Learning Outcomes

This article explains derivatives-based portfolio risk management with swaps, collars, and protective put strategies in a CFA Level 3 context. It outlines the structure, cash-flow mechanics, and basic valuation of plain-vanilla interest rate and equity swaps, and how they are used to adjust duration, yield-curve exposure, and equity or sector exposure without trading the underlying securities. The article details how to design collar and protective put overlays, including option type, strike and maturity choices, and zero-cost versus premium-paying structures, and how to diagram and interpret their payoff profiles. It compares swaps, options, futures, and direct asset trades as alternative hedging tools, highlighting when each is most appropriate. Key risks—basis, gap, counterparty, liquidity, and collateral or margin risk—are evaluated, and guidance is provided on selecting and justifying derivative strategies, using qualitative reasoning and simple numerical calculations, in IPS-based, exam-style scenarios with concentrated positions and benchmark or regulatory constraints.

Key Term: duration

Duration is a measure of a bond or fixed-income portfolio’s price sensitivity to small parallel shifts in interest rates, commonly interpreted as the approximate percentage price change for a 1% change in yield.

CFA Level 3 Syllabus

For the CFA Level 3 exam, you are required to understand derivatives-based portfolio risk management using swaps, collars, and related protective strategies, with a focus on the following syllabus points:

- Explain the rationale and mechanics of using interest rate and equity swaps to manage risk exposure or alter asset class exposure.

- Describe how exchange-traded and OTC derivatives can be structured to protect against adverse price movements or to synthetically rebalance a portfolio.

- Construct and interpret collar strategies combining protective puts and written calls.

- Assess the suitability of swaps and collars for various risk management objectives and portfolio constraints.

- Evaluate payoff profiles, risks, and limitations of derivatives-based risk management solutions.

- Compare derivatives-based hedges with cash market rebalancing in the context of asset allocation and benchmark management.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

A manager wants to convert a portfolio of fixed-rate bonds into a synthetic floating-rate exposure without selling the bonds. Which derivative is most appropriate?

- a) Long interest rate futures contracts

- b) Short equity index futures

- c) Enter a pay-floating, receive-fixed interest rate swap

- d) Enter a pay-fixed, receive-floating interest rate swap

-

An investor holds a large long stock position and implements a collar by buying a put and selling a call on the same stock. Which risk is most clearly left unhedged?

- a) Downside risk below the put strike

- b) Upside risk above the call strike

- c) Price movements within the band between the put and call strikes

- d) Liquidity risk of the reference stock

-

A portfolio manager wants equity downside protection for six months but considers direct purchase of at-the-money index puts too expensive. Which alternative most closely replicates a protective put at lower initial cost?

- a) Use an equity swap to receive equity total return and pay a floating rate

- b) Implement a zero-cost collar by buying a put and selling an out-of-the-money call

- c) Short index futures contracts equal to the portfolio’s beta-adjusted value

- d) Buy deep-in-the-money calls on the index

-

When hedging a domestic equity portfolio with index options, which source of risk is most likely to remain after implementing a protective put or collar strategy?

- a) Counterparty default risk on exchange-traded options

- b) Basis risk between the index and the specific portfolio holdings

- c) Risk of early exercise of the long put

- d) Risk that the option premium will increase after purchase

Introduction

Derivatives allow portfolio managers to precisely manage risk and return exposures. By incorporating swaps, collars, and protective strategies, managers can either hedge unwanted exposures, create synthetic positions, or construct cost-effective downside protection. This article explains how these techniques work, the key terms involved, and practical CFA exam scenarios you may be tested on. The emphasis at Level 3 is on synthesizing these tools into coherent portfolio recommendations and explaining the trade-offs in qualitative, IPS-based terms.

