Learning Outcomes

After reading this article, you will be able to explain when and why assets are tested for impairment under IAS 36, identify both internal and external indicators of impairment, and calculate recoverable amount using value in use (VIU) and fair value less costs of disposal (FVLCD). You will also be able to compare VIU and FVLCD in practice and understand which figure should be used in the financial statements.

ACCA Financial Reporting (FR) Syllabus

For ACCA Financial Reporting (FR), you are required to understand how to apply IAS 36 when measuring and recognising impairment losses. Focus your revision on:

- Identifying circumstances that indicate an asset may be impaired

- Explaining how to determine the recoverable amount of an asset

- Distinguishing between value in use and fair value less costs of disposal

- Calculating and recognising impairment losses in the financial statements

- Understanding the implications for different asset types

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- Which two types of evidence are considered when evaluating if an asset may be impaired under IAS 36?

- What is the definition of recoverable amount, and what two methods must be compared to determine it?

- Choose which impairment indicator below is internal and which is external:

- a) A major increase in market interest rates

- b) Physical damage to a machine

- Briefly describe how value in use (VIU) is calculated for impairment purposes.

Introduction

IAS 36 ensures that assets are not carried above their recoverable amount in the statement of financial position. This standard applies to most non-current tangible and intangible assets, but excludes inventories, deferred tax, and financial instruments, which are measured under different standards. Impairment is the process of writing down assets when their value has fallen below their current carrying amount.

Key Term: impairment

A fall in the value of an asset below its carrying amount, requiring the asset to be written down so that its carrying amount does not exceed its recoverable amount. Key Term: recoverable amount

The higher of an asset’s fair value less costs of disposal and its value in use. Key Term: value in use (VIU)

The present value of the future cash flows expected from an asset’s continued use and disposal. Key Term: fair value less costs of disposal (FVLCD)

The amount obtainable from the sale of an asset in an arm’s length transaction between knowledgeable, willing parties, less the costs of disposal.Test Tip: When revising Indicators and recoverable amount (VIU vs FVLCD), connect each definition, method, or rule to the kind of question the assessment is likely to ask.

When is an Impairment Test Required?

An entity must assess at each reporting date whether there is any indication that an asset may be impaired. If such indications exist, the asset’s recoverable amount must be estimated. In some cases, annual impairment tests are mandatory, such as for goodwill and intangible assets with indefinite useful lives, even when no indicators are present.

Indicators of Impairment

IAS 36 sets out both external and internal sources to identify possible impairment:

External Indicators

- Unexpected significant decline in market value

- Adverse changes in the technological, market, economic, or legal environment

- Increases in market interest rates, affecting the discount rate (which reduces VIU)

- Market capitalisation below net asset value (for listed companies)

Internal Indicators

- Physical damage or obsolescence of the asset

- Significant underperformance compared to budget

- Evidence that the asset’s economic performance is worse than expected

- Plans to discontinue or restructure the operation to which the asset belongs

Key Term: impairment indicator

A sign or event, internal or external, that suggests an asset may have lost value and may need to be tested for impairment under IAS 36.

Calculating Recoverable Amount

Once an indicator of impairment has been identified (or for assets requiring annual testing), the asset’s recoverable amount must be calculated.

Key Term: recoverable amount

The higher of an asset's fair value less costs of disposal (FVLCD) and its value in use (VIU).

- If the recoverable amount is lower than the carrying amount, an impairment loss is recognised.

Value in Use (VIU)

Value in use is based on the present value of expected future cash flows that the asset will generate, discounted using a pre-tax rate that reflects current market assessments of the time value of money and risks specific to the asset.

Key steps:

- Estimate future cash flows from the asset (or cash-generating unit)

- Exclude cash flows relating to financing and tax

- Determine a suitable pre-tax discount rate

- Calculate the present value of the estimated cash flows

Fair Value Less Costs of Disposal (FVLCD)

FVLCD is the amount that would be received if the asset were sold at the reporting date, less any costs needed to complete the sale, such as legal fees, removal costs, or agent’s commissions.

Recognising Impairment

If recoverable amount < carrying amount, the asset is written down to recoverable amount. The impairment loss is recognised immediately in profit or loss, unless the asset has previously been revalued upwards; in that case, the loss may reverse a previous revaluation surplus via other comprehensive income.

Worked Example 1.1

An entity owns equipment with a carrying amount of $100,000. At year end, there are signs of impairment. The fair value less costs of disposal is $78,000. Management estimates future cash flows from continued use as $30,000 per year for three years. The appropriate pre-tax discount rate is 10%.

Required: Calculate the impairment loss, if any, to be recorded.

Answer:

Step 1: Calculate VIU.

- Present value of $30,000 for 3 years at 10%: Year 1: $27,273 Year 2: $24,793 Year 3: $22,539 Total VIU = $27,273 + $24,793 + $22,539 = $74,605 Step 2: Compare FVLCD ($78,000) and VIU ($74,605): Recoverable amount is $78,000. Step 3: Carrying amount – recoverable amount = $100,000 – $78,000 = $22,000 Impairment loss to record: $22,000.

