF) models are core to equity valuation in the CFA curriculum. Instead of focusing solely on dividends, these models use measures of free cash flow—either to the firm (FCFF) or to equity holders (FCFE)—as the basis for valuation. FCFF and FCFE approaches are widely used because they can be applied even when dividend policies are irregular or capital structures are changing, and they align more closely with the fundamental economics of the business.

From a conceptual standpoint:

- FCFF takes the viewpoint of all capital providers (both debt and equity). It answers: “How much cash is generated by the operations of the business that is available to service debt and equity, after reinvestment needs?”

- FCFE takes the viewpoint of common equity holders only. It answers: “How much cash could, in principle, be paid out to common shareholders this period, after meeting all operating, reinvestment, and debt-related obligations?”

Key Term: free cash flow to the firm (FCFF)

The cash flow available to all providers of capital (debt and equity) after operating expenses, cash taxes, and necessary investments in fixed and working capital, but before any payments to debt or equity holders. Key Term: free cash flow to equity (FCFE)

The cash available to common shareholders after funding operating expenses, cash taxes, required investments in fixed and working capital, and net payments to debtholders (interest and principal), but before any common dividends or share repurchases.

These free cash flow models are absolute valuation models: they estimate fundamental value by discounting a firm’s own expected cash flows, rather than comparing its multiples to peers.

Key Term: absolute valuation model

A valuation approach that estimates an asset’s fundamental value directly from its fundamentals, usually by discounting expected future cash flows.

When correctly applied, FCFF-, FCFE-, and dividend-discount models should give consistent values if they are based on the same base cash flow forecasts and discount rates. In practice, however, free cash flow models are often more practical for firms with no dividends, irregular dividends, or changing leverage.

Key Term: weighted average cost of capital (WACC)

The average after-tax required return for all providers of capital, weighted by their respective market values. It reflects the opportunity cost of the firm’s overall capital.Test Tip: When revising FCFF and FCFE models, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

FCFF AND FCFE MODELS: PURPOSE AND SELECTION

DCF valuation models estimate either the total value of a firm (using FCFF) or the value of equity (using FCFE).

- FCFF is appropriate when the firm has substantial debt, fluctuating capital structure, or pays irregular or no dividends. It is also the natural starting point if the objective is to value the enterprise (debt + equity) for an acquisition.

- FCFE is used when you are valuing equity from the viewpoint of a controlling or prospective owner able to direct cash flows, and when leverage is expected to be stable or changes can be modeled explicitly.

An important conceptual difference vs the dividend discount model (DDM):

- DDM treats the analyst as a minority shareholder, assuming dividends are what you actually receive and you cannot force management to change policy.

- FCFE treats the analyst as a controlling shareholder, assuming that all excess cash that is economically available to equity could be distributed, regardless of current dividend policy.

Key Term: leverage (financial leverage)

The extent to which a firm uses debt (and other fixed-obligation financing) in its capital structure, typically measured by ratios such as debt-to-equity or debt-to-assets.

In general:

- If leverage is changing, especially because of restructuring or recapitalizations, FCFF is usually more stable and easier to forecast.

- If leverage is relatively stable around a target ratio, FCFE can be used reliably and often aligns well with the equity viewpoint used in equity research.

FCFF: CALCULATION APPROACHES

In exam questions, FCFF can be calculated starting from net income, EBIT, EBITDA, or CFO. You must be comfortable moving between these starting points and making the necessary adjustments.

Let:

- = net income

- = non-cash charges (e.g., depreciation, amortization, provisions)

- = interest expense

- = marginal tax rate

- = fixed capital investment

- = working capital investment

Key Term: non-cash charges (NCC)

Expenses such as depreciation, amortization, and certain provisions that reduce reported earnings but do not involve a current-period cash outflow. Key Term: fixed capital investment (FCInv)

Net cash outflow for investments in long-lived assets (property, plant, equipment, intangibles), usually calculated as capital expenditures minus proceeds from sales of fixed assets. Key Term: working capital investment (WCInv)

The net investment in non-cash current assets minus non-interest-bearing current liabilities; usually measured as the period-to-period change in non-cash working capital. Key Term: cash flow from operations (CFO)

The cash generated by a firm’s core business activities, as reported in the statement of cash flows under US GAAP or IFRS, before investing and financing flows.

