Learning Outcomes

After reading this article, you will be able to explain when the capitalisation of borrowing costs must be suspended or ceased under IAS 23. You will understand the criteria for suspending capitalisation during interruptions to qualifying asset construction, know how to determine the point when capitalisation stops, and be able to apply these rules accurately in ACCA FR exam questions.

ACCA Financial Reporting (FR) Syllabus

For ACCA Financial Reporting (FR), you are required to understand the correct treatment of borrowing costs, especially when their capitalisation must be stopped or paused. Focus your revision on:

- The point at which capitalisation of borrowing costs is suspended (including interruptions in asset construction)

- The criteria for cessation of capitalisation

- The impact of suspending or ceasing capitalisation on asset measurement and statement of profit or loss

- Application of IAS 23 in single entity financial statements

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- Under IAS 23, in which situation must capitalisation of borrowing costs be suspended?

- At what event does IAS 23 require the cessation of capitalising borrowing costs on a qualifying asset?

- True or false? Borrowing costs are always capitalised until the full repayment of the related loan.

- A company temporarily stops asset construction due to a labour strike. How are borrowing costs incurred during this pause treated?

Introduction

IAS 23 Borrowing Costs requires entities to capitalise those borrowing costs directly attributable to the acquisition or construction of a qualifying asset. However, there are specific rules about when capitalisation is paused (suspended) and when it must finally stop (ceased). These rules ensure only relevant costs are included in the asset’s carrying amount and that costs not supporting progress are shown as expenses. For exam purposes, recognising these moments is critical for accurate financial reporting.

Key Term: qualifying asset

An asset that necessarily takes a substantial period of time to get ready for its intended use or sale, such as certain items of property, plant and equipment or inventories.

