Learning Outcomes

This article outlines claims under the Inheritance (Provision for Family and Dependants) Act 1975 and their impact on estate distribution, including:

- identifying who qualifies as an applicant under the Act and how exam questions might test borderline categories such as cohabitants and adult children

- distinguishing the two standards of reasonable financial provision (spousal standard and maintenance standard) and applying them to short problem scenarios

- analysing the statutory section 3 factors guiding the court’s discretion and weighing competing needs of applicants and beneficiaries

- explaining how successful claims alter testamentary or intestacy distributions and how the court structures lump sum, periodical payment, and property adjustment orders

- assessing the treatment of assets passing outside the estate (for example, joint tenancies, nominations and life policies) and the limits of the court’s powers over them

- understanding the inheritance tax consequences of “writing back” and how court orders can increase or reduce available IHT reliefs

- evaluating the practical duties, protections and risks affecting personal representatives and beneficiaries where a claim is threatened or issued

- practising SQE1-style analysis through typical MCQ and single-best-answer patterns, focusing on time limits, procedure and common traps in exam fact patterns

SQE1 Syllabus

For SQE1, you are required to understand the effect of claims under the Inheritance (Provision for Family and Dependants) Act 1975 on the distribution of estates, with a focus on the following syllabus points:

- the categories of people who may apply for financial provision from an estate under the Act

- the legal standards for "reasonable financial provision" and how they differ for spouses/civil partners and other applicants

- the factors the court must consider when deciding whether to make an order and what type of order to make

- the types of orders the court can make and their practical effect on estate distribution

- the time limits and procedural requirements for bringing a claim

- the practical consequences for personal representatives and beneficiaries

- the IHT implications of court orders (including the “writing back” rule) and how provision interacts with assets passing outside the estate

- the court’s powers to address transactions intended to defeat claims, variation of nuptial settlements, and variation of trusts on which the estate is held

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- Who is eligible to bring a claim under the Inheritance (Provision for Family and Dependants) Act 1975?

- What is the difference between the "maintenance standard" and the "spousal standard" for reasonable financial provision?

- Name three factors the court must consider when deciding whether to make an order under the Act.

- What is the usual time limit for bringing a claim under the Act, and can it be extended?

- How can a successful claim under the Act affect the distribution of an estate under a will or intestacy?

