Learning Outcomes

After reviewing this article, you will be able to explain how exchange rates are determined and the theoretical basis of parity relationships. You will understand how to forecast future exchange rates using parity models, distinguish between types of parity, and discuss the practical limitations of these forecasting approaches. You should be able to apply these principles to ACCA exam scenarios and highlight common issues and exam pitfalls.

ACCA Advanced Financial Management (AFM) Syllabus

For ACCA Advanced Financial Management (AFM), you are required to understand both the theory and practicalities of exchange rate behavior and forecasting. This article addresses the following:

- Explain exchange rate determination and the concept of currency parity

- Distinguish between Purchasing Power Parity (PPP) and Interest Rate Parity (IRP)

- Calculate and apply parity-based exchange rate forecasts

- Discuss the limitations of parity models in real-world forecasting

- Recognise the practical challenges facing multinational organisations regarding currency forecasting

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which parity theory suggests that the expected change in a currency’s exchange rate is driven by inflation differentials?

- a) Interest Rate Parity

- b) Purchasing Power Parity

- c) Real Interest Parity

- d) Covered Interest Parity

-

True or false? If Interest Rate Parity holds, arbitrage opportunities exist resulting from differences in interest rates between two countries.

-

A UK-based company needs to forecast the USD/GBP spot rate for one year ahead. Given current spot USD/GBP = 1.2000, UK expected inflation = 4%, US expected inflation = 2%, use the PPP formula to estimate the future spot rate.

-

List two practical reasons why real-world exchange rates may not strictly follow parity relationships.

Introduction

Exchange rates fluctuate as a result of international trade, capital flows, and macroeconomic factors. Accurate forecasting is essential for financial managers managing overseas investments and risks. Parity relationships, such as Purchasing Power Parity (PPP) and Interest Rate Parity (IRP), provide a theoretical framework for understanding and predicting exchange rate movements. However, practical forecasting involves challenges, and real-world deviations from parity are common. This article reviews key parity models, demonstrates their application, and highlights their limitations for ACCA AFM candidates.

EXCHANGE RATE PARITY: CONCEPTS AND FORMULAS

Understanding why exchange rates move is an essential skill for ACCA AFM. Parity models offer guidance by linking exchange rates to inflation and interest rate differentials.

Forecasting framework links forward-rate requirements to IRP, longer horizons with inflation data to PPP, and validates quotation direction and timing.

Key Term: Exchange Rate Parity

The principle that the value of one currency relative to another is governed by economic variables, most notably inflation and/or interest rates.

Purchasing Power Parity (PPP)

PPP suggests that identical goods should have the same price in different countries, once prices are expressed in a common currency. The “law of one price” supports the view that exchange rates adjust to offset inflation differentials.

Key Term: Purchasing Power Parity (PPP)

A theory stating that the rate of exchange between two currencies adjusts so that a basket of goods costs the same in each country after exchange rate changes, reflecting relative inflation rates.