Standard FCFF formulas:

-

From net income:

-

From EBIT:

-

From EBITDA:

-

From CFO:

Intuition:

- Start with a profit or cash flow measure.

- Add back non-cash charges because they reduced but did not use cash.

- Subtract investments in long-term assets (FCInv) and increases in non-cash working capital (WCInv) because they absorb cash.

- Add back after-tax interest when starting from or because FCFF is calculated before servicing debtholders.

Estimating FCInv and WCInv

From financial statements:

- If there are no asset sales, a useful formula is:

- If there are asset sales, FCInv is typically:

Working capital investment is:

An increase in working capital is a use of cash (subtract in FCFF); a decrease is a source (add back).

FCFE: CALCULATION APPROACHES

There are two main methods to derive FCFE.

Let = net borrowing = new debt issued − debt repaid.

Key Term: net borrowing

The net cash inflow from debtholders in a period, equal to debt issued minus debt repaid across both short-term and long-term debt.

-

From FCFF:

Here you remove flows that belong to debtholders (after-tax interest) and add any net new money raised from them (net borrowing).

-

Direct from net income:

-

From CFO:

Notice that unlike FCFF, FCFE does not add back after-tax interest because FCFE is cash after servicing debtholders.

For forecasting, when a firm targets a constant debt-to-asset ratio , net borrowing is often modeled as a constant fraction of net investment:

Key Term: target debt-to-asset ratio (DR)

The proportion of new investment in assets that management plans to finance with debt over the forecast horizon.

If is the target debt ratio, a commonly tested forecasting relationship is:

This substitutes explicit net borrowing forecasts with the assumption that a constant proportion of investment is financed with debt.

Worked Example 1.1

Calculate FCFF and FCFE from Financial Statements

A company reports the following for the current year (in millions): Net income = 90; Depreciation = 20; Capital expenditures = 25; Increase in non-cash working capital = 5; Interest expense = 10; Tax rate = 30%; Net borrowing = 12.

Answer:

Start with the FCFF formula from net income:

For FCFE from net income:

So FCFF = 87 million and FCFE = 92 million.

Interpretation: because net borrowing (12) exceeds after-tax interest (7), FCFE is greater than FCFF in this period.

VALUATION MODELS

Once FCFF or FCFE is forecast, valuation follows the standard DCF principle: value is the present value of expected future cash flows discounted at the appropriate rate.

Key Term: required return on equity (r)

The return that equity investors demand for holding a company’s stock, often estimated using CAPM or other risk-based models; used to discount FCFE or dividends. Key Term: terminal value

The estimated value of a business (or its equity) at the end of an explicit forecast horizon, typically calculated using a constant-growth perpetuity or an exit multiple.

Firm Valuation: Using FCFF

Firm value is the present value of expected future FCFF discounted at the WACC:

To obtain equity value:

If there is preferred stock, remember to subtract its market value as well; FCFF belongs to all capital providers.

Equity Valuation: Using FCFE

Equity value is the present value of expected FCFE discounted at the required return on equity :

Both models support single-stage (constant growth) and multistage (variable growth) forms, analogous to dividend discount models.

Key Term: single-stage free cash flow model

A valuation model that assumes free cash flow grows at a constant rate forever and discounts the implied perpetuity at a constant required return. Key Term: multistage free cash flow model

A valuation model that allows free cash flow growth to vary across two or more stages (e.g., high growth then stable growth), with potentially different discount rates or assumptions in each stage.

Under constant growth, the FCFF-based firm value is:

And the FCFE-based equity value is:

where or is next year’s free cash flow.

Worked Example 1.2

Valuing Equity with Constant-Growth FCFE

A firm’s expected FCFE next year is 5 per share and is expected to grow at 4% in perpetuity. The required return on equity is 10%.

