Learning Outcomes

After reading this article, you will be able to explain key disclosure requirements under IAS 23 Borrowing Costs, identify common practical issues when applying the standard, and describe how borrowing costs are treated in financial statements. You will also practise exam-style scenarios on capitalisation and disclosure, enhancing your readiness for ACCA Financial Reporting (FR) assessment.

ACCA Financial Reporting (FR) Syllabus

For ACCA Financial Reporting (FR), you are required to understand how borrowing costs are capitalised, disclosed, and presented in the financial statements under IAS 23. In this article, you should focus on:

- The main disclosure requirements when borrowing costs are capitalised under IAS 23

- How to present borrowing costs and capitalised interest in the financial statements

- Common challenges and issues in practical application, including cessation and suspension of capitalisation, and distinguishing between qualifying and non-qualifying assets

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which of the following must be disclosed when borrowing costs are capitalised for the period?

- a) Total borrowing costs incurred and total amount capitalised

- b) The bank interest rate

- c) Only the total amount capitalised

- d) Internal memos on loan agreements

-

Under IAS 23, when must an entity suspend capitalising borrowing costs?

- a) When the project manager leaves

- b) During extended periods where development of a qualifying asset is interrupted

- c) When loan interest changes

- d) During short-term project stoppages caused by supplier delays

-

True or false? An entity can choose whether to disclose capitalisation rates used for general borrowings.

-

Briefly explain one difficulty in applying IAS 23 capitalisation rules in practice.

Introduction

IAS 23 Borrowing Costs requires that certain interest expenses are capitalised as part of the cost of qualifying assets, while others are expensed as incurred. To meet the standard’s objective, financial statements must provide clear information about the total borrowing costs incurred, the portion capitalised, and relevant capitalisation rates. These disclosures help users understand the impact of interest on asset measurement and profit for the year.

Key Term: borrowing costs

Interest and other costs an entity incurs in connection with the borrowing of funds, such as loan interest, finance charges on leases, and certain exchange differences. Key Term: qualifying asset

An asset which necessarily takes a substantial period of time to get ready for its intended use or sale, such as major construction, manufacturing plants, or self-constructed inventories.Test Tip: In IAS 23 disclosure questions, state both the amount of borrowing costs capitalised and the capitalisation rate used for general borrowings.

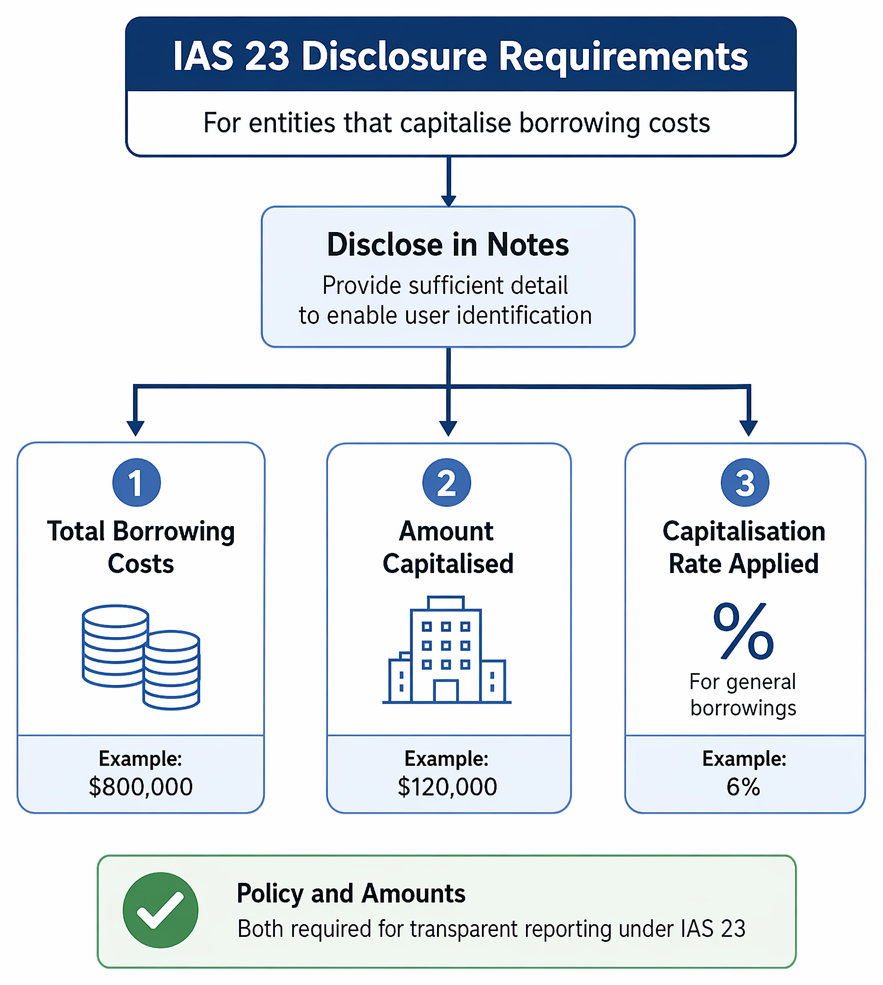

Disclosure Requirements under IAS 23

IAS 23 prescribes explicit disclosures for entities that capitalise borrowing costs. The financial statements must include sufficient detail to enable users to identify:

IAS 23 identifies commencement, temporary suspension, cessation, and post-completion expensing of borrowing costs on a qualifying asset project.

