Learning Outcomes

This article explains how volatility management and variance swaps are used in portfolio risk management, including:

- Identifying sources of volatility and variance risk in equity and multi-asset portfolios, and linking them to option-like exposures and tail-risk scenarios.

- Distinguishing common volatility management approaches, such as using index options, volatility index (VIX) derivatives, and structured option overlays, versus employing variance and volatility swaps.

- Explaining the economic intuition, payoff structure, and settlement mechanics of a variance swap, and contrasting it with a volatility swap or a simple long-straddle position.

- Calculating variance swap payoffs, mark-to-market P&L, and hedging outcomes from the standpoint of both long and short counterparties, using exam-style numerical data.

- Evaluating when variance swaps are the most appropriate tool for hedging or expressing volatility views, compared with alternative derivatives or dynamic hedging strategies.

- Recognizing key exam pitfalls, including confusion between variance and volatility, misinterpretation of notional versus strike, and incorrect sign conventions when determining cash flows.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are required to understand derivatives for portfolio risk management and volatility trading, with a focus on the following syllabus points:

- Principles of volatility risk and variance risk management in a portfolio context.

- Uses of volatility derivatives, including equity options, VIX futures and options, and variance swaps.

- Mechanics and payoff structure of variance swaps, including realized variance calculation.

- Distinction between volatility swaps, options strategies, and variance swaps for risk mitigation and speculation.

- Pricing and margining issues, including P&L calculation and risks in variance swap implementation.

- Common exam pitfalls concerning volatility exposures using swaps and index options, and interpretation of variance versus volatility.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which statement best describes the principal difference between a variance swap and a volatility swap?

- a) A variance swap pays on the difference between realized and implied volatility, while a volatility swap pays on the difference between realized and implied variance.

- b) A variance swap payoff is linear in realized volatility, while a volatility swap payoff is linear in realized variance.

- c) A variance swap payoff is linear in realized variance, while a volatility swap payoff is linear in realized volatility.

- d) Both contracts are linear in realized volatility but use different discount factors.

-

A manager wants to hedge a concentrated long equity index portfolio against a sudden spike in market volatility over the next year, with minimal need for rebalancing. Which instrument is most appropriate?

- a) A series of monthly at-the-money (ATM) index call options.

- b) A one-year long variance swap on the equity index.

- c) A one-year short position in VIX futures.

- d) A one-year short variance swap on the equity index.

-

A one-year S&P 500 variance swap has a variance strike of 0.02 and a variance notional of $100,000. If realized variance is 0.03, what is the final cash flow to the long position at expiration (ignoring discounting)?

- a) –$1,000

- b) $1,000

- c) –$10,000

- d) $10,000

-

Why might a long position in a variance swap provide a more precise long-volatility exposure than simply buying an at-the-money straddle on the same index?

- a) Because the variance swap has no vega exposure.

- b) Because the variance swap delivers linear exposure to realized variance without requiring delta rebalancing.

- c) Because the straddle depends only on realized variance and not on implied volatility.

- d) Because the straddle’s payoff is linear in volatility, whereas the variance swap’s payoff is capped.

Introduction

Effective risk management requires not only controlling market beta, duration, and sector exposures, but also systematically managing volatility risk as a distinct dimension of portfolio risk. Volatility tends to be low and stable during benign periods, then spike sharply when markets sell off. Equity volatility also exhibits clustering and mean reversion. For a portfolio with option-like exposures (explicit options or embedded guarantees), these volatility regimes can dominate returns.

Key Term: volatility risk

Volatility risk is the risk to a portfolio arising from changes in expected or realized volatility of reference assets, over and above the risk from directional price moves.

Volatility is now widely treated as a separate “asset class.” Long volatility positions (for example, via long puts, VIX futures, or variance swaps) can hedge equity drawdowns and tail events. Short volatility positions can generate premium income but expose the investor to large losses when volatility spikes.

This article focuses on variance swaps, which are over-the-counter (OTC) derivatives that deliver a payoff directly linked to realized variance of an asset over a specified period. They are powerful for hedging or expressing views on volatility, but they also introduce specific risks and implementation nuances that are tested at Level 3.

