Learning Outcomes

This article explains the regime for costs management and budgeting in civil litigation under the Civil Procedure Rules (CPR). It outlines the purpose, key procedures, and potential consequences associated with managing litigation costs. For the SQE1 assessments, you will need to understand the process of preparing and filing costs budgets, the nature and effect of Costs Management Orders (CMOs), the requirements for revising budgets, and the implications of non-compliance. Your understanding will enable you to apply the relevant rules to SQE1-style single best answer MCQs concerning costs management scenarios.

It also develops the skills to identify when the costs management regime applies (and when it does not), how the court approaches costs reasonableness and proportionality through the CCMC, and how approved budgets influence detailed assessment. You should be able to explain the practical steps and documents involved (Precedent H, R and T), the “good reason” test under CPR 3.18, the interaction between budgets and the standard versus indemnity bases of assessment, and how to seek relief from sanctions (Denton) where budget deadlines are missed.

SQE1 Syllabus

For SQE1, you are required to understand the practical application of the costs management rules. It is likely that you will need to identify the correct procedure for budgeting, recognise the implications of a CMO, or determine the consequences of failing to comply with the rules, with a focus on the following syllabus points:

- the purpose and scope of the costs management regime (CPR 3.12-3.18)

- the process for preparing, filing, and agreeing costs budgets (Precedent H)

- the nature, content, and effect of Costs Management Orders (CMOs)

- the procedure for seeking variations to approved budgets (Precedent T)

- the consequences of failing to comply with costs management rules and orders, particularly CPR 3.14

- the court's approach to assessing costs by reference to approved or agreed budgets.

- when costs management is disapplied (e.g., claims valued at £10 million or more, fixed costs cases) and when the court may order it nonetheless

- how budgets interact with the basis of assessment (standard versus indemnity) and the “good reason” test to depart from budgets.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

In which type of case does the costs management regime under CPR Part 3 generally apply?

- a) Small claims track cases

- b) Fast track cases

- c) Multi-track cases

- d) All cases regardless of track.

-

What is the primary form used for setting out a party's detailed costs budget?

- a) Form N244

- b) Precedent T

- c) Form N265

- d) Precedent H.

-

What is the likely sanction if a party, required to file a costs budget, fails to do so by the specified deadline?

- a) The party's claim or defence may be struck out.

- b) The party will be limited to recovering only the applicable court fees for their costs.

- c) The party must pay the costs of the Costs Management Conference immediately.

- d) The party automatically receives an extension of time.

Introduction

Managing the costs of litigation effectively is a fundamental aspect of modern civil procedure in England and Wales. The rules aim to ensure that the costs incurred by parties are proportionate to the issues in dispute and that litigation is conducted efficiently. For SQE1, you must understand the framework established by the CPR for controlling costs through budgeting and management orders. This involves knowing the key procedural steps, the documents involved, and the potential sanctions for non-compliance. The court actively manages costs, particularly in multi-track cases, to keep expenses under control from an early stage.