Introduction

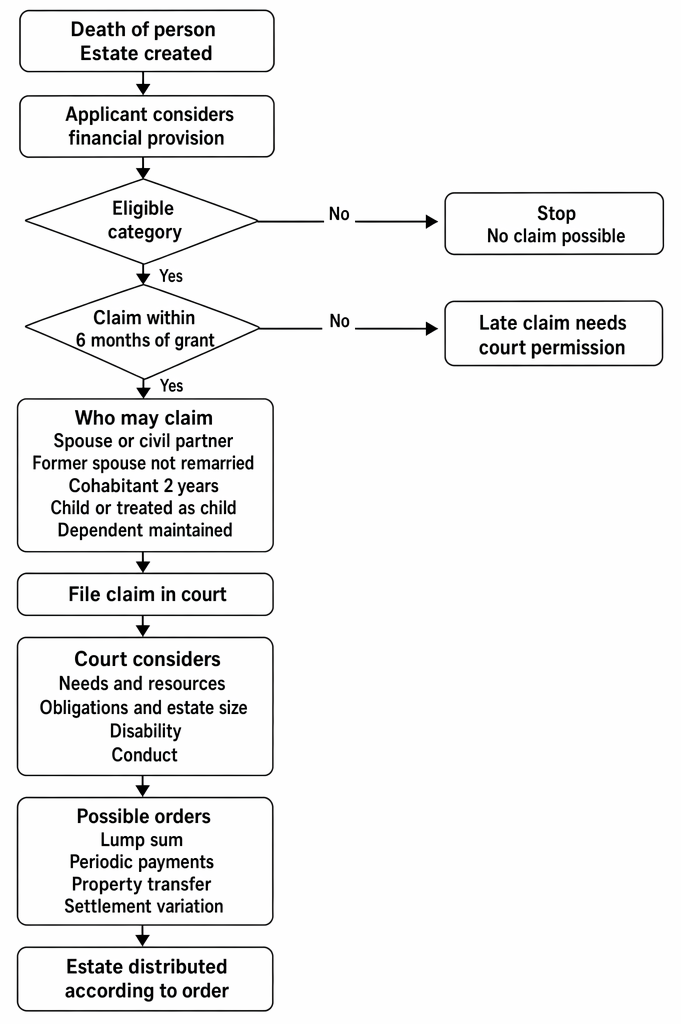

The Inheritance (Provision for Family and Dependants) Act 1975 ("the Act") allows certain people to apply to the court for financial provision from a deceased person's estate if the will or intestacy rules do not make reasonable provision for them. This can change the way an estate is distributed, even if the deceased left a valid will. For SQE1, you must know who can claim, what the court considers, and how such claims can alter the intended distribution of assets.

The Inheritance (Provision for Family and Dependants) Act 1975 claim process is presented through eligibility, limitation, judicial factors, and possible orders.

The court’s powers are wide. It may order lump sums, periodical payments, transfers or settlements of property, the acquisition of property for an applicant, and for spouses/civil partners, variation of ante- or post-nuptial settlements. Since 2014, the court may also vary the trusts on which the estate is held. Practically, this means personal representatives (PRs) must manage estates anticipating potential claims, delaying distribution where appropriate, and ensuring compliance if orders are made. A successful order is treated as if the estate had been disposed of according to the order from the date of death, which can also affect inheritance tax (IHT) calculations.

Key Term: applicant

A person in one of the categories above who is entitled to apply for financial provision from the estate under the Act.

Who Can Claim?

Only people in specific categories can apply for financial provision under the Act. These are:

- the deceased's spouse or civil partner at the time of death

- a former spouse or civil partner who has not remarried or entered a new civil partnership (unless barred by a court order)

- a person who lived with the deceased as spouse or civil partner in the same household for at least two years immediately before death

- a child of the deceased (including adult children)

- a person treated by the deceased as a child of the family (such as a stepchild)

- any person who was being wholly or partly maintained by the deceased immediately before death

Important clarifications for SQE1:

- Former spouses/civil partners: if the family court has made a “clean break” financial order expressly barring claims under the Act, they may be prevented from applying. If not barred, they qualify but the maintenance standard applies.

- Cohabitants: the two-year requirement must be immediately before death and the relationship must be akin to marriage/civil partnership in substance. The maintenance standard applies.

- Child of the family: includes those treated by the deceased as a child of the family in relation to the marriage/civil partnership (commonly stepchildren), even if not biologically related. Needs-based analysis applies.

- Maintained persons: maintenance means financial provision which was in fact made (wholly or partly) for the person’s reasonable needs immediately before death. The court examines the reality of support, not just formal obligations.

Key Term: reasonable financial provision

The amount or type of provision the court considers fair for the applicant, applying the relevant standard under the Act.

What Is "Reasonable Financial Provision"?

The Act sets out two standards for what counts as "reasonable financial provision":

- For spouses and civil partners, the standard is what would be reasonable in all the circumstances, whether or not required for their maintenance. The court may consider what the applicant would have received on divorce.

- For all other applicants, the standard is what would be reasonable for their maintenance only.

The spousal/civil partner standard is deliberately wider. It permits capital provision beyond bare subsistence to reflect fairness having regard to the marriage/civil partnership, contributions to family welfare, and the likely financial settlement on marital/civil breakdown. In contrast, the maintenance standard focuses on the cost of everyday living appropriate to the applicant’s circumstances, not a redistribution of wealth.

The Supreme Court in Ilott v Blue Cross [2017] confirmed that “maintenance” does not extend to everything desirable. Claims by independent adult children require careful scrutiny; absent special circumstances, adult children with adequate means will not generally receive awards. However, the court will consider moral claims alongside need, estrangement, and the deceased’s recorded reasons.

