Learning Outcomes

This article provides an overview of legal expenses insurance (LEI) as a method for funding legal services. It details the two main types of LEI: before-the-event (BTE) and after-the-event (ATE) insurance. For the SQE1 assessments, you will need to understand the characteristics of BTE and ATE policies, the solicitor's duties when a client has or considers LEI, and the client's right to choose their solicitor under such policies. Your understanding of these subjects will enable you to identify and apply the relevant legal rules and principles to SQE1-style single best answer MCQs.

In addition, you should be clear on the practical steps a firm must take when assisting clients to obtain or use LEI. This includes complying with insurance distribution requirements when arranging or advising on ATE or BTE policies, managing insurer-imposed conditions on case conduct, and recognising the impact of LEI on costs exposure, case strategy, and interactions with other funding options (such as CFAs, DBAs, and legal aid). A solid understanding of merits thresholds, indemnity limits, exclusions, and the client’s freedom to choose a solicitor is essential to advise effectively and avoid professional pitfalls.

SQE1 Syllabus

For SQE1, you are required to understand the practical implications of funding legal services through legal expenses insurance. You may be assessed on your ability to advise a client on the existence and suitability of LEI, the steps required when dealing with insurers, and the impact of LEI on case management and costs. An appreciation of LEI is essential for advising clients effectively on how to finance their legal matters, particularly litigation, with a focus on the following syllabus points:

- The distinction between Before-the-Event (BTE) and After-the-Event (ATE) insurance.

- The solicitor's duty to enquire about and advise on existing BTE policies.

- The client's statutory right to choose their own solicitor under LEI policies.

- The practical implications of policy limits, exclusions, and insurer requirements on case conduct.

- The role of ATE insurance, particularly in conjunction with Conditional Fee Agreements (CFAs) and Damages-Based Agreements (DBAs).

- Compliance with financial services regulation when assisting clients to obtain LEI, including insurance distribution activities and reliance on the s327 Financial Services and Markets Act 2000 (FSMA) exemption.

- The effect of LEI availability on eligibility for civil legal aid (where alternative funding exists, legal aid may be refused).

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which type of legal expenses insurance is commonly found as part of household or motor insurance policies?

- a) After-the-Event (ATE) insurance

- b) Before-the-Event (BTE) insurance

- c) Third-party funding insurance

- d) Conditional Fee Agreement (CFA) insurance

-

Under the Insurance Companies (Legal Expenses Insurance) Regulations 1990, when does a client's right to choose their own solicitor typically arise in LEI-funded matters?

- a) Only if the insurer agrees.

- b) As soon as the claim is notified to the insurer.

- c) Once legal proceedings are initiated or where a conflict of interest arises.

- d) Never, the insurer always appoints the solicitor.

-

What is the primary purpose of After-the-Event (ATE) insurance in civil litigation?

- a) To cover the client's own solicitor's fees if they win.

- b) To cover the client's disbursements and the opponent's costs if the client loses.

- c) To fund the initial investigation of a claim.

- d) To provide cover for claims existing before the policy start date.

