Learning Outcomes

This article explains how key macroeconomic indicators are defined, measured, and interpreted for CFA Level 1, including:

- identifying the components of gross domestic product (GDP) and comparing expenditure, income, and output approaches to GDP measurement;

- distinguishing clearly between nominal and real GDP, using price indices and the GDP deflator to remove the effects of inflation and assess true economic growth;

- defining inflation and explaining how common indices such as the consumer price index (CPI) are constructed, used to calculate inflation rates, and interpreted in real‑world data releases;

- contrasting disinflation, deflation, and hyperinflation, and evaluating their economic consequences for growth, income distribution, and financial markets;

- defining the labor force, calculating unemployment and labor force participation rates, and interpreting changes in these measures across the business cycle;

- differentiating frictional, structural, and cyclical unemployment and linking each type to economic conditions;

- integrating GDP, inflation, and unemployment data to diagnose the phase of the business cycle, infer likely policy responses, and anticipate the implications for asset prices and investment decisions.

CFA Level 1 Syllabus

For the CFA Level 1 exam, you are required to understand how macroeconomic indicators—including GDP, inflation, and unemployment—are calculated and interpreted, with a focus on the following syllabus points:

- calculation and interpretation of gross domestic product (GDP) using expenditure, income, and output approaches;

- distinction between nominal and real GDP, including the use of price indices and the GDP deflator;

- measurement and effects of inflation, including how CPI, PPI, and other price indices are constructed and used;

- calculation and interpretation of unemployment rates, labor force participation, and types of unemployment;

- relationship among business cycles, GDP growth, inflation, and unemployment, including potential GDP and output gaps;

- basic implications of macroeconomic conditions for monetary and fiscal policy and for asset markets.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which statement best distinguishes nominal from real GDP?

- a) Nominal GDP includes exports while real GDP excludes exports.

- b) Nomimal GDP is measured at current prices, while real GDP is measured at constant base‑year prices.

- c) Nominal GDP adjusts for population, while real GDP does not.

- d) Nominal GDP excludes services, while real GDP includes services.

-

Which type of unemployment is most likely to persist even when the economy is operating close to its long‑run potential?

- a) Cyclical unemployment

- b) Structural unemployment

- c) Seasonal unemployment

- d) Demand‑deficient unemployment

-

A price index increases from 120 to 126 over one year. The annual inflation rate is closest to:

- a) 4.0%

- b) 5.0%

- c) 6.0%

- d) 26.0%

-

The unemployment rate falls from 7% to 6%, but the labor force participation rate also declines. This most likely indicates that:

- a) Employment has risen strongly because more people have entered the labor force.

- b) Employment has fallen because cyclical unemployment has increased.

- c) Some previously unemployed people have stopped looking for work and left the labor force.

- d) Structural unemployment has immediately fallen to zero.

Introduction

Macroeconomics studies the aggregate performance, structure, and behavior of national economies. Three central indicators—GDP, inflation, and unemployment—are essential for assessing a country's economic health and serve as the basis for policy analysis, economic forecasting, and CFA exam questions. These statistics are also key inputs in asset allocation, equity and fixed‑income valuation, and risk assessment.

Macroeconomic data appear regularly in economic calendars and market commentary. Analysts and exam candidates must not only know the formulas but also interpret the data: for example, to recognize that a surprise fall in the unemployment rate with firm inflation data may increase the probability of monetary tightening and hence put downward pressure on bond prices.

Macroeconomic statistics are estimates that are revised over time. First releases of quarterly GDP or monthly employment often rely on partial information and may be significantly revised as more data arrive. In practice, market participants compare the data both with previous values and with consensus forecasts, and they react most strongly to unexpected changes. For exam purposes, figures can be treated as exact, but it is useful to remember that real‑world data carry measurement uncertainty and that different countries may use slightly different definitions or methods.

Another practical detail is the way data are reported:

- Many series (such as GDP and industrial production) are seasonally adjusted to remove predictable calendar effects (for example, Christmas spending, Chinese New Year, or harvest seasons).

- Growth rates may be reported as:

- quarter‑on‑quarter annualized rates,

- simple quarter‑on‑quarter rates, or

- year‑on‑year rates (current quarter versus the same quarter a year earlier).

Always check what comparison is being used in a question before interpreting whether growth is accelerating or slowing. For instance, a quarter‑on‑quarter annualized rate of 3% may sound strong, but if the year‑on‑year rate has fallen from 4% to 3%, growth is actually slowing compared with the previous year.

Key Term: gross domestic product (GDP)

The total market value of all final goods and services produced within a country during a specified period, typically one year or one quarter.

GDP is a flow concept (measured “per period”) rather than a stock. Wealth or capital stock is measured at a point in time, but GDP measures how much value was produced during the period. This distinction between flows and stocks is frequently tested in conceptual questions.

Key Term: GDP per capita

Real GDP divided by the population, used as a rough measure of the average standard of living in an economy.

GDP per capita is only an approximation to welfare: it does not capture income distribution, leisure time, environmental quality, or non‑market activities. You should be aware of these limitations when an exam question asks you to evaluate statements about “living standards” based solely on GDP figures.

Even small differences in annual real GDP per capita growth matter a lot over long horizons because of compounding. For example, if one country grows at 2% per year and another at 4% per year, the second country’s income per person roughly doubles in about 18 years (using the rule of 70: ), while the first country takes about 35 years () to double.

Key Term: business cycle

Recurrent fluctuations in aggregate economic activity around a long‑term growth trend, typically described in terms of expansion, peak, contraction (recession), and trough.

GDP, inflation, and unemployment each behave differently across business cycle phases, and understanding these patterns is central for interpreting macroeconomic news in an investment context.

Test Tip: When revising GDP inflation and unemployment, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Exam Warning: Do not rely on keyword recognition alone; check the precise condition, exception, calculation step, or evidence the question requires.

GDP: Concepts and Calculation

Components of GDP

Gross domestic product (GDP) quantifies the value of economic activity within a country. There are three common methods for calculating GDP:

- expenditure approach: adds up total spending on final goods and services produced in the economy;

- income approach: sums all incomes earned by households and companies in the production of goods and services;

- output (product) approach: totals value added at each stage of production across the economy.

All three methods should yield the same overall GDP figure because total expenditure on final output equals total income earned from producing that output, which in turn equals total value added.

Key Term: final goods and services

Goods and services purchased by the final user and not used as inputs into the production of other goods and services.

Intermediate goods (such as steel used to make cars) are deliberately excluded to avoid double counting; they are captured indirectly through value added.

Under the expenditure approach, GDP is usually decomposed as:

where:

- : consumption expenditure by households (durables, non‑durables, services);

- : gross private investment (business capital spending, residential construction, and inventory investment);

- : government spending on goods and services (but not transfer payments such as pensions or unemployment benefits);

- : exports of goods and services;

- : imports of goods and services.

Key Term: expenditure approach

A method of measuring GDP by summing spending on final goods and services: consumption, investment, government purchases, and net exports (exports minus imports).

Some clarifications that are frequently tested:

-

Consumption (C): Includes spending by households on:

- durable goods (for example, cars, appliances),

- non‑durable goods (for example, food, clothing), and

- services (for example, healthcare, education, transport, financial services). Services are now the largest share of consumption in many advanced economies.

-

Investment (I): In macroeconomics, “investment” means physical capital formation, not the purchase of financial assets. It includes:

- business spending on plant, equipment, and software;

- residential construction (new houses and apartments); and

- changes in inventories (stocks of unsold goods). If inventory levels rise, that counts as additional investment in the current period; if they fall, investment is negative.