Key Term: variance swap

A variance swap is a derivative contract that settles in cash based on the difference between realized variance of a reference asset over a period and a fixed variance strike, multiplied by a variance notional. Key Term: volatility swap

A volatility swap is a derivative contract that settles based on the difference between realized volatility and a volatility strike; the payoff is linear in volatility, not variance.

Understanding how variance swaps differ from volatility swaps, VIX futures, and option strategies—and how they interact with portfolio exposures—is critical for constructing hedges and answering exam questions.

Test Tip: When revising Volatility management and variance swaps, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

VOLATILITY RISK IN PORTFOLIO MANAGEMENT

Volatility Exposure and Its Management

Managers increasingly treat volatility as an explicit risk factor:

- Volatility affects the distribution of returns, especially tail risk.

- Many portfolios have embedded short gamma exposures (for example, from covered call writing), making them vulnerable to jumps in volatility.

- Institutions often work with risk budgets expressed in volatility terms (target-volatility funds, risk parity, or volatility caps in IPS documents).

Key Term: realized volatility

Realized volatility is the ex post standard deviation of returns of an asset over a specified period, annualized from observed data. Key Term: realized variance

Realized variance is the square of realized volatility over a period; for daily log returns , it is typically computed as

where is the number of trading days.

Key motivations for managing volatility include:

-

Hedging volatility spikes (tail-risk hedging): Long volatility exposures can partially offset losses during sharp market sell-offs. Empirical evidence shows that equity index volatility is strongly negatively correlated with equity returns, especially in crises.

-

Harvesting the variance risk premium: On average, the market’s implied volatility exceeds subsequent realized volatility, reflecting a volatility risk premium paid by hedgers to volatility sellers. Systematically being short volatility (for example, via short variance swaps) seeks to capture this premium, but carries fat-tail risk.

Key Term: implied volatility

Implied volatility is the market’s consensus forecast of future volatility derived from option prices, under a chosen option pricing model.

-

Targeting portfolio volatility: Many institutional mandates specify volatility bands; derivatives allow managers to adjust effective portfolio volatility without disrupting existing holdings.

-

Trading volatility as a view: Investors can take directional views on volatility independent of directional price forecasts, for example, “volatility is too low given macro risks.”

Common tools include:

- Index options (puts, calls, and structured overlays such as collars or put spreads).

- Volatility index derivatives (for example, VIX futures and options).

- Variance and volatility swaps.

Key Term: volatility index (VIX)

A volatility index such as the VIX measures the market’s expectation of near-term equity index volatility, derived from option prices; it is used as a benchmark for implied volatility and underlies VIX futures and options. Key Term: volatility futures

Volatility futures are futures contracts on volatility indexes (such as VIX futures), providing linear exposure to expected future implied volatility of the index.

Variance swaps stand out because they deliver a linear payoff in realized variance, closely matching what risk managers often care about: how volatile the equity market actually was over the hedge horizon, not just where implied volatility traded.

VARIANCE SWAPS: STRUCTURE AND APPLICATION

Overview

Variance swaps provide pure, linear exposure to future realized variance, usually on an annualized basis. The standard payoff at maturity is:

where:

- Realized variance is computed from daily log returns over the life of the swap, annualized.

- The variance strike is set at inception so that the swap has zero market value initially; it reflects the market’s expectation of future variance.

- The variance notional scales the payoff.

Key Term: variance strike

The variance strike is the fixed annualized variance level (square of volatility) specified in a variance swap, representing the market’s expected variance at trade inception.

At expiration:

- A long variance swap profits if realized variance exceeds the strike.

- A short variance swap profits if realized variance falls short of the strike.

Although the payoff is linear in variance, as a function of volatility it is convex because variance is the square of volatility. This convexity makes long variance swaps especially valuable as tail-risk hedges.

Key Term: variance notional

Variance notional is the dollar multiplier in a variance swap that applies to the difference between realized variance and the variance strike to determine the settlement amount.

How Variance Swaps Are Quoted in Practice

Market participants typically think in terms of volatility rather than variance. To make sizing intuitive, dealers usually quote:

- A volatility strike (for example, 20%), whose square is the variance strike.