Introduction

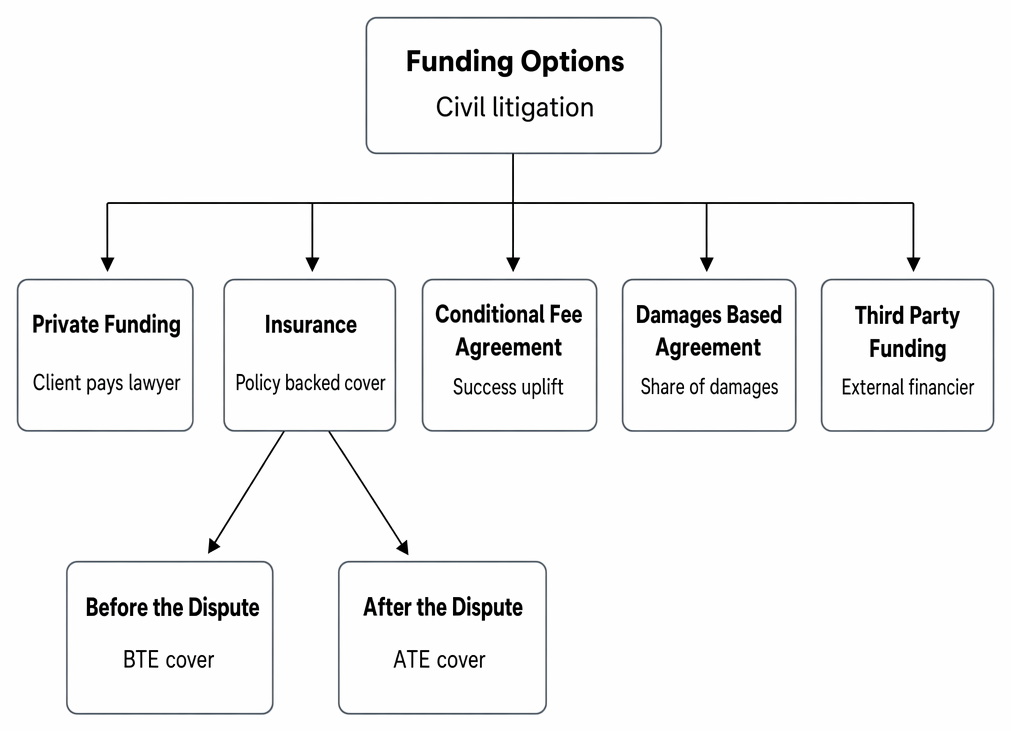

When clients face potential legal action, a primary concern is how to fund the associated costs. Alongside options like private funding, CFAs, and DBAs, legal expenses insurance (LEI) provides a significant source of funding, particularly for individuals and small businesses. LEI policies are designed to cover legal costs incurred in pursuing or defending certain types of legal claims. Understanding the operation of LEI, including the solicitor's duties and the client's rights, is essential for providing comprehensive advice on funding options. This article explores the two main forms of LEI: Before-the-Event (BTE) and After-the-Event (ATE) insurance.

Principal funding methods for civil litigation are presented, with insurance divided into before-the-event and after-the-event legal expenses cover.

LEI interacts with other funding routes in important ways. BTE cover can avoid the need to enter into CFAs/DBAs at all, but may impose panel-solicitor or reporting conditions that shape case strategy. ATE cover is frequently paired with CFAs/DBAs to manage adverse costs and disbursement risk. Where LEI exists, civil legal aid may be unavailable on the basis that the client has alternative funding. Solicitors who arrange, advise on, or assist with LEI must also consider the financial services regulatory framework for insurance distribution activities to avoid unlawful conduct.

Key Term: Before-the-Event insurance (BTE)

Insurance cover purchased before any specific legal dispute arises, typically as an add-on to other insurance policies like home or motor insurance, or sometimes as a standalone policy. It covers potential future legal costs for specified types of disputes.

Before-the-Event (BTE) Insurance

Identifying BTE Cover

A key professional conduct point for solicitors is the duty to enquire at the outset of any contentious matter whether the client has any existing insurance policies that might include BTE cover. This principle was highlighted in Sarwar v Alam [2001] EWCA Civ 1401 (though specific case names are not usually required for SQE1, the principle is essential). Failure to check for BTE could leave a client unnecessarily paying costs that could have been covered by insurance, potentially leading to negligence claims against the solicitor.

Solicitors should advise clients to check documentation for policies such as:

- Home contents/buildings insurance

- Motor insurance

- Specialist standalone LEI policies

- Cover provided through trade union membership or employee benefits schemes.

- Packaged bank accounts or credit card benefits that sometimes include legal advice helplines and limited legal expenses cover.

Request the actual policy schedule and wording rather than relying on summaries. Many policies include legal helplines and “initial advice” services; these can be gateways to formal BTE claims, and failure to notify promptly can jeopardise cover.