-

Government spending (G): Includes government purchases of goods and services (teachers’ salaries, military equipment, infrastructure). Transfer payments (for example, social security, unemployment benefits, pensions) are excluded because they are not payments for current production; they will be reflected in GDP only when recipients spend them.

-

Net exports (X − M): Exports add to domestic GDP because they are domestically produced goods and services sold abroad. Imports are subtracted because they were included in C, I, or G but are not produced domestically.

Imports are subtracted to ensure that GDP measures domestic production only. For example, if a household buys a foreign‑made car, it is counted in consumption (C) and subtracted in imports (M), so it has no net effect on domestic GDP.

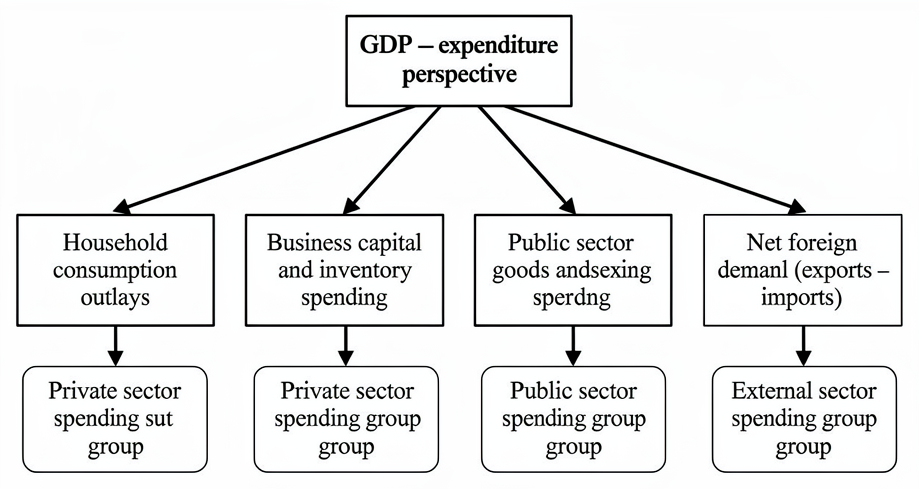

In macro analysis it is often useful to group expenditure components into those undertaken by:

- the private sector ( and ),

- the government sector (), and

- the foreign sector ().

These groupings help when thinking about how changes in household saving, government budget balances, or trade balances will affect total demand and GDP. For example, a larger government budget deficit (higher relative to tax revenue) must, in aggregate, be financed by some combination of higher private saving, lower private investment, or increased borrowing from abroad (a larger current‑account deficit). Level 1 does not require you to manipulate the full set of national income identities, but recognizing that the accounts must balance sharpens intuition about macro questions.

Some typical exam‑style classifications:

- A newly built house purchased by a household: counted in I (residential investment), not in C.

- A firm buying new machinery: counted in I (business investment).

- Government paying interest on its outstanding debt: not part of G in the GDP identity; it is a transfer of income.

- A foreign tourist staying in a domestic hotel: part of C and also counted as an export (X), because it is a non‑resident purchasing a domestic service.

Under the income approach, GDP is the sum of all income earned in the production of goods and services:

- wages and salaries (including benefits),

- interest,

- rent,

- corporate profits,

- mixed income of unincorporated businesses, and

- indirect taxes less subsidies and depreciation (capital consumption allowance).

Key Term: income approach

A method of measuring GDP by summing all income earned by factors of production in the economy, including wages, interest, rent, and profit, plus adjustments for taxes and depreciation.

In compact form, national income is often expressed as:

- employee compensation (wages, salaries, benefits),

- corporate profits,

- interest and rent,

- indirect taxes minus subsidies, and

- depreciation (capital consumption).

In exam problems, you may be given several of these components and asked to compute GDP by the income approach. The key is to include only income generated from current production, not pure transfers such as gifts or social benefits.

Because the national accounts are compiled from many different data sources (tax records, business surveys, household surveys), the totals from the expenditure, income, and output approaches will not match perfectly. Statistical agencies therefore include a small statistical discrepancy term so that, after adjustment, all three approaches are consistent. In exam problems, the data are usually constructed so that the approaches match exactly.

Two important words in “gross domestic product”:

- Gross: Means before deducting depreciation (capital consumption). If we subtract depreciation from GDP, we obtain net domestic product, a measure of new value created after allowing for wear and tear of the capital stock.

Key Term: net domestic product (NDP)

GDP minus capital consumption (depreciation); it measures the value of new production after accounting for the wear and tear on existing capital.

Depreciation is often called the capital consumption allowance. If gross investment in an economy just equals depreciation, the capital stock is constant; only when gross investment exceeds depreciation does the productive capacity of the economy expand.

- Domestic: Means production within the country’s borders, regardless of who owns the factors of production. By contrast, gross national product/income (GNP/GNI) measures output produced by the country’s residents (nationals), whether at home or abroad.

Key Term: gross national income (GNI) / gross national product (GNP)

The total income (or value of output) earned by a country’s residents, regardless of where production takes place, including net income from abroad.

For example, profits earned by a domestic company’s factory overseas contribute to that country’s GNI but not to its GDP; profits remitted abroad by foreign‑owned firms operating domestically add to GDP but not to GNI.

Questions may ask which measure is more relevant. GDP is usually used for analyzing short‑run activity and business cycles; GNP/GNI is used when the focus is on the income of residents (for example, for external debt sustainability or household income analysis).

The output (product) approach is based on the concept of value added.

Key Term: output (product) approach

A method of measuring GDP by summing the value added at each stage of production of all goods and services in the economy. Key Term: value added

The difference between the selling price of a product and the cost of intermediate goods used to produce it, measured at each stage of production.

To see this clearly, consider the following simplified production chain (amounts in dollars):

- Producers of basic materials supply inputs (steel, plastics, semiconductors) to a car assembler with total sales of 5,000; because these producers do not buy intermediate inputs within this simplified example, their value added is 5,000.

- The car assembler buys these inputs and sells the finished car to a dealer for 15,000; the assembler’s value added is 10,000 (15,000 − 5,000).

- The dealer sells the car to the final consumer for 18,000; the dealer’s value added is 3,000 (18,000 − 15,000).

Total value added is 5,000 + 10,000 + 3,000 = 18,000, which equals the retail price paid by the consumer. This 18,000 is what appears in GDP.

Many statistical agencies also report GDP by industry, based on this value‑added approach. Analysts can then see how much sectors such as manufacturing, construction, financial services, and information technology contribute to overall growth, which is useful in sector allocation decisions.

Worked Example 1.1

A country produces a car with a retail price of 30,000. The assembler buys 10,000 worth of imported parts and 5,000 of domestically produced materials. The assembler’s other costs are 8,000 of domestic wages. The dealer buys the car from the assembler for 28,000 and sells it for 30,000. What is the contribution to domestic GDP from this car?

Answer:

We must count only domestic value added. Assembler:

- Domestic intermediate inputs: 5,000 of materials (imported parts are excluded because they are not domestic production).

- Other domestic factor cost: wages = 8,000.

- Value of output: 28,000 (price to dealer).

Assembler’s value added is the sale value minus domestic intermediate inputs: 28,000 − 5,000 = 23,000. This 23,000 covers wages plus profit and depreciation. Dealer:

- Buys at 28,000, sells at 30,000.

- Dealer’s value added = 2,000.

Total contribution to domestic GDP is assembler value added (23,000) plus dealer value added (2,000) = 25,000. Imported parts are excluded because they add to foreign GDP, not domestic GDP.

What Is Included and Excluded in GDP

Most goods and services counted in GDP are traded in markets, where prices are observable. Two important exceptions are included at imputed values:

- owner‑occupied housing: treated as if homeowners rent the house to themselves; statistical agencies impute a rental value that enters GDP as both income and expenditure;

- government services: output of police, judges, firefighters, and civil servants is valued at its cost (mainly wages), because there is no market price.