Key Term: swap

A swap is a contractual agreement in which two parties exchange sequences of cash flows, typically to alter risk exposures or synthetically adjust portfolio positions. Key Term: collar

A collar is an options-based strategy that combines buying a protective put and selling a covered call to cap both downside loss and upside gain on a position over a defined horizon. Key Term: protective put

A protective put is a strategy involving a long position in the asset and a long put option on that asset, providing downside insurance while retaining most upside.

In exam questions, these strategies rarely appear in isolation. You will often be asked to choose between a swap, a futures hedge, a protective put, and a collar, considering costs, constraints (e.g., no short selling, tax deferral), and residual risks.

Using Swaps in Portfolio Risk Management

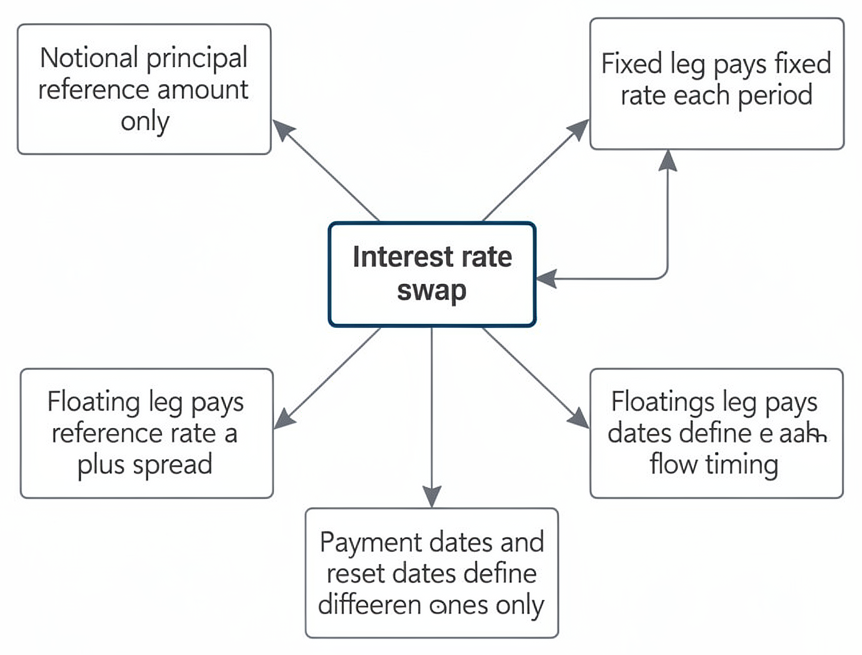

Interest rate swap mechanics include a reference notional, periodic fixed-versus-floating cash flows, scheduled resets, and net settlement of payment differentials.

Mechanics and Purpose of Swaps

Swaps are OTC contracts where two parties agree to exchange sets of cash flows on specified dates and notional amounts. The contract is usually designed so that its value is approximately zero at inception; as market conditions change, the swap’s market value becomes positive for one party and negative for the other.

In most portfolio risk management contexts, the two most common types are interest rate swaps and equity swaps.

Key Term: interest rate swap

An interest rate swap is an agreement to exchange fixed interest payments for floating-rate payments, or vice versa, based on a set notional amount and payment schedule. Key Term: equity swap

An equity swap is a swap in which one party pays the return on an equity index or basket (price change plus dividends), and the other typically pays a fixed or floating interest payment on a notional amount.

Key design features:

- Notional principal: Reference amount on which interest or total returns are calculated; not exchanged in a standard interest rate or equity swap.

- Payment dates / reset dates: Dates when floating rates are set and cash flows are exchanged (e.g., every 3 or 6 months).

- Day-count conventions: Determine the year fraction used to calculate interest for each period.

- Netting: In plain-vanilla interest rate swaps in a single currency, only the net payment (fixed minus floating) is exchanged each period.

Portfolio managers use swaps to:

- Convert fixed-rate to floating-rate (or vice versa) exposure.

- Adjust portfolio duration without buying or selling reference bonds.

- Alter asset class or sector exposure synthetically (for example, shifting from equity to fixed income, or from one equity index to another).