Key Term: Prospects of success

A merits threshold commonly used by LEI insurers to determine whether a claim is sufficiently likely to succeed to justify indemnity. Often expressed as a percentage (for example, 51% or 60%) and assessed with reference to evidence and proportionality.

Scope of BTE Cover

BTE policies vary significantly in their scope and limitations. Solicitors must carefully review the policy wording to advise the client accurately. Common features include:

- Types of disputes covered: Policies usually specify the types of legal disputes covered (e.g., personal injury, employment disputes, property disputes, consumer contract issues). Family law matters are often excluded. Business-related disputes may be excluded unless the policy is a business LEI product.

- Indemnity limits: There will be a maximum amount the insurer will pay towards legal costs. Some policies impose per-claim limits, while others include overall annual limits. Costs of counsel and experts may be within or outside limits depending on terms.

Key Term: Indemnity limit

The maximum amount an insurer will pay under the policy for covered legal costs. Limits can be per claim, per policy period, or staged, and may treat disbursements and counsel’s fees differently.

-

Prospects of success: Insurers typically require the claim to have reasonable prospects of success (often defined as more than 50% or 60%) before agreeing to provide cover. They may withdraw cover if prospects diminish or where cost-benefit deteriorates (for example, where likely damages are disproportionate to costs).

-

Exclusions: Policies contain specific exclusions, such as claims arising before the policy inception date, small claims, or disputes with the insurer itself. Small claims track matters (typically up to £10,000) are frequently excluded because adverse costs risk is lower.

-

Notification and cooperation: Policyholders are commonly required to notify the insurer promptly when a dispute arises and to cooperate with the insurer’s requests for information, case updates, and merits assessments (including counsel’s opinions if requested).

-

Panel solicitors: Insurers often maintain panels of preferred law firms. While clients generally have the right to choose their own solicitor (see below), using a panel firm may be more straightforward administratively and may avoid a shortfall if non-panel rates exceed the insurer’s maximum rate.

Key Term: Panel solicitor

A law firm pre-approved by an insurer to act under its LEI scheme, typically agreeing to set hourly rates, reporting protocols, and merit assessments required by the insurer.

Insurers may set reasonable conditions on cover, including:

- Hourly rate caps and cost budgets that require prior authority to exceed.

- Requirements to seek settlement where proportionate to the merits and costs.

- Staged authorization (for example, pre-action, issue of proceedings, trial) tied to merits reassessment and updated budgets.

Key Term: Freedom to choose a solicitor

A right under the Insurance Companies (Legal Expenses Insurance) Regulations 1990 for policyholders to choose their own lawyer once proceedings are initiated, or where a conflict of interest arises, subject to reasonable insurer conditions.

Freedom to Choose a Solicitor

A fundamental right for policyholders under the Insurance Companies (Legal Expenses Insurance) Regulations 1990 (implementing EU Directive 87/344/EEC) is the freedom to choose their own solicitor once legal proceedings have been initiated, or where a conflict of interest arises.

Insurers cannot compel a client to use a solicitor from their panel in these circumstances, although they can propose a panel solicitor. However, insurers can impose reasonable conditions on the chosen solicitor, such as requiring relevant experience or adherence to specified hourly rates or terms of appointment. Before proceedings, many policies legitimately require panel usage for pre-action advice and initial investigation. If a client insists on a non-panel firm before issue, the insurer may decline cover for that phase, though the right to choose arises once proceedings are commenced.

Where the insurer proposes rates lower than a chosen solicitor’s standard rates, the client must be warned about any shortfall they may need to fund privately.

Worked Example 1.1

Fatima is dismissed from her job and believes it was unfair. She consults a solicitor, Aisha. Fatima mentions she has home insurance. Aisha asks to see the policy documents. Upon review, Aisha discovers a BTE legal expenses add-on covering employment disputes up to £50,000, provided prospects of success are assessed by the insurer as over 51%. The insurer has a panel of solicitors but Fatima wants Aisha to act. Proceedings have not yet been issued.