Key Term: maintenance standard

The standard applied to all applicants except spouses/civil partners: provision for their maintenance only. Key Term: spousal standard

The standard applied to spouses/civil partners: provision as would be reasonable in all the circumstances, not limited to maintenance.

What Does the Court Consider?

The court must weigh up all the circumstances of the case. Section 3 of the Act lists the factors the court must consider, including:

- the financial resources and needs (now and in the foreseeable future) of the applicant

- the financial resources and needs of any other applicant and any beneficiary

- any obligations and responsibilities the deceased had towards the applicant or any beneficiary

- the size and nature of the estate

- any physical or mental disability of the applicant or any beneficiary

- any other relevant matter, including the conduct of any person

For spouses/civil partners, the court also considers the applicant's age, the duration of the marriage/civil partnership, and their contribution to the family.

Expanded points for SQE1:

- Financial resources and needs include current and likely future income, capital, earning capacity, and liabilities. The court may take into account the impact of orders on means-tested state benefits (for example, avoiding awards that would merely replace benefits).

- Obligations extend beyond strict legal duties; the court may reflect moral obligations in its assessment, such as promises or understandings regarding family property.

- The size and nature of the estate is critical; where the estate is small, awards may be limited or refused to avoid disproportionate costs (as illustrated in cases where widows’ needs prevail over adult children’s modest claims).

- Conduct is relevant but usually carries limited weight unless extreme (for example, serious misconduct or unlawful killing—while entitlement under a will would be forfeit, a dependent could theoretically still bring a needs-based claim).

Time Limits and Procedure

A claim must normally be brought within six months of the grant of probate or letters of administration. The court has discretion to allow late applications, but this is rare and only with good reason.

Applications are typically commenced under CPR Part 8 and must be served on the PRs and relevant beneficiaries. PRs should avoid distributing the estate within the six-month window or if they have notice of a potential claim. Although PRs have statutory protection if they distribute after six months without notice, the court may require beneficiaries to restore funds or bear the burden of an order made later.

Re Salmon [1981] illustrates the strict approach to extensions: the widow’s late claim failed where her solicitor had missed the deadline and the estate had already been distributed. The court expects prompt action when a claim is contemplated, and where delay is attributable to advisors, negligence remedies may be the appropriate recourse.

Key Term: grant of representation

The legal document (probate or letters of administration) giving authority to deal with the estate.

Types of Orders the Court Can Make

If the court finds that reasonable financial provision has not been made, it can make a wide range of orders, including:

- payment of a lump sum

- regular (periodical) payments

- transfer of specific property to the applicant

- settlement of property for the applicant's benefit

- acquisition of property for the applicant

- variation of ante-nuptial or post-nuptial settlements (for spouses/civil partners)

The court can also make interim orders for urgent financial support while the claim is pending.

Additional points:

- Lump sum and transfer/settlement/acquisition orders, once made, cannot be varied. Periodical payments orders can be varied or discharged if circumstances change (for example, upon the applicant’s re-partnering or altered needs).

- Settlement of property is common for minors or vulnerable adults; the terms should align with trust and tax rules (for example, creating a bereaved minor/young person’s interest or an immediate post-death interest (IPDI) where appropriate).

- Variation of nuptial settlements can adjust ongoing family arrangements to secure fair provision for a surviving spouse/civil partner or children of the marriage/civil partnership. The court examines the settlement’s scope and beneficiaries.

- Variation of trusts on which the deceased’s estate is held enables direct adjustment of will/intestacy trusts to achieve fair provision without creating replacement structures.

- Where the deceased entered into transactions intended to defeat claims within six years prior to death, the court may set aside or bring back value into the estate for provision, if the necessary statutory tests are met.

Key Term: interim order

A temporary order for financial support made pending final determination of the claim. Key Term: nuptial settlement

An arrangement making continuing provision for one or both spouses/civil partners qua spouse/civil partner, which the court may vary for provision under the Act. Key Term: estate

All the property, money, and assets owned by the deceased at death, available for distribution.

Impact on Estate Distribution

A successful claim under the Act can change how the estate is distributed, overriding the terms of the will or the intestacy rules. The court's order takes priority, and the personal representatives must distribute the estate in accordance with the order. This may reduce the share of other beneficiaries.