- Manage risk when direct trading of constituent securities is costly, illiquid, or restricted.

Swaps and Duration Management

Conceptually:

- Receive-fixed, pay-floating interest rate swap: Similar to adding a fixed-rate bond and funding it with a floating-rate liability. This increases the portfolio’s interest rate sensitivity (duration).

- Pay-fixed, receive-floating interest rate swap: Similar to issuing a fixed-rate bond and investing in a floating-rate asset. This reduces the portfolio’s duration.

In duration terms, managers target the portfolio’s dollar value of a basis point (DV01 or BPV). To change portfolio duration using swaps, they choose a swap notional so that:

- The change in DV01 from the swap approximately equals the desired change in the portfolio’s DV01.

You are not required to memorize detailed DV01 formulas for swaps, but you must correctly identify the direction (pay-fixed or receive-fixed) and be able to explain how the swap modifies duration and cash flow uncertainty.

Worked Example 1.1

A pension fund holds $50 million in 5-year fixed-rate bonds, but expects rates to rise. How can the fund use swaps to reduce interest rate risk?

Answer:

The fund can enter into a pay-fixed, receive-floating interest rate swap with a notional of $50 million and matching maturity. Economically, this overlays a synthetic short position in fixed-rate exposure on top of the existing fixed-rate bonds, converting the net exposure toward floating rate. The portfolio’s effective duration decreases because the swap position benefits when rates rise (higher floating receipts relative to fixed payments), partially offsetting price losses on the bonds. Residual risks include:

- Basis risk if the bonds’ yields and the swap’s reference rate do not move in lockstep.

- Mismatch risk if maturities or reset dates do not align perfectly with the bond cash flows.

Equity Swaps for Tactical and Strategic Allocation

Equity swaps allow managers to change equity exposures without transacting in the cash equity market. A typical structure:

- One leg: Pay total return on Index A (or a single stock or sector basket).

- Other leg: Receive total return on Index B, or receive a floating rate plus spread.

Applications include:

- Rebalancing across equity markets: E.g., synthetically rotate from domestic equities to emerging market equities while leaving existing holdings unchanged for tax or liquidity reasons.

- Hedging concentrated stock positions: Pay total return on a single stock and receive a floating rate or index return, reducing idiosyncratic risk without an outright sale.

- Equitizing cash: Receive equity index total return and pay a short-term floating rate, creating synthetic equity exposure on idle cash.

On the exam, you should be able to explain which leg the investor should receive or pay to achieve a desired exposure, and why this may be preferable to trading the reference securities (for example, lower transaction costs, avoidance of short-sale restrictions, or tax deferral).

Key Risks of Swaps

Swaps introduce several important risks that must be weighed against their hedging benefit.

Key Term: basis risk

Basis risk is the risk that the derivative used for hedging does not move in perfect correlation with the reference exposure, leaving residual risk.

- Basis risk:

- Interest rate swap vs. specific bonds: The swap’s floating leg is tied to a money market reference rate (e.g., 6‑month Libor or similar), while the bonds’ yields embed credit and liquidity spreads.

- Equity swap vs. portfolio: The index used in the swap may not match the composition or beta of the actual portfolio.

Key Term: counterparty risk

Counterparty risk is the risk that the other party to an OTC derivative contract will default on its obligations.

- Counterparty risk:

- Historically a major concern for bilateral OTC swaps.

- Now often mitigated by central clearing, initial margin, and variation margin, but still relevant in many bespoke or non-cleared swap structures.

Key Term: liquidity risk

Liquidity risk is the risk that a position cannot be unwound or adjusted at a reasonable cost within the desired time frame.

- Liquidity risk:

- Some swap markets (especially for less common equity indices or long-dated tenors) may be illiquid.

- Large notional positions can be costly to unwind, particularly in stressed markets.

Key Term: gap risk

Gap risk is the risk that the reference variable moves sharply between hedge reset dates or collateral calls, creating losses that are not fully offset by the hedge or collateral.

