Learning Outcomes

This article explains counterparty risk margining and clearing in swaps for the CFA Level 1 exam, including:

- identifying the main sources of counterparty (credit) risk in over-the-counter and centrally cleared swaps, and how exposure evolves with market movements, time to maturity, and contract structure.

- explaining the objectives and mechanics of margining arrangements, distinguishing clearly between initial margin, variation margin, and maintenance or threshold levels used in practice.

- analyzing how daily mark-to-market, minimum transfer amounts, and margin frequency affect both credit risk mitigation and the liquidity management challenges faced by swap participants.

- describing collateral eligibility criteria, valuation haircuts, and re-use restrictions, and assessing how these terms influence the effectiveness of collateralization in stressed markets.

- detailing the structure and risk-management role of central clearing counterparties, including novation, multilateral netting, default waterfalls, and the operation of CCP default funds.

- interpreting margin calls, margin shortfalls, and closeout procedures, and relating these to default events, termination values, and recovery prospects in exam-style scenarios.

- connecting the legal documentation framework, such as ISDA agreements, credit support annexes, and netting provisions, to quantitative exposure measures commonly tested in the CFA curriculum.

CFA Level 1 Syllabus

For the CFA Level 1 exam, you are expected to understand the main risk management tools and practices used in derivative markets relevant to swaps and counterparty protection, with a focus on the following syllabus points:

- Describe counterparty (credit) risk in derivative transactions, with an emphasis on swaps.

- Explain the role and mechanisms of margining in the context of derivative contracts (variation and initial margin).

- Describe the function and benefits of central clearing counterparties (CCPs) for swaps.

- Identify the effects of daily settlement (mark-to-market) and collateralization on risk for swap participants.

- Explain margin calls, collateral posting, and the consequences of a margin shortfall or default.

- Recognize key legal and operational protections to manage the risk of counterparty failure in swaps.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the principal source of counterparty risk in a typical over-the-counter (OTC) swap?

- What is the main difference between variation margin and initial margin in swap risk management?

- How does a central clearing counterparty (CCP) reduce system-wide risk in the swap market?

- What typically happens if a swap participant fails to meet a margin call by the deadline?

Introduction

Swaps are widely used financial derivatives that expose participants to counterparty risk: the chance that the other party fails to meet its contractual obligations. During market stress, the risk of default can be substantial. The risk management framework for swaps combines legal protections, margining requirements, and central clearing to limit potential losses and safeguard market stability. Margining and clearing are central to current best practices for swaps, following major regulatory reforms. This article introduces the key concepts of counterparty risk, margining, and clearing, along with their application for CFA exam candidates.

Test Tip: When revising Counterparty risk margining and clearing, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Counterparty Risk in Swaps

Unlike exchange-traded futures, most swaps have traditionally been traded over-the-counter (OTC), directly between two financial institutions or a dealer and a client. Each side commits to a stream of future cash flows, exchanged according to the swap contract's terms. If one party becomes insolvent, the remaining payments from that party may be lost.

Key Term: Counterparty risk

The possibility that the other party to a financial contract will default on contractual obligations—particularly relevant in derivative markets, like swaps.

Swaps typically accumulate exposure as market prices change between settlement dates. Credit risk is especially significant for contracts with long maturities, material mark-to-market values, or illiquid underlyings.

Margining: Managing Exposure

To limit credit risk, swap participants use margining. Margining refers to the process where both parties post collateral to secure their obligations. Margin is adjusted regularly to account for market value changes and protect against future adverse movements.

Key Term: Margining

The practice of requiring collateral (cash or securities) to be posted to offset potential future credit exposures in a swap or other derivative.

