Learning Outcomes

This article explains the differences between market-based and cost-based pricing strategies and the relevance of cost information in pricing decisions. You will learn how organisations set prices, the impact of internal and external factors, and the importance of using relevant cost data. By the end, you should be able to select and evaluate appropriate pricing methods and apply relevant costing principles in ACCA exam scenarios.

ACCA Advanced Performance Management (APM) Syllabus

For ACCA Advanced Performance Management (APM), you are required to understand how organisations set prices and the significance of relevant cost information. This article focuses your revision on the following key syllabus areas:

- Evaluate different pricing strategies, including market-based and cost-based approaches

- Explain the concept of relevant costs for decision making

- Assess the implications of pricing choices for performance management

- Critically appraise the use of cost information in pricing decisions

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which of the following best describes relevant costs in the context of pricing decisions?

- a) Past costs already incurred

- b) Future cash flows that will change as a result of a decision

- c) Non-cash costs such as depreciation

- d) Absorbed overhead costs allocated to products

-

A company faces competitive pressure on its main product and is considering reducing its price below full cost. Which pricing method is being used?

- a) Market-based pricing

- b) Cost-plus pricing

- c) Absorption costing

- d) Marginal cost pricing

-

True or false? Cost-based pricing always leads to optimal pricing decisions in highly competitive markets.

-

List two factors that may limit the ability of a business to set prices using cost-based methods.

Introduction

Pricing is a key decision in performance management. Choosing the right price affects sales, profit, and market position. Organisations often set prices based on either the forces of the market or their own cost structures. However, the method chosen must be suitable for the business context and supported by relevant cost information.

This article compares market-based and cost-based pricing approaches, discusses the concept of relevant costs for pricing decisions, and outlines the main advantages and challenges of each pricing method.

Key Term: pricing strategy

The approach an organisation uses to set the price of its goods or services, considering both internal costs and external market conditions.Test Tip: When revising Market based and cost based pricing, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

MARKET-BASED PRICING

Market-based pricing determines selling prices by considering external factors such as competitor prices, customer demand, and overall market trends. This approach is common in competitive or commoditised sectors.

Features of Market-Based Pricing

- Prices are influenced by customer willingness to pay and competitive pressures

- Often used for standard products with many alternatives available

- Pricing can be dynamic, adjusting in response to market changes

Key Term: market-based pricing

A pricing method where the price is set primarily by reference to market conditions, including competitor pricing and customer demand.

Advantages of Market-Based Pricing

- Reflects real-world competition

- Ensures the product remains attractive to customers

- Facilitates rapid response to changes in the external environment

Challenges of Market-Based Pricing

- May result in prices below full cost, reducing profitability

- Organisations have less control over profit margins

- Internal cost structures may become less relevant for pricing

Worked Example 1.1

Scenario: PowerCom sells standard batteries and operates in a crowded market. The main competitor sets its price at £2.50 per pack. PowerCom’s full cost per pack is £2.60. Management considers matching the competitor's price.

Required: Should PowerCom match the price, and what are the implications?

Answer:

If PowerCom matches the competitor at £2.50, it will sell at a loss based on full cost. However, if relevant costs (variable and avoidable costs) per unit are less than £2.50, PowerCom may cover these and contribute toward fixed costs. The company must decide if maintaining market share is worth potential profit sacrifices.

COST-BASED PRICING

Cost-based pricing uses internally calculated product costs as the starting point for setting prices. A desired profit margin is generally added to the total cost to establish the final price.

Types of Cost-Based Pricing

- Full cost (absorption) pricing: All production and overhead costs, plus a mark-up

- Marginal cost pricing: Only variable costs included, with a margin added

Key Term: cost-based pricing

A pricing method that sets prices by adding a mark-up to the cost of producing a product or service. Key Term: relevant costs

Costs that will change as a direct result of the pricing decision being considered. Only future, cash flows that differ between alternatives are relevant. Key Term: full cost

The total of all direct and indirect (fixed and variable) costs associated with producing a product. Key Term: marginal cost

The additional cost of producing one extra unit, typically including only variable costs and direct expenses.

Advantages of Cost-Based Pricing

- Simple to calculate, especially when costs are stable

- Provides a clear target for minimum price to avoid losses

- Useful for pricing in customised or made-to-order markets

Challenges of Cost-Based Pricing

- May ignore demand and competitor prices—risking overpricing in competitive markets

- Full costs depend on accuracy of overhead allocations

- Does not always reflect opportunity costs

Worked Example 1.2

Scenario: AMS Ltd produces a specialist part for car manufacturers. The unit variable cost is £30, fixed overhead per unit is £10, and the company desires a 25% mark-up on full cost.

Required: Calculate the cost-plus price per unit.

Answer:

Full cost per unit = £30 (variable) + £10 (fixed) = £40 Target price = £40 x 125% = £50 per unit

If market demand is weak or competitors charge less than £50, AMS may struggle to make sales at this cost-plus price.

Exam Warning: In APM exams, avoid assuming that cost-based pricing is always suitable. Assess whether the business operates in a competitive market—sometimes market-based pricing is required regardless of internal costing.

