Learning Outcomes

After reading this article, you will be able to identify when an asset is impaired, explain the measurement and recognition of impairment losses under IAS 36, and describe the requirements for reversing impairment losses. You will be prepared to apply these principles to both individual assets and cash-generating units (CGUs), ensuring accurate and compliant financial reporting for the ACCA Financial Reporting (FR) exam.

ACCA Financial Reporting (FR) Syllabus

For ACCA Financial Reporting (FR), you are required to understand the identification, measurement, and reversal of asset impairment under IAS 36. Specifically, you should be able to:

- Define, calculate, and account for an impairment loss on individual assets and CGUs, including goodwill

- Recognise and measure the reversal of impairment losses, including any restrictions

- Identify internal and external indications of impairment

- Calculate recoverable amounts (higher of fair value less costs of disposal and value in use)

- Allocate impairment losses to CGU assets in accordance with IAS 36

- Apply the rules for impairment reviews of intangible assets with indefinite useful lives and goodwill

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the recoverable amount of an asset in IAS 36, and how is it calculated?

- If the carrying amount of an asset exceeds its recoverable amount, what must an entity do?

- Which assets must have annual impairment reviews even if there is no indication of impairment?

- Can an impairment loss for goodwill ever be reversed under IAS 36?

- What are the key steps in allocating an impairment loss within a cash-generating unit?

Introduction

IAS 36 Impairment of Assets sets out rules to ensure that assets are not reported in financial statements at more than their recoverable amount. This is essential for providing a true and fair view to users. You must recognise impairment losses when an asset is shown at more than the value recoverable from its use or sale. IAS 36 also provides guidance on when impairment losses can be reversed and the restrictions that apply.

Test Tip: When revising Recognising and reversing impairment losses, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Recognition and Indicators of Impairment

IAS 36 applies to most non-financial assets, including property, plant and equipment, and intangible assets (except goodwill under certain circumstances). It does not apply to inventory, financial assets, or investment property measured at fair value.

Impairment must be tested if there is any indication from either internal or external sources that an asset’s value may be reduced.

External indications include:

- Significant decline in asset market value

- Adverse changes in technological, market, economic, or legal environment

- Increases in market interest rates affecting the discount used in value in use

Internal indications include:

- Physical damage or obsolescence of an asset

- Changes in how an asset is used

- Actual or expected lower economic performance of an asset or CGU

For goodwill and intangible assets with indefinite useful lives, an annual impairment review is required even if there is no indicator of impairment.

Key Term: impairment

A reduction in the recoverable amount of an asset below its carrying amount, requiring a write-down in the financial statements under IAS 36. Key Term: carrying amount

The amount at which an asset is recognised after deducting accumulated depreciation and impairment losses. Key Term: recoverable amount

The higher of an asset's fair value less costs of disposal and its value in use. Key Term: value in use

The present value of the future cash flows expected to be derived from an asset. Key Term: fair value less costs of disposal

The price that would be received to sell an asset in an orderly transaction between market participants, less direct selling costs.

Measurement of Impairment Loss

If indicators of impairment exist, compare the asset's carrying amount to its recoverable amount. An impairment loss must be recognised if the carrying amount exceeds the recoverable amount.

Recoverable amount calculation:

- Recoverable amount = Higher of fair value less costs of disposal and value in use

Impairment loss = Carrying amount − Recoverable amount

Recognise the impairment loss immediately in profit or loss unless it reverses a previous revaluation gain, in which case it is deducted first from the revaluation surplus (and shown in other comprehensive income up to the surplus).

Worked Example 1.1

Question: A company owns equipment with a carrying amount of $120,000. Its fair value less disposal costs is $98,000 and value in use is $105,000. What impairment loss should be recognised?

Answer:

The recoverable amount is $105,000 (the higher of $98,000 and $105,000). Impairment loss = $120,000 − $105,000 = $15,000

Allocating Impairment Losses for Cash-Generating Units (CGUs)

Some assets do not generate cash flows independently. In such cases, impairment is assessed at the CGU level.

Recoverable amount under IAS 36 determines whether an impairment loss is recognised and whether the carrying amount and depreciation basis are revised.