Key Term: underground economy

Economic activity that is not recorded in official statistics, either because it is illegal or because it is deliberately concealed to evade taxes or regulation.

These imputed values are necessary so that shifts from renting to owning, or from private to public provision of services, do not artificially distort GDP.

Many activities are excluded from GDP:

- unpaid household work (cooking, cleaning, childcare for one’s own family);

- underground economy (unreported legal work and illegal activities);

- pure financial transactions (trading existing shares or bonds) and sales of used goods;

- barter transactions between households.

If you buy a used car from another household, no new car is produced; the transaction simply transfers ownership of an existing asset, so it is not counted in current GDP. However, the dealer’s commission and any repairs undertaken as part of the sale are included as current services.

These exclusions mean that official GDP may understate actual economic activity, especially in economies with large informal sectors. Some estimates suggest that the underground economy is equivalent to around 8% of recorded GDP in some large advanced economies and can reach around 60% in some developing economies. That implies that national accounts for such countries may miss a substantial share of true economic activity, and cross‑country comparisons of GDP are less precise than the raw numbers suggest.

In exam questions, be ready to classify whether specific transactions:

- add to GDP now (for example, a newly built house, payment to a doctor),

- do not affect current GDP (for example, purchase of existing shares),

- or only affect GDP through associated services (for example, brokerage commission, real‑estate fees).

Worked Example 1.2

Which of the following increases the current year’s GDP?

- A used machine is sold from Firm A to Firm B through a broker.

- A household pays a contractor to renovate its kitchen.

- A government increases unemployment benefits.

Answer:

- Used machine: the machine itself is not newly produced, so its sale does not enter GDP. However, the broker’s commission is a current service and thus adds to GDP.

- Kitchen renovation: payment to the contractor is for newly produced services and materials, so it increases GDP.

- Unemployment benefits: these are transfer payments, not payments for current production, so they do not directly enter GDP.

Therefore, the contractor’s services (and the broker’s commission in 1) increase GDP; the used asset and the pure transfer do not.

GDP and Economic Welfare

GDP is central for macro analysis but is not a perfect measure of welfare:

- It does not reflect income distribution. Two countries can have the same GDP per capita, but one may have much more inequality.

- It omits non‑market production (home production, volunteer work).

- It does not deduct environmental degradation or resource depletion.

- It ignores changes in leisure time and working conditions.

- It does not directly capture health outcomes, education quality, or life expectancy.

For CFA Level 1, be able to recognize statements that over‑interpret GDP per capita as a measure of “well‑being” and point out these limitations. In addition, high measured GDP growth that relies on depleting natural resources or generating high pollution may not be sustainable in the long run.

International comparisons of welfare often adjust GDP using purchasing power parity (PPP) exchange rates, which attempt to reflect differences in price levels across countries. PPP‑adjusted GDP per capita can give a more realistic comparison of living standards than market exchange rates, especially between rich and poor countries.

Key Term: purchasing power parity (PPP) exchange rate

An exchange rate constructed so that a basket of goods and services costs the same in two countries when priced in a common currency, used to compare real purchasing power across countries.

The detailed mechanics of PPP are not required at Level 1, but you should know that simple conversion at market exchange rates can be misleading. For example, prices of non‑traded services (such as haircuts) are often much lower in developing economies, so their PPP‑adjusted income is higher than suggested by market exchange rates.

Nominal vs. Real GDP

Nominal GDP is measured at current market prices and can be affected by changes in both output and price levels. Real GDP adjusts for inflation by valuing current output using the prices from a chosen base year. This comparison eliminates the effect of price changes and reflects true economic growth.

Key Term: nominal GDP

GDP measured at current market prices, reflecting both changes in quantities and changes in prices. Key Term: real GDP

GDP measured at constant prices of a base year, which reflects changes in quantities rather than prices.

Formally:

-

Nominal GDP in year :

where is the vector of current prices and the vector of current quantities.

-

Real GDP in year (with base year ):

Real GDP growth measures how rapidly the volume of output is expanding. Per capita real GDP growth adjusts this for population growth and is often used as a measure of changes in average living standards.

A simple example reinforces the distinction. Suppose an economy produces only cars:

- In 2019 it produces 300,000 cars at an average price of 18,750; nominal (and real, if 2019 is the base year) GDP is 5.625 billion.

- In 2020 it still produces 300,000 cars, but the price rises by 7% to 20,062.5. Nominal GDP rises to about 6.019 billion, up 7%, even though real output is unchanged. Real GDP in 2020, valued at 2019 prices, is still 5.625 billion.

This example shows why nominal GDP growth is not a reliable measure of real economic progress when the price level is changing.

In practice, statistical agencies often use chain‑weighted indices, where the base year is updated regularly to reduce distortions from large relative price changes (for example, when the price of computers falls rapidly while their quality improves).

Key Term: chain‑weighted index

A real GDP or price index constructed by frequently updating the base year, reducing bias from large changes in relative prices.

For CFA Level 1, you can usually assume a fixed base year unless the question explicitly mentions chain‑weighting.

Practical Interpretation

Suppose nominal GDP grows by 10% while prices rise by 6%. The approximate real GDP growth rate is:

Here is the nominal GDP growth rate and the inflation rate.

For small changes, this subtraction is a good approximation; for higher rates, use the exact formula:

Real GDP growth is what matters for long‑run improvements in living standards and for analyzing where an economy is relative to its long‑run potential.

GDP Deflator and Economic Growth

To separate price changes from quantity changes, economists use the GDP deflator.

Key Term: GDP deflator

A price index calculated as (Nominal GDP / Real GDP) × 100, reflecting the overall level of prices for all domestically produced final goods and services.

The GDP deflator for year can also be written as:

Equivalently:

GDP growth rates are usually reported in real terms to assess actual increases in output.

Worked Example 1.3

A country produces 1 trillion worth of goods and services in Year 1 at that year's prices. In Year 2, nominal GDP rises to 1.08 trillion, but prices have increased by 3%. What is real GDP growth?

Answer:

Nominal GDP growth is:

If prices rose by 3%, then, approximately:

For more precision, use:

so real GDP growth is about 4.85%. For small rates, the subtraction approximation is acceptable in the exam.

Worked Example 1.4

In a certain year, an economy’s nominal GDP is 6,000 billion. The value of that same year’s output at base‑year prices is 5,000 billion. Calculate the GDP deflator and interpret the result.

Answer:

A GDP deflator of 120 means that the overall price level for domestically produced final goods and services is 20% higher than in the base year. The 20% is the cumulative inflation since the base year.

Worked Example 1.5

The nominal GDP of a country is 8,400 billion, and its GDP deflator is 140 (base year = 100). What is real GDP, and by how much have prices risen compared with the base year?

Answer:

- Real GDP:

So real GDP is 6,000 billion in base‑year prices.

- Price increase: A deflator of 140 means the price level is 40% higher than in the base year.

Worked Example 1.6

Suppose the price index in Year 1 is 100, and in Year 2 it is 104. What is the annual inflation rate?

Answer:

A reading of “4% CPI inflation” typically means the CPI is 4% higher than one year earlier.

Besides the CPI, other important indices include:

Key Term: producer price index (PPI)

A price index that measures the average change over time in prices received by domestic producers for their output, often broken down by industry or stage of processing.

The PPI (or wholesale price index) can be an early indicator of future consumer inflation if rising producer costs are passed on to consumers.

The items in a PPI often include:

- fuels and energy products;

- agricultural commodities;

- manufactured intermediate goods (chemicals, metals);

- capital goods (machinery and equipment); and

- finished consumer goods.

