Learning Outcomes

This article covers the application of pricing strategies and the concept of relevant costs in short-term decision-making. You will learn to identify and classify relevant and irrelevant costs, analyse pricing decisions under limiting factors, and apply these concepts to real-world scenarios. By the end, you should be able to recommend optimal actions when resources are restricted and understand the financial impact of alternative short-term choices.

ACCA Advanced Performance Management (APM) Syllabus

For ACCA Advanced Performance Management (APM), you are required to understand how relevant cost concepts and short-run pricing strategies impact decision-making, especially when resources are scarce. This article addresses:

- Distinguishing relevant from irrelevant costs in short-run decisions

- Applying relevant cost analysis to pricing and make-or-buy decisions

- Assessing pricing under limiting (scarce) factor constraints

- Determining optimal product mix for maximum contribution

- Recommending actions when faced with resource limitations

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which type of cost is always considered relevant when making a short-term decision?

- a) Sunk cost

- b) Future variable cost that changes as a result of the decision

- c) Past fixed cost

- d) Committed cost

-

If a company faces a shortage of machine hours, which criterion should management use to prioritise production?

- a) Highest total profit per unit

- b) Highest sales volume

- c) Highest contribution per limiting factor

- d) Lowest material cost per unit

-

True or false? Fixed overheads are always relevant in short-term decisions.

-

A product uses 3 labour hours. The contribution per unit is $9, but labour hours are limited. What is the contribution per labour hour?

-

Briefly explain the term “opportunity cost” in the context of relevant costing.

Introduction

Short-term business decisions often require managers to choose between alternative actions, such as setting prices for special orders, accepting or rejecting contracts, or selecting which products to make when resources are limited. The correct approach demands identifying which costs and benefits are truly relevant to the decision and then applying this information to maximise financial gain. Understanding how to use relevant cost analysis and choose the best product mix under scarcity is essential for the ACCA APM exam.

Key Term: relevant cost

A future cash flow that differs between alternative decisions, and is therefore applicable to the decision at hand.Test Tip: When revising Short run decisions and limiting factors, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

RELEVANT AND IRRELEVANT COSTS

For accurate decision-making, you must distinguish between relevant and irrelevant costs.

Relevant Costs

Relevant costs are:

- Future (not past) costs or benefits

- Cash flows (not accounting allocations)

- Incremental (arising only if a particular action is taken)

- Different between the alternatives

Examples include extra material, direct labour, or the opportunity cost of using a resource elsewhere.

Key Term: opportunity cost

The benefit forgone by choosing one course of action instead of the best alternative. Key Term: sunk cost

A cost already incurred that cannot be recovered or changed by current or future decisions.

Irrelevant Costs

Irrelevant costs include:

- Sunk costs (already incurred and cannot change)

- Costs that remain the same regardless of decision

- Committed future costs that are unavoidable

RELEVANT COSTING IN SHORT-RUN PRICING DECISIONS

Short-run decisions focus on actions over a brief period, where some costs are fixed and unavoidable. Common scenarios include special orders, discontinuing a product, or make-or-buy choices.

Identifying Relevant Costs

Relevant costs often include:

- Additional materials

- Additional labour (if not idle)

- Incremental variable overheads

- Opportunity costs (e.g., use of scarce resources)

- Avoided fixed costs (if they will truly be saved by an action)

Irrelevant costs:

- Unchanged fixed overheads

- Historical costs

- Non-cash items (depreciation, apportioned overheads)

Worked Example 1.1

A business can accept a one-off order for 1,000 units at $12 each. The normal selling price is $15 per unit. Variable cost is $8 per unit. Fixed costs are allocated at $3 per unit, but fixed overheads will not increase even if the order is accepted. Should the order be accepted?

Answer:

Only incremental costs and revenues are relevant. The additional revenue is $12,000 ($12 × 1,000). The relevant cost is $8,000 (variable cost only). Fixed overheads are not relevant as they do not increase. The relevant profit is $4,000 ($12,000 – $8,000), so the order should be accepted.

Special Orders and Capacity

If there is spare capacity, relevant costs are usually variable and opportunity costs are zero. If capacity is fully used, accepting an order may involve sacrificing sales elsewhere, so opportunity costs must be included.

PRICING AND LIMITING FACTORS

When resources such as machine hours, labour, or materials are limited, management must decide how to best allocate them to maximise profit.

Key Term: limiting factor

Any resource or constraint that restricts output and hence limits the company's ability to produce goods or services.

Contribution per Limiting Factor

The optimal use of scarce resources is determined by ranking products based on their contribution per unit of the limiting factor.

Contribution per limiting factor = Contribution per unit ÷ Quantity of limiting factor required per unit

Worked Example 1.2

ABC Ltd makes two products, X and Y:

| X | Y | |

|---|---|---|

| Contribution/unit | $20 | $16 |

| Machine hrs/unit | 4 | 2 |

Total available machine hours: 2,000.

Which product mix maximises profit?

Answer:

Calculate contribution per machine hour:

- X: $20 ÷ 4 = $5 per hour

- Y: $16 ÷ 2 = $8 per hour Y generates more contribution per machine hour, so machine time should be used to make as many units of Y as possible.

Other Constraints

If more than one limiting factor exists, linear programming may be used, but for simple single limiting factor problems, ranking by contribution per unit of limiting factor is sufficient.

RELEVANT COSTING AND OPTIMAL PRODUCT MIX

The best product mix in the short run is the combination of products that yields the highest total contribution, given the resource constraint.

Special order appraisal applies relevant costing by testing capacity, excluding unchanged fixed overheads, and comparing revenue with contribution or relevant cost.

Steps:

- Calculate contribution per limiting factor for each product.

- Rank products from highest to lowest.