- Gap and collateral risk:

- Swaps often reset discretely (e.g., every 3 or 6 months). Large rate or price moves between reset dates can leave hedges imperfect.

- Adverse market moves can trigger significant collateral calls, forcing asset sales or borrowing at an inconvenient time.

Revision Tip: Remember: exam questions frequently ask how swaps change the duration or beta of a portfolio and why a swap may be preferred to cash-market trades. Be explicit about:

- The direction of the swap (pay-fixed vs receive-fixed, pay-equity vs receive-equity).

- The approximate notional (qualitatively, “match notional to the exposure being hedged” unless DV01 data are provided).

- The new risks introduced (basis, counterparty, liquidity, and collateral risk).

Collars and Their Role in Risk Management

Collars use listed (or OTC) options to define a band of possible returns, providing targeted risk reduction at low or zero cost.

Construction of a Basic Collar

A collar involves holding the reference asset and combining:

- Buy a put option at a chosen strike to insure against a drop below that price (protective put leg).

- Sell a call option at a higher strike to fund the put by giving up upside above that level (covered call leg).

Result:

- Downside loss is limited once the asset price falls below the put strike.

- Upside gain is capped once the asset price rises above the call strike.

- Between the two strikes, the investor participates in most of the price movement, adjusted for net option premium.

Key Term: zero-cost collar

A zero-cost collar is a collar constructed so that the premium paid for the protective put equals (approximately) the premium received for the written call, resulting in no net initial cash outlay (excluding transaction costs).

Strike selection is driven by:

- Risk tolerance: How much downside can be tolerated before protection kicks in?

- Return objectives: At what upside level is the investor content to be “called away”?

- Cost constraints: Willingness (or not) to pay net option premium, especially for longer horizons.

Worked Example 1.2

An investor holds 1,000 shares of XYZ at $60. She buys a $50-strike put for $2 and sells a $70-strike call for $2. What's her payoff profile?

Answer:

Ignoring time value and transaction costs and focusing on payoffs at expiry per share: Below $50: The stock may fall further, but losses are effectively limited. The put finishes in the money with payoff approximately:

offsetting further declines. The maximum loss is about $10 per share (= $60 initial price − $50 protected level), because the net option cost is zero ($2 paid for the put and $2 received for the call). Between $50 and $70: The put expires worthless, and the call is out-of-the-money or at most at-the-money. The investor enjoys linear participation in this range: profit is approximately:

Above $70: The call is exercised. The investor effectively sells the stock at $70. The maximum gain is about $10 per share (= $70 − $60), again adjusted for the zero net premium. This is a zero-cost collar: downside is limited below $50, upside is capped above $70, and the investor gives up potential gains beyond $70 in exchange for downside protection.

In payoff-diagram terms, the collar “compresses” the payoff distribution into a band between the maximum loss and maximum gain.

Practical Guidelines for Using Collars

Collars are especially useful when:

- Protection against larger losses is required, but the investor can give up some upside.

- Cash is scarce, or clients object to paying large visible option premiums.

- Concentrated positions must be hedged without immediate sale (for example, an executive’s stock, large low-basis holdings, or holdings subject to lock-up or insider restrictions).

- Policy or regulation disallows short selling but allows option overlays.

Design considerations:

-

Put strike selection:

- Deeper out-of-the-money (e.g., 10–20% below spot) reduces premium cost but leaves a larger “deductible” before protection starts.

- At-the-money or slightly out-of-the-money puts provide tighter protection but cost more unless offset by a richer call.

-

Call strike selection:

- Strike often set near a realistic target price or valuation ceiling.

- Higher call strikes preserve more upside but may not fully finance the put (non-zero-cost collar).

- Lower call strikes generate more premium (and perhaps zero cost) but sacrifice more upside.

-

Maturity:

- Ideally aligned with the risk horizon: an earnings season, lock-up period, or tax year.

