Learning Outcomes

This article explains the process of costs management in civil litigation, focusing on Costs Management Orders (CMOs). The role of costs management is situated within the court’s duty to ensure litigation proceeds at proportionate cost. You will understand when costs management applies (and common exceptions), the purpose and content of costs budgets (Precedent H), the obligations to file and exchange budgets and budget discussion reports, and the court’s approach to managing budgets at a costs and case management conference (CCMC). The article also covers how and when budgets can be varied mid-proceedings (Precedent T), what counts as a “significant development,” and the effect of an approved budget at detailed assessment, including what amounts to a “good reason” to depart. You will be able to identify and advise on the sanction for late or non-filing of budgets, apply the Denton relief-from-sanctions framework, and appreciate the strategic impact of budgets on case planning and settlement.

SQE1 Syllabus

For SQE1, you are required to understand costs management in civil litigation, including Costs Management Orders (CMOs) under CPR Part 3 and Practice Direction 3D (which from 6 April 2023 replaced the former PD 3E as the costs-management practice direction; PD 3E now deals with costs capping), with a focus on the following syllabus points:

- The purpose and scope of costs management under CPR Part 3, including common exclusions and specialist list practices.

- The requirements for filing and exchanging costs budgets (Precedent H) and budget discussion reports (Precedent R).

- The specific time limits for filing costs budgets (CPR 3.13) and the need for verification and assumptions.

- The nature and effect of a Costs Management Order (CMO) made by the court (CPR 3.15, 3.18), including treatment of incurred versus estimated costs.

- The significant sanction for failing to file a costs budget on time (CPR 3.14) and how CPR 3.9 relief is approached using the Denton stages.

- The mechanism for budget variations (Precedent T) after significant developments (CPR 3.15A).

- Proportionality as the guiding principle in costs management and assessment (CPR 44.3).

- The interaction between CMOs and costs assessed on the standard versus indemnity basis.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

In which track does costs management primarily apply?

- a) Small claims track

- b) Fast track

- c) Multi-track

- d) All tracks equally

-

What is the usual sanction if a party fails to file a costs budget by the deadline specified in CPR 3.13?

- a) The party must pay the opponent's costs immediately.

- b) The party's budget is treated as comprising only the applicable court fees.

- c) The party's statement of case is automatically struck out.

- d) The party must attend an extra case management conference.

-

What is the primary purpose of a Costs Management Order (CMO)?

- a) To fix the exact amount of costs payable at the end of the case.

- b) To approve or revise the parties' budgeted costs for each phase of the litigation.

- c) To penalise parties for spending too much on legal fees.

- d) To dispense with the need for detailed assessment.

Introduction

Managing the costs of civil litigation is a fundamental aspect of the court's role under the Civil Procedure Rules (CPR). The overriding objective requires cases to be dealt with justly and at proportionate cost (CPR 1.1). Costs management, primarily applicable to multi-track claims, is a key mechanism through which the court actively controls litigation expenditure. This involves parties preparing and exchanging detailed costs budgets, which the court then reviews and manages, often by making a Costs Management Order (CMO). Understanding this process is important for advising clients and ensuring compliance with court requirements.