- A vega notional , which approximates the P&L for a 1 percentage point change in realized volatility relative to the strike.

Key Term: vega notional

Vega notional is the amount used to express the size of a variance swap in terms of P&L per 1% change in realized volatility relative to the volatility strike.

The exact variance notional implied by a given vega notional and volatility strike is:

where is expressed as a decimal (for example, 0.20, not 20).

Given realized volatility , the settlement amount can be written equivalently as:

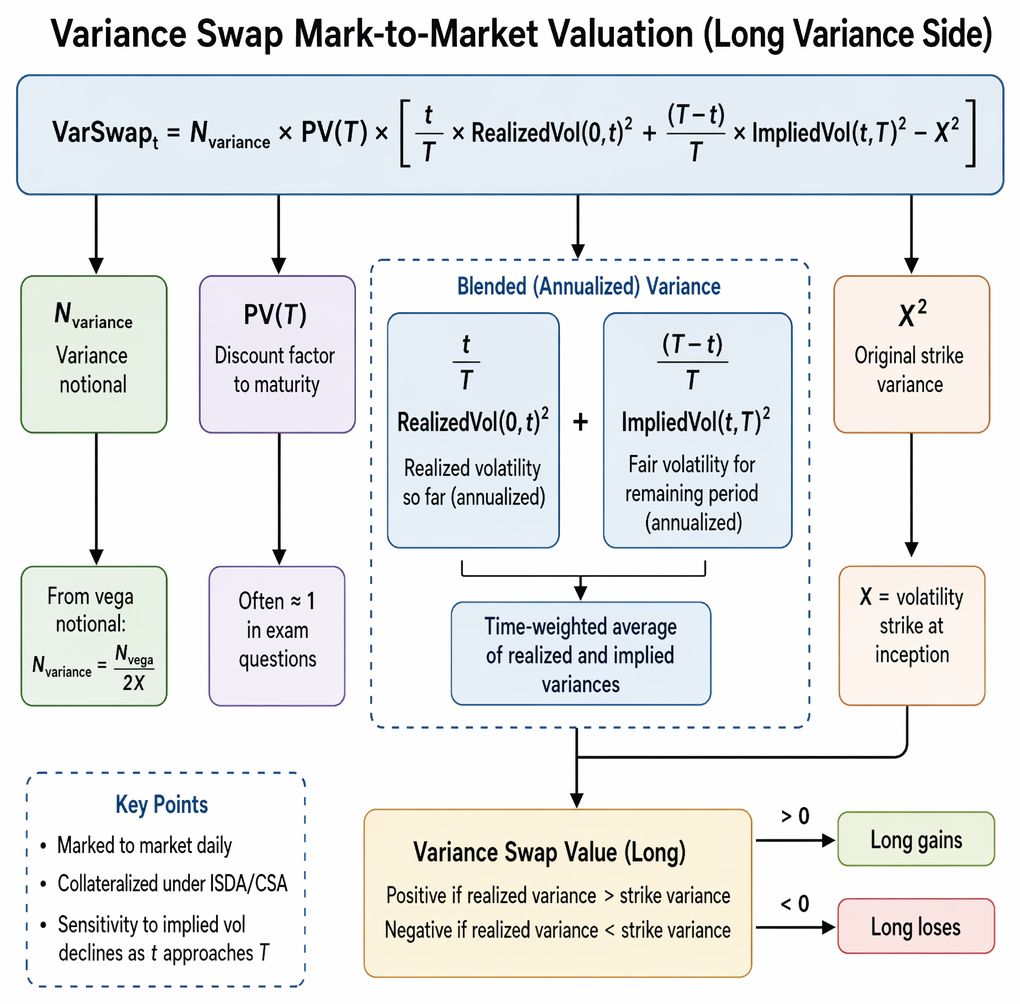

= N_{\text{variance}}(\sigma^2 - X^2) = N_{\text{vega}} \times \frac{\sigma^2 - X^2}{2X}$$ This formulation highlights both the linear dependence on variance and the convexity with respect to volatility. ### Worked Example 1.1 A fund buys a 6‑month S&P 500 variance swap with a variance notional of \$100,000 and a variance strike of 0.015 (corresponding to an implied volatility of about 12.25%). At expiry, observed annualized realized variance is 0.025 (realized volatility of about 15.8%). > **Answer:** > The long side receives > > $$> \text{Payoff} = 100{,}000 \times (0.025 - 0.015) = \$1{,}000$$ > > because realized variance exceeded the strike. ### Practical Uses in Portfolio Management Variance swaps allow: - Tail-risk hedging for long equity portfolios: A long variance position benefits from volatility spikes that typically accompany equity market drawdowns. - Neutralizing short-gamma exposures: Overwriting strategies (systematically selling calls or puts), structured products, and certain insurance guarantees create **short gamma** positions that suffer in volatile markets. Buying variance swaps can transfer that variance risk to the dealer. > **Key Term: gamma** > Gamma measures the curvature of an option’s value with respect to the asset price; a long-gamma position gains from large price moves (up or down), while a short-gamma position loses from such moves, typically accompanied by short volatility exposure. > **Key Term: short gamma** > Short gamma refers to a position (often from selling options) whose value decreases when the asset moves sharply in either direction, typically accompanied by short volatility exposure. > **Key Term: long gamma** > Long gamma refers to a position (often from buying options or variance swaps) that benefits from large asset price moves and increases in realized volatility. Being long a variance swap is economically similar to: - Being long a broad strip of out-of-the-money (OTM) calls and puts across strikes (long volatility, long gamma). - Being short the asset via futures to remove directional exposure. Because this is implemented as a single swap contract, it avoids the operational complexity of managing a large options portfolio. - Speculating on volatility: A manager who believes that future realized volatility will be higher than implied volatility can buy variance swaps; if realized variance ends up above the strike, the position profits even if the reference index ends unchanged. - Replacing options overlays: Instead of repeatedly rolling index puts for crash protection, a manager might use a medium-term variance swap to reduce transaction costs and avoid timing decisions in rolling. In contrast with VIX futures (which reference **implied** volatility at a future point), variance swaps reference **realized** volatility over the full contract period. This aligns them closely with risk management objectives that are expressed in terms of realized risk. ### PRICING AND MECHANICS OF VARIANCE SWAPS  _Annualized realized variance is derived by squaring daily log returns, summing them over the observation period, and applying an annualization factor._ ### Realized Variance Calculation As noted, realized variance over the life of the swap is usually computed as: $$\text{Realized variance} = \frac{252}{N-1} \sum_{i=1}^{N-1} \left[\ln\left(\frac{P_{i+1}}{P_i}\right)\right]^2$$ Key points: - Use **log