How should Aisha advise Fatima regarding solicitor choice?

Answer:

Aisha should advise Fatima that while the insurer may prefer a panel solicitor, Fatima has the right to choose her own solicitor once proceedings are issued. Before proceedings, the insurer might legitimately require a panel firm to handle pre-action steps. Aisha should explain that if Fatima insists on using Aisha before proceedings, the insurer might refuse cover for that stage. Aisha should also clarify if her fees align with the insurer's approved rates, as Fatima might face a shortfall if Aisha charges more. They should first notify the insurer and seek confirmation of cover based on prospects.

Worked Example 1.2

Luca has BTE cover under his motor policy. After a collision, he wishes to pursue a claim worth about £6,000 for vehicle damage. His policy excludes “small claims” and requires notification within 30 days of the incident. He contacts a solicitor four months later.

Can Luca rely on his BTE cover now?

Answer:

The claim value suggests it will likely be allocated to the small claims track, which many BTE policies exclude. In addition, delayed notification beyond the policy’s time limit can justify refusal of cover. A solicitor should review the exclusions and notification terms; if the small claims exclusion and time limit apply, BTE is unlikely to respond. The solicitor should explain alternative funding approaches, including private funding and potential cost recovery limits on the small claims track.

After-the-Event (ATE) Insurance

Key Term: After-the-Event insurance (ATE)

Insurance cover purchased after a specific legal dispute has arisen. It primarily covers the risk of having to pay the opponent's legal costs and potentially the client's own disbursements if the claim is unsuccessful.

Purpose and Use of ATE

ATE insurance is most commonly used in civil litigation, particularly in personal injury and clinical negligence claims, often alongside Conditional Fee Agreements (CFAs) or Damages-Based Agreements (DBAs). Since CFAs and DBAs typically mean the client does not pay their own solicitor's fees if they lose, the main financial risks remaining are their own disbursements (e.g., court fees, expert report fees) and liability for the opponent's costs. ATE insurance is designed to cover these specific risks.

A practical consideration is the recoverability of premiums. Since the LASPO 2012 reforms, ATE premiums are generally not recoverable from the losing opponent, with exceptions in narrowly defined categories (for example, the cost of expert reports in clinical negligence claims). Most ATE premiums are therefore payable by the client, often structured so payment is deferred to the end of the case and deducted from damages on success, or staged to reflect increasing risk and cost as the case progresses.

Obtaining ATE Cover

- Timing: ATE is taken out after the dispute has arisen but ideally as early as possible in the proceedings. Late placement may result in higher premiums or refusals where the adverse costs risk has already crystallised (for example, after a Part 36 offer has been rejected).

- Assessment: Insurers will assess the merits of the case before offering cover, usually requiring strong prospects of success (often 60% or higher). Some insurers require an independent counsel’s opinion for complex claims.

- Premiums: ATE premiums can be substantial, reflecting the known risk of the existing dispute. Premiums may be staged (increasing towards trial) or deferred until the conclusion of the case. Insurers may offer “self-insured” arrangements, where the premium is waived or reduced if the client loses, but deducted from damages if successful.

Key Term: Insurance distribution activity

Activities such as advising on, proposing, arranging, or assisting in the administration and performance of insurance contracts. Assisting a client to obtain ATE or BTE insurance is an insurance distribution activity and engages FSMA/RAO requirements.

When arranging ATE, a firm will be engaging in insurance distribution activities under the Financial Services and Markets Act 2000 regime and the Regulated Activities Order 2001. Firms typically rely on the designated professional body exemption in s327 FSMA to lawfully carry on these activities as incidental to legal services. Firms must notify the SRA that they carry out insurance distribution, be placed on the relevant register, and appoint an insurance distribution officer to oversee compliance. Where the activity cannot rely on the exemption, FCA authorisation would be required.