- The amount of borrowing costs capitalised during the period

- The capitalisation rate used to determine the amount of borrowing costs eligible for capitalisation when the asset is funded from general borrowings (not just specific borrowings)

- The accounting policy adopted for borrowing costs

Key Term: capitalisation rate

The rate applied to expenditure on a qualifying asset to determine borrowing costs eligible for capitalisation when the asset is financed from general borrowings.

These disclosures are usually presented in the notes to the financial statements.

Worked Example 1.1

During the year, Peckham Ltd incurred $800,000 in total borrowing costs. Of these, $120,000 was capitalised to qualifying assets at a capitalisation rate of 6%. The financial statement notes show the following disclosure:

- Total borrowing costs for the year

- Amount capitalised in accordance with IAS 23

- Capitalisation rate applied to general borrowings.

Answer:

Peckham Ltd must disclose (i) total borrowing costs ($800,000), (ii) total capitalised ($120,000), and (iii) that a 6% capitalisation rate was used for qualifying assets funded from general borrowings. Both policy and amounts are required to satisfy IAS 23 for transparent reporting.

Practical Issues in Applying IAS 23

Applying IAS 23 requires careful judgment and attention to specific circumstances:

Distinguishing Qualifying Assets

- Not all assets are eligible for capitalisation of borrowing costs. Only assets requiring a substantial period of preparation meet the definition. Routine inventory manufacturing or assets ready for use on acquisition are excluded.

- Determining what constitutes a "substantial" period can be subjective. Typically, it refers to assets taking 12 months or more to prepare, but the standard does not define a strict threshold.

Exam Warning: Do not assume every asset funded by debt is a qualifying asset; the asset must take a substantial period of time to get ready for intended use or sale.

Measuring Capitalised Amounts

- When borrowings are specific to an asset, only actual interest incurred minus any income earned from temporary investment of these borrowings is capitalised.

- For general borrowings, a weighted average capitalisation rate based on all outstanding borrowings must be applied to expenditure on qualifying assets.

- Errors often arise if entities apply the wrong rate, miscalculate average expenditures, or fail to deduct income earned.

Starting, Suspending, and Ceasing Capitalisation

- Capitalisation of borrowing costs begins only when expenditure on a qualifying asset is incurred, borrowing costs are being incurred, and activities to prepare the asset for use or sale are in progress.

- Capitalisation must be suspended during extended periods of inactivity, except when necessary for technical reasons.

- Capitalisation ceases when substantially all activities required to prepare the asset are complete.

Worked Example 1.2

Global Developers Co. borrowed $10 million at 8% to construct a facility expected to take 18 months. After six months, work stopped for five months pending a redesign, before resuming. How long should interest be capitalised?

Answer:

Capitalise interest only during periods when (1) qualifying asset expenditure is being incurred, (2) borrowing costs are incurred, and (3) active construction is taking place. The five-month suspension for redesign means borrowing costs during this inactivity must be expensed, not capitalised.

Common Disclosure Pitfalls

- Omitting the capitalisation rate for general borrowings is a frequent error.

- Failing to distinguish between specific and general borrowings in disclosures can confuse users.

- Not stating the entity’s policy—e.g., whether IAS 23 is applied to all eligible assets—is non-compliance.

Exam Warning: Candidates often lose marks by calculating the capitalised amount correctly but forgetting the related disclosure of the capitalisation rate for general borrowings.

Summary

IAS 23 mandates clear disclosure of both amounts capitalised and rates used. Entities must be precise in distinguishing qualifying from non-qualifying assets. Capitalisation should be suspended during prolonged interruptions and ceases once the asset is ready for use or sale. Errors often arise in practice with the timing of capitalisation, calculation of eligible costs, or incomplete notes in financial statements.

Key Point Checklist

This article has covered the following key knowledge points:

- Disclose total borrowing costs and total amount capitalised for the period

- State the capitalisation rate used for general borrowings in the notes

- Identify periods where capitalisation must be suspended or ceased

- Recognise only assets meeting the “substantial period” test as qualifying assets

- Avoid common errors such as incomplete disclosure or misapplying rates

Key Terms and Concepts

- borrowing costs

- qualifying asset

- capitalisation rate