They are sometimes grouped by stage of processing (crude materials, intermediate goods, finished goods). Because PPI baskets differ widely across countries depending on their industrial structure, PPIs are less comparable internationally than CPIs.

CPI Baskets and International Differences

The CPI basket and weights differ across countries and over time:

- In many emerging economies, food often has a very high weight (for example, 30–50% of the basket), so food price shocks have a big impact on measured inflation.

- In advanced economies, housing and services typically have larger weights, and food is a smaller share.

For example, one comparison of CPI baskets found approximate weights:

- food and beverages: around 30–47% in some large developing economies, but closer to 15% in some advanced economies;

- housing and utilities: above 30% in several advanced economies, but lower in some developing economies.

The scope of the CPI also varies:

- Some indices cover both urban and rural households.

- Others (such as the US CPI‑U) cover only urban consumers.

- Some indices, like the US personal consumption expenditures (PCE) deflator, use business surveys and cover all consumer spending, not just a fixed household basket.

Central banks choose specific indices for policy:

- The European Central Bank focuses on the Harmonised Index of Consumer Prices (HICP).

- The US Federal Reserve focuses on the PCE price index, partly because it has smaller upward biases than the CPI‑U and covers a broader range of spending.

When comparing inflation rates across countries in a question, always consider that differences may partly reflect different baskets and weights, not just different economic conditions.

Many contracts and financial instruments are indexed to price indices:

- inflation‑linked government bonds (such as US Treasury Inflation‑Protected Securities, TIPS) adjust principal according to a CPI;

- long‑term rental agreements and commercial leases often include clauses that adjust rents periodically with CPI;

- wage contracts in some economies are indexed (formally or informally) to consumer prices.

Indexation reduces the effect of inflation on real incomes but can also make inflation more persistent by automatically feeding past price increases into future wages and rents.

Headline versus Core Inflation

Key Term: headline inflation

The inflation rate calculated from a broad price index that includes all goods and services, such as the overall CPI. Key Term: core inflation

The inflation rate calculated from a price index that excludes volatile items, typically food and energy, to better capture fundamental inflation trends.

Because food and energy prices are highly volatile (due to weather, geopolitical events, and commodity market swings), headline inflation can bounce around from month to month. Policymakers often focus on core inflation to avoid overreacting to temporary price spikes that may not persist.

Many central banks target inflation in terms of a consumer price index, but they use core measures as a guide to the persistent trend. In a typical policy report, you might see:

- headline CPI inflation (all items);

- core CPI inflation (excluding food and energy); and sometimes

- additional trimmed‑mean or median measures that further reduce the influence of outliers.

Understanding which measure is being targeted helps interpret central bank communication and likely interest rate decisions.

Types of Inflation

- disinflation: a decline in the inflation rate (prices still rise, but more slowly);

- deflation: a sustained fall in the general price level (negative inflation);

- hyperinflation: extremely high and typically accelerating inflation, often defined as monthly inflation exceeding 50%.

Key Term: disinflation

A decrease in the rate of inflation; prices are rising but at a slower pace than before. Key Term: deflation

A persistent decline in the general price level, leading to an increase in the real value of money. Key Term: hyperinflation

An exceptionally high and rapidly accelerating inflation rate, usually associated with a collapse in the value of money and severe economic disruption.

Hyperinflation episodes have occurred historically in some economies where annual inflation rates reached thousands or even millions of percent. At Level 1 you do not need to know specific historical numbers, but you should understand the typical consequences: currency collapse, a shift to barter or foreign currencies, and severe damage to financial markets and long‑term contracting.

Deflation is particularly dangerous because falling prices can increase the real burden of debt, encourage households and firms to postpone spending, and potentially trigger a downward economic spiral.

Worked Example 1.7

Which of the following statements is most accurate?

- “Disinflation occurs when the overall price level falls.”

- “Deflation occurs when the inflation rate becomes negative.”

- “A 10% increase in the price of chicken necessarily raises the inflation rate.”

Answer:

Statement 2 is correct. Deflation refers to a negative inflation rate, meaning the overall price level declines. Statement 1 is incorrect because it describes deflation, not disinflation. Statement 3 is incorrect because inflation reflects the overall price level; a price increase for one item may be offset by declines elsewhere.

CPI Biases and Limitations

Because the CPI is based on a fixed basket, it tends to overstate the true cost of living in an inflationary environment:

- Substitution bias: Consumers respond to relative price changes by substituting cheaper goods for more expensive ones (for example, buying more chicken and less beef if beef becomes relatively expensive). A fixed basket assumes no substitution and thus overstates the increase in the cost of maintaining a given level of utility.

- Quality bias: Improvements in product quality (for example, better mobile phones or medical treatments) often raise prices, but part of the price rise reflects higher quality, not pure inflation. Although statistical agencies attempt to adjust for quality, such adjustments are imperfect.

- New product bias: New goods and services may not be added to the basket immediately, so the CPI can initially miss changes in spending patterns.

- Outlet substitution bias: Consumers may shift toward discount retailers or online shopping when prices rise, but a fixed basket that assumes traditional outlets can overstate the cost of achieving a given standard of living.

Over time, statistical agencies revise baskets and methodologies, but some upward bias remains. This is why some central banks, such as the US Federal Reserve, prefer broader indices like the PCE deflator when assessing inflation trends.

In exam questions, if you are asked how a fixed‑basket price index behaves in an inflationary environment, the correct answer is typically that it overstates the increase in the cost of living. This bias implies that:

- real wages based on CPI may be understated;

- real GDP growth measured using CPI may be slightly understated over long horizons.

Using Price Indices to Deflate Nominal Variables

Analysts frequently convert nominal variables into real terms using price indices.

For a nominal variable (for example, nominal wage, sales revenue) and a price index (for example, CPI, GDP deflator), the real value in base‑year prices is:

For interest rates, the approximate real interest rate is:

where is the expected inflation rate.

Key Term: real interest rate

The nominal interest rate adjusted for inflation, approximated by nominal rate minus expected inflation.

In practice, the choice of price index used to deflate will depend on the application:

- To express household incomes or wages in real terms, a consumer price index is appropriate.

- To analyze a firm’s real revenues, an index corresponding to its output prices (such as a sector‑specific PPI) may be better.

- To convert nominal GDP into real GDP, the GDP deflator is used.

Worked Example 1.8

An investor earns a nominal return of 7% on a bond in a year when CPI inflation is 3%. What is the approximate real return?

Answer:

The approximate real return is:

For most CFA Level 1 questions, this subtraction method is sufficient.

For more precision, you could use the exact Fisher relationship:

but this is rarely required at Level 1.

Causes of Inflation

Three broad explanations are emphasized in the curriculum:

- demand‑pull inflation;

- cost‑push inflation;

- monetarist (monetary) view.

Key Term: demand‑pull inflation

Inflation caused by increases in aggregate demand when the economy is operating near or above potential output. Key Term: cost‑push inflation

Inflation caused by rising production costs (such as wages or raw material prices) that shift short‑run aggregate supply leftward. Key Term: monetarist view of inflation

The view that sustained inflation is fundamentally a monetary phenomenon arising when money supply grows faster than real output.

-

Demand‑pull inflation: Occurs when aggregate demand (total spending) grows faster than the economy’s productive capacity. In terms of aggregate demand and supply, the AD curve shifts right faster than aggregate supply, pushing both real GDP and the price level higher.

-

Cost‑push inflation: Occurs when rising production costs (for example, wages, raw materials, oil prices, imported input costs) shift the short‑run aggregate supply (SRAS) curve to the left, resulting in higher prices and lower output.

-

Monetarist view: Emphasizes that in the long run, sustained inflation is linked to excessive growth of the money supply relative to real output (“too much money chasing too few goods”). Rapid money growth ultimately shows up as higher nominal spending and inflation.