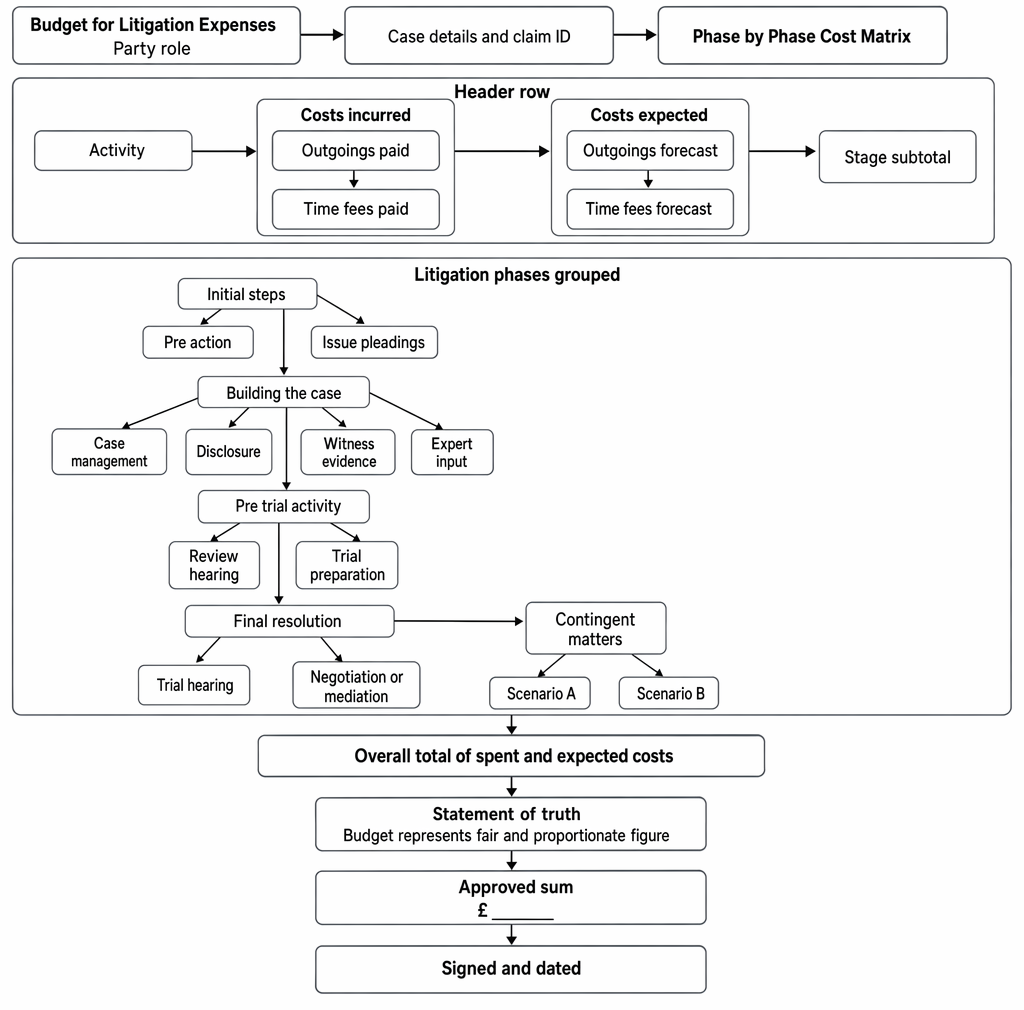

Structure of a civil litigation costs budget, showing budget phases, incurred and estimated costs, overall total, and approval details.

Key Term: Proportionality

The principle that costs incurred in litigation should bear a reasonable relationship to the factors of the case, including the sums in issue, complexity, and importance.

THE COSTS MANAGEMENT REGIME (CPR 3.12 – 3.18)

The primary rules governing costs management are found in CPR 3.12 to 3.18 and Practice Direction 3D. (Note: prior to 6 April 2023 the companion practice direction was numbered PD 3E; PD 3E is now the practice direction dealing with costs capping.) The regime generally applies to most multi-track cases commenced on or after 1 April 2013, with some exceptions (e.g., cases valued at £10 million or more, unless the court orders otherwise, and cases subject to fixed or scale costs).

The overarching purpose is to enable the court to manage both the steps to be taken and the costs to be incurred by the parties, ensuring litigation is conducted proportionately and at reasonable expense. Costs management supports the overriding objective (CPR 1.1) by encouraging early identification of steps and their likely expense, and by using budgets as a reference point throughout case management and at assessment.

In practice, the court will engage with costs at, or around, the first Costs and Case Management Conference (CCMC), considering the parties’ budgets alongside the proposed directions. The judge may approve, reduce, or otherwise revise budgeted figures to the extent necessary to keep costs within a reasonable and proportionate range, while recording comments on incurred costs.

Key Term: Costs Management

The court’s process, under CPR 3.12–3.18 and PD 3D, of controlling the parties’ future costs through budgets and orders so that cases proceed at proportionate cost. Key Term: Costs and Case Management Conference (CCMC)

A hearing, often held after allocation in multi-track claims, at which the court considers case directions and parties’ costs budgets in tandem, typically making a Costs Management Order (CMO).

Proportionality

A key principle supporting costs management is proportionality. Costs incurred are proportionate if they bear a reasonable relationship to the sums in issue, the value of non-monetary relief, the complexity of the litigation, additional work generated by the paying party's conduct, and any wider factors like reputation or public importance. Costs budgets help the court assess proportionality from the outset.

Proportionality is revisited at assessment (CPR 44.3). On the standard basis, costs which are disproportionate may be reduced or disallowed, even if reasonably incurred. The court will factor in approved or agreed budgeted costs when deciding whether the overall figure remains proportionate.

Key Term: Proportionality

The principle that costs incurred in litigation should bear a reasonable relationship to the factors of the case, including the sums in issue, complexity, and importance, and any vulnerability-related additional work.