Answer:

Apply the constant-growth FCFE model:

This is the fundamental value per share implied by the FCFE forecast and required return.

Worked Example 1.3

Valuing Equity with a Single-Stage FCFF Model

Beta Foods generated FCFF of 40 million last year. FCFF is expected to grow at 3% per year indefinitely. The firm’s before-tax cost of debt is 6%, tax rate is 30%, and required return on equity is 11%. The market value of debt is 160 million, and there are 20 million shares outstanding. The target capital structure is 30% debt, 70% equity (by market value).

Answer:

First compute the after-tax cost of debt:

Determine WACC using target weights:

We have FCFF_0 = 40, so:

Apply the single-stage FCFF model:

Equity value is firm value minus debt:

Value per share:

This is the implied value per share based on FCFF.

Multistage Models and Terminal Value

Most real-world applications (and many exam vignettes) involve two-stage or three-stage free cash flow models:

- A first stage of explicit forecast (e.g., 3–5 years) with detailed year-by-year FCFF or FCFE estimates.

- A second stage where growth converges to a long-run stable rate, and a terminal value is calculated, often using a constant-growth formula at the start of the stable period.

Typical structure for a two-stage FCFF model:

- Forecast for years 1 to using explicit assumptions about sales, margins, capital expenditures, and working capital.

- Compute the terminal value at :

- Discount all (1 to ) and back to today at the appropriate WACC (often using the high-growth WACC if the firm’s risk does not change materially).

FCFE multistage models follow exactly the same structure, with FCFE and replacing FCFF and WACC.

Key Term: recapitalization

A significant change in a company’s capital structure, often involving large debt issuance or repayment, equity issuance, or share repurchases that alter leverage.

In situations involving large recapitalizations or planned leverage changes, multistage models are particularly useful because they allow different assumptions about net borrowing, interest expense, and discount rates in each stage.

SPECIAL CONSIDERATIONS

Free cash flow to the firm can be derived from several accounting bases using tax-adjusted interest and reinvestment adjustments.