returns**, not simple returns. - Use trading days only; 252 is the typical annualization factor. - Large daily moves contribute disproportionately because returns are squared, so tail events significantly impact the payoff. ### Strike Determination and Implied Volatility Surface The variance strike is set so that the present value of expected payoff is zero at inception. In practice, dealers: - Infer the entire **implied volatility surface** from option prices (different strikes and maturities). - Use a model-free formula to replicate variance using a continuum of OTM calls and puts. - Set the variance strike equal to the fair value implied by that replication. As a rule of thumb, for equity index variance swaps the volatility strike is often close to the implied volatility of a 90% moneyness put, reflecting the skewed demand for downside protection. > **Key Term: volatility-of-volatility** > Volatility-of-volatility refers to the variability of volatility itself; high volatility-of-volatility makes variance swap payoffs more uncertain and can increase the cost of hedging. ### Mark-to-Market Valuation Although classical descriptions say “no cash flows occur before maturity,” in practice variance swaps are: - Marked to market daily, and - Collateralized under ISDA/CSA agreements to control counterparty risk. The fair value of a variance swap at time $t$ (before maturity $T$), from the standpoint of the long-variance side, is: $$\text{VarSwap}_t = N_{\text{variance}} \times PV(T) \times \left[ \frac{t}{T} \times \text{RealizedVol}(0,t)^2 + \frac{T - t}{T} \times \text{ImpliedVol}(t,T)^2 - X^2 \right]$$ where: - $\text{RealizedVol}(0,t)$ is realized volatility so far (annualized). - $\text{ImpliedVol}(t,T)$ is the fair volatility strike today for a new variance swap over the remaining period. - $X$ is the original volatility strike at inception. - $PV(T)$ is the discount factor to maturity (often taken as 1 in exam questions). This formula blends realized variance to date with the market’s current expectation for future variance, weighted by time. ### P&L Calculation and Margining To value or settle a variance swap: - Compute realized variance from the daily log returns over the period. - Plug into the payoff formula with the contracted variance strike. - Multiply by the variance notional to obtain the settlement amount (positive for the long side if realized variance > strike). ### Worked Example 1.2 A variance swap has a volatility strike of 12% (so the variance strike is $0.12^2 = 0.0144$), a variance notional of \$50,000, and at expiry realized volatility is 8%, so realized variance is $0.08^2 = 0.0064$. What is the payoff to the **long** variance position at expiry? > **Answer:** > The payoff to the long variance side is > > $$> \text{Payoff} = 50{,}000 \times (0.0064 - 0.0144) = 50{,}000 \times (-0.008) = -\$400$$ > > so the long position pays \$400 to the short side; the short variance counterparty earns \$400. ### Worked Example 1.3 You sell (short) a variance swap on the Euro Stoxx 50 with a variance notional of €200,000 and a variance strike of 0.013. Realized volatility over the period is 8%, so realized variance is $0.08^2 = 0.0064$. What is your P&L at expiration? > **Answer:** > The payoff to the **long** variance side is > > $$> 200{,}000 \times (0.0064 - 0.013) = 200{,}000 \times (-0.0066) = -€1{,}320$$ > > so the long loses €1,320 and the short gains €1,320. As the seller, your P&L is **+€1,320**. This example illustrates a common exam pitfall: applying the payoff formula from the wrong party’s side and getting the sign wrong. ### Worked Example 1.4 Mark-to-market valuation of a variance swap An investor sells (short) \$50,000 vega notional of a one-year S&P 500 variance swap at a volatility strike of 20% (so $X = 0.20$). Six months later ($t/T = 0.5$): - Annualized realized volatility over the first six months is 16% ($0.16$). - The fair volatility strike for a new 6‑month variance swap is 19% ($0.19$). - Assume