- Allocate available resource in order of ranking.

- Calculate total contribution and profit.

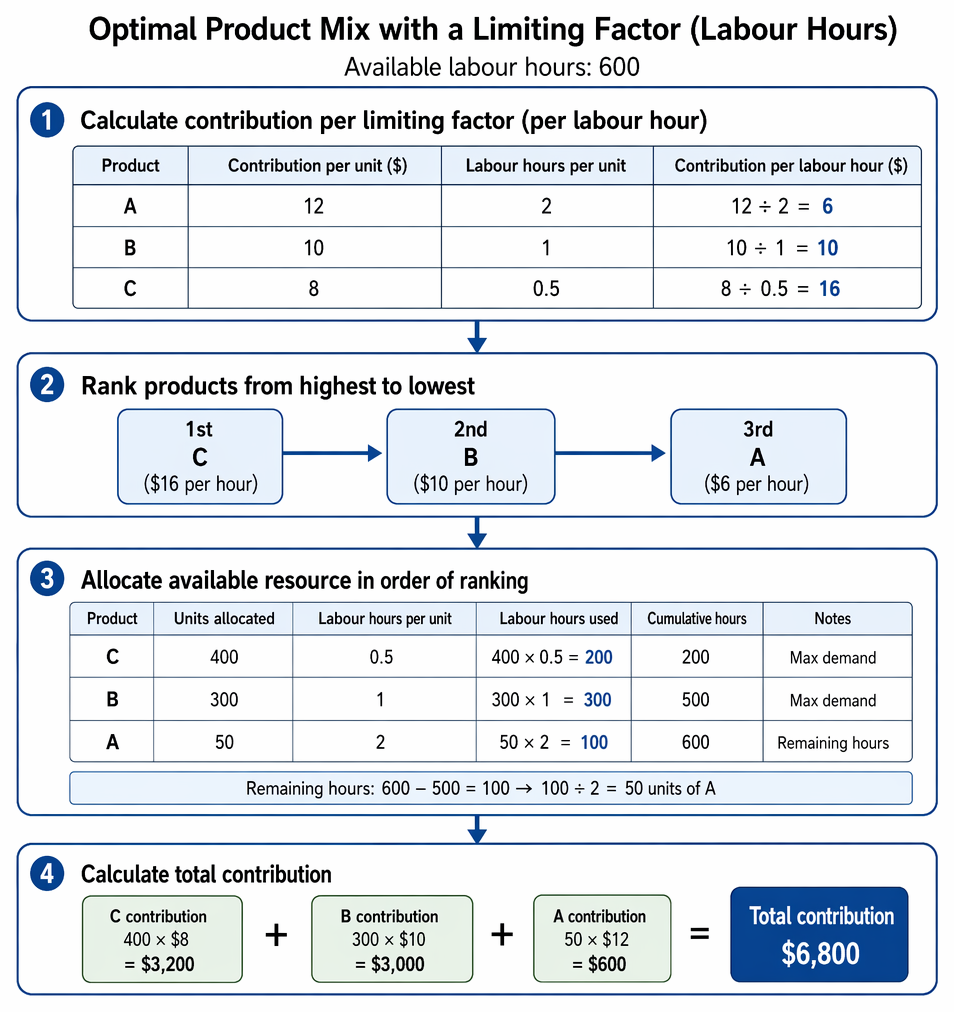

Worked Example 1.3

A firm makes three products (A, B, C) using limited skilled labour hours (available: 600):

| Contribution/unit | Labour hours/unit | Max demand (units) | |

|---|---|---|---|

| A | $12 | 2 | 100 |

| B | $10 | 1 | 300 |

| C | $8 | 0.5 | 400 |

What product mix yields the highest profit?

Answer:

Calculate contribution per labour hour:

- A: $12 ÷ 2 = $6

- B: $10 ÷ 1 = $10

- C: $8 ÷ 0.5 = $16 Priority: C ($16), B ($10), A ($6) Allocate hours:

- C: 400 units × 0.5 = 200 hours

- B: 300 units × 1 = 300 hours (cumulative: 500)

- Remaining hours: 600 – 500 = 100 hours for A (100 ÷ 2 = 50 units) Total contribution = (400 × $8) + (300 × $10) + (50 × $12) = $3,200 + $3,000 + $600 = $6,800

OPPORTUNITY COSTS IN SHORT-RUN DECISION MAKING

Opportunity costs arise when acceptance of a decision causes the business to sacrifice a benefit from the next best alternative.

For example, if a scarce material could be sold instead of used, the relevant cost includes not only the purchase price but also the lost revenue from not selling.

NON-FINANCIAL FACTORS

When advising on short-run pricing and limiting factor issues, always consider:

- Customer relationships and brand reputation

- Potential future orders or contracts

- Employee morale or workload issues

- Quality standards and company strategy

These may outweigh pure financial analysis in some cases.

Exam Warning: In APM exams, do not treat allocated fixed costs or past expenditure as relevant. Focus only on costs and revenues that will change as a direct result of the proposed decision.

Summary

Short-run pricing and product mix decisions must be based on relevant costs, which are future, incremental, and cash flows that differ among alternatives. When faced with limiting factors, maximise contribution per unit of the scarce resource. Always include opportunity costs where resources must be diverted from existing uses. Ignore all sunk and unchanged costs.

Key Point Checklist

This article has covered the following key knowledge points:

- Differentiate relevant and irrelevant costs for short-run decisions

- Calculate and interpret contribution per unit of limiting factor

- Apply the optimal product mix approach when resources are scarce

- Recognise the role of opportunity cost in decision-making

- Identify non-financial considerations that can affect recommendations

Key Terms and Concepts

- relevant cost

- opportunity cost

- sunk cost

- limiting factor