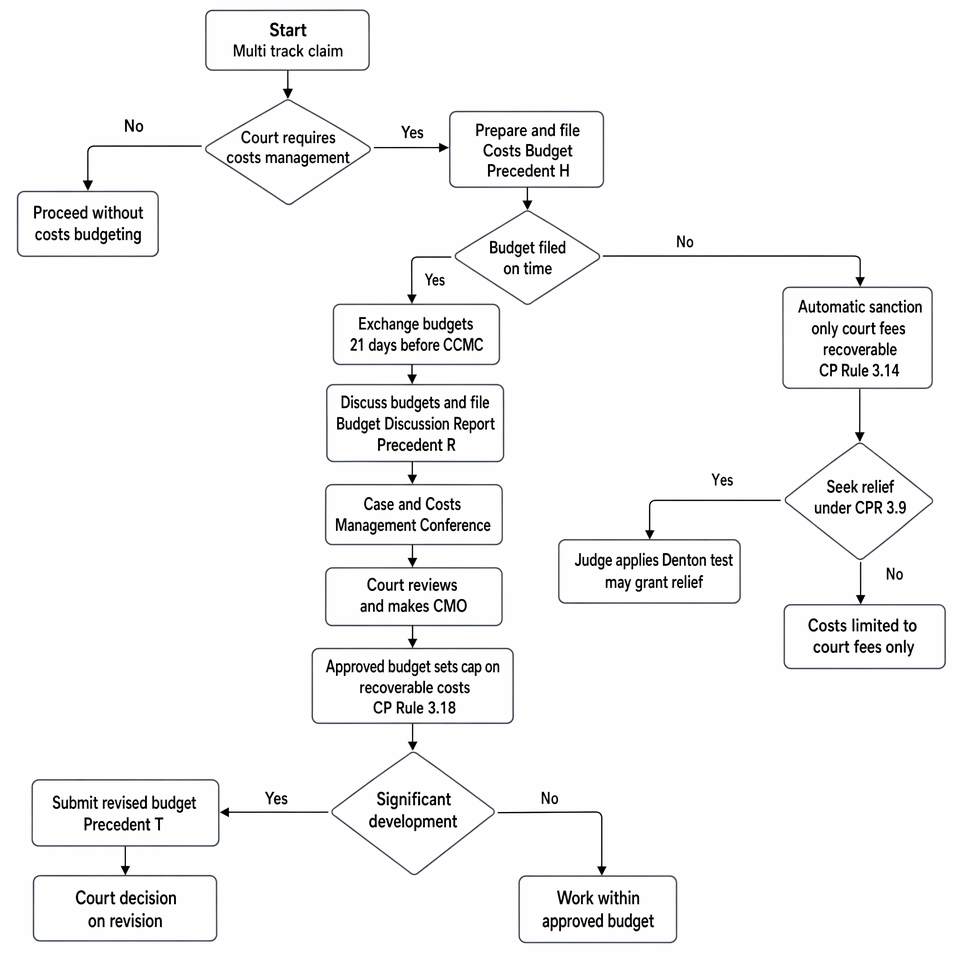

Process for costs management orders in multi-track claims, including budgeting, CCMC approval, revision after significant developments, and CPR 3.14 sanctions.

Costs management applies only where budgets are relevant and useful. Claims governed by fixed recoverable costs (e.g., most fast track and intermediate track claims) are not subject to budgeting. In multi-track cases, however, budgeting is the norm unless an exception applies. Costs management is not a detailed assessment in advance; it sets reasonable and proportionate parameters for future costs and gives greater certainty for recovery on the standard basis if the party is successful.

The Framework for Costs Management

The rules governing costs management are principally found in CPR 3.12 to 3.18 and Practice Direction 3D. The primary aim is to ensure that the costs incurred by parties throughout the litigation process are proportionate to the value, complexity, and importance of the claim.

Under CPR 3.12(1), costs management generally applies to multi-track cases commenced after 22 April 2014 where the amount of money claimed is less than £10 million. The court retains a discretion to apply or disapply budgeting in appropriate cases. In addition, certain specialist lists have different practices (for example, in some commercial cases costs management is commonly disapplied unless ordered). Litigants in person are excluded from the obligation to file budgets unless the court orders otherwise (CPR 3.13).

Key Term: Costs Management

The process by which the court manages both the steps to be taken and the costs to be incurred by the parties to proceedings, primarily in multi-track claims, to ensure proportionality to the issues, value, complexity, and importance of the case.

Costs management is not concerned with detailed scrutiny of individual time entries; rather, it places reasonable and proportionate bounds on future costs by phases (e.g., disclosure, witness evidence, experts, trial preparation, trial). The court may comment on incurred costs (pre-budget) and will take them into account when approving or revising future phases.

Costs Budgets (Precedent H)

Unless the court orders otherwise, all parties (except litigants in person) in cases subject to costs management must file and exchange costs budgets.

Key Term: Costs Budget

A detailed statement estimating the costs (solicitor's fees and disbursements) that a party anticipates incurring for each stage of the litigation process. It must be prepared in the mandatory format and verified.