- Long-dated collars provide longer protection but are more sensitive to volatility and may have limited liquidity.

-

Instrument choice:

- Listed options for standardized strikes and maturities, typically on liquid single stocks or major indices.

- OTC options for customized strikes, maturities, and notional sizes, but with counterparty and liquidity considerations.

Risk and Opportunity Cost in Collars

Collars reduce downside risk but introduce:

- Opportunity cost: Foregone upside above the call strike; in qualitative answers, you should explicitly state this.

- Basis risk: When using index options to hedge a portfolio that is not perfectly aligned with the index.

- Early exercise / assignment risk: Most relevant when American options are involved and the written call goes deep in the money, especially around ex-dividend dates.

- Liquidity and roll risk: At expiration, new collars must be rolled if protection is still needed; market conditions (volatility, liquidity) may have changed.

Exam scenarios often ask whether a collar is appropriate for an executive or high-net-worth individual. You should weigh:

- The desire for capital preservation vs. upside retention.

- Any constraints on selling the reference asset.

- Tax considerations (e.g., deferral of capital gains if the asset is not sold).

- The client’s stated return and risk objectives in the IPS.

Protective Put Strategies

Protective puts are simpler than collars—they provide downside asset protection with most of the upside retained. The cost is the option premium.

Mechanically, a protective put combines:

- Long reference asset at price .

- Long put with strike and premium .

At expiry:

- Stock value:

- Put payoff:

- Portfolio value:

The profit at expiry is:

From this, we can derive:

- Maximum loss (for ): occurs when . Portfolio value tends to , so .

- Maximum gain: theoretically unlimited; for , the put expires worthless and , which increases with .

- Breakeven price: for , breakeven when , so .

This is a key comparison with collars: the protective put preserves unlimited upside but requires a cash outlay equal to the put premium.

Worked Example 1.3

A manager wishes to hedge a $5m equity portfolio against significant market falls for the next 6 months. The index at 4,000 has 6‑month at-the-money (ATM) puts priced at 100 (index multiplier = $50). How could this be used?

Answer:

Each index put has a notional value of 4,000 \times 50 = \200,000. The manager needs \5,000,000 of protection, so she buys:

ATM puts (strike 4,000).

- Cost of protection: 25 \times 100 \times 50 = \125,000$.

- Effect: If the index level in six months falls below 4,000, each put gains:

offsetting index declines in the portfolio (assuming beta ≈ 1). Losses below 4,000 are substantially hedged; above 4,000, the puts expire worthless and the manager forgoes only the premium paid. This structure is a protective index put overlay. Residual risks include imperfect beta matching and any active bets relative to the index.

Protective Puts and Option Sensitivities

Protective puts can be understood using option Greeks (from earlier levels):

- Long stock has delta ≈ +1 (per share); long put has delta between 0 and −1.

- Combined position delta is between 0 and +1, reducing downside sensitivity compared to stock alone.

- The protective put is long gamma and long vega, giving convexity: losses are limited when the market falls sharply, while gains remain largely intact when it rises.

However, repeatedly purchasing protective puts as a permanent overlay can be costly and may significantly drag long-term returns. Level 3 questions often involve temporary hedges (around an earnings announcement, macro event, or during a planned liquidity need), where the premium is justified by specific risk management goals.

Worked Example 1.4

A fund holds €100 million of a stock currently trading at €40 and expects that, over the next month, disappointing news could cause at most a 15% drop. One-month put options are available with:

- Strike €36, premium €1.00

- Strike €38, premium €1.80

- Strike €40, premium €3.20

Which put is most appropriate if the goal is to limit drawdown while keeping cost “modest”?

Answer:

The manager expects a worst-case price of about €34 (= €40 × 0.85). Compare breakeven and protection:

- Strike 36 put:

- Breakeven: €36 − €1.00 = €35 (only modest gain if the stock falls to €34).

- Protection starts meaningfully only below €36, leaving a sizeable loss from €40 to €36.