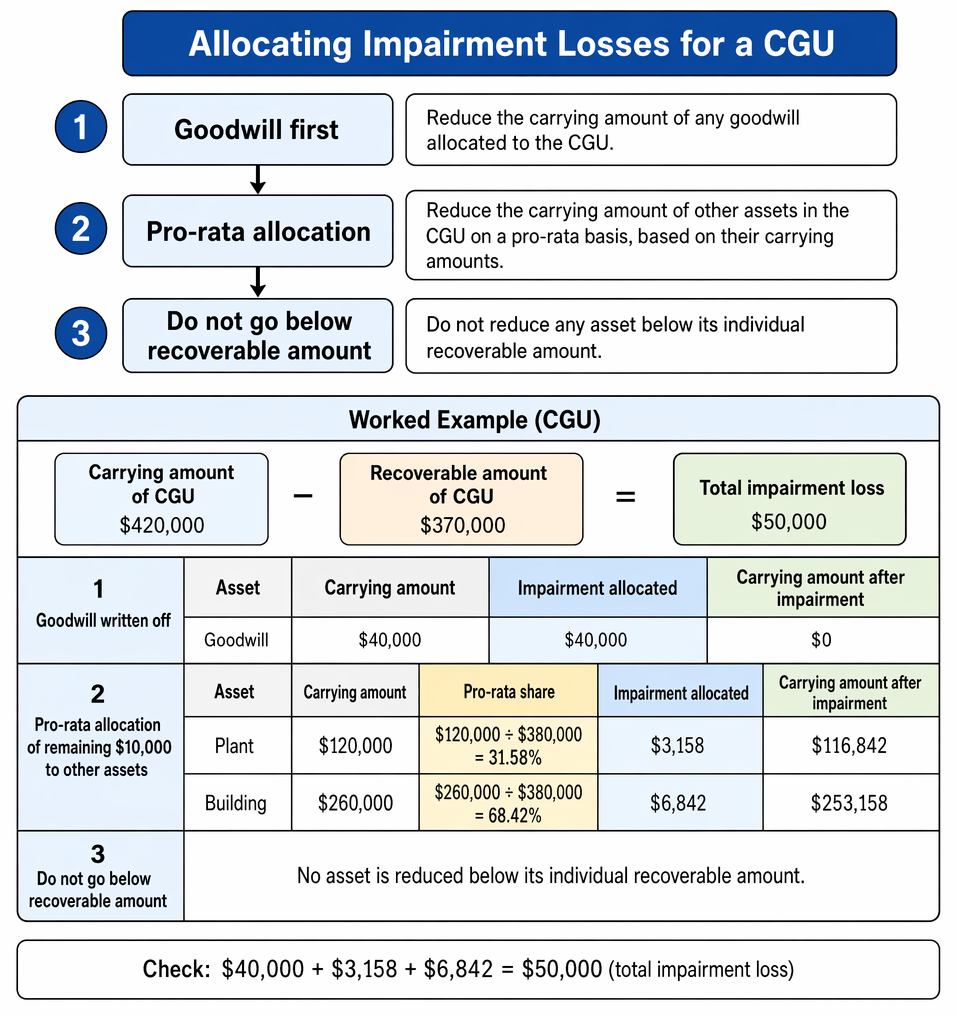

Impairment within a CGU is allocated as follows:

- Reduce the carrying amount of any goodwill allocated to the CGU.

- Reduce the carrying amount of other assets in the CGU on a pro-rata basis, based on their carrying amounts.

- Do not reduce any asset below its individual recoverable amount.

Worked Example 1.2

Question: A CGU consists of the following assets:

- Goodwill: $40,000

- Plant: $120,000

- Building: $260,000

If the CGU’s carrying amount is $420,000 and the recoverable amount is $370,000, how is the impairment loss allocated?

Answer:

Total impairment loss = $420,000 − $370,000 = $50,000 Step 1: Write off goodwill ($40,000) Step 2: Allocate remaining $10,000 to plant and building based on their carrying amounts ($120,000 + $260,000 = $380,000):

- Plant: $10,000 × $120,000/$380,000 = $3,158

- Building: $10,000 × $260,000/$380,000 = $6,842

Reversal of Impairment Losses

After recognising an impairment loss, an asset should be reviewed at each reporting date for possible reversal if indicators suggest that previous estimates have changed. A reversal can only occur if there has been a change in the estimates used to determine recoverable amount since the last impairment was recognised.

Key rules for reversal:

- Recognise immediately as income in profit or loss (unless the impairment was previously deducted from a revaluation surplus, in which case restore to the surplus first).

- Do not increase the carrying amount above the depreciated historical cost had no impairment been recognised.

- Impairment losses recognised for goodwill must not be reversed in subsequent periods.

Key Term: reversal of impairment

An increase in the recoverable amount of a previously impaired asset, with the gain recognised up to the limit of what the carrying amount would have been (net of depreciation) if no impairment had occurred.

Worked Example 1.3

Question: An asset cost $30,000 with a 10-year useful life, depreciated straight-line. After 4 years, an impairment loss of $10,000 was recognised, reducing the carrying amount to $10,000. Two years later, the recoverable amount increases to $18,000. What carrying amount can be recognised?

Answer:

Had there been no impairment, carrying amount after 6 years = $30,000 − (6 × $3,000) = $12,000 Reversal is limited to the depreciated historical cost. Carrying amount can be restored up to $12,000. The $6,000 increase is credited to profit or loss.Exam Warning: A common exam error is to reverse impairment losses above the asset’s original depreciated cost. Remember, reversal cannot set the carrying amount above what it would have been if no impairment had occurred.

Special Cases: Goodwill and Intangible Assets

- Goodwill impairment losses cannot be reversed in any circumstances.

- For intangible assets with indefinite useful lives or not yet available for use, an annual impairment review is mandatory, regardless of indication of impairment.

Summary

IAS 36 requires that assets are not carried above the amount recoverable from use or sale. When indicators suggest impairment, the asset must be written down to the higher of its value in use and fair value less costs of disposal. An impairment loss is recognised in profit or loss unless it relates to a previous revaluation. Reversal of impairment losses is permitted if justified by changed circumstances, but not for goodwill, and only up to the depreciated cost as if no impairment had been recognised.

Key Point Checklist

This article has covered the following key knowledge points:

- Recognise when to perform impairment testing under IAS 36

- Define and calculate recoverable amount (higher of value in use and fair value less costs of disposal)

- Recognise and measure impairment losses and allocate them within a CGU

- Recognise when and how impairment losses may be reversed

- Explain and apply restrictions on reversal of impairment, especially for goodwill

- Mandatory annual impairment reviews for goodwill and indefinite-life intangibles

Key Terms and Concepts

- impairment

- carrying amount

- recoverable amount

- value in use

- fair value less costs of disposal

- reversal of impairment