Learning Outcomes

This article explains mortgage-backed securities (MBS) prepayments and cash flow modeling, including:

- understanding how borrower prepayments arise, how they are measured, and why they create cash flow uncertainty for MBS investors;

- applying key prepayment metrics such as the Single Monthly Mortality rate (SMM) and Conditional Prepayment Rate (CPR), and converting between them for exam-style calculations;

- interpreting the Public Securities Association (PSA) benchmark, scaling CPR for different PSA speeds, and using these assumptions to project MBS principal and interest cash flows;

- analyzing how changes in prepayment speeds affect average life, duration, yield, and the negative convexity profile of pass-through MBS and related securitized products;

- evaluating how prepayment risk gives rise to embedded call options in mortgage-backed structures, and assessing the implications for pricing, option-adjusted spreads (OAS), and risk management at the CFA Level 2 standard;

- contrasting different prepayment scenarios and PSA speeds in numerical examples, checking the internal consistency of assumptions, and interpreting results in terms of extension risk, contraction risk, and their impact on portfolio-level performance measures.

CFA Level 2 Syllabus

For the CFA Level 2 exam, you are expected to understand the prepayment features and cash flow modeling of mortgage-backed securities as part of your knowledge of embedded options and securitized products, with a focus on the following syllabus points:

- Explaining the mechanics of mortgage prepayments and their key drivers

- Describing methods for modeling mortgage prepayments, including the PSA benchmark

- Calculating and interpreting the effects of prepayments on MBS cash flows

- Analyzing the interaction between prepayments and embedded options in securitized products

- Evaluating prepayment risk implications for pricing and risk management of MBS

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What are the main factors that influence the speed of mortgage prepayments in mortgage-backed securities?

- Which industry-standard model is commonly used to express MBS prepayment rates?

- Why are the cash flows of pass-through MBS considered uncertain, even if there is no credit loss?

- How does the potential for prepayment create an embedded call option in a typical residential MBS?

Introduction

Mortgage-backed securities (MBS) are fixed income products whose principal and interest cash flows depend on payments from pools of residential or commercial mortgages. A unique feature of most MBS is the ability for the constituent borrowers to prepay, in full or part, before contractual maturity. Prepayments significantly affect the timing and amount of cash flows to investors, creating prepayment risk. This risk influences the valuation, duration, and embedded option characteristics of MBS structures. Accurately modeling and interpreting prepayments is essential for correct analysis of MBS, especially at Level 2 of the CFA exam.

Key Term: Prepayment

The unscheduled return of principal on a mortgage loan before its contractual maturity, typically due to refinancing, property sale, or voluntary borrower payment. Key Term: Prepayment Risk

The uncertainty faced by MBS investors arising from the variability in the estimated timing and amount of principal repayments due to borrower prepayments. Key Term: Embedded Option

An implicit feature within a security, such as the borrower's right to prepay a mortgage, which can be seen as a call option against the lender or investor.Test Tip: When revising Mortgage-backed securities prepayments and cash flow modeling, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Drivers of Mortgage Prepayments

Borrowers may prepay their mortgages for several reasons, including:

- Interest rate declines: Homeowners refinance at lower rates.

- Home sales: Borrowers repay loans when selling the property.

- Default and foreclosure: Liquidation of the mortgage leads to principal recovery.

- Curtailed payments: Partial prepayment of principal, often via extra monthly payments.

- Economic/seasonal factors: Changes in employment, consumer behavior, or tax-related motivations.

Prepayments tend to accelerate when market rates fall below the current mortgage rate, increasing the likelihood of refinancing.

Measuring Prepayment Speeds

Prepayments are quantified using several metrics:

Key Term: Single Monthly Mortality Rate (SMM)

The proportion of the remaining principal in a mortgage pool that is expected to be prepaid in a given month. Key Term: Conditional Prepayment Rate (CPR)

The annualized rate at which borrowers are expected to prepay the remaining principal on a pool of mortgage loans.

