Learning Outcomes

This article explains how the core features of debt securities and their embedded options shape cash flows, pricing, and risk for CFA Level 1 candidates. It develops your ability to identify standard fixed‑rate (plain‑vanilla) bond structures, describe the timing and magnitude of their coupon and principal payments, and contrast these predictable patterns with bonds that contain optionality. You learn to distinguish common embedded options—such as call, put, conversion, and sinking fund provisions—and to state clearly which party (issuer or holder) benefits in different interest rate and credit environments. The article explains how call and put features alter expected life, cash‑flow uncertainty, and required yield, and how they create effective price ceilings and floors. It further examines how convertible provisions trade current income for equity‑linked upside and how option‑adjusted yield measures facilitate comparison across bonds with and without options. Throughout, the focus is on interpreting exam‑style scenarios, linking each embedded feature to its implications for valuation, yield, effective duration, and investor decision‑making.

CFA Level 1 Syllabus

For the CFA Level 1 exam, you are expected to understand the fundamental characteristics and risk factors affecting bond cash flows, especially where embedded options are present, with a focus on the following syllabus points:

- Describing typical bond cash flow structures and features

- Defining and identifying embedded options and their effects on both issuer and holder

- Explaining the risks and valuation effects of call, put, and other common embedded options in debt securities

- Analyzing the practical consequences of embedded options for investors and issuers

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- Which embedded option grants the issuer the right to redeem a bond before maturity, and how does this generally affect required yield?

- How does the presence of a put option in a bond protect holders—especially in rising interest rate environments?

- How does a sinking fund provision differ from a call option in terms of cash flow risk for bondholders?

- What is a convertible bond and how does its embedded equity option influence investor return potential?

Introduction

Bonds are debt securities that require the issuer to make stated payments to the bondholder, usually fixed interest and principal. However, many bonds incorporate features—called embedded options—that alter these cash flows. Understanding the effect of these features is critical to accurate bond valuation and risk assessment for the CFA exam.

Key Term: embedded option

An embedded option is a provision within a bond that gives the issuer or holder rights to take certain actions affecting the bond’s cash flows, such as redeeming or selling the bond before maturity.

Bond Cash Flows: Standard Structures

The typical plain-vanilla bond provides periodic interest payments (coupons) at a stated rate, with full principal repaid at maturity. For fixed-rate bonds, coupon amounts and timing are fixed in advance. Investors rely on these scheduled cash flows unless the contract specifies otherwise.

When a bond lacks optionality, issuer and investor obligations are straightforward. However, many real-world bonds include additional rights.

Common Embedded Options

Embedded options change the risk/return profile for both bondholders and issuers. The most common are call, put, and conversion features.

Key Term: call option (on a bond)

A call option allows the issuer to redeem the bond before maturity at a set price and under specified conditions. Key Term: put option (on a bond)

A put option allows the bondholder to require the issuer to redeem the bond before maturity at a preset price. Key Term: convertible option

A convertible option allows the bondholder to exchange the bond for a fixed number of issuer shares under set terms.