The required format for a costs budget is Precedent H, as annexed to Practice Direction 3D. It breaks down costs into distinct phases of litigation:

- Pre-action costs

- Issue/Statements of Case

- Case Management Conference (CMC)

- Disclosure

- Witness Statements

- Expert Reports

- Pre-Trial Review (PTR)

- Trial Preparation

- Trial

- ADR/Settlement discussions

- Contingencies (for anticipated but uncertain steps)

The budget distinguishes between incurred costs (up to the date of the budget) and estimated future costs for each phase. Assumptions supporting the estimated costs must be stated with clarity (e.g., number of witnesses, expert disciplines, expected trial length, search methodology for disclosure). Precedent H must be completed in horizontal format, in an easily legible typeface, and verified by a statement of truth signed by a senior legal representative. In cases where a party’s total costs (incurred and estimated) do not exceed £25,000, or the stated value of the claim is less than £50,000, only the first page of Precedent H is used.

Budgeted figures exclude VAT (if applicable), success fees and ATE insurance premiums, the costs of detailed assessment, any appeal, and enforcement costs.

Key Term: Precedent H

The specific mandatory form prescribed by the CPR for presenting a costs budget to the court and other parties, separating incurred and estimated costs and setting out assumptions by phase.

Filing Deadlines (CPR 3.13):

- For claims valued at less than £50,000, the budget must be filed with the directions questionnaire.

- For any other case, the budget must be filed not later than 21 days before the first case management conference (CMC).

Compliance with form and timing is important. A budget should be realistic and based on what is more likely than not to be incurred, supported by reasoned assumptions. Excessive or speculative contingencies should be avoided; genuine contingencies (e.g., an application to amend, a third-party disclosure application) may be included with proper justification.

Budget Discussion Reports (Precedent R):

After exchanging budgets, parties must discuss them and seek agreement. They must then file a budget discussion report, using Precedent R, no later than 7 days before the first CMC. This report details which figures are agreed, which are not agreed, and provides brief reasons for any disagreement. Proper engagement is expected; if one party fails to engage, the court may note that failure when making costs management decisions and in costs orders.

Key Term: Budget Discussion Report

A report (using Precedent R) filed before the CMC, outlining the extent to which parties have agreed or disagreed on the figures presented in each other's costs budgets, with concise reasons for any dispute. Key Term: Costs and Case Management Conference (CCMC)

The hearing (often combined with general case management) at which the court considers directions and reviews parties’ costs budgets, recording agreements and approving or revising disputed budgeted figures.

Costs Management Orders (CMOs)

At the case management conference (often referred to as a Costs and Case Management Conference or CCMC when costs are considered), the court reviews the parties' budgets. The court's role is not to conduct a detailed assessment but to consider whether the budgeted costs fall within a range of reasonable and proportionate costs for each phase, having regard to factors such as the value, complexity, importance, and the parties’ conduct (CPR 44.3 and PD 3D).

The court may then make a Costs Management Order (CMO).

Key Term: Costs Management Order (CMO)

A court order which records the extent to which the parties' budgeted costs are agreed or approved by the court. It manages the recoverable costs for the remainder of the litigation by approving, revising, or capping phase totals.

A CMO will record which parts of the budget are agreed between the parties and, for those parts not agreed, record the court's approval following any revisions made by the judge (CPR 3.15). The court focuses on estimated future costs but may record comments on incurred costs, and will take incurred costs into account when considering the reasonableness and proportionality of subsequent phases (PD 3D, para 7.4). If the court chooses not to make a CMO, PD 44 paras 3.2–3.7 provide guidance at the later assessment stage (e.g., the 20% variance explanation rule and reliance by the paying party on the filed budget figures).

The effect of a CMO is significant. When the court later assesses the costs recoverable by the winning party on the standard basis, it will not depart from the receiving party's last approved or agreed budget unless satisfied that there is a good reason to do so (CPR 3.18). “Good reason” is fact-specific; typical examples include a significant development necessitating additional work where a timely variation application was made, or where the party demonstrably incurred materially less than a phase total due to efficiencies (in which case departure may be downward). Inefficiency, duplication, or an unexplained overspend is unlikely to be a good reason.

Importantly, budgets constrain recovery only on the standard basis. Where costs are awarded on the indemnity basis (e.g., following certain Part 36 outcomes or sanctions for conduct), budgeting constraints do not apply, although the budget may still be a reference point for reasonableness.

Key Term: Good Reason to Depart

A justification at assessment for moving away from an approved/agreed budget figure for a phase, such as a significant development or clear underuse, assessed case-by-case under CPR 3.18.