The SMM and CPR are linked by the formula:

The SMM gives a monthly view, while CPR expresses prepayment behavior on an annualized basis.

Standard Prepayment Models

To standardize prepayment modeling, the industry uses the Public Securities Association (PSA) benchmark:

Key Term: PSA Benchmark

A prepayment model that assumes low initial prepayments, ramping up for the first 30 months and then flattening, serving as a "standard" for expressing actual prepayment speeds.

The "100% PSA" model postulates:

- Annualized CPR begins at 0.2% in month 1, increases by 0.2% per month until reaching 6% at month 30.

- From month 31 onwards, CPR remains at 6%. “X% PSA” means prepayments are X% of the standard 100% PSA assumptions.

Worked Example 1.1

An MBS pool starts with $100 million principal. In month 12, the PSA speed is 150%. What is the SMM for that month?

Answer:

Under 100% PSA at month 12: CPR = 0.2% × 12 = 2.4%. At 150% PSA, CPR = 2.4% × 1.5 = 3.6%. SMM = 1 − (1 − 0.036)^(1/12) ≈ 0.00306, or 0.306% of principal prepaid in month 12.

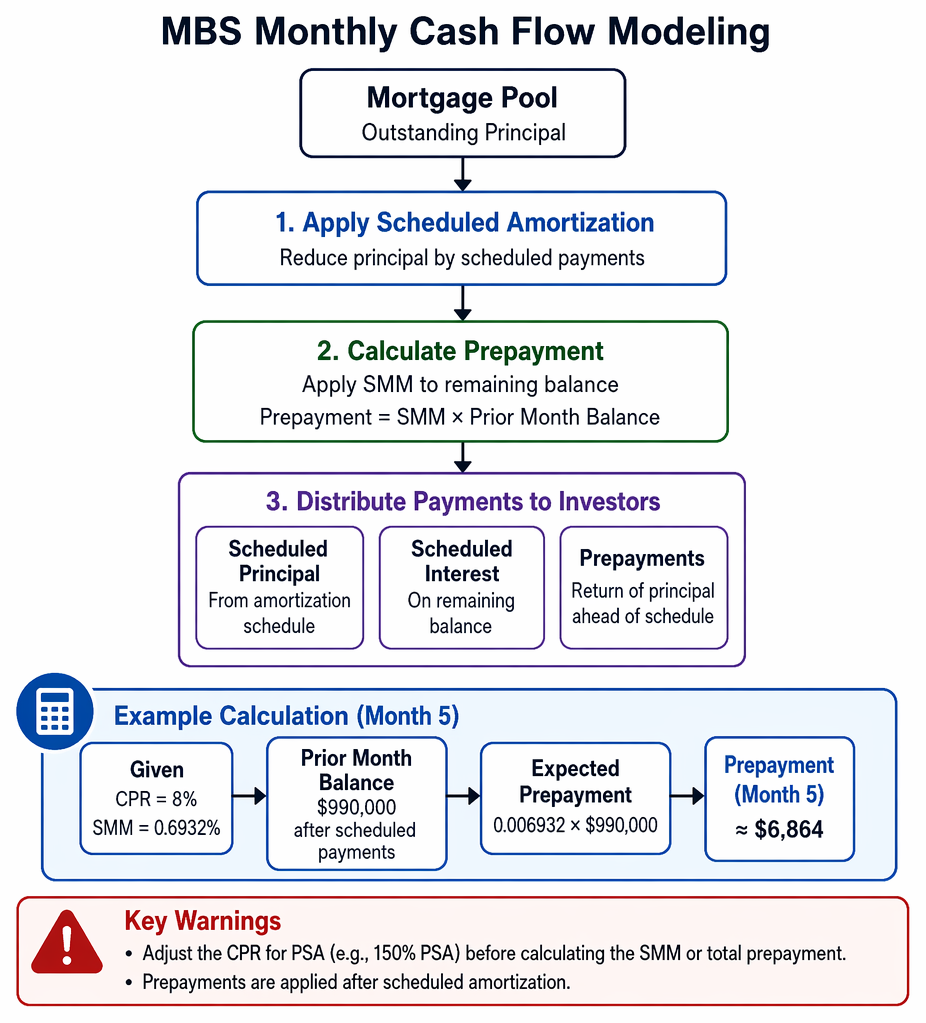

MBS Cash Flow Modeling

Pass-through MBS distribute monthly principal and interest to investors. Each payment consists of:

Mortgage cash flow modeling traces prepayment assumptions to monthly principal and interest, average life, duration, OAS, and extension or contraction risk.

- Scheduled principal (per amortization schedule)

- Scheduled interest

- Prepayments (reducing outstanding principal ahead of schedule)

Since prepayments are uncertain, models assume a CPR or SMM rate throughout the bond's life to project cash flows. Increasing prepayment speeds accelerate principal return, shortening average life and altering yield and duration metrics.

Worked Example 1.2

Question: Given a $1,000,000 mortgage pool, an annual CPR of 8%, and SMM of 0.6932%, how much prepayment is expected in month 5 after accounting for scheduled amortization?

Answer:

SMM = 1 − (1 − 0.08)^(1/12) ≈ 0.6932%. If the prior month's principal balance is $990,000 after scheduled payments, expected prepayment = 0.006932 × $990,000 ≈ $6,864.Exam Warning: Do not confuse the PSA prepayment model with actual prepayment experience. Exam questions may specify “at 150% PSA” or another rate; always adjust the CPR before calculating the SMM or total prepayment. Also, prepayments are applied after scheduled amortization.

Embedded Options in MBS: The Investor’s Viewpoint

MBS exhibit embedded call options as borrowers can prepay principal at any time. For the investor:

- When interest rates fall, prepayments accelerate (the pool is "called" away), limiting price gains.

- When rates rise, prepayments slow, extending the maturity of the pool ("extension risk"). This option-like feature leads to negative convexity in MBS price/yield profiles. Prepayment modeling is essential for pricing pass-through MBS, collateralized mortgage obligations (CMOs), and other deals with complex cash flow waterfalls.

Impact of Prepayment Modeling Assumptions

Prepayment modeling relies on historical patterns and assumptions about borrower behavior. Accurately assuming prepayment rates is necessary for:

- Estimating average life, duration, and yield

- Valuing embedded options and option-adjusted spreads (OAS)

- Measuring exposure to interest rate risk

Misestimating prepayment speeds leads to valuation and risk errors.

Worked Example 1.3

An MBS is priced assuming 100% PSA. If actual prepayments run at 200% PSA due to falling rates, what is the impact on the investor?

Answer:

Principal returns much faster than expected. Yield to maturity is likely lower than originally projected, as more principal is reinvested at new, lower market rates. Duration shortens, price appreciation is limited: classic prepayment risk.

Summary

Prepayments considerably affect the cash flows of mortgage-backed securities, making their performance dependent on interest rates and borrower behavior. Standard measures (SMM and CPR) and models (PSA) are used to estimate prepayment speeds and to model MBS cash flows. Prepayment risk introduces embedded options in MBS, leading to unique valuation and risk management needs. Accurate modeling of prepayments is essential for assessing the true risk and value of any MBS investment.

Key Point Checklist

This article has covered the following key knowledge points:

- Define prepayments and prepayment risk in mortgage-backed securities

- Recognize the factors driving prepayment behavior

- Apply CPR and SMM, and use the PSA benchmark model for prepayment assumptions

- Analyze how MBS cash flows can only be projected with assumed prepayment rates

- Understand the effect of prepayments on embedded call options in MBS

- Evaluate the valuation and risk implications of prepayment modeling errors

Key Terms and Concepts

- Prepayment

- Prepayment Risk

- Embedded Option

- Single Monthly Mortality Rate (SMM)

- Conditional Prepayment Rate (CPR)

- PSA Benchmark