In practice, episodes of inflation often involve a mix of these forces, together with inflation expectations.

Key Term: inflation expectations

The rate of inflation that households, firms, and investors anticipate in the future, which can influence wage bargaining, price setting, and interest rates.

Indicators of Demand‑Pull Inflation

Analysts look at:

- GDP relative to potential GDP (output gaps);

- capacity utilization rates (for example, when factories operate near 82–85% of capacity, bottlenecks and price pressures tend to emerge);

- growth of money supply and credit relative to nominal GDP;

- strong commodity prices as a possible sign of global demand pressure.

Key Term: capacity utilization

A measure of how fully production capacity (plant and equipment) is being used, typically expressed as a percentage of potential output.

When actual output is close to or above potential GDP and capacity utilization is high, firms may find it difficult to meet demand without raising prices, generating demand‑pull inflation.

Indicators of Cost‑Push (Wage‑Push) Inflation

Cost‑push inflation is often linked to:

- rising unit labor costs (wages rising faster than productivity);

- sharp increases in key input prices (oil, basic materials);

- sustained depreciation of the domestic currency, which raises import prices.

Key Term: unit labor cost (ULC)

Labor compensation per unit of output, often calculated as total hourly compensation divided by output per hour:

where W is wage per hour and O is output per hour.

When unemployment falls below the natural rate (discussed later) and wage growth outpaces productivity growth, firms’ costs per unit of output rise, putting upward pressure on prices.

To detect cost‑push pressure, practitioners compare:

- wage growth versus productivity growth; and

- current unemployment versus its estimated natural rate or NAIRU (non‑accelerating inflation rate of unemployment).

If unit labor cost growth is persistently high while unemployment is low, it is a sign that cost‑push inflation may be building.

Money Growth and Velocity

Monetarist analysis often looks at money growth relative to nominal GDP. Another related concept is the velocity of money.

Key Term: velocity of money

The ratio of nominal GDP to the money supply, indicating how frequently a unit of money is used to purchase final goods and services:

If money supply grows much faster than nominal GDP (or if velocity rises sharply), inflationary pressures are likely to build. If money growth lags nominal GDP (or velocity falls), there may be disinflationary or deflationary pressure.

Practitioners track:

- trends in monetary aggregates (for example, M2);

- whether money growth is accelerating or decelerating relative to its historical trend;

- whether money growth is outpacing or lagging nominal GDP.

If money growth accelerates and exceeds nominal GDP growth, especially when the economy is near potential output, the risk of higher inflation is elevated.

Inflation Expectations

Once inflation becomes embedded in an economy, expectations can sustain it:

- Workers bargain for higher wages anticipating future inflation.

- Firms preemptively raise prices to keep pace with expected cost increases.

- Lenders demand higher nominal interest rates to compensate for expected inflation.

This can create an inflationary momentum even after the original shock (for example, an oil price spike) has faded—an important ingredient in episodes of stagflation (explained later).

Measuring expectations is not straightforward, but analysts may use:

- surveys of households and firms;

- extrapolation from past inflation trends;

- the difference between yields on nominal government bonds and inflation‑indexed bonds (break‑even inflation).

If a 10‑year nominal bond yields 3.5% and a 10‑year inflation‑linked bond yields 1.5%, markets are implicitly pricing in about 2% average inflation over the next 10 years, subject to caveats about liquidity and risk premia.

Expectations can also be influenced by central bank credibility. If the central bank has a track record of maintaining inflation near its target, inflation expectations may remain anchored even in the face of temporary shocks, making it easier to keep inflation under control.

Consequences of Inflation and Deflation

Moderate, predictable inflation is typically compatible with healthy economic growth. However:

- High or volatile inflation:

- blurs the information content of prices, making it harder for firms and households to make decisions;

- distorts tax burdens (for example, if nominal interest income is taxed without full inflation adjustment);

- redistributes wealth between borrowers and lenders (unexpectedly high inflation benefits borrowers and hurts lenders, and vice versa);

- increases uncertainty, discouraging long‑term investment.

For financial markets:

-

nominal bonds are particularly vulnerable to unexpected increases in inflation (real returns fall, yields rise, prices decline);

-

equities may provide some hedge in the long run (as nominal earnings and dividends can grow with prices), but high inflation often coincides with higher discount rates and valuation pressures;

-

real assets (real estate, commodities) can perform relatively well when inflation surprises on the upside.

-

Deflation:

- reduces nominal revenues while debt obligations remain fixed, raising real debt burdens;

- may induce firms to cut investment and employment, deepening recessions;

- can lead to expectations of further price falls, postponing consumption and investment;

- can make monetary policy less effective, especially when nominal interest rates approach zero.

Key Term: stagflation

A macroeconomic situation characterized by high unemployment and high inflation, typically arising from negative supply shocks that shift short‑run aggregate supply leftward.

Stagflation cannot be identified from a high inflation rate alone; it requires the combination of high inflation and high unemployment.

Historical episodes such as the 1970s oil shocks illustrate stagflation: sharp increases in oil prices raised firms’ costs, shifting aggregate supply left. Output fell and unemployment rose, yet inflation increased because higher input costs drove up prices. Central banks then faced a difficult trade‑off between supporting growth and controlling inflation.

Exam questions may deliberately present you with inflation and unemployment data together; recognising that “high inflation and high unemployment” is characteristic of a negative supply shock is a common test.

Exam warning: Inflation rates calculated using different baskets or weights (CPI, PPI, GDP deflator) can diverge. When comparing inflation data, always note which index is being used and whether figures are year‑on‑year or month‑on‑month.

Unemployment: Concepts and Categories

Defining and Calculating Unemployment

Unemployment measures the share of the labor force actively seeking but not finding work.

Key Term: working‑age population

The segment of the population typically aged 15–64 (definition varies by country) and considered old enough to work. Key Term: labor force

All people of working age who are either employed or actively seeking employment.

People who are neither working nor looking for work (students, retirees, full‑time homemakers, discouraged workers who have stopped searching) are not in the labor force.

To be classified as unemployed, an individual must typically:

- be without work during the reference period;

- be available for work; and

- have actively sought work (for example, applied for jobs) during a recent period (often the last four weeks).

Key Term: unemployment rate

The percentage of the labor force that is without a job and actively looking for work:

A related measure is the labor force participation rate.

Key Term: labor force participation rate

The percentage of the working‑age population that is in the labor force (employed or unemployed and seeking work):

A falling unemployment rate accompanied by a falling participation rate may signal that people are leaving the labor force, not necessarily that employment is booming.

Key Term: discouraged worker

A person who would like to work but has stopped actively looking for a job because they believe none are available; such individuals are not counted as unemployed and are excluded from the labor force.

Some countries also publish broader measures of labor underutilization that include discouraged workers and those working part‑time involuntarily.

Worked Example 1.9

A country has 1.5 million unemployed, a labor force of 25 million, and a total working‑age population of 40 million. What are the unemployment and labor force participation rates?

Answer:

Unemployment rate:

Labor force participation rate:

An analyst would typically track these rates over time. For example, a fall in unemployment to 5% with participation falling to 60% could indicate that some job‑seekers have given up and left the labor force instead of finding jobs.

Worked Example 1.10

In Year 1, a country has a working‑age population of 50 million, of which 30 million are in the labor force and 2.4 million are unemployed. In Year 2, the labor force is still 30 million, but only 1.8 million are unemployed. Calculate the unemployment rate in both years and interpret the change.

Answer:

Year 1:

- Unemployment rate:

Year 2:

- Unemployment rate:

Interpretation: The unemployment rate fell from 8% to 6%. Because the labor force is unchanged, this reflects a genuine increase in employment, not a change in participation. If the labor force had also fallen, we would need to examine whether people left the labor force instead of finding jobs.