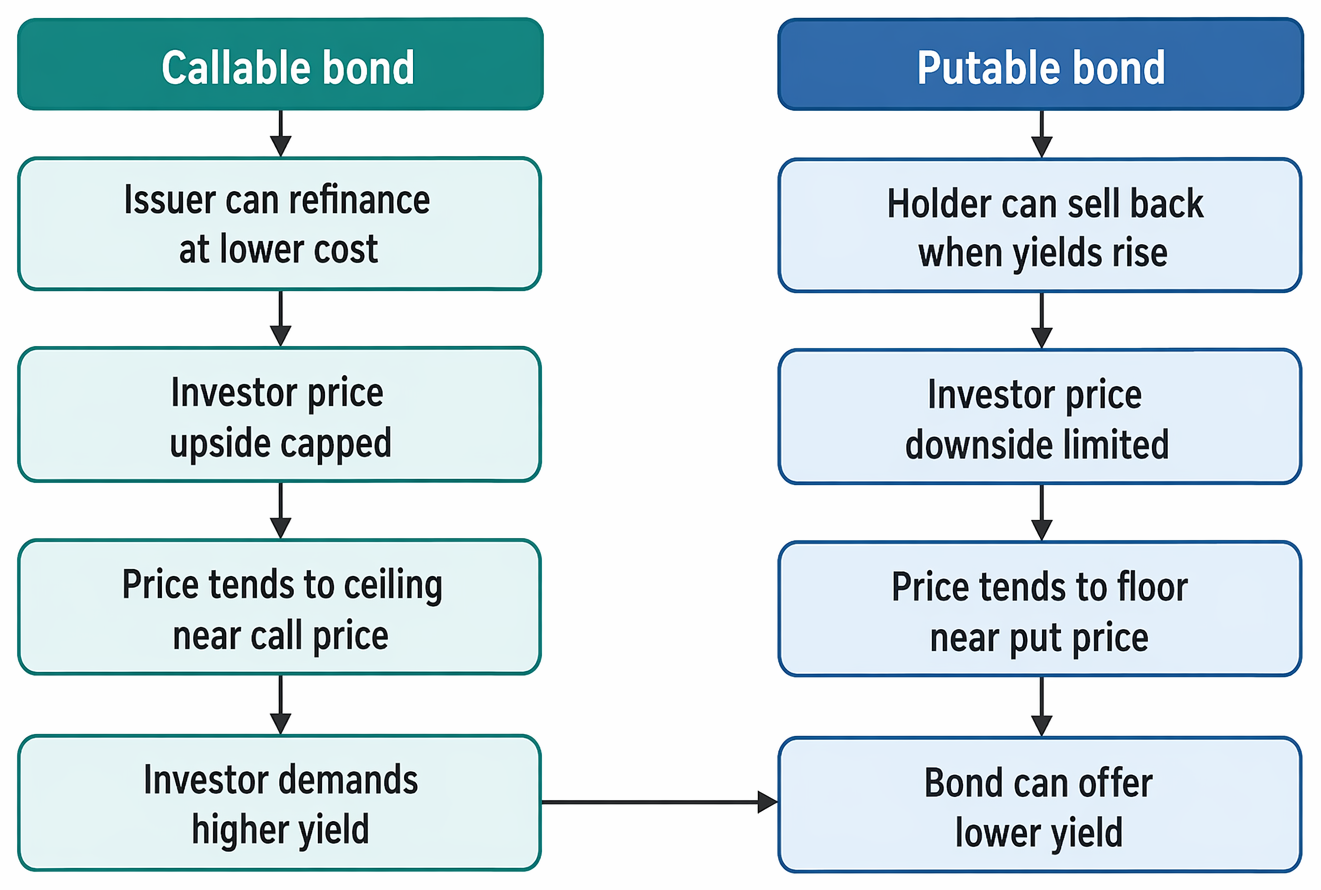

Callable Bonds

A callable bond gives the issuer the right to redeem (call) the bond early, usually after a non-callable period. Issuers are likely to call the bond when interest rates fall below the coupon rate, enabling refinance at a lower cost. As a result, the price upside for investors is capped. Holders of callable bonds therefore require a higher yield—known as the yield to worst—compared to otherwise similar non-callable bonds.

Putable Bonds

A putable bond gives the investor protection by allowing the holder to redeem the bond at par (or a predetermined price) prior to maturity, typically at set dates. This feature reduces price risk for bondholders, particularly when interest rates rise or issuer credit deteriorates. Therefore, putable bonds offer lower yields than similar non-putable issues.

Convertible Bonds

Convertible bonds contain an embedded option for bondholders to convert their bonds into a specified number of shares of issuer equity, typically at the holder’s discretion. This adds upside potential, as bondholders may convert when share prices are favorable, trading off some coupon/yield in exchange.

Sinking Fund Provisions and Others

Some bonds have a sinking fund, which requires the issuer to retire a portion of the principal periodically pre-maturity. While not an explicit option, this feature introduces partial call-like risk.

Less commonly, bonds may include caps, floors, or make-whole calls, each tailoring risk.

Implications for Pricing, Yield, and Risk

Embedded options always affect the value of a bond:

- Callable bonds: Investor risk increases, required yield increases, price ceiling exists (especially near call price as rates fall).

- Putable bonds: Investor risk decreases, required yield decreases, price floor exists (especially near put price as rates rise).

- Convertible bonds: Offer lower yields but greater upside due to conversion value.

The presence of options generally makes a bond’s cash flows less certain and requires option-adjusted yield analysis.

Key Term: option-adjusted yield

The yield on a bond after adjusting for the value of its embedded options, used to compare bonds with and without options on an equal basis.

How Optionality Alters Effective Duration and Volatility

Bonds with embedded options may show different price sensitivity to yields:

Callable and putable bonds are compared by issuer or holder exercise rights, associated price ceilings or floors, and yield implications.

- Callables: As rates fall, duration decreases, since the probability of call rises.

- Putables: As rates rise, duration also decreases, since bondholder may put.

- Convertibles: Effective duration depends on both interest rate and equity price movements.

For exam purposes, understanding that embedded options reduce or cap effective duration in certain regions is essential.

Worked Example 1.1

A 10-year, 5% fixed coupon bond is callable at par after 5 years. Market yields fall to 3%. What is the likely impact on the bond’s price, and why?

Answer:

As market yields fall below the coupon rate, the bond price would normally rise, but for a callable bond, the upside is capped as investors anticipate the bond will be called at par in five years. The bond will price close to its call price, and its yield will reflect the shorter expected life.

Worked Example 1.2

A 7-year bond gives the holder a put at par after 3 years. If market rates rise above the coupon, how does this feature affect investor risk?

Answer:

The put option protects the bondholder. If yields rise sharply, the bond price may not fall as far as a comparable non-putable bond, because the ability to redeem at par limits downside. Investors thus face lower interest rate risk.

Worked Example 1.3

A bond with a principal of $1,000 is convertible into 20 shares, with the current stock trading at $40. If the share price rises to $60, what happens to the value of the convertible bond?

Answer:

If the share price exceeds the conversion price ($50), it becomes optimal for the holder to convert. The bond’s value will approximate or exceed $1,200, offering upside versus comparable straight debt (which remains at or below par).Exam Warning: The yield to maturity on bonds with embedded options (such as call, put, or convert features) can be misleading for comparison. Use the yield to worst or, for advanced pricing, the option-adjusted yield for exam-style questions and analysis.

Revision Tip: On the exam, carefully read the bond’s features—including embedded options and redemption terms—to determine real cash flow risks and the investor’s position on optionality.

Summary

Embedded options significantly affect bondholder risk and return. Calls increase issuer flexibility, raising required yields for investors. Puts protect investors, reducing risk and yield. Convertible provisions trade yield for equity participation. Accurate valuation and risk assessment depend on option-adjusted analysis.

Key Point Checklist

This article has covered the following key knowledge points:

- Identify the standard cash flow pattern for a plain-vanilla bond

- Recognize and define common embedded options (call, put, conversion)

- Explain how call and put features affect cash flow timing and risk

- Describe the pricing/yield effects of embedded options for both investors and issuers

- Distinguish option-adjusted yield from nominal yield for comparison

- Apply option-related effects to bond risk assessment in exam questions

Key Terms and Concepts

- embedded option

- call option (on a bond)

- put option (on a bond)

- convertible option

- option-adjusted yield