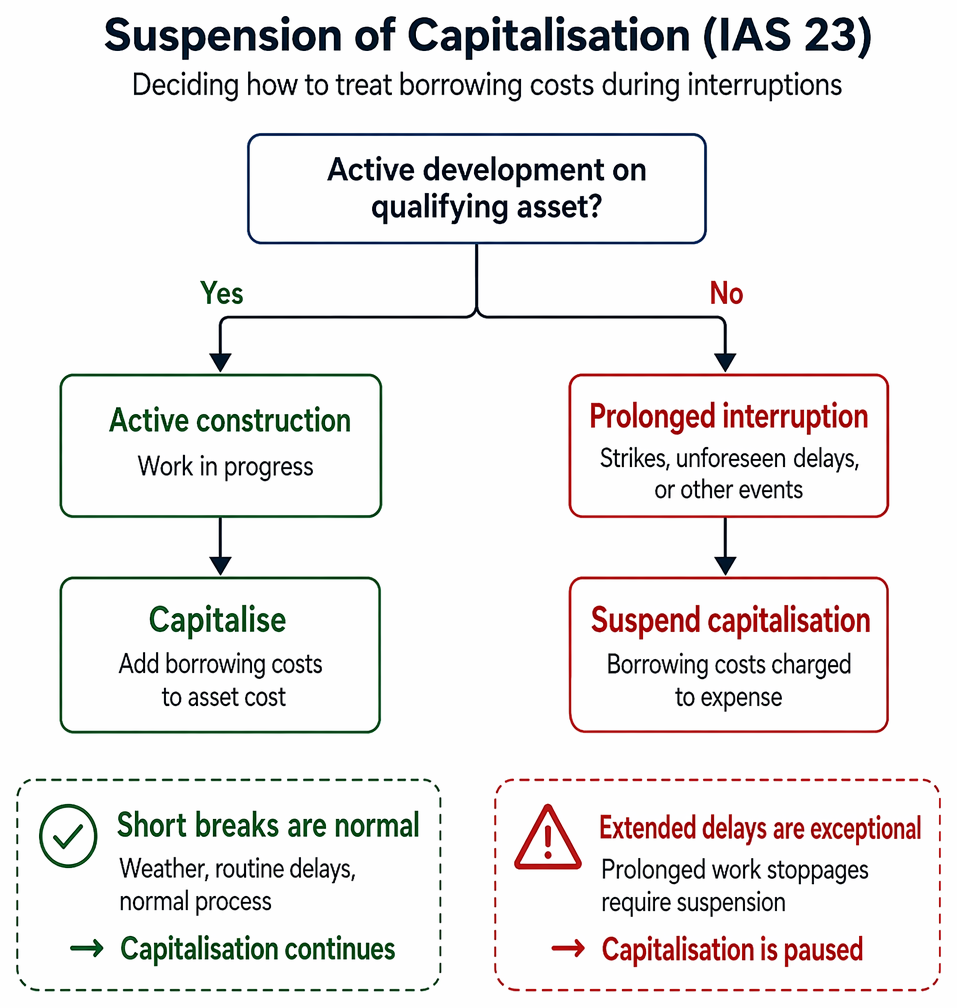

Suspension of Capitalisation

Borrowing costs on a qualifying asset remain capitalised during normal delays but are expensed during extended inactivity until development recommences.

When Capitalisation Should Be Suspended

IAS 23 states capitalisation must be suspended during extended periods when active development on a qualifying asset is interrupted. Typical reasons include strikes, unforeseen delays, or other events causing construction to halt.

Key Term: suspension of capitalisation

The temporary pausing of adding borrowing costs to an asset’s cost during prolonged inactivity in its construction or production.

When work on a qualifying asset is stopped for a prolonged period and no active development is taking place, borrowing costs incurred in this period are charged to expense, not capitalised. Short breaks, such as those necessary for weather or routine delays that are part of the normal process, do not require suspension.

Worked Example 1.1

Question: A company is constructing a manufacturing plant, with work beginning in January. In July, construction halts for three months due to a worker strike. Should borrowing costs for these three months be capitalised or expensed?

Answer:

Borrowing costs incurred during the three-month strike should be treated as expense in the statement of profit or loss. Only costs incurred while actively constructing the asset can be capitalised; costs during an extended suspension are not capitalised.Revision Tip: In the exam, if you see “extended delays” or “prolonged work stoppages,” consider whether capitalisation of borrowing costs must be paused.

Exam Warning: Do not confuse routine delays (e.g. normal site preparation) with exceptional events requiring suspension; only prolonged inactivity triggers suspension.

Cessation of Capitalisation

When Capitalisation Ceases

IAS 23 requires that the capitalisation of borrowing costs must stop when substantially all activities necessary to prepare the qualifying asset for its intended use or sale are complete. Any further borrowing costs—such as those incurred after project completion, or during minor finishing works or the asset's idle period—are expensed to the statement of profit or loss.

Key Term: cessation of capitalisation

The point at which no further borrowing costs are added to a qualifying asset because it is ready for use or sale.

If parts of the asset can be used independently, capitalisation ceases for those completed parts even if work continues on other sections.

Worked Example 1.2

Question: Domel Co completes all major construction on a building project on 1 August and uses the building from that date. However, minor landscaping work continues until October, and interest continues to be incurred. Should Domel Co continue to capitalise interest after 1 August?

Answer:

Domel Co must cease capitalising borrowing costs from 1 August, as substantially all activities necessary to get the building ready for use are finished. Borrowing costs incurred after this point are expensed, even if minor work such as landscaping continues.

Worked Example 1.3

Question: Felix Ltd is building a piece of plant that will be operational as soon as assembly ends. Once assembly is complete, further minor modifications are made, but the plant is already used in production. Should borrowing costs after assembly be capitalised?

Answer:

Borrowing costs cannot be capitalised after the asset is available for use or sale, regardless of minor post-completion enhancements. They must be presented as expense in the statement of profit or loss.

Summary

IAS 23 directs that borrowing costs are capitalised only while active construction of a qualifying asset is taking place. Capitalisation must be suspended during prolonged inactivity and ceased when the asset is substantially ready for intended use or sale. In the ACCA FR exam, correct treatment of these moments is essential for full marks and accurate financial statements.

Key Point Checklist

This article has covered the following key knowledge points:

- Define “suspension of capitalisation” of borrowing costs under IAS 23

- List routine versus exceptional interruptions affecting capitalisation

- State when cessation of capitalisation is required on a qualifying asset

- Recognise when borrowing costs should be expensed, not capitalised

- Apply IAS 23’s suspension and cessation rules to standard exam scenarios

Key Terms and Concepts

- qualifying asset

- suspension of capitalisation

- cessation of capitalisation