PREPARING AND FILING COSTS BUDGETS

Parties subject to costs management must prepare and exchange detailed costs budgets.

The Costs Budget (Precedent H)

The budget must be drafted using the prescribed court form, Precedent H. It requires parties to set out the costs they have already incurred (incurred costs) and the costs they estimate they will incur for each future stage of the litigation (estimated costs).

Key Term: Costs Budget (Precedent H)

A detailed statement, in the prescribed form (Precedent H), setting out the costs a party has incurred to date and estimates it will incur for each stage of the proceedings going forward. Key Term: Incurred Costs

Costs relating to work done before the date of the budget. The court typically does not approve incurred costs but may comment on them. Key Term: Estimated Costs

Costs relating to work anticipated to be done after the date of the budget for defined future stages (phases) of the litigation. These are the primary focus of court approval.

Precedent H is structured by phases, typically including: pre-action, issue/statements of case, CMC, disclosure, witness statements, expert reports, ADR/settlement discussions, trial preparation, PTR (if ordered), trial, and contingencies. Contingencies capture discrete steps not already covered (e.g., a third-party disclosure application, amendment applications, or preliminary issues). Budgets should include assumptions explaining the scope of work and key drivers behind the figures (e.g., number of witnesses, expected disclosure volume, expert disciplines).

As a general rule (confirmed in PD 3D), budgets exclude VAT (where not recoverable), success fees, ATE insurance premiums, costs of detailed assessment, appeals, and enforcement. Counsel’s fees, expert fees, court fees, and solicitor time should be included where relevant to the phases.

The budget must be signed with a statement of truth by a senior legal representative of the party. Parties should also provide fundamental assumptions for their figures.

Filing and Exchange Deadlines

The timing for filing and exchanging budgets depends on the value of the claim:

- For claims valued under £50,000: File and exchange with the Directions Questionnaire.

- For other multi-track claims: File and exchange not later than 21 days before the first Case Management Conference (CMC).

Failure to file a budget on time carries a severe sanction under CPR 3.14.

Worked Example 1.1

Your client is the Claimant in a multi-track case valued at £200,000. The first Case Management Conference (CMC) is listed for 30th June. What is the latest date your client must file and exchange their costs budget (Precedent H)?

Answer:

The costs budget must be filed and exchanged not later than 21 days before the first CMC. Therefore, the latest date is 9th June.

The Budget Discussion Report (Precedent R)

Parties are required to discuss each other's budgets after exchange. They must file an agreed Budget Discussion Report (Precedent R) no later than 7 days before the first CMC, setting out which figures are agreed, which are not agreed, and brief reasons for disagreement.

Key Term: Budget Discussion Report (Precedent R)

A short report in Precedent R listing, phase-by-phase, the figures agreed and not agreed between parties, with concise grounds of dispute, filed at least 7 days before the first CMC.

Best practice is to use assumptions consistently between Precedent H and Precedent R so the judge can cross-reference easily. Meaningful engagement at this stage can reduce CCMC time and costs. Where significant agreement is achieved, the court may approve the agreed parts and focus only on disputed phases.

COSTS MANAGEMENT ORDERS (CMOs)

At the CMC, or another hearing, the court will typically consider the parties' budgets and make a Costs Management Order (CMO).

Key Term: Costs Management Order (CMO)

An order made by the court recording the extent to which the parties' budgeted costs (usually the estimated costs for each phase) are approved.

The court will review the estimated costs for each phase of the litigation. It may approve the figures as budgeted or set different figures if it considers the budgeted amounts disproportionate. The court will not typically approve figures for incurred costs but may comment on them.

The effect of a CMO is significant. When assessing costs at the end of the case, the court will not depart from the approved or agreed estimated costs in the CMO unless satisfied that there is a good reason to do so (CPR 3.18). This provides parties with greater certainty about their potential costs recovery (and liability).

Key Term: Good Reason (CPR 3.18)

A justification sufficient to depart at assessment from approved or agreed budgeted costs for a phase; examples include significant developments not captured by the budget, or where costs were not incurred at all or were much less than budgeted (supporting downward adjustment).

Approved budgets guide case management decisions (CPR 3.17) and remain a central point of reference at detailed assessment. The CCMC may be combined with case directions or held separately in complex cases, and judges can revisit budgets later if necessary.

The regime includes tools beyond budgets:

- In appropriate cases, the court may make a costs capping order (CPR 3.19) limiting future recoverable costs where justified to further the overriding objective.