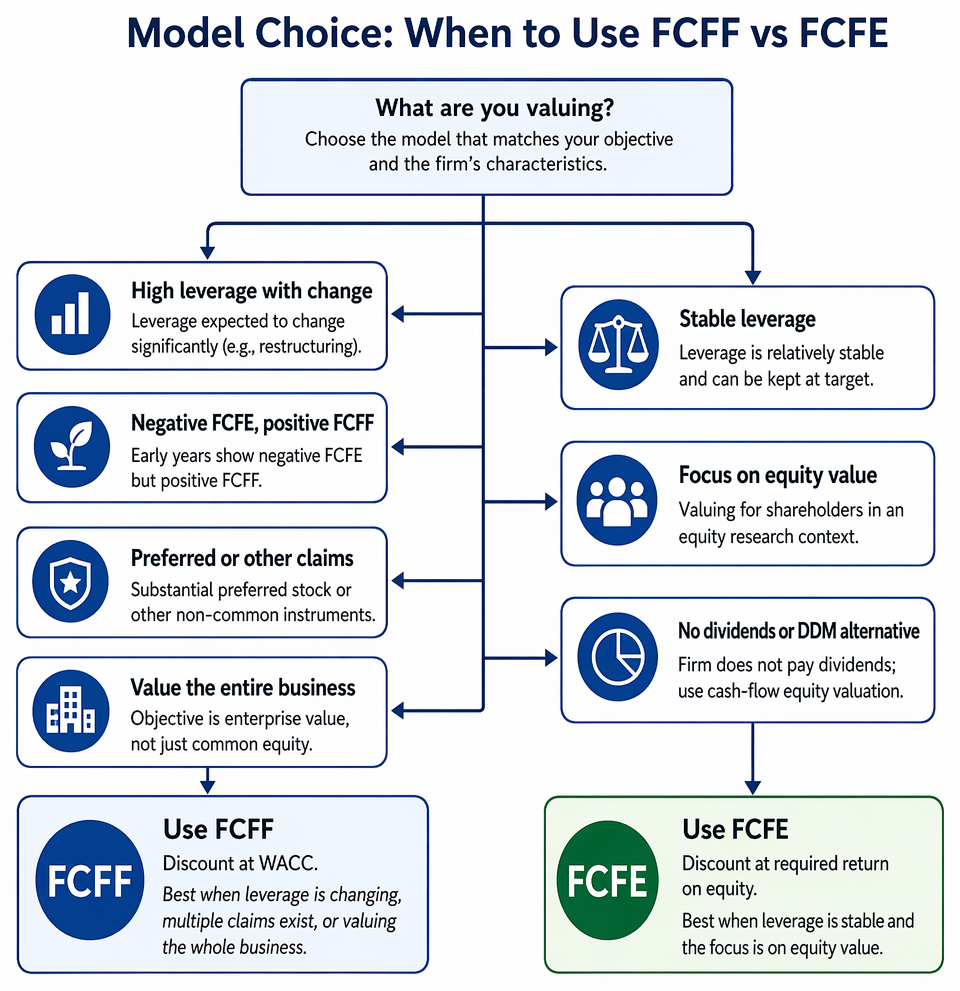

Model Choice: When to Use FCFF vs FCFE

-

Use FCFF when:

- The firm is highly leveraged and leverage is expected to change significantly (e.g., debt restructuring, buyouts).

- The firm has negative FCFE but positive FCFF in early years (common for firms aggressively funding growth with debt).

- There is substantial preferred stock or other non-common equity instruments.

- You want to value the entire business, not just the common equity.

-

Use FCFE when:

- Leverage is relatively stable and can be modeled as a constant target ratio.

- You are focusing on the equity value for shareholders, especially in an investment or equity research context.

- The firm does not pay dividends, but you want a cash-flow-based equity valuation alternative to DDM.

Leverage and Volatility of Cash Flows

FCFE is more sensitive than FCFF to leverage changes:

- Increased borrowing raises FCFE in the short run (through positive net borrowing) but reduces FCFE in later years via higher interest and principal payments.

- Deleveraging (repaying debt) does the opposite: FCFE is lower today but higher in the future.

FCFF largely filters out these financing choices because it focuses on cash before debt payments. As a result, FCFF is often smoother and easier to forecast in periods of capital structure change.

Dividends, Share Repurchases, and Share Issues

Dividends, share repurchases, or share issues have no direct impact on FCFF or FCFE because they are uses of free cash flow, not determinants of it.

- FCFF and FCFE are calculated before any common dividends or share repurchases.

- These transactions affect how free cash flow is distributed, not how much is generated.

Key Term: dividends and share repurchases (payouts)

Cash distributions to common shareholders; they are applications of free cash flow rather than components in its calculation.

Everything else equal, a firm could cut dividends and repurchases to zero for a period; FCFE would be unchanged, but cash on the balance sheet would grow.

Exam Warning: FCFF should be discounted at the WACC. FCFE should be discounted at the required return on equity. Using the wrong discount rate is a frequent exam mistake, especially when both FCFF and FCFE are provided in the vignette.

Another recurring pitfall is using the wrong cash flow (0 vs 1) in constant-growth models. The formulas require next period free cash flow ( or ), not last year’s.

Forecasting FCFF and FCFE

There are two main approaches on the exam:

-

Top-down (aggregate FCF growth):

- Compute a base-year FCFF or FCFE.

- Apply assumed growth rates for each stage (e.g., 8% for three years, then 3% forever).

- This is simple but assumes the relationship between earnings, capital expenditure, and working capital remains stable.

-

Bottom-up (component-based):

- Forecast revenues, margins, capital expenditures (maintenance + growth), depreciation, working capital, and net borrowing separately.

- Use FCFF or FCFE formulas each year.

- This is more realistic and allows different growth rates and margin behavior, but is more detailed.

Capital expenditures should be separated conceptually into:

- Spending needed to maintain current capacity (maintenance capex).