RELEVANT COSTS IN PRICING DECISIONS

When setting prices, only costs that will be affected by the pricing decision are relevant. Historical or sunk costs must not influence the price.

Identifying Relevant Costs

Relevant costs typically include:

- Additional variable costs incurred by accepting an order

- Any incremental fixed costs directly linked to fulfilling the order

- Opportunity costs—benefits sacrificed or lost by choosing an alternative

Costs that are not relevant:

- Sunk costs (already incurred and irreversible)

- Allocated fixed overheads that will not change as a result of pricing

Worked Example 1.3

Scenario: Turin Engineering has spare capacity and receives a one-off export order for 2,000 units at a unit price below its normal full cost but above variable cost. Variable cost per unit is $12. Fixed overheads will not change. The customer offers $15 per unit.

Required: Is this order financially acceptable?

Answer:

The relevant cost is the $12 variable cost. The offered price of $15 covers the relevant cost and provides a $3 contribution per unit. Accepting the order will benefit the company as long as there are no adverse strategic implications.

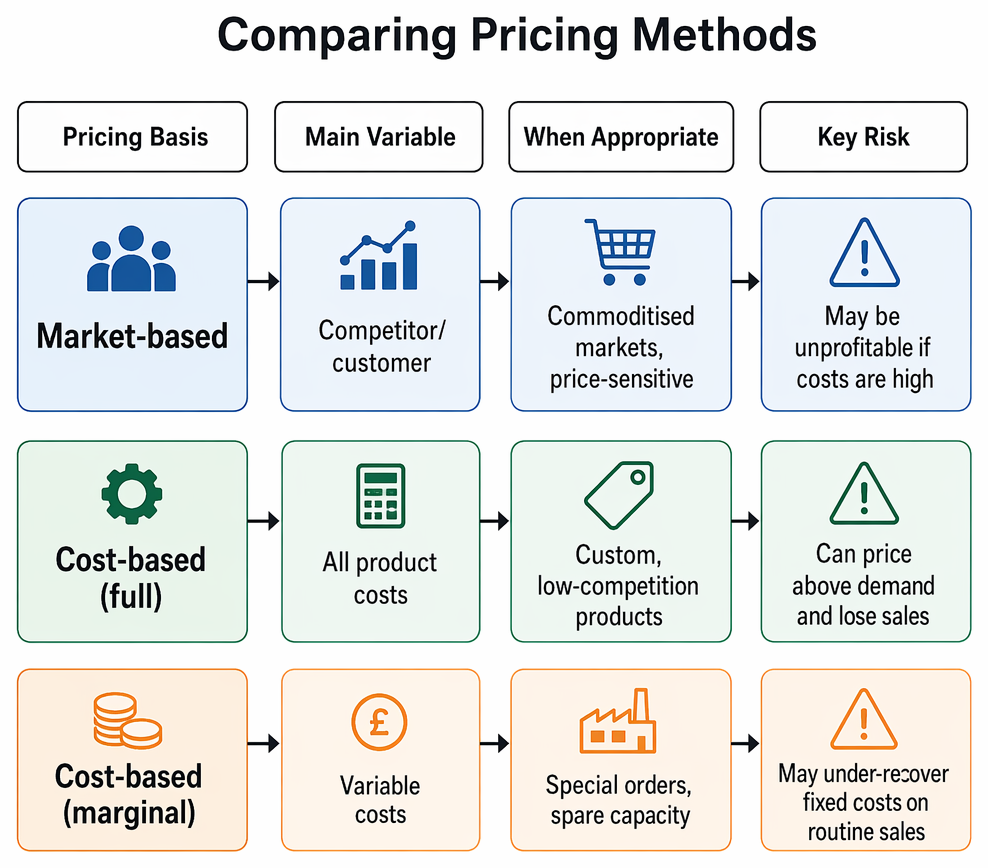

COMPARING PRICING METHODS

Cost relevance criteria for pricing decisions classify items as sunk, committed, non-cash, incremental cash flows, or opportunity costs.

| Pricing Basis | Main Variable | When Appropriate | Key Risk |

|---|---|---|---|

| Market-based | Competitor/customer | Commoditised markets, price-sensitive | May be unprofitable if costs are high |

| Cost-based (full) | All product costs | Custom, low-competition products | Can price above demand and lose sales |

| Cost-based (marginal) | Variable costs | Special orders, spare capacity | May under-recover fixed costs on routine sales |

Summary

Choosing a pricing method depends on business context, competition, and information available. Market-based pricing is essential in competitive environments, while cost-based methods suit unique or low-competition offerings. For decision making, only relevant—future, incremental—costs should influence pricing, not sunk or allocated historic overheads.

Key Point Checklist

This article has covered the following key knowledge points:

- Distinguish between market-based and cost-based pricing strategies

- Explain when to use each pricing method for products or services

- Identify relevant costs for pricing decisions

- Recognise the impact of market conditions on pricing strategy

- Apply relevant costing principles to one-off orders or special pricing scenarios

Key Terms and Concepts

- pricing strategy

- market-based pricing

- cost-based pricing

- relevant costs

- full cost

- marginal cost