In real‑world data, analysts often also look at:

- employment‑to‑population ratio: employed divided by working‑age population;

- average duration of unemployment: which tends to lengthen in recessions;

- breakdowns by age, education, and region.

These details help distinguish between cyclical changes and deeper structural issues in the labor market.

Types of Unemployment

Unemployment has different causes and therefore different policy implications.

- frictional unemployment: short‑term unemployment as people move between jobs, change careers, or enter the labor force;

- structural unemployment: results from mismatches between workers' skills or locations and job requirements;

- cyclical unemployment: arises from downturns in the business cycle, when aggregate demand is insufficient.

Key Term: frictional unemployment

Unemployment arising from normal labor market turnover as people voluntarily change jobs or enter/re‑enter the labor force. Key Term: structural unemployment

Unemployment resulting from changes in the structure of the economy that eliminate some jobs while creating others for which displaced workers may not be qualified or suitably located. Key Term: cyclical unemployment

Unemployment linked to the fluctuations of the business cycle, increasing during recessions and falling in expansions.

Examples:

- A new graduate searching for a first job is frictionally unemployed.

- A coal miner who loses his job because power generation shifts to natural gas and renewables is structurally unemployed if he cannot easily transition to a new sector.

- A factory worker laid off during a recession when demand falls is cyclically unemployed.

Even when the economy is operating at its long‑run potential, some frictional and structural unemployment will persist.

Key Term: natural rate of unemployment

The rate of unemployment that prevails when the economy is at potential GDP, consisting mainly of frictional and structural unemployment, with cyclical unemployment equal to zero.

This is sometimes referred to as the non‑accelerating inflation rate of unemployment (NAIRU): at this rate, unemployment does not create upward or downward pressure on inflation.

In practice, the natural rate / NAIRU is not directly observable and can change over time due to factors such as:

- demographics (age structure of the population);

- labor market institutions (minimum wages, firing costs, unionization);

- technology and globalization (making some skills obsolete, others more valuable).

Because of this, using a fixed estimate of the natural rate can be misleading; policymakers must regularly reassess it in light of evolving economic structure.

For exam purposes, linkages to inflation are important. When actual unemployment falls significantly below the natural rate, labor shortages tend to push up wages faster than productivity, raising unit labor costs and putting upward pressure on inflation. Conversely, if unemployment is above the natural rate, wage growth tends to slow, easing inflationary pressure.

Limitations of Unemployment Statistics

Analysts should be aware of several limitations:

- discouraged workers who stop looking for work are counted as “not in the labor force,” so the unemployment rate may understate labor market slack;

- underemployment (workers involuntarily working part‑time or in jobs below their skill level) is not captured by the standard unemployment rate.

Key Term: underemployment

A situation where workers are employed part‑time or in jobs that do not fully utilize their skills and abilities, often because full‑time suitable work is unavailable.

- differences in measurement methodologies and definitions across countries complicate international comparisons;

- changes in the participation rate (for example, more women entering the labor force, or older workers delaying retirement) can affect the unemployment rate even if the actual job market is strong.

Because of these limitations, many statistical agencies publish broader measures of labor underutilization that add discouraged workers and underemployed workers to the narrowly defined unemployed.

For investors and analysts, it is important to interpret unemployment figures together with:

- participation rates;

- wage growth (for example, hourly earnings);

- job vacancy rates;

- survey measures of labor market tightness.

A low unemployment rate combined with strong wage growth and high job vacancies suggests a tight labor market and possible upward pressure on inflation, even if headline unemployment is not at a record low.

Understanding these details is important for interpreting macroeconomic data releases in a realistic way and for interpreting exam questions that present combinations of unemployment and participation data.

Macroeconomic Indicators and the Business Cycle

Expenditure-based GDP is decomposed into consumption, investment, government spending, and net exports, with corresponding private, public, and external demand categories.

Economic Growth, Potential GDP, and Output Gaps

Over time, economies tend to grow as the labor force, capital stock, and productivity increase. The concept of potential output is central.

Key Term: potential GDP

The level of real GDP an economy can produce when using its resources (labor and capital) at normal, sustainable rates, without generating undue inflationary pressure. Key Term: output gap

The difference between actual real GDP and potential GDP, often expressed as a percentage of potential GDP.

- A negative output gap (actual GDP below potential) is associated with high cyclical unemployment and downward pressure on inflation.

- A positive output gap (actual GDP above potential) indicates an overheating economy, tight labor markets, and rising inflation.

Real GDP growth can be:

- demand‑driven: strong growth in aggregate demand pushes output closer to or beyond potential, often raising inflation;

- supply‑driven: increases in aggregate supply (for example, from productivity gains or lower input costs) raise output and lower or stabilize inflation.

Long‑run sustainable growth is closely related to the growth of potential GDP, not just actual GDP. Potential GDP, in turn, depends on:

- growth of the labor force;

- growth of the capital stock;

- growth in productivity (output per unit of input).

A simple way to express this is via the production function.

Key Term: production function

A relationship that specifies the maximum output an economy can produce for given quantities of inputs and technology, often written as

where Y is output, L is labor, K is capital, and A captures productivity. Key Term: total factor productivity (TFP)

A scale factor in the production function that captures the efficiency with which an economy uses labor and capital; higher TFP allows more output from given inputs and is often interpreted as the effect of technology and organization.

Increases in potential GDP can come from:

- input growth: more workers (higher labor force), more capital (investment in machinery, buildings, infrastructure), more effective use of raw materials;

- TFP growth: better technology, improved management, stronger institutions, better infrastructure, and higher human capital (education and skills).

The neoclassical growth model makes three important assumptions:

- constant returns to scale: if all inputs double, output doubles;

- diminishing marginal productivity: holding other inputs fixed, adding more of one input (for example, capital) eventually yields smaller and smaller increases in output;

- no externalities from inputs: use of inputs does not generate additional positive or negative effects not captured in the production function.

Because of diminishing marginal productivity, simply adding more capital per worker (capital deepening) raises output but at a decreasing rate. Sustained long‑run growth in living standards typically requires ongoing improvements in TFP.

This has two important implications:

- Long‑term sustainable growth cannot rely solely on ever‑higher investment in physical capital. Without productivity improvements, growth will eventually slow as returns to capital investment diminish.

- Developing economies, which typically have lower capital per worker, can achieve high growth rates by accumulating capital and adopting existing technologies, leading to convergence in income levels with richer countries—provided they have supportive institutions and policies.

Central banks and international organizations often approximate the growth rate of potential GDP as:

- growth rate of the labor force plus

- growth rate of labor productivity (output per worker).

A simple numerical illustration: if the labor force grows at 1% per year and labor productivity grows at 2% per year, potential GDP growth is approximately 3% per year. If actual GDP is growing at 5% per year in this situation, the economy is likely operating above potential, and inflation pressure may build.

From an investment standpoint:

- faster potential GDP growth supports higher long‑run equity earnings growth and may justify higher valuations for growth‑sensitive sectors;

- output gaps relative to potential GDP help analysts assess inflation pressures and likely monetary policy moves;

- for fixed‑income investors, potential growth influences real interest rate trends and debt sustainability.

Potential GDP is not directly observable and must be estimated using statistical filters (to separate trend from cycle) or production‑function approaches. These estimates are uncertain, but they provide a useful benchmark for thinking about whether an economy is running “hot” or “cold.”

The Business Cycle and Indicator Behavior

Stylized phases of the business cycle and associated behavior of indicators are:

-

Early expansion (recovery):

- Real GDP growth moves from negative to positive and then above trend.

- Unemployment is high but starting to fall.