- Incremental spending needed to support growth.

Only the total FCInv matters for free cash flow, but understanding the split helps you judge whether growth assumptions are consistent with investment levels.

Effects of Leverage Changes on FCFF and FCFE

- FCFF is not affected by changes in leverage (aside from second-order tax effects if the tax rate or interest tax shield changes in economic terms).

- FCFE is partially offset over time:

- A debt increase boosts FCFE now via positive net borrowing, but reduces future FCFE via higher interest and repayment.

- A debt decrease reduces FCFE now and increases it in later years as interest savings materialize.

This timing pattern is sometimes explicitly tested: you may be asked to identify short-term vs long-term effects of a leverage change on FCFE.

Comparing FCFE and Dividend Discount Models

Both DDM and FCFE discount cash flows to equity at , but:

- DDM uses actual or forecast dividends, which may not reflect the firm’s capacity to pay if management retains excess cash or follows a conservative policy.

- FCFE uses potential distributable cash, assuming a controlling investor can set payout policy optimally.

Thus, FCFE models are particularly useful when:

- The firm does not pay dividends, or dividends are unrelated to profitability.

- You are valuing private companies or control stakes where you could change payout policy.

Net Income and EBITDA as Proxies: Why They Are Poor Substitutes

On the exam, you may be asked to evaluate statements such as “FCFE can be approximated by net income” or “EBITDA is a good proxy for FCFF.” These are generally incorrect, because:

-

Net income leaves out:

- Non-cash charges that must be added back.

- Capital expenditures and changes in working capital.

- Net borrowing.

-

EBITDA ignores:

- Taxes.

- Investments in fixed and working capital.

Key Term: EBITDA

Earnings before interest, taxes, depreciation, and amortization; a pre-tax, pre-capex, pre-working-capital profitability measure, not a measure of free cash flow.

Only in stable, mature firms with low growth and stable investment patterns might net income or EBITDA loosely resemble free cash flow, but this is not reliable for valuation.

Sensitivity Analysis in FCFF and FCFE Valuation

Key Term: sensitivity analysis

A technique that assesses how sensitive a valuation estimate is to changes in key inputs, such as growth rates, discount rates, or margins.

For FCFF/FCFE models, the most important sensitivities typically include:

- Long-run growth rate () in free cash flow.

- Discount rates (WACC or ).

- Base-year free cash flow (especially if the chosen year is not representative).

- Assumptions about capital expenditure and working capital intensity.

On the exam, you may be given a table of alternative values based on different input assumptions and asked to:

- Identify which input has the largest impact on value.

- Assess whether the analyst’s “base case” is robust or relies on optimistic assumptions.

ADVANTAGES AND LIMITATIONS

Advantages:

-

Broad applicability:

- Applicable to firms with no or irregular dividends.

- Useful for firms where accounting earnings are volatile but core cash generation is more stable.

-

Control viewpoint:

- Especially FCFE is useful for controlling shareholders or potential acquirers, as it reflects cash that could be distributed.

-

Economic focus:

- Links valuation explicitly to fundamental drivers: profitability, reinvestment needs, and financing policy.

Limitations:

-

Forecasting difficulty:

- Requires assumptions about growth, margins, capital expenditures, and debt policy, which can be difficult to forecast—particularly for young, cyclical, or transitional firms.

-

Model sensitivity:

- Terminal value often represents a large fraction of total value, so small changes in or WACC can materially affect the valuation.

-

Data and complexity:

- Multistage models require detailed year-by-year projections that may not be supported by reliable information.

-

Capital structure uncertainty:

- FCFE models can be unreliable if leverage is changing unpredictably; FCFF partly mitigates this but still requires assumptions about the long-run target capital structure (for WACC).

Worked Example 1.4

Two-Stage FCFE Valuation (Conceptual Structure)

Suppose an analyst projects the following FCFE per share for Delta Tech:

- Years 1–3: FCFE grows from 2.00 to 2.40 to 2.80 per share (explicit forecasts).

- From Year 4 onwards: FCFE grows at a constant 4% per year.