The order is treated as if it had always governed the disposition from the date of death. This “writing back” principle applies for IHT purposes: the estate is taxed as if the court-ordered pattern of disposition had been in the original will/intestacy (for example, increasing spouse exemption where provision is made for a surviving spouse/civil partner, or reducing it if spousal provision is decreased). The court also has power to direct how the burden of an order falls between beneficiaries to secure fairness; “beneficiary” here includes, for burden allocation purposes, a person who took by survivorship, nomination, or donatio mortis causa.

Two practical limits are important:

- Property passing outside the estate (for example, a house passing by survivorship to a joint tenant) is generally outside the PRs’ control. The court cannot rewrite survivorship, but it may direct how the burden of an order is borne and can use estate funds to acquire property for an applicant if justified.

- Transactions intended to defeat claims can be scrutinised and unwound under the Act where statutory conditions are met, bringing assets (or their value) effectively back into play for provision.

For PRs, the presence or likelihood of a claim should inform estate administration:

- avoid distributing within six months of the grant or where notice of a claim exists

- seek directions where competing claims exist or estate assets are illiquid

- consider advertising under Trustee Act 1925 section 27 for creditor protection and ensure timely payment of tax to secure the grant

- anticipate how a court order would impact abatement, appropriation, and any arrangements involving the matrimonial home

Worked Example 1.1

Scenario: Maya dies leaving a will giving her entire estate to her brother. She is survived by her long-term partner, Sam, who lived with her for three years before her death. Sam was financially dependent on Maya but is left nothing in the will.

Question: Can Sam bring a claim under the Act, and how might this affect the estate distribution?

Answer:

Yes. Sam qualifies as an applicant (as a cohabitant living with the deceased for at least two years). If the court finds that reasonable financial provision was not made for Sam, it may order a lump sum or other provision for him from the estate. The brother's share will be reduced accordingly.

Worked Example 1.2

Scenario: James dies intestate, survived by his wife and two adult children. His will left everything to his wife, but after divorce he did not make a new will. The estate passes under the intestacy rules. One child, Anna, is disabled and financially dependent on James. Anna receives only a small share under intestacy.

Question: Can Anna claim more from the estate?

Answer:

Yes. Anna is a child of the deceased and can apply for reasonable financial provision. The court will consider her needs and may order additional provision for her, reducing the shares of the other beneficiaries.

Worked Example 1.3

Scenario: Leila dies leaving a modest estate of £180,000 to charity. She was married for 25 years to Omar, who supported the family while Leila cared for their children. Omar receives nothing under the will.

Question: How will the spousal standard affect an application by Omar?

Answer:

As a surviving spouse, Omar’s claim is assessed by the spousal standard (not limited to maintenance). The court will consider contributory factors (duration of marriage, family contributions) and what Omar might have received on divorce. Even if the estate is modest, the court can order a lump sum or transfer of property. The charity’s gift will be reduced to fund the award.

Worked Example 1.4

Scenario: A former spouse, Priya, was divorced from Arun ten years ago. The financial settlement contained an order that neither party would bring any further claims against the other’s estate. Arun dies, leaving his estate to his brother.

Question: Can Priya claim under the Act?

Answer:

Likely no. A properly made “clean break” order barring claims under the Act usually prevents an application by a former spouse/civil partner. Without such a bar, a former spouse could apply, but would be confined to the maintenance standard.

Worked Example 1.5

Scenario: Six months before death, Ben transferred his sole home to his son for £1. The will leaves everything to Ben’s new partner, Noor, who cohabited with him for three years.

Question: What can the court do if Ben’s transfer was intended to defeat Noor’s claim?

Answer:

If the court finds the transfer was intended to defeat claims and the statutory conditions are met, it may set aside the disposition or treat the property’s value as available for provision. Noor can then obtain provision (for example, a lump sum or acquisition order using estate funds) that would otherwise have been frustrated.