- Inflation is low or falling (slack remains).

- Interest rates are low and monetary policy is often accommodative.

-

Mid‑expansion:

- Real GDP grows at a solid, sustainable pace.

- Unemployment continues to decline toward the natural rate.

- Inflation is stable or rising gradually.

- Corporate profits grow strongly; credit quality improves.

-

Late expansion / peak:

- Growth remains positive but may slow.

- Unemployment is low, possibly below the natural rate.

- Capacity utilization is high; inflation often accelerates.

- Central banks often tighten monetary policy; yield curves may flatten or invert.

-

Contraction (recession):

- Real GDP declines or grows below trend.

- Firms cut output; cyclical unemployment rises.

- Inflation often slows; in severe downturns, deflation risks appear.

- Policy is typically eased (lower interest rates, higher fiscal deficits).

-

Trough:

- Output stabilizes at a low level.

- Unemployment is high but may start to fall.

- Inflation is typically low; accommodative policy persists.

Questions frequently present combinations of GDP growth, inflation, and unemployment and ask you to infer the likely phase of the cycle.

For example:

- High real GDP growth, falling unemployment, and rising core inflation typically signal a late‑expansion phase.

- Falling GDP, rising unemployment, and slowing inflation (or deflation) are characteristic of a recession.

Example: Business Cycle Downturn and Unemployment

During a business cycle downturn, real GDP falls and the unemployment rate rises from 5% to 8%. What type of unemployment increases the most?

Answer:

Cyclical unemployment increases the most. Frictional and structural unemployment tend to change slowly, but cyclical unemployment rises when aggregate demand weakens and firms reduce output and employment.

Aggregate Demand and Supply: Demand and Supply Shocks

Key Term: aggregate demand

The total planned spending on final goods and services in an economy at different price levels, equal (in a simple model) to:

Key Term: aggregate supply

The total quantity of goods and services that firms in an economy are willing to produce at different price levels in the short run (SRAS) or long run (LRAS).

Using aggregate demand and aggregate supply (AD–AS) terminology:

-

An increase in aggregate demand (AD):

- raises real GDP;

- lowers the unemployment rate;

- increases the price level (inflationary pressure).

-

A decrease in AD:

- lowers real GDP;

- raises unemployment;

- tends to reduce inflation (or cause deflation in extreme cases).

-

An increase in aggregate supply (AS) (for example, from lower input costs or higher productivity):

- raises real GDP;

- lowers unemployment;

- lowers the price level (disinflationary).

-

A decrease in AS (for example, from higher input costs or negative supply shocks):

- lowers real GDP;

- raises unemployment;

- raises the price level.

Negative supply shocks (for example, major oil price spikes) can produce stagflation—high unemployment with high inflation—because output falls while prices rise.

The distinction between demand‑driven and supply‑driven changes matters for interpreting combinations of GDP, inflation, and unemployment:

- Demand‑driven expansions are usually associated with rising inflation and rising interest rates.

- Supply‑driven expansions (positive supply shocks) are associated with higher output but lower or stable inflation and interest rates.

Determinants of Aggregate Demand

Several factors can shift the AD curve (beyond movements along the curve due to price changes):

-

Household wealth: Household wealth includes financial assets (cash, deposits, securities, pensions) and real assets (real estate). When these assets increase in value, households feel richer and tend to save a smaller fraction of their income and consume more. This wealth effect shifts AD to the right. A decline in wealth has the opposite effect.

-

Consumer and business expectations: Greater confidence about future income and profitability encourages more consumption and investment, shifting AD to the right. When confidence falls, households and firms cut spending, shifting AD to the left.

-

Capacity utilization: When firms have substantial spare capacity, they have little incentive to invest in new capital; investment spending is weak. When capacity utilization rises toward high levels (often around 82–85% in manufacturing), firms are more likely to invest in additional capacity, raising and shifting AD to the right.

-

Fiscal policy: Government spending () enters AD directly. Higher or lower taxes (which raise disposable income and after‑tax profits) increase AD; lower or higher taxes reduce AD.

-

Monetary policy: Expansionary monetary policy (lower policy interest rates, higher money supply) tends to:

- reduce borrowing costs;

- boost interest‑sensitive spending (housing, durable goods, capital investment);

- raise asset prices and credit availability. This shifts AD to the right. Contractionary monetary policy does the reverse.

-

Exchange rate and foreign income: A depreciation of the domestic currency makes exports cheaper and imports more expensive, boosting net exports () and shifting AD right. Strong growth in foreign economies raises demand for exports and similarly shifts AD right; global recessions reduce external demand.

Understanding these determinants helps interpret macroeconomic news: for example, a large fiscal stimulus package or aggressive monetary easing typically signals a rightward shift in AD, supporting growth but potentially increasing inflationary pressure if the economy is near potential output.

Output Gaps and Inflationary/Recessionary Gaps

When actual GDP is:

-

below potential: the economy has a recessionary (negative) gap;

- high cyclical unemployment;

- downward pressure on inflation.

-

above potential: the economy has an inflationary (positive) gap;

- resources (labor, capital) are overutilized; firms may run overtime and face bottlenecks;

- upward pressure on wages and prices.

In an inflationary gap, wages and other input prices eventually rise, causing the short‑run aggregate supply (SRAS) curve to shift left and bringing output back toward potential, but at a higher price level. This is sometimes called the self‑correcting mechanism of the economy, although it may operate slowly.

In a recessionary gap, high unemployment and low capacity utilization put downward pressure on wages and prices. Over time, this can shift SRAS to the right, moving output back toward potential and stabilizing the price level at a lower level. Again, this natural correction can be slow, which is why governments and central banks often use policy tools to speed the adjustment.

Policy Responses: Fiscal and Monetary Policy

Governments and central banks monitor GDP, inflation, and unemployment to judge the position in the business cycle and choose policy responses.

Key Term: fiscal policy

The use of government spending and taxation decisions to influence the level of aggregate demand, output, and employment in the economy. Key Term: monetary policy

Actions taken by a country’s central bank to influence the quantity of money and credit and the level of interest rates, with the aim of affecting aggregate demand, output, and inflation.

Typical patterns:

-

When unemployment is above the natural rate and real GDP is below potential (negative output gap), policymakers may adopt expansionary policy:

- fiscal: higher government spending and/or lower taxes;

- monetary: lower policy interest rates, increased money supply, quantitative easing.

-

When the economy is overheating (positive output gap), with low unemployment and rising inflation, they may adopt contractionary policy:

- fiscal: spending cuts and/or tax increases;

- monetary: higher policy rates, slower money growth, asset sales.

Central banks implement monetary policy primarily through:

- open‑market operations: buying or selling government securities to change bank reserves and short‑term interest rates;

- policy rate changes: adjusting the target for a key short‑term rate (such as the federal funds rate in the United States);

- reserve requirements (where used): changing the fraction of deposits banks must hold as reserves.

An increase in bank reserves and a reduction in policy rates generally lower borrowing costs, encourage credit expansion, and shift AD to the right. The opposite actions tighten monetary conditions and shift AD left.

In practice, both fiscal and monetary policy face time lags:

- recognition lag: time to identify that conditions have changed;

- implementation lag: time to design and pass policy measures;

- impact lag: time for the measures to affect spending and inflation.

These lags mean that even well‑intentioned policies can sometimes arrive late and exacerbate the cycle rather than smooth it. The CFA curriculum expects awareness of these limitations at a conceptual level.

These policy actions affect financial markets:

- Expansionary policies tend to lower interest rates (supporting bond prices initially) and support equity prices through higher expected earnings.

- Contractionary policies tend to raise interest rates (pressuring bond prices) and may dampen equity valuations through slower expected growth.