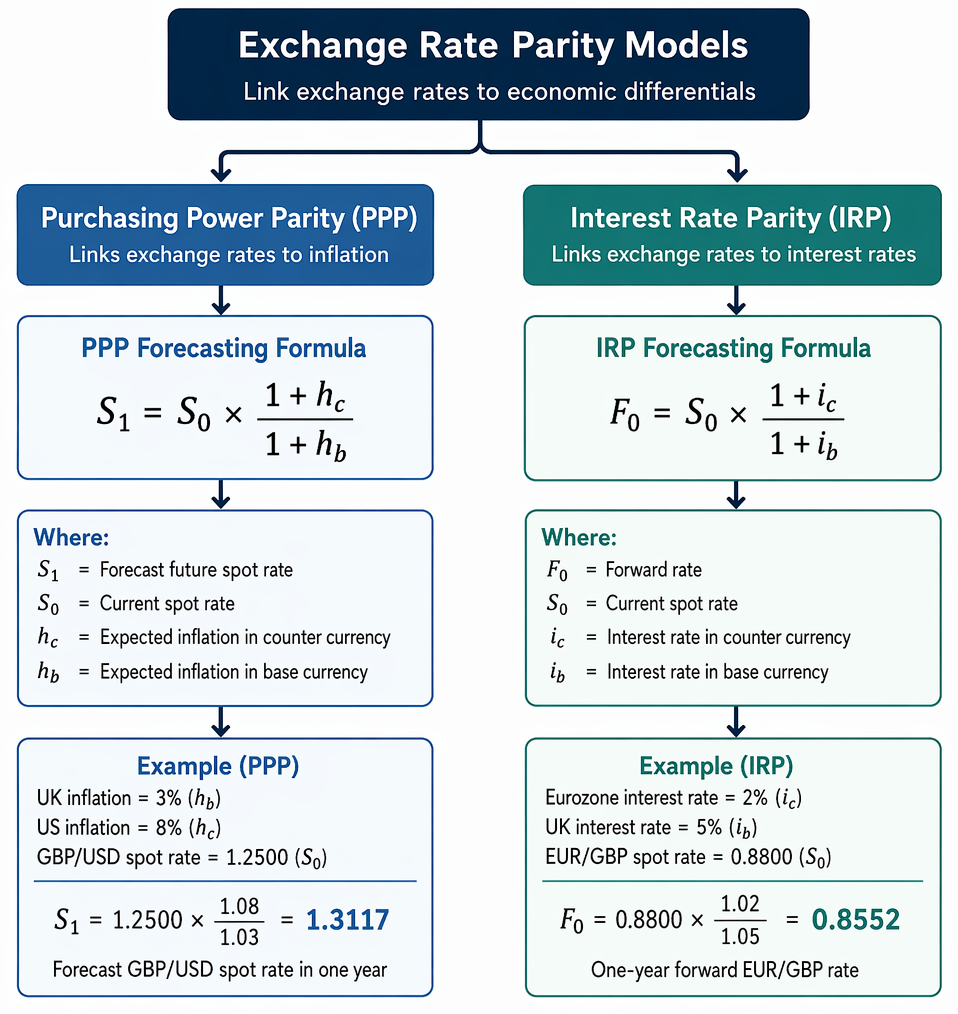

The PPP forecasting formula is:

Where: = Forecast future spot rate = Current spot rate = Expected inflation in the counter currency = Expected inflation in the base currency

Interest Rate Parity (IRP)

IRP states that differences in national interest rates for securities of similar risk and maturity should be reflected in the forward rates of currencies, preventing riskless arbitrage.

Key Term: Interest Rate Parity (IRP)

A theory that the differential between the forward rate and spot rate equals the interest rate differential between two countries, ensuring no arbitrage via covered interest.

The IRP forecasting formula is:

Where: = Forward rate = Interest rate in counter currency = Interest rate in base currency

Worked Example 1.1

Question: A firm expects UK inflation at 3% and US inflation at 8%. The current GBP/USD spot rate is 1.2500. What is the forecast GBP/USD spot rate in one year using PPP?

Answer:

Using PPP:

Therefore, the forecast rate is 1.3117 USD per GBP.

Worked Example 1.2

Question: A company can invest in one-year deposits in the Eurozone at 2% or in the UK at 5%. The EUR/GBP spot rate is 0.8800. What is the one-year forward rate using IRP?

Answer:

Using IRP:

The one-year forward EUR/GBP rate should be 0.8552 if IRP holds.

LIMITATIONS OF PARITY MODELS

While PPP and IRP offer a theoretical basis for forecasting, they often fail to hold exactly due to real-world influences.

Key Term: Parity Deviation

The situation where actual exchange rate movements differ from those predicted by parity models, due to market imperfections or unexpected factors. Key Term: Transaction Costs

The expenses incurred in trading assets or currencies, including spreads, commissions, and fees, which can prevent theoretical arbitrage conditions from holding in reality.

Factors limiting parity-based forecasts include:

- Government intervention and exchange controls

- Market speculation and capital flows unrelated to trade or interest

- Price stickiness and non-tradable goods affecting PPP

- Transaction costs and taxes

- Short-term capital movements outweighing trade flows

Worked Example 1.3

Question: Suppose a company forecasts using PPP, but, in reality, the exchange rate moves less than predicted over one year. What practical factors may explain this divergence?

Answer:

Possible reasons include import/export quotas, central bank currency intervention, price stickiness, or changes in investor sentiment offsetting inflation-driven movements.Exam Warning: Parity formulas are only as reliable as the forecasts for inflation or interest rates. Always check the time period and direction of exchange rate quotes. Exam questions may require converting between “currency per GBP” and “GBP per currency” formats—be careful to apply the rate in the correct direction.

Revision Tip: In exam scenarios, always state (and justify) any assumptions you make about inflation or interest rates. Show clear workings for each calculation step.

PRACTICAL USE AND ALTERNATIVE APPROACHES

Parity models are most applicable for longer-term forecasts where inflation and interest effects have time to materialize. For short-term needs, firms may consider:

- Using forward rates as market-based forecasts (reflecting current expectations and available hedges)

- Applying technical analysis or econometric models (not covered in detail in ACCA AFM)

- Adjusting for expected government policy actions or anticipated macroeconomic shocks

No single forecasting method is foolproof; financial managers should utilise several approaches and remain aware of their limitations.

Summary

Parity models underpin the theoretical forecast of exchange rates, linking movements to inflation or interest rate differences. In practice, real-world frictions cause frequent deviations. Financial managers must be prepared to justify and explain both the use of parity principles and their limitations on the ACCA exam.

Key Point Checklist

This article has covered the following key knowledge points:

- Describe exchange rate parity and its significance in currency forecasting

- Apply Purchasing Power Parity (PPP) and Interest Rate Parity (IRP) formulas for forecasts

- Identify key differences between PPP and IRP and their relevance

- Calculate expected spot and forward rates under parity models

- Recognise common limitations and causes of deviation from parity models

- Suggest practical considerations for forecast reliability

Key Terms and Concepts

- Exchange Rate Parity

- Purchasing Power Parity (PPP)

- Interest Rate Parity (IRP)

- Parity Deviation

- Transaction Costs