Worked Example 1.1

Alpha Ltd is suing Beta Ltd in a complex contractual dispute valued at £200,000. Both parties file costs budgets 21 days before the first CCMC. Alpha Ltd's budget estimates £40,000 for the disclosure phase. Beta Ltd's budget estimates £25,000 for disclosure. In their Budget Discussion Report, Beta Ltd disputes Alpha Ltd's disclosure estimate as disproportionate.

At the CCMC, the judge reviews the budgets and the nature of the likely disclosure exercise. The judge considers Alpha Ltd's estimate high given the issues and likely volume of documents.

Answer:

The judge is likely to revise Alpha Ltd's budgeted costs for disclosure downwards when making the Costs Management Order. For example, the judge might approve only £30,000 for Alpha Ltd's disclosure phase, deeming this a more reasonable and proportionate figure. Alpha Ltd will then know that, if successful, they are unlikely to recover more than £30,000 for disclosure costs unless they can later show a good reason for departure.

Consequences of Non-Compliance

The CPR imposes strict consequences for failing to comply with costs management rules. The court expects compliance with both timing and substance, including proper engagement in budget discussions and realistic, justified assumptions.

Failure to File a Budget (CPR 3.14):

The most severe sanction relates to failing to file a costs budget on time.

Key Term: CPR 3.14 Sanction

The rule stating that unless the court orders otherwise, a party failing to file or exchange a costs budget by the deadline will be treated as having filed a budget comprising only the applicable court fees.

This means the defaulting party risks being unable to recover any of their solicitors' fees or disbursements (beyond court fees) from the opponent, even if they win the case and obtain a costs order in their favour. Relief from this sanction can be sought under CPR 3.9, but it is not guaranteed and requires satisfying the court based on the Denton criteria (seriousness/significance of breach, reason for default, and all the circumstances including the need to enforce compliance and conduct litigation efficiently).

Late filing is assessed strictly. Prompt applications for relief, cogent reasons (e.g., genuinely unforeseeable events preventing compliance), and immediate remedial steps are critical. Administrative oversight or workload pressure is unlikely to justify relief. Even where relief is granted, the court may impose conditions or adverse costs.

Worked Example 1.2

Gamma Ltd is suing Delta Ltd. The case is allocated to the multi-track, and budgets are ordered to be filed 21 days before the CCMC scheduled for 1st July. Gamma Ltd's solicitor misses the deadline (9th June) and only files the budget on 20th June. Delta Ltd filed its budget on time.

At the CCMC, Delta Ltd points out Gamma Ltd's late filing.

Answer:

Gamma Ltd is subject to the CPR 3.14 sanction. Their recoverable costs will be limited to court fees unless they successfully apply for relief from sanctions. They would need to make a prompt application under CPR 3.9, explaining the reason for the delay and satisfying the Denton criteria. The court has discretion, but relief is not automatic, especially if no good reason is provided. Budget Revisions (CPR 3.15A):

Once a CMO is made, parties must comply with their approved budgets. If unforeseen "significant developments" occur during the litigation which warrant changes to the budget, the party must promptly revise their budget (using Precedent T) and submit it to the other parties for agreement. If not agreed, the revised budget must be submitted to the court for approval. Failure to do so means the party risks not recovering costs exceeding the originally approved budget.

Significant developments include events such as unexpected third-party disclosure producing many more documents than assumed, permission for additional experts, joinder of parties, or substantial amendments altering the scope of work. Routine evolution of a case, or a party’s late realization of underestimated work, will rarely suffice.

Key Term: Precedent T

The Budget Variation Summary form used to propose and justify revisions to approved budgets after significant developments, to be sent to other parties promptly and then, if not agreed, to the court for approval.

Worked Example 1.3

Epsilon plc obtained a CMO approving £20,000 for the expert reports phase, based on one engineering expert. Midway through proceedings, the court grants the defendant permission to rely on an additional materials expert, and orders concurrent experts’ evidence. Epsilon applies promptly using Precedent T to increase its expert phase budget to £35,000, explaining the additional discipline, joint meetings, and supplemental reports.

Answer:

The court is likely to regard this as a significant development and approve a reasonable upward variation. If Epsilon failed to apply promptly and simply overspent, at detailed assessment it would struggle to show a good reason to depart from the approved figure. Timely use of Precedent T supports recovery aligned to the expanded scope.