- Commodity prices often respond strongly to demand‑driven expansions and to changes in expected inflation.

Example: Identifying Late‑Expansion Conditions

An economy is growing at 4% in real terms, above its estimated potential growth rate of 2%. Unemployment has fallen to a 20‑year low, and core inflation has risen from 1% to 3% over two years. What is the most likely policy stance of the central bank, and what phase of the business cycle does this describe?

Answer:

- With growth above potential, very low unemployment, and rising core inflation, the economy is likely in a late expansion or approaching a peak.

- The central bank is most likely to adopt a contractionary stance: raising policy interest rates and possibly slowing the growth of the money supply to prevent inflation from accelerating further.

Investment Implications of AD and AS Shifts

The AD–AS framework also has direct investment implications:

-

Increase in AD creating an inflationary gap (demand‑driven expansion):

- Corporate profits and cyclical sectors (consumer discretionary, industrials, materials) often benefit.

- Commodity prices and commodity‑linked equities tend to rise as demand for raw materials increases.

- Interest rates usually rise over time as inflation pressure builds, hurting long‑duration fixed‑income securities.

- Credit risk tends to fall; high‑yield bonds may perform relatively well despite rising rates.

-

Decrease in AD (demand‑driven recession):

- Real GDP falls; unemployment rises.

- Inflation slows; interest rates typically decline as central banks ease policy.

- High‑quality government bonds tend to perform well.

- Cyclical sectors and high‑yield credit are vulnerable; defensive sectors (utilities, consumer staples, healthcare) may outperform.

-

Decrease in AS (negative supply shock / stagflation):

- Output falls; unemployment rises.

- Inflation rises due to higher production costs.

- Profit margins are squeezed; broad equity markets often perform poorly.

- Nominal interest rates may rise because of higher inflation, hurting fixed‑income returns.

- Commodities, especially the ones experiencing the shock (for example, energy), may see strong price gains.

-

Increase in AS (positive supply shock):

- Output rises; unemployment falls.

- Inflation declines or remains subdued.

- Both equities and bonds can benefit: higher growth supports earnings, while lower inflation supports bond prices.

- Commodities may face downward price pressure.

Whether growth is demand‑driven or supply‑driven therefore has implications for asset allocation, especially the balance between equities, bonds, and commodities.

Summary

GDP, inflation, and unemployment are core macroeconomic indicators used to evaluate a country's economic performance.

-

GDP measures the value of domestic production. It can be measured via expenditure, income, and output (value‑added) approaches, all of which should conceptually yield the same result. Nominal GDP reflects both prices and quantities; real GDP adjusts for inflation and captures changes in the volume of output. The GDP deflator provides a broad measure of the overall price level for domestic output. Distinctions between gross and net, and between domestic and national (GDP versus GNI), are important for interpreting macro data. GDP per capita is a rough proxy for living standards but has significant limitations, especially regarding distribution, non‑market activity, and environmental impacts. PPP‑adjusted measures help when comparing living standards across countries with different price levels.

-

Inflation is measured as the percentage change in a price index, such as the CPI, PPI, or GDP deflator. The CPI is a fixed‑basket consumer index and tends to overstate the true cost of living due to substitution, quality, new‑goods, and outlet substitution biases. Headline inflation includes all items, while core inflation strips out volatile components like food and energy to reveal the persistent trend. Inflation can be caused by excess demand (demand‑pull), rising costs (cost‑push), or excess money growth (monetarist view), and it is influenced by expectations. Disinflation, deflation, and hyperinflation describe different regimes with distinct economic and financial consequences. Price indices are also used to convert nominal variables into real terms and to gauge real returns for investors.

-

Unemployment statistics—including the unemployment rate and labor force participation rate—describe labor market conditions. Distinguishing frictional, structural, and cyclical unemployment and understanding the natural rate of unemployment helps link labor market data to the business cycle and to inflation pressures. Official unemployment rates have limitations: they may understate slack when discouraged workers exit the labor force or when underemployment is widespread. Broader measures of labor underutilization can provide a more complete picture.

-

Business cycles reflect fluctuations around the economy’s potential GDP. Output gaps (differences between actual and potential GDP) are associated with specific combinations of GDP growth, inflation, and unemployment. Demand‑driven expansions usually bring rising inflation and interest rates, while supply‑driven expansions can deliver growth with stable or falling inflation. Fiscal and monetary policies are key tools used to stabilize the economy, with expansionary policies deployed in downturns and contractionary policies in overheating phases. The AD–AS framework provides a systematic way to think about how various shocks and policy measures affect output, employment, and prices.

Integrating GDP, inflation, and unemployment data allows analysts to infer the phase of the business cycle, estimate output gaps relative to potential GDP, anticipate fiscal and monetary policy moves, and assess likely effects on different asset classes. These skills are central to the macroeconomic analysis required at CFA Level 1.

Key Point Checklist

This article has covered the following key knowledge points:

- Define, calculate, and interpret gross domestic product (GDP) using expenditure, income, and output approaches, and understand what is included and excluded from GDP.

- Distinguish between gross and net (GDP versus NDP), and between domestic and national (GDP versus GNI/GNP), when interpreting GDP‑related measures.

- Explain imputed values (owner‑occupied housing, government services), the underground economy, and recognize how these affect GDP comparisons.

- Distinguish between nominal GDP and real GDP, and use the GDP deflator to adjust for inflation and measure real economic growth.

- Explain the difference between the GDP deflator and consumer price indices such as the CPI, and when each measure is appropriate.

- Explain how price indices such as the CPI and PPI are constructed, and calculate inflation rates from index values.

- Recognize sources of CPI bias (substitution, quality, new goods, and outlet substitution) and their implications for measuring the cost of living.

- Distinguish headline from core inflation, and understand the causes and macroeconomic effects of inflation, disinflation, deflation, hyperinflation, and stagflation.

- Describe demand‑pull, cost‑push, and monetarist explanations of inflation, and identify indicators that signal emerging inflationary or deflationary pressures, including unit labor costs, output gaps, and money growth relative to nominal GDP.

- Use price indices to deflate nominal variables and approximate real interest rates, and interpret the impact of inflation on different asset classes.

- Define, calculate, and analyze the unemployment rate and labor force participation rate, and recognize the limitations of these measures (discouraged workers, underemployment, international differences).

- Differentiate frictional, structural, and cyclical unemployment, and relate them to the natural rate of unemployment and potential GDP.

- Explain the concepts of potential GDP, output gaps, and the production function, including the role of total factor productivity in long‑run growth.

- Relate GDP growth, inflation, and unemployment to business cycle phases, aggregate demand and supply shocks, and likely fiscal and monetary policy responses.

- Interpret combinations of GDP, inflation, and unemployment data to infer the phase of the business cycle and likely implications for interest rates and asset prices.

- Recognize the role of PPP‑adjusted GDP in cross‑country welfare comparisons and the limitations of market‑exchange‑rate comparisons.

Key Terms and Concepts

- gross domestic product (GDP)

- GDP per capita

- business cycle

- final goods and services

- expenditure approach

- income approach

- net domestic product (NDP)

- gross national income (GNI) / gross national product (GNP)

- output (product) approach

- value added

- underground economy

- purchasing power parity (PPP) exchange rate

- nominal GDP

- real GDP

- chain‑weighted index

- GDP deflator

- producer price index (PPI)

- headline inflation

- core inflation

- disinflation

- deflation

- hyperinflation

- real interest rate

- demand‑pull inflation

- cost‑push inflation

- monetarist view of inflation

- inflation expectations

- capacity utilization

- unit labor cost (ULC)

- velocity of money

- stagflation

- working‑age population

- labor force

- unemployment rate

- labor force participation rate

- discouraged worker

- frictional unemployment

- structural unemployment