a flat yield curve with negligible discounting, so $PV(T) \approx 1$. Compute the mark-to-market value of the swap for the long-variance side (and hence the P&L for the short). > **Answer:** > First, compute the variance notional: > > $$> N_{\text{variance}} = \frac{N_{\text{vega}}}{2X} = \frac{50{,}000}{2 \times 0.20} = \frac{50{,}000}{0.40} = 125{,}000$$ > > Next, compute the blended variance term: > > $$> \frac{t}{T}\text{RealizedVol}^2 + \frac{T-t}{T}\text{ImpliedVol}^2 > = 0.5 \times 0.16^2 + 0.5 \times 0.19^2 > = 0.5 \times 0.0256 + 0.5 \times 0.0361 > = 0.0128 + 0.01805 = 0.03085$$ > > The original strike variance is $X^2 = 0.20^2 = 0.04$. > The variance term in brackets is > > $$> 0.03085 - 0.04 = -0.00915$$ > > So the value to the **long** variance side is > > $$> \text{VarSwap}_t = 125{,}000 \times (-0.00915) \approx -\$1{,}144$$ > > Therefore, the short-variance position (the seller) has a mark-to-market gain of about \$1,144. Note how the sensitivity to implied volatility diminishes over time: six months of realized volatility are locked in, and only the remaining six months depend on implied volatility. ### COMPARISON WITH ALTERNATIVE VOLATILITY STRATEGIES ### Variance Swaps vs Volatility Swaps From an exam standpoint, you must distinguish clearly between these: - **Variance swaps:** payoff linear in realized variance. - **Volatility swaps:** payoff linear in realized volatility. A volatility swap payoff at maturity is: $$\text{Settlement amount} = N_{\text{vol}} \times (\sigma_{\text{realized}} - \sigma_{\text{strike}})$$ Because realized volatility enters linearly, the volatility swap’s exposure to volatility is more straightforward. The variance swap’s payoff is convex in volatility (through the square). Consequences: - For a given move from 20% to 30% realized volatility, the variance swap payoff change is proportional to $0.30^2 - 0.20^2 = 0.09 - 0.04 = 0.05$, whereas the volatility swap payoff change is proportional to $0.30 - 0.20 = 0.10$. - For very large volatility spikes, the variance swap payoff grows faster (in volatility terms) than that of a volatility swap. In practice, the curriculum emphasizes **variance swaps**; volatility swaps are less commonly tested but important conceptually. ### Variance Swaps vs Long Straddles A **long at-the-money straddle** (long call + long put with the same strike) is also a long volatility, long gamma position. However: - The straddle’s payoff is **non-linear** in the asset price and depends on both volatility and the final price level. - The option buyer must pay an upfront premium and faces **theta decay** (time decay). - The sensitivity to volatility (vega) decays as expiration approaches and as the asset price moves away from the strike. - Maintaining a pure volatility exposure via options often requires **delta hedging** (rebalancing the asset position) and potentially rolling options. By contrast: - A variance swap’s payoff depends **only** on realized variance; it is independent of the final level of the index. - There is no upfront premium in the standard swap; the “price” is embedded in the strike. - The exposure to realized variance is **linear** (in variance) and does not require delta hedging. For a portfolio manager whose objective is clearly “hedge realized volatility over the next 12 months,” a variance swap generally provides a more **direct and stable** hedge than a single straddle. ### Variance Swaps vs VIX Futures and Options VIX futures and options provide exposure to **implied** volatility, not realized variance. Key differences: - A long VIX future profits if implied volatility at expiration exceeds the futures price; realized volatility over the period is only indirectly related. - The term structure of VIX futures (contango or backwardation) creates **roll yield** effects that can materially impact returns. Variance swaps, in turn: - Deliver a payoff based on realized variance over the full period. - Are not affected by