Worked Example 1.2

A vehicle is carried at $12,000. Fair value less costs to sell is $11,000; value in use is $9,500.

Required: Which figure should be used as recoverable amount, and what loss, if any, is recorded?

Answer:

The recoverable amount is higher of $11,000 (FVLCD) and $9,500 (VIU), so $11,000. The impairment is $12,000 – $11,000 = $1,000. Write the asset down to $11,000 and recognise a $1,000 loss in profit or loss.Exam Warning: Be careful to calculate both VIU and FVLCD. Students often lose marks by stopping at the first figure calculated, but the recoverable amount is explicitly the higher of the two. Failing to consider both can result in an incorrect impairment loss.

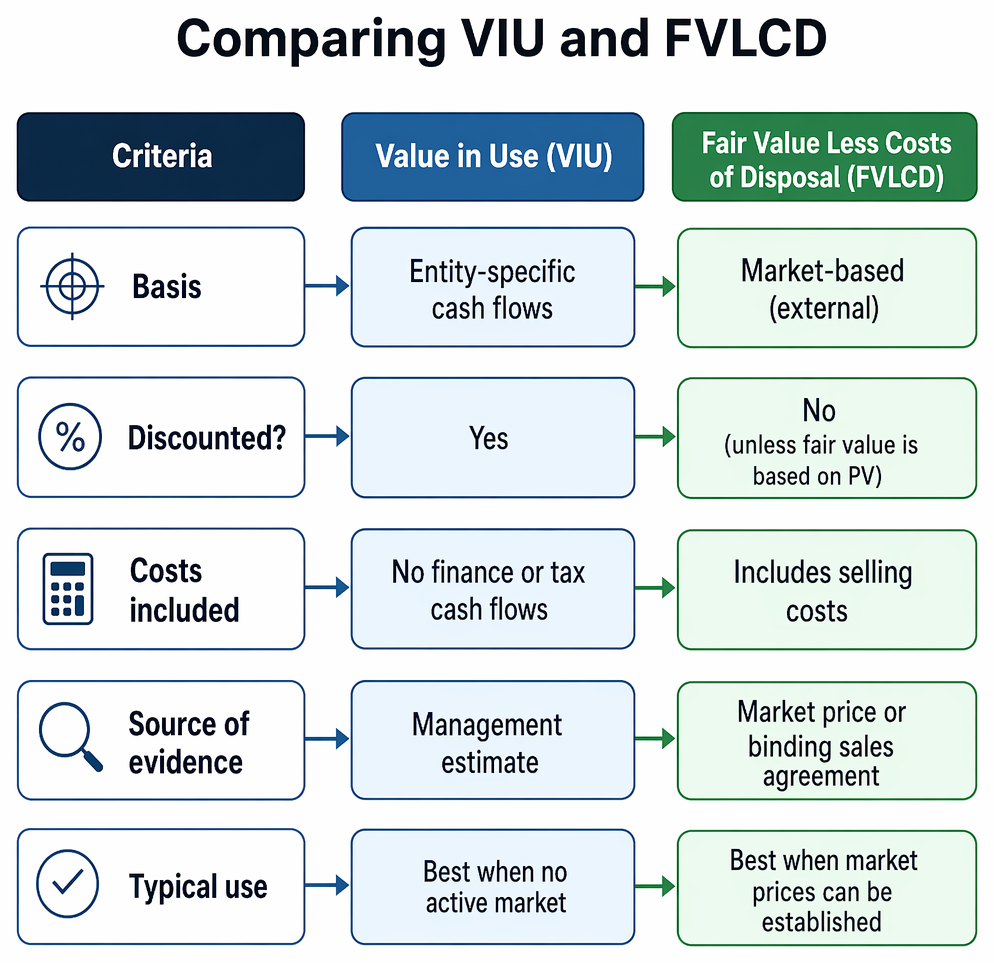

Summary Table: Comparing VIU and FVLCD

Impairment indicators under IAS 36 are organised into external and internal categories used to determine whether recoverable amount should be estimated.

| Criteria | Value in Use (VIU) | Fair Value Less Costs of Disposal (FVLCD) |

|---|---|---|

| Basis | Entity-specific cash flows | Market-based (external) |

| Discounted? | Yes | No (unless fair value is based on PV) |

| Costs included | No finance or tax cash flows | Includes selling costs |

| Source of evidence | Management estimate | Market price or binding sales agreement |

| Typical use | Best when no active market | Best when market prices can be established |

Key Point Checklist

This article has covered the following key knowledge points:

- Explain the objective of IAS 36 and which assets it applies to

- List and recognise both internal and external indicators of impairment

- Calculate recoverable amount as the higher of VIU and FVLCD

- Calculate VIU by discounting expected future cash flows at a pre-tax rate

- Define and identify the correct use of FVLCD

- Recognise how to record impairment losses in the financial statements

Key Terms and Concepts

- impairment

- recoverable amount

- value in use (VIU)

- fair value less costs of disposal (FVLCD)

- impairment indicator