- The court may consider whether a party’s conduct is oppressive, and take steps to manage proceedings and costs proportionately (e.g., by limiting expert fields or directing issue-based disclosure).

Key Term: Costs Capping Order

An order limiting the amount of future costs a party may recover, made under CPR 3.19 where necessary to further the overriding objective and control disproportionate expenditure.Exam Warning: Remember the strict consequence under CPR 3.14: If a party fails to file a budget when required, they are treated as having filed a budget comprising only the applicable court fees. They will generally be unable to recover any further costs for the litigation, even if successful. This is a draconian sanction underscoring the importance of compliance.

Where the CPR 3.14 sanction bites, an application for relief from sanctions under CPR 3.9 may be made. The Denton approach (three-stage test) will be applied: seriousness/significance of the breach, why the default occurred, and all the circumstances (including efficient conduct and compliance). Prompt applications with cogent reasons fare better, but relief is not guaranteed.

Key Term: Relief from Sanctions (Denton)

The structured approach to CPR 3.9: assess seriousness/significance; consider reasons for default; then evaluate all circumstances, including efficiency and compliance, to decide whether relief should be granted.

Worked Example 1.2

The Defendant in a multi-track claim (value £750,000) fails to file a Precedent H by the deadline. The CCMC is in two weeks. What is the immediate consequence, and what procedural step should the Defendant consider?

Answer:

Under CPR 3.14 the Defendant is treated as having filed a budget consisting of court fees only. The Defendant should promptly apply for relief from sanctions under CPR 3.9, addressing the Denton criteria with evidence and proposing any remedial steps.

REVISING COSTS BUDGETS

Litigation can be unpredictable. If circumstances change significantly during the proceedings, a party may need to revise its approved budget.

Significant Developments

A budget can only be revised if there has been a significant development in the litigation that warrants such a revision. Minor changes or miscalculations in the original budget are generally not sufficient.

Key Term: Significant Development

A change in circumstances occurring after the last approved budget which was not reasonably foreseeable and which significantly impacts the estimated costs.

Examples include an unexpected doubling of disclosure volume, late introduction of complex new issues or additional expert disciplines, or court-ordered steps not contemplated when the budget was approved. Parties must act promptly to seek variation once the development becomes apparent.

The Variation Process (Precedent T)

If a party wishes to revise its budget due to a significant development, it must:

- Promptly prepare a variation using Precedent T, explaining the significant development and the proposed changes.

- Serve Precedent T on other parties for agreement.

- If not agreed, apply to the court for approval of the variation.

The court has discretion whether to approve the revised figures. Failure to seek timely approval for necessary variations can prejudice a party's ability to recover costs exceeding the previously approved budget. Variations are phase-specific; assumptions should be updated to reflect the revised scope and drivers.

Key Term: Budget Variation (Precedent T)

The prescribed form (Precedent T) used by a party to propose revisions to its approved costs budget following a significant development.

Worked Example 1.3

A Claimant's costs budget was approved in a CMO. Six months later, the Defendant amends its Defence to introduce a complex new issue requiring substantial additional expert evidence not originally anticipated. The Claimant estimates this will increase costs for the expert evidence phase by £25,000. What should the Claimant do?

Answer:

This likely constitutes a significant development. The Claimant should promptly prepare a Precedent T detailing the development and the revised figure for the relevant phase(s). They should serve it on the Defendant, seeking agreement. If agreement is not reached, the Claimant must apply to the court for approval of the budget variation.

Worked Example 1.4

During disclosure, the Defendant produces 10,000 documents instead of the anticipated 2,000. The Claimant’s disclosure phase was approved at £18,000. The Claimant has already incurred £17,500 and anticipates a further £20,000 to complete reasonable review. How should the Claimant proceed to maximise recoverability?

Answer:

Prepare and serve a prompt Precedent T explaining the unexpected increase in disclosure volume and its impact, revising the disclosure phase upward with clear assumptions (review methodology, staffing, technology used). If not agreed, seek court approval. Without variation, it will be hard to show a “good reason” to depart at assessment.

Costs Assessment and Exceeding Budgets

At the conclusion of the case, when costs are assessed, the court will have regard to the last approved or agreed budget (CPR 3.18). As noted, the court will not depart from the budget unless there is a "good reason". Simply exceeding the budget without it being varied is unlikely to constitute a good reason. Therefore, careful monitoring and timely applications to vary budgets where justified are essential.