futures roll yield but do embed the **variance risk premium** (difference between implied and realized variance) in the strike. > **Key Term: variance risk premium** > The variance risk premium is the expected excess of implied variance (embedded in option and variance swap prices) over subsequent realized variance, reflecting compensation to volatility sellers for bearing volatility risk. In an exam context: - Use VIX futures to express a view on **implied volatility levels** or to hedge over shorter horizons where implied volatility sensitivity is desired. - Use variance swaps when the objective is to hedge or trade **realized volatility** over the full period, with minimal rebalancing. ### When Are Variance Swaps Most Appropriate Variance swaps are most appropriate when: - The invested portfolio is highly correlated with the reference index (for example, a large-cap US equity portfolio vs S&P 500), minimizing basis risk. - The manager wants a **fixed-horizon hedge** against realized volatility over that horizon. - Operational simplicity (a single OTC contract) and limited need for dynamic management are desired. - The investor is comfortable with counterparty and liquidity risk associated with OTC derivatives. They may be less appropriate when: - The portfolio is very concentrated or idiosyncratic, increasing basis risk between portfolio volatility and index variance. - Regulatory or governance frameworks restrict OTC derivatives or require centralized clearing with significant margin. - The manager has strong views on short-term implied volatility moves but not on long-term realized variance (VIX futures might be better). ### RISKS, PITFALLS, AND BEST PRACTICES ### Key Risks and Limitations Variance swaps introduce several distinct risks. - Tail risk and volatility-of-volatility risk (for short positions): A short variance swap earns the variance risk premium in calm markets but can suffer very large losses if volatility spikes sharply, as realized variance can increase dramatically due to squared returns. - Mark-to-market volatility and margin calls: Even if realized variance over the full period ultimately matches the strike, large interim movements in implied volatility can cause mark-to-market swings and margin calls, which can be problematic for liquidity-constrained investors. - Basis risk: When using an index variance swap to hedge a specific portfolio, hedge effectiveness depends on the correlation between portfolio returns and index returns. A diverging correlation, especially in stress periods, can reduce hedge effectiveness. - Counterparty and liquidity risk: Variance swaps are OTC instruments. Liquidity tends to be best for major equity indexes and can dry up in stressed markets. Counterparty credit risk is mitigated by collateralization but does not disappear. - Model and implementation risk: Mis-estimating the relationship between variance swaps and related options, or misunderstanding the contract specifications (for example, realized variance calculation methodology), can lead to mispricing or mis-hedging. > **Key Term: tail risk** > Tail risk refers to the risk of extreme portfolio losses that occur in the far tails of the return distribution, often associated with crises and volatility spikes. ### Common Exam Pitfalls > **Exam Warning:** > For the exam, be particularly careful to distinguish **variance** from **volatility** and to interpret notional and strike correctly when computing cash flows. Typical pitfalls: - Confusing volatility and variance: If a question gives volatility (for example, 20%), you must square it (0.04) to obtain variance when applying the standard payoff formula, unless the strike is already given in variance terms. - Misinterpreting the notional: Some questions specify **vega notional** rather than variance notional. If so, you must convert using $$ N_{\text{variance}} = \frac{N_{\text{vega}}}{2X}$$ before using the variance payoff formula. - Sign conventions: Always clarify