There are two main types of margin:

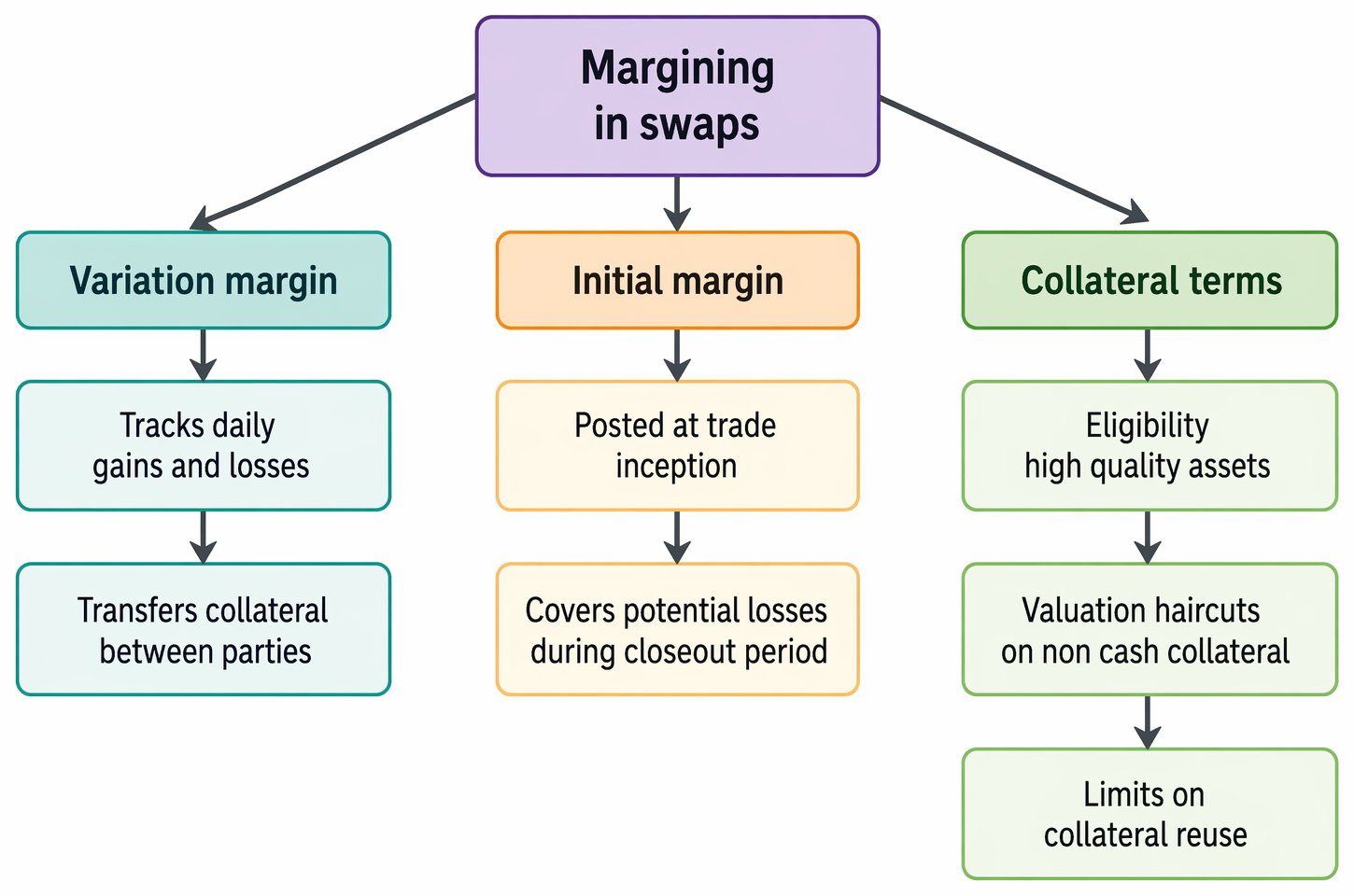

- Variation margin: Adjusts collateral daily (or intraday) to reflect changes in the swap's value. This is also called mark-to-market margin.

- Initial margin: An upfront deposit to protect against changes in value that could occur between market movements and the closeout/settlement of the position. This serves as a buffer against uncollateralized risk during the time required to liquidate or replace the contract after a default.

Only highly rated collateral is accepted (e.g., cash, government securities), and rules may specify requirements for eligibility, valuation, and re-use.

Key Term: Variation margin

Collateral regularly exchanged between swap parties to reflect gains or losses since the previous settlement, ensuring the current market value is covered. Key Term: Initial margin

Upfront collateral posted at the outset of a swap (and adjusted over time) to absorb losses during the period between a counterparty default and closeout.

Worked Example 1.1

A bank enters into a five-year interest rate swap. The next week, interest rates move, creating a mark-to-market gain of $600,000 in the bank's favor. What happens under standard margining procedures?