A “good reason” may justify reductions as well as increases. For example, where budgeted costs were not incurred at all for a phase (or were incurred substantially below the approved figure), the court may adjust downward. By contrast, budgets generally do not cap indemnity costs; if the court orders indemnity costs for part of the period, proportionality does not apply, and the budget is less constraining. However, the budget may still be a relevant indicator of reasonableness.

Key Term: Costs Assessment and Budgets

Under CPR 3.18, approved or agreed budgeted costs guide the standard basis assessment, with departures permitted only for a good reason; on indemnity basis, budgets do not control recovery but may inform reasonableness.

Worked Example 1.5

The Defendant is ordered to pay the Claimant’s costs on the standard basis. The Claimant seeks £80,000 for trial preparation and trial phases against an approved combined budget of £65,000. No Precedent T was filed. The Claimant argues a longer-than-expected trial due to the Defendant’s conduct. What is the likely approach?

Answer:

The court will start from the approved budgets. Without a timely budget variation, exceeding approved figures is rarely allowed. If the Claimant demonstrates a clear, unforeseen development caused by the Defendant (e.g., unexpected witness issues extending trial time) with contemporaneous evidence, the court may find a “good reason” to depart upward. Otherwise, recovery will likely be limited to the budgeted figures.Revision Tip: Focus on the key documents (Precedent H, Precedent R, Precedent T) and their purpose within the costs management timeline. Understand the critical deadlines and the severe consequences of non-compliance under CPR 3.14.

Additional Practical Points

- Costs management applies primarily to multi-track cases. It does not usually apply where the stated value is £10 million or more, or where fixed recoverable costs apply. The court can nonetheless direct costs management in otherwise excluded cases if appropriate.

- Litigants in person are not required to file budgets (CPR 3.13), though the court may still consider costs management when making directions.

- Parties should use budgets actively: monitor spend per phase, track assumptions against developments, and engage early if variance is likely. Regular internal reviews reduce the risk of last-minute overspend or missed variation opportunities.

- Assumptions matter: vague or generic assumptions hinder CCMC outcomes and later variation. Specificity on witness numbers, data volumes, expert disciplines, and trial length supports credible figures.

- Oppressive conduct and disproportionate steps can be addressed by directions limiting scope: issue-by-issue disclosure, single joint expert where appropriate, or costs capping orders in rare cases.

Worked Example 1.6

A Defendant considers the Claimant’s proposed expert costs disproportionate and oppressive (three experts in overlapping disciplines, total budgeted expert costs £120,000 in a £200,000 claim). What application or step should the Defendant take?

Answer:

Raise the issue in the Precedent R and at the CCMC, seeking directions limiting expert evidence (e.g., single joint expert or fewer disciplines) and inviting a costs management order reducing the expert phases accordingly. If necessary, consider a costs capping application, although caps are rare and require justification under CPR 3.19.

Key Point Checklist

This article has covered the following key knowledge points:

- Costs management applies primarily to multi-track cases, aiming for proportionality and efficiency.

- Parties must prepare and exchange costs budgets using Precedent H, detailing incurred and estimated costs, with phase-specific assumptions.

- Strict deadlines apply for filing budgets; failure can lead to recovery being limited to court fees (CPR 3.14), subject to potential relief from sanctions.

- Parties must discuss budgets and file a Budget Discussion Report (Precedent R).

- The court usually makes a Costs Management Order (CMO) approving estimated costs per phase and may comment on incurred costs.

- Approved budgets guide assessment on the standard basis; departures require a ‘good reason’ (CPR 3.18).

- Budgets can be formally revised using Precedent T only if there is a ‘significant development’, and parties must act promptly.

- Court approval is required for budget variations if not agreed; without timely variation, exceeding budgets is unlikely to be recovered.

- The court may use directions (and rarely costs capping orders) to control disproportionate expenditure and oppressive conduct.

- On the indemnity basis, budgets do not cap recovery but may inform reasonableness; proportionality is not applied.

Key Terms and Concepts

- Proportionality

- Costs Management

- Costs and Case Management Conference (CCMC)

- Costs Budget (Precedent H)

- Incurred Costs

- Estimated Costs

- Budget Discussion Report (Precedent R)

- Costs Management Order (CMO)

- Good Reason (CPR 3.18)

- Significant Development

- Budget Variation (Precedent T)

- Costs Capping Order

- Relief from Sanctions (Denton)

- Costs Assessment and Budgets