whether the question is asking for the payoff to the **long** or **short** variance position. Start from the formula from the long side’s standpoint, then invert the sign for the short. - Ignoring time weighting in mark-to-market: When valuing a swap mid-life, properly weight realized and implied variance by $t/T$ and $(T-t)/T$ as in the mark-to-market formula. - Assuming variance swaps are identical to VIX: VIX measures expected short-term implied volatility, not realized variance over the swap’s horizon. Do not treat them as interchangeable. ### Best Practices in Implementation In practice, institutional managers using variance swaps often: - Limit the size of short-variance positions relative to capital, recognizing the potential for nonlinear losses. - Combine long variance swaps with other derivative overlays (for example, out-of-the-money put spreads) to shape the payoff profile. - Use stress tests and scenario analysis to evaluate how the variance swap and the overall portfolio behave under extreme volatility scenarios. - Align the hedge horizon with the risk horizon specified in the IPS (for example, one-year risk budget). > **Key Term: volatility derivatives** > Volatility derivatives are financial instruments whose primary payoff depends on the volatility of a reference asset or index, rather than its price level, including VIX futures and options, variance swaps, and volatility swaps. ## Summary Variance and volatility swaps extend the toolbox for managing volatility risk beyond standard options and futures: - Variance swaps deliver **linear exposure to realized variance**, independent of the final asset level, making them powerful tools for hedging or speculating on volatility in a clean, targeted way. - Long variance positions are effectively **long volatility, long gamma**, and convex in volatility, offering attractive tail-risk protection for equity portfolios. - Short variance positions seek to harvest the **variance risk premium** but expose the investor to potentially large losses in stress scenarios. From a Level 3 exam standpoint, being able to: - Map portfolio exposures (for example, option overlays, structured notes, concentrated equity) into volatility and variance risks, - Choose between variance swaps, VIX derivatives, and option strategies given an objective, and - Compute and interpret variance swap payoffs and P&L, is central to integrating derivatives into comprehensive portfolio risk management. ## Key Point Checklist _This article has covered the following key knowledge points:_ - Differentiate volatility risk and variance risk and describe their role in portfolio risk management. - Explain how long and short gamma exposures arise in portfolios and why volatility management is critical for tail-risk control. - Describe the structure, quoting convention (volatility strike and vega notional), pricing, and settlement of variance swaps. - Compute realized variance from return data and calculate variance swap payoffs to both long and short counterparties. - Distinguish variance swaps from volatility swaps, VIX futures, and long straddle strategies, including their economic exposures. - Evaluate when variance swaps are the most appropriate tool for hedging or expressing volatility views, relative to options and volatility index derivatives. - Identify and avoid common exam pitfalls, including confusion between variance and volatility, incorrect use of notionals, and sign errors in P&L calculations. - Recognize key implementation risks of variance swaps, including tail risk, volatility-of-volatility, basis risk, and counterparty risk. ## Key Terms and Concepts - volatility risk - variance swap - volatility swap - realized volatility - realized variance - implied volatility - volatility index (VIX) - volatility futures - variance strike - variance notional - vega notional - gamma - short gamma - long gamma - volatility-of-volatility - variance risk premium - tail risk - volatility derivatives