Scope of Cover

ATE policies typically cover:

- Adverse costs: The opponent's legal costs and disbursements if the client is ordered to pay them on losing.

- The client's own disbursements: Court fees, expert fees, and other disbursements incurred during the case.

Cover for the client's own solicitor's fees is less common under ATE, as these are often covered by a CFA or DBA, but bespoke policies exist. Exclusions can include fraud or dishonesty, failure to cooperate with the insurer, significant changes in prospects of success that are not reported, and costs incurred without the insurer’s prior approval where required.

ATE terms often require:

- Prior authority for certain steps (for example, instructing experts or issuing proceedings).

- Regular updates to merits and budgets.

- Prompt notification of significant case developments, such as offers, new evidence, or adverse rulings.

Worked Example 1.3

David is pursuing a professional negligence claim against his former architect under a Conditional Fee Agreement (CFA) with his solicitor. The CFA means David won't pay his solicitor's fees if he loses. However, David is concerned about having to pay the architect's legal costs (estimated at £40,000) and his own disbursements (expert reports costing £10,000) if his claim fails.

What funding option could mitigate these risks for David?

Answer:

David's solicitor should advise him about obtaining After-the-Event (ATE) insurance. An ATE policy could cover his liability for the opponent's costs (£40,000) and his own disbursements (£10,000) should he lose the case. Obtaining the policy would depend on an insurer assessing the claim as having sufficient prospects of success. The premium would likely be significant and payable by David, potentially deferred and paid from damages if he wins.

Worked Example 1.4

A firm acting in a clinical negligence case on a CFA wishes to arrange ATE cover for the client. The solicitor plans to recommend a specific ATE product and introduce the client to the insurer.

What regulatory steps must the firm consider when arranging the policy?

Answer:

Assisting the client to obtain ATE is an insurance distribution activity. The firm should ensure it relies on the s327 FSMA exemption (activities must be incidental to legal services and to the client’s matter), notify the SRA that it undertakes insurance distribution, be registered accordingly, and appoint an insurance distribution officer to oversee compliance. The solicitor should provide fair, clear, and non-misleading information about the product, consider conflicts, and keep an audit trail of advice and the client’s informed choice. If the activity cannot rely on the exemption, FCA authorisation would be required.Exam Warning: Be clear on the distinction between BTE and ATE insurance. BTE is 'before the event' cover for potential future disputes, often part of other policies. ATE is 'after the event' cover for an existing dispute, typically covering adverse costs and disbursements, and often used with CFAs/DBAs. Understand what each type typically covers and when they are relevant. Where a firm assists a client in obtaining LEI, treat that as an insurance distribution activity and ensure compliance with FSMA/RAO requirements or exemptions.

Solicitor Duties and Practicalities

Regardless of the type of LEI, solicitors have ongoing duties:

-

Advising on suitability: Discuss whether the LEI policy offers adequate cover for the likely costs and risks of the specific case. Consider indemnity limits, track allocation (small claims exclusions), prospects thresholds, staged approvals, and any rate caps that might create shortfalls.

-

Transparency: Clearly explain the policy terms, indemnity limits, deductibles (excess), conditions, and exclusions to the client. Advise on the potential for insurer withdrawals if prospects change and the implications of not following insurer protocols.

-

Insurer relations: Liaising with the insurer, providing necessary updates, seeking authority for specific steps (if required by the policy), and managing costs within policy limits. Record communications, approvals, and reporting obligations. If the insurer seeks to direct litigation strategy contrary to the client’s best interests or the overriding objective, the solicitor must balance duties to the court and to the client, and raise concerns with the insurer.

-

Client choice: Advising the client on their right to choose a solicitor and the implications of selecting a non-panel firm. Explain the timing of the right (once proceedings commence, or if a conflict arises) and the risk of shortfalls where non-panel rates exceed insurer caps.