- Strike 38 put:

- Breakeven: €38 − €1.80 = €36.20.

- If the stock falls to €34, the put value is €4, so net benefit vs. no hedge is significant. Premium is moderate.

- Strike 40 put:

- Tightest protection but the highest premium (€3.20). Breakeven: €40 − €3.20 = €36.80. Given the manager wants to limit drawdown but keep cost modest, the €38 strike put is a reasonable compromise: it provides effective protection around the expected downside while avoiding the very high cost of the ATM put.

On the exam, you should explicitly relate strike selection to the expected range of outcomes and the investor’s risk tolerance, not just choose the tightest hedge.

Synthesizing Swaps and Options: Creating Synthetic Positions

Portfolio managers can combine swaps and option-based strategies to structure tailored solutions, sometimes replicating option payoffs without directly trading the option itself.

Key Term: synthetic position

A synthetic position is a combination of cash instruments and/or derivatives constructed to replicate the payoff of another position.

Examples:

-

Synthetic equity exposures:

- Use an equity swap (receive equity total return, pay floating rate) to replace direct equity purchases or to gain exposure when market access is restricted.

-

Synthetic downside protection:

- Use combinations of forwards/futures and options to replicate puts or calls, exploiting put–call parity.

Synthetic Long Put and Long Call

From the options reading:

-

Synthetic long put:

- Short stock at price and long call with the same strike and maturity.

- At expiry, this payoff is identical to a long put with strike .

-

Synthetic long call:

- Long stock at and long put with strike (a protective put).

- At expiry, this payoff is identical to a long call with strike .

These identities help in understanding protective strategies:

- A protective put can be viewed as a synthetic long call on the asset.

- A manager who cannot trade calls directly might implement a protective put plus financing cash position to achieve similar risk-return characteristics.

Worked Example 1.5

Three months ago, a manager entered a short forward contract to deliver 50,000 shares of stock ABC at €18 in one month. The stock is now at €16. She remains bearish but wants to cap potential losses if the stock unexpectedly rallies on earnings. How can she modify the position?

Answer:

The current short forward pays off at expiry:

with unlimited loss potential if the stock price at expiry rises substantially above €18. To introduce downside protection on the short position (i.e., protection against price increases), she can buy a call with strike close to the current spot, say €16, expiring in one month. Combined position: Short forward: payoff

Long €16 call: payoff

For terminal prices at or below €16, the call expires worthless; she keeps the forward profit less the call premium. For terminal prices above €16, the long call gains value, offsetting increasing losses on the short forward. Her maximum loss is capped at approximately:

This is effectively transforming the linear short-forward payoff into an asymmetric profile similar to a synthetic long put.

Swaps and Options in Asset Allocation

Swaps and options can be combined to adjust exposures and risk characteristics:

- Use an equity swap to move from domestic equity to global equity exposure without liquidating existing holdings.

- Add a protective index put or collar on top of the new synthetic equity exposure to control drawdown risk.

- Combine interest rate swaps with bond futures and swaptions (options on swaps) for more flexible duration and convexity management.

These are typical Level 3 essay-style scenarios: you must justify why a particular combination best fits the client’s objectives, constraints, and views, compared to pure cash or futures-based adjustments.

Exam Warning: A common exam error is failing to account for the cash flows and risks of both legs of a derivative strategy. When describing a collar, protective put, or swap overlay, always specify:

- Which positions are long and which are short.

- The strikes, maturities, and notionals.

- Both the benefits (e.g., limited downside) and the costs/opportunity losses (e.g., capped upside, option premiums, collateral requirements).

Comparing Swaps, Collars, and Protective Puts

In practice and in exam questions, you will often have to choose between multiple derivative tools. Key comparative points:

-

Swaps vs futures vs cash trades:

- Swaps can restructure exposures without trading reference securities, often with lower upfront cash, but involve counterparty and collateral risk.