- Required return on equity = 10%.

Outline the valuation steps and compute the terminal value at the end of Year 3.

Answer:

Step 1: Use the forecast FCFE for Years 1–3:

- FCFE_1 = 2.00

- FCFE_2 = 2.40

- FCFE_3 = 2.80

Step 2: Compute FCFE_4 under constant growth:

Step 3: Calculate the terminal value at t = 3 using the constant-growth FCFE formula:

Step 4 (not fully required here): The total equity value per share today would be the present value of FCFE_1, FCFE_2, FCFE_3, and TV_3, all discounted at r = 10%.

Worked Example 1.5

Choosing Between FCFF and FCFE

Which valuation model is more appropriate for a highly leveraged company currently restructuring its debt?

Answer:

The FCFF model is generally better. Because the firm's future debt payments, net borrowing, and capital structure are unpredictable, FCFE will be highly volatile and difficult to forecast. FCFF, which is calculated before servicing debt, is less sensitive to these financing changes and can be discounted at an appropriately estimated WACC to obtain firm value, from which equity value can be derived.

Summary

Discounted cash flow models based on FCFF and FCFE are key tools for equity and firm valuation in cases where dividends are irregular, capital structures change, or the analyst requires a viewpoint reflecting all providers of capital or only equity holders. Accurate calculation of free cash flow, appropriate model selection, and careful forecasting are critical to correct application.

Key exam skills include:

- Knowing which starting point (NI, EBIT, EBITDA, CFO) to use and making the correct adjustments.

- Selecting FCFF vs FCFE based on leverage profile and valuation objective.

- Applying constant-growth and multistage models, including correct use of or and terminal value formulas.

- Recognizing how leverage changes and financing decisions affect FCFE but not FCFF.

- Using sensitivity analysis to judge the robustness of valuation results.

Be vigilant for common exam mistakes, such as using the wrong discount rate, confusing FCFF with FCFE, miscalculating capital investments, or using net income and EBITDA as free cash flow proxies without appropriate adjustments.

Key Point Checklist

This article has covered the following key knowledge points:

- Distinguish FCFF from FCFE in terms of definition, cash flow claimants, and ownership viewpoint.

- Select the suitable model (FCFF vs FCFE) based on leverage stability, dividend policy, and valuation focus (firm vs equity).

- Calculate FCFF and FCFE using net income, EBIT, EBITDA, or CFO, making correct adjustments for non-cash charges, FCInv, WCInv, interest, and net borrowing.

- Estimate FCInv and WCInv from balance sheet and cash flow information, including cases with asset sales.

- Apply the proper discount rate for FCFF (WACC) and FCFE (cost of equity), and avoid mixing cash flow types with the wrong discount rate.

- Implement single-stage constant-growth and multistage free cash flow models, including terminal value estimation.

- Understand how capital structure, financial gearing, changes in leverage, and net borrowing affect FCFE and why FCFF is largely unaffected.

- Recognize that dividends, share repurchases, and share issues are uses of free cash flow and do not directly affect FCFF or FCFE.

- Compare FCFE models with dividend discount models and explain when each is more appropriate.

- Explain why net income and EBITDA are poor proxies for free cash flow unless adjusted.

- Use sensitivity analysis to identify which assumptions (growth, discount rates, investment intensity) have the greatest impact on valuation.

- Evaluate the main strengths and limitations of FCFF and FCFE models for equity valuation.

Key Terms and Concepts

- free cash flow to the firm (FCFF)

- free cash flow to equity (FCFE)

- absolute valuation model

- weighted average cost of capital (WACC)

- leverage (financial leverage)

- non-cash charges (NCC)

- fixed capital investment (FCInv)

- working capital investment (WCInv)

- cash flow from operations (CFO)

- net borrowing

- target debt-to-asset ratio (DR)

- required return on equity (r)

- terminal value

- single-stage free cash flow model

- multistage free cash flow model

- recapitalization

- dividends and share repurchases (payouts)

- EBITDA

- sensitivity analysis