Answer:

The losing counterparty must transfer $600,000 (variation margin) in eligible collateral to the bank, protecting the bank against default on the gain.

Clearing and Central Counterparties

After the 2008 financial crisis, regulators required most standardized swaps to use central clearing counterparties (CCPs). A CCP becomes the legal counterparty to both sides. The benefits of central clearing are:

Margining in swaps is divided into variation margin, initial margin, and collateral provisions governing eligible assets, haircuts, and collateral reuse.

- All parties face the CCP, which novates (replaces) the original contracts and guarantees performance, provided collateral rules are observed.

- CCPs impose strict margining, daily settlement, and default management mechanisms.

- The risk of a large default spreading through the market is contained.

Key Term: Central clearing counterparty (CCP)

An institution that acts as intermediary in derivative transactions, becoming the buyer to every seller and the seller to every buyer, managing counterparty risk via margining and default fund resources.

Worked Example 1.2

A corporate counterparty clears a plain-vanilla interest rate swap through a CCP. The CCP requires an initial margin of $2 million and performs a daily mark-to-market. On Monday, sharp moves in rates create $0.5 million losses for the corporate. What is the CCP likely to request?

Answer:

The CCP issues a margin call for $0.5 million (variation margin) from the corporate, to be posted by the deadline or the position may be closed and default procedures triggered.

Margin Calls, Defaults, and Default Protections

If a swap participant has insufficient collateral after a market move or their assets fall in value, a margin call is triggered. If the margin call is not met within the deadline (typically within hours), the non-defaulting party or CCP has the contractual right to terminate or close out the swap and seize posted collateral. The CCP may use its default fund (a pool of member contributions) if losses exceed the defaulting member's margin.

Key Term: Margin call

A formal request for additional collateral when a participant's margin falls below the required threshold due to market moves. Key Term: Default fund

A reserve pool contributed by CCP members, available to absorb losses if margin is insufficient after a member default.

Legal Protections: Agreements and Documentation

Risk management also relies on legal protections. Framework agreements, such as the ISDA Framework Agreement, set out default provisions, collateral procedures, and legal rights during insolvency. Netting provisions allow participants to offset gains and losses across positions, reducing owed balances to a single net exposure.

Key Term: Netting

Contractual provisions to aggregate (net) the value of multiple contractual obligations between counterparties, so only a single net amount is paid or owed on default.

Margining and Clearing in Practice

Margin requirements and clearing obligations are set by regulation, CCP rules, or bilateral agreement, depending on instrument and jurisdiction. Central clearing is now mandatory for many standardized swaps. Non-cleared OTC swaps face higher margin requirements and additional regulation.

Worked Example 1.3

Suppose Participant A enters a bespoke swap directly with Bank X (non-cleared). The contract's value rises by $1.2m in favor of Participant A, but Bank X defaults before transferring the margin. What is Participant A's loss?

Answer:

Participant A is typically exposed for the uncollateralized gain of $1.2m, subject to any further legal recovery. Central clearing would have required daily margin and reduced or eliminated this loss.Exam Warning: Some candidates confuse variation margin with initial margin, or believe margining removes all risk. In practice, margin may not always fully cover positions during extreme volatility or between margin periods. Understand the distinction for the exam.

Summary

Margining and central clearing are the backbone of modern counterparty risk management for swaps. Daily margining (variation margin) and upfront collateral (initial margin) limit losses if one party defaults. Central clearing via CCP reduces system-wide risk by guaranteeing performance through novation, margin calls, and default funds. Legal agreements set out netting, margin, and default rights. Understanding these mechanisms is essential for CFA Level 1 candidates.

Key Point Checklist

This article has covered the following key knowledge points:

- Identify and describe counterparty risk in swap transactions.

- Explain how margining (variation and initial margin) manages swap credit risk.

- Distinguish the role of central clearing via CCP versus bilateral OTC swap arrangements.

- Understand how margin calls, defaults, and CCP default funds operate in swap markets.

- Recognize the legal tools (netting, agreements) that support swap risk management.

Key Terms and Concepts

- Counterparty risk

- Margining

- Variation margin

- Initial margin

- Central clearing counterparty (CCP)

- Margin call

- Default fund

- Netting