- Futures are standardized, exchange-traded, and more liquid, but available only on certain indices or benchmarks.

- Cash trades (buying/selling bonds or equities) directly alter holdings and can have tax and transaction cost implications.

-

Protective puts vs collars:

- Protective puts offer full upside and limit downside but require premium; suitable when upside potential is valued highly and paying for insurance is acceptable.

- Collars provide cheaper or zero-cost protection but cap upside; suitable when the investor is willing to sacrifice gains beyond a target level.

-

Swaps vs options for hedging equity risk:

- An equity swap that pays equity return and receives a floating rate can eliminate equity risk entirely for the swap notional, but also eliminates upside.

- A collar or protective put reduces downside risk while retaining some or all upside, more consistent with typical equity investment objectives.

Worked Example 1.6

A private client holds 500,000 shares of her employer’s stock, currently at $40, representing a large fraction of her wealth. She cannot sell for the next 18 months due to insider restrictions but wants to reduce downside risk while retaining some upside. Her IPS indicates:

- High concern for capital preservation.

- Willingness to forgo some gains above $50.

- Aversion to large upfront cash outlays.

Which derivative-based strategy is most appropriate?

Answer:

Given: Concentrated, restricted stock position. Emphasis on capital preservation. Willingness to cap upside above a target ($50). Preference for low or zero initial cash outlay. A long-dated zero-cost collar on the employer’s stock is most appropriate: Buy an 18‑month put with strike somewhat below $40 (e.g., $35–$38) to limit downside. Sell an 18‑month call with strike around $50–$55 to finance the put premium. This structure: Aligns with the holding restriction (no need to sell shares). Reduces the risk of large wealth losses if the stock falls. Satisfies the client’s willingness to give up some upside in exchange for protection. Alternative strategies such as an equity swap that pays the stock’s return and receives a floating rate would hedge risk but eliminate all upside, which conflicts with her desire to retain some appreciation potential.

On the exam, you would also note implementation details (likely OTC options with a dealer), counterparty risk, and the need to ensure the collar does not breach insider or regulatory constraints.

Summary

Swaps, collars, and protective strategies are versatile tools in the portfolio risk management toolkit:

- Swaps adjust exposures across interest rates or asset classes without trading constituent assets, enabling duration modification, equity rotation, and cash equitization.

- Collars and protective puts offer structured methods to manage downside equity risk, with explicit trade-offs between cost and upside participation.

- Synthetic constructions using swaps and options allow replication of desired payoff profiles when direct implementation is infeasible or inefficient.

For CFA Level 3, precise understanding and clear explanation of payoffs, risks, and implementation details—framed within client objectives and constraints—are essential. You should be comfortable evaluating alternatives and recommending the derivative strategy that best balances risk reduction, cost, and opportunity cost.

Key Point Checklist

This article has covered the following key knowledge points:

- Explain the structure and risk management purpose of interest rate swaps and equity swaps.

- Describe how swaps can be used to increase or decrease portfolio duration without selling reference bonds.

- Construct basic collar strategies and describe their risk/reward profiles, including maximum loss and maximum gain.

- Distinguish between protective puts and collars in terms of cost, upside participation, and suitability for different investor profiles.

- Identify advantages, risks, and trade-offs of using swaps and collars versus direct asset or simple option positions.

- Calculate and interpret payoffs for swaps, collars, and protective puts at option expiry, including breakeven levels.

- Recognize synthetic risk management applications of combining swaps and options, such as synthetic puts and calls.

- Evaluate basis risk, gap risk, counterparty risk, liquidity risk, and collateral impacts introduced by derivative overlays.

- Assess the appropriateness of swaps, collars, and protective puts in IPS-based scenarios with concentrated positions, constraints, and specific risk objectives.

Key Terms and Concepts

- duration

- swap

- collar

- protective put

- interest rate swap

- equity swap

- basis risk

- counterparty risk

- liquidity risk

- gap risk

- zero-cost collar

- synthetic position