-

Costs management: Ensuring work undertaken is reasonable and proportionate, especially given policy limits. Unreasonable costs may not be recoverable from the insurer, even if within the indemnity limit. Cost budgets should reflect the policy cap to avoid unrecoverable excess.

-

Legal aid interaction: Where the client’s case might otherwise be eligible for legal aid, advise that the Legal Aid Agency may refuse funding if LEI is available. At the outset, determine whether LEI or other alternative funding exists before directing the client towards legal aid.

-

Insurance distribution compliance: Assisting a client to obtain ATE/BTE involves insurance distribution activities. Firms should:

- Rely on the s327 FSMA exemption (ensuring the activity is incidental to legal services and the particular matter).

- Notify the SRA they carry out insurance distribution, be placed on the appropriate register, and appoint an insurance distribution officer.

- Provide appropriate disclosures, keep records, and avoid conflicts (for example, where the firm benefits from a particular insurer relationship).

Key Term: Insurance Companies (Legal Expenses Insurance) Regulations 1990

UK regulations that, among other things, protect the policyholder’s freedom to choose a lawyer once proceedings are issued or where a conflict exists, subject to reasonable conditions set by insurers.

Confidentiality and consent are especially relevant where insurers request access to the client’s file for merits assessments. The solicitor should obtain the client’s informed consent before sharing information and ensure disclosure complies with confidentiality obligations.

Worked Example 1.5

A BTE insurer approves cover for a consumer contract dispute up to £25,000 and requires a panel firm, monthly reporting, and a rate cap of £180/hour. The client prefers a non-panel solicitor charging £250/hour. Proceedings have now been issued.

How should the chosen solicitor manage the retainer and insurer engagement?

Answer:

The client’s right to choose a solicitor applies once proceedings are issued, but the insurer can impose reasonable conditions, including rate caps and reporting. The solicitor should advise the client of any shortfall risk and, if instructed, accept the matter at the insurer’s capped rate or agree how any excess will be privately funded. The firm should obtain the insurer’s written confirmation of cover, comply with reporting and authority requirements, and keep costs proportionate to the indemnity limit to avoid unrecoverable spend.Revision Tip: When advising a client with potential LEI, always obtain a copy of the full policy schedule and wording. Do not rely solely on the client's recollection or summary documents. Check the indemnity limit, the excess, any specific conditions relating to reporting or solicitor choice, and key exclusions.

Key Point Checklist

This article has covered the following key knowledge points:

- Legal Expenses Insurance (LEI) helps clients fund legal costs.

- Before-the-Event (BTE) insurance is purchased before a dispute arises, often with home/motor policies. Solicitors must check for existing BTE cover at the outset of a contentious matter.

- BTE policies feature indemnity limits, prospects-of-success thresholds, exclusions (commonly small claims), notification requirements, and panel-solicitor arrangements.

- Clients generally have the right to choose their own solicitor under LEI once proceedings commence or if a conflict arises, though insurers may set reasonable conditions (e.g., on fees, experience, reporting).

- After-the-Event (ATE) insurance is purchased after a dispute arises, primarily covering opponent's costs and own disbursements if the client loses. It's often used with CFAs/DBAs.

- ATE premiums are generally not recoverable from the losing party since LASPO 2012, subject to limited exceptions (e.g., some clinical negligence expert report costs).

- Assisting a client to obtain LEI engages insurance distribution activities under FSMA/RAO. Firms typically rely on the s327 exemption, must notify the SRA, be appropriately registered, and appoint an insurance distribution officer.

- Effective case management under LEI requires adherence to insurer protocols, proportionate costs within indemnity limits, and clear client advice on shortfalls and conditions.

- Availability of LEI may impact eligibility for civil legal aid.

Key Terms and Concepts

- Before-the-Event insurance (BTE)

- After-the-Event insurance (ATE)

- Prospects of success

- Indemnity limit

- Panel solicitor

- Freedom to choose a solicitor

- Insurance Companies (Legal Expenses Insurance) Regulations 1990

- Insurance distribution activity