Worked Example 1.6

Scenario: Hugh dies with a life interest trust under his will for his widow, Sarah, remainder to their children. The residuary estate is small. Sarah seeks variation of the trust to increase her immediate provision.

Question: Can the court vary the trusts on which the estate is held?

Answer:

Yes. The court may vary the trusts on which the deceased’s estate is held to secure reasonable financial provision for an eligible applicant. It could, for example, convert or restructure the interests to increase Sarah’s income or capital provision, while balancing fairness to the remainder beneficiaries.Exam Warning: For SQE1, remember that adult children can claim under the Act, but the court will not automatically make provision unless there is a real need for maintenance or special circumstances. The court balances the needs of all applicants and beneficiaries.

Revision Tip: When answering MCQs, check the applicant's relationship to the deceased, their financial needs, and whether the claim is within the time limit. Apply the correct standard for reasonable provision.

Independently of claims under the 1975 Act, the beneficiaries of an estate may alter the distribution of assets by post-death variation, disclaimer, or precatory trust. These mechanisms operate outside the court's jurisdiction under the Act and are governed by different rules.

A post-death variation is a written instrument by which an original beneficiary redirects all or part of their inheritance to another person. Variations may be made in respect of the whole or part of an inheritance, and the original beneficiary is free to determine who receives the varied entitlement. However, minors or persons lacking mental capacity cannot make a variation. There is no limit to the number of times a will can be varied, but each asset can only be varied once. Certain property cannot be varied: this includes property in respect of which the deceased was a life tenant immediately before death, and gifts made during lifetime without reservation of benefit. If the statutory conditions are met and the variation is made within two years of death, it is treated for IHT purposes as if the revised disposition had been made by the deceased, which can create significant tax-planning opportunities.

A disclaimer is a refusal to accept property left by will or on intestacy. A disclaimer can only be made before the beneficiary has accepted the inheritance, and the beneficiary must disclaim the whole gift (partial disclaimer is not possible). Where a gift is disclaimed, the inheritance passes as if the gift had failed—typically falling into residue or passing on intestacy. Unlike a variation, a disclaimer cannot redirect the gift to a specific person.

A precatory trust arises where a gift is made to a beneficiary by will with a wish expressed as to how the beneficiary should pass on those assets to others, commonly through a letter of wishes. The subject matter of the gift must be certain for the precatory trust to operate. No written election is necessary for the beneficiary to comply with the wish. Precatory trusts allow flexibility with regard to gifts of chattels, as the testator may change their mind and update the letter of wishes without amending the will itself.

Summary

| Applicant Type | Standard Applied | Court Powers | Impact on Distribution |

|---|---|---|---|

| Spouse/civil partner | Spousal standard (not limited to maintenance) | Lump sum, periodical payments, property transfer, settlement, variation of settlements | May significantly alter shares of other beneficiaries |

| Other applicants | Maintenance standard | Lump sum, periodical payments, property transfer, settlement | Provision limited to maintenance; may reduce other shares |

Key Point Checklist

This article has covered the following key knowledge points:

- The Act allows certain categories of people to claim financial provision from an estate if reasonable provision is not made.

- The court applies different standards for spouses/civil partners and other applicants.

- The court considers the applicant's and beneficiaries' financial needs, the size of the estate, and other relevant factors.

- Orders can include lump sums, regular payments, transfers or settlements of property, acquisition of property, and (for spouses/civil partners) variation of nuptial settlements; trusts on which the estate is held can also be varied.

- Periodical payments orders can be varied; lump sum, transfer, settlement, and acquisition orders cannot be varied.

- Transactions intended to defeat claims can be scrutinised and unwound where statutory conditions are satisfied.

- Claims must usually be brought within six months of the grant of representation; extensions are discretionary and rare, especially if the estate has been distributed.

- Successful claims “write back” to the date of death for IHT purposes, altering the tax position to reflect the court’s order.

- Personal representatives must comply with any court order, even if it overrides the will or intestacy, and should avoid premature distribution where claims may be brought.

Key Terms and Concepts

- applicant

- reasonable financial provision

- maintenance standard

- spousal standard

- grant of representation

- interim order

- nuptial settlement

- estate