Worked Example 1.4

Zeta Ltd’s CMO approved £30,000 for trial preparation. Zeta later spends £42,000 on trial preparation without seeking any variation. At detailed assessment, Zeta argues that intense settlement talks broke down late, necessitating additional work.

Answer:

Without a timely Precedent T variation, Zeta faces an uphill task. The court will only depart for a good reason. Late settlement negotiations are common and often contemplated in the ADR/Settlement phase. Absent evidence of a significant development not reasonably foreseeable at budgeting, departure is unlikely and recovery will generally be limited to £30,000 for that phase.Exam Warning: Remember the strict deadline under CPR 3.13 for filing costs budgets. Missing this deadline triggers the severe sanction under CPR 3.14, limiting recoverable costs to court fees only. Advise clients of the importance of providing timely instructions to allow for budget preparation. Also, be aware that the court's approval of a budget at a CCMC does not guarantee recovery of that amount at detailed assessment; it sets a cap, and costs must still be shown to have been reasonably and proportionately incurred up to that cap. Where costs are awarded on the indemnity basis, budgeting constraints do not apply.

Strategic Importance

Costs management significantly influences how litigation is conducted. Parties must plan strategy within the financial constraints of their likely budget. Decisions regarding the scope of disclosure, the number of witnesses, or the instruction of experts will be heavily influenced by the approved or anticipated budget figures. The transparency provided by exchanged budgets can facilitate settlement discussions, as parties have a clearer picture of potential costs liability.

Budgeting also fosters early case analysis. To produce realistic assumptions, lawyers must identify issues, likely evidence, and reasonable steps. This front-loading often reduces surprises and helps the court tailor directions. Proper engagement in budget discussions demonstrates co-operation under the overriding objective and may lead to agreement on several phases, focusing the CCMC on genuinely disputed items.

If one party acts oppressively by pursuing excessive steps or attempting to drive disproportionate costs, the court can grant appropriate relief to prevent disproportionate expenditure and protect the other party’s position. Maintaining internal monitoring against the approved budget, and seeking Precedent T variation promptly after significant developments, is essential to preserve recovery prospects.

Revision Tip: Focus on the interaction between CPR 3.13 (filing deadlines), CPR 3.14 (sanction for default), CPR 3.15 (CMOs), and CPR 3.18 (effect of CMO on assessment). Understand that proportionality is the guiding principle. Use flowcharts in your revision to map out the process: budget preparation, exchange and Precedent R, CCMC review and CMO, Precedent T variations on significant developments, and assessment with the “good reason to depart” test.

Key Point Checklist

This article has covered the following key knowledge points:

- Costs management aims to control litigation costs, ensuring they are proportionate, primarily in multi-track cases.

- Costs management generally applies to multi-track claims below £10 million, subject to court discretion and specialist list practices.

- Parties (except litigants in person) must file and exchange detailed costs budgets using Precedent H by strict deadlines (CPR 3.13), with clear assumptions and verification.

- Parties should discuss budgets and file a Budget Discussion Report (Precedent R) before the first CCMC.

- The court reviews budgets at a CCMC and may make a Costs Management Order (CMO) approving or revising the budgeted costs for future phases (CPR 3.15).

- The court may comment on incurred costs and will take them into account when assessing proportionality of subsequent phases (PD 3D, para 7.4).

- A CMO provides greater certainty: on the standard basis, the court will generally not depart from the approved budget at assessment unless there is good reason (CPR 3.18).

- Failure to file a budget on time results in a severe sanction under CPR 3.14, limiting recoverable costs to court fees only, unless relief is granted under CPR 3.9 applying Denton.

- Approved budgets can be varied after significant developments using Precedent T; prompt application is required (CPR 3.15A).

- Budgeting constraints do not apply to indemnity basis costs; however, reasonableness still governs.

- Where no CMO is made, PD 44 paras 3.2–3.7 guide assessment, including explanations for a 20% or greater variance.

Key Terms and Concepts

- Costs Management

- Costs Budget

- Precedent H

- Budget Discussion Report

- Costs and Case Management Conference (CCMC)

- Costs Management Order (CMO)

- CPR 3.14 Sanction

- Precedent T

- Good Reason to Depart