Learning Outcomes

After completing this article, you will be able to define a cash-generating unit (CGU), explain why and how impairment losses are allocated within a CGU, and understand the special rules for allocating impairment to goodwill. You will also be able to perform the key impairment calculations for groups of assets, and apply these concepts to typical ACCA FR exam scenarios.

ACCA Financial Reporting (FR) Syllabus

For ACCA Financial Reporting (FR), you are required to understand the principles and calculations of impairment of assets—especially as they relate to cash-generating units and goodwill. Revision for this topic should ensure you can:

- Define "cash-generating unit" and identify situations when individual asset impairment is not practical

- State the basis for impairment loss allocation within a CGU

- Apply the order required by IAS 36 for allocating impairment between goodwill and other assets

- Perform impairment loss calculations involving goodwill at group level in accordance with the standard

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is a cash-generating unit (CGU) according to IAS 36?

- If a CGU comprising goodwill, plant, and land must be impaired, in which order are assets reduced?

- Can an individual asset within a CGU be written down below its recoverable amount under IAS 36?

- True or false? Goodwill impairment losses can be reversed in future periods under IFRS.

Introduction

Impairment of assets under IAS 36 ensures that assets are not carried in financial statements above the amount recoverable from their use or sale. But for many items—like part of a factory or store—calculating "recoverable amount" for each item is not realistic. Instead, these assets are grouped into a cash-generating unit (CGU). Understanding how to define a CGU and allocate impairment, especially when goodwill is present, is key for FR exam success.

Key Term: cash-generating unit (CGU)

The smallest identifiable group of assets that generates cash inflows largely independent of those from other assets or groups of assets.Test Tip: When revising Cash-generating units and goodwill allocation, connect each definition, method, or rule to the kind of question the assessment is likely to ask.

Cash-Generating Units (CGUs): Definition and Purpose

Some assets do not generate separate cash inflows—they work together with other assets to generate income. When you cannot determine an individual asset's recoverable amount, IAS 36 requires you to group the related assets into a CGU and assess impairment on the group as a whole.

Common examples of CGUs:

- A retail store (where individual fixtures or equipment do not generate cash separately)

- A manufacturing line within a factory

Goodwill and Cash-Generating Units

When a business acquires a subsidiary and pays more than the net fair value of its assets and liabilities, the excess is recognised as goodwill.

Key Term: goodwill

The excess of the purchase consideration over the identifiable net assets acquired in a business combination.

Goodwill is never tested for impairment individually—it must be assigned to a CGU or group of CGUs expected to benefit from the synergies of the combination. Misallocating or failing to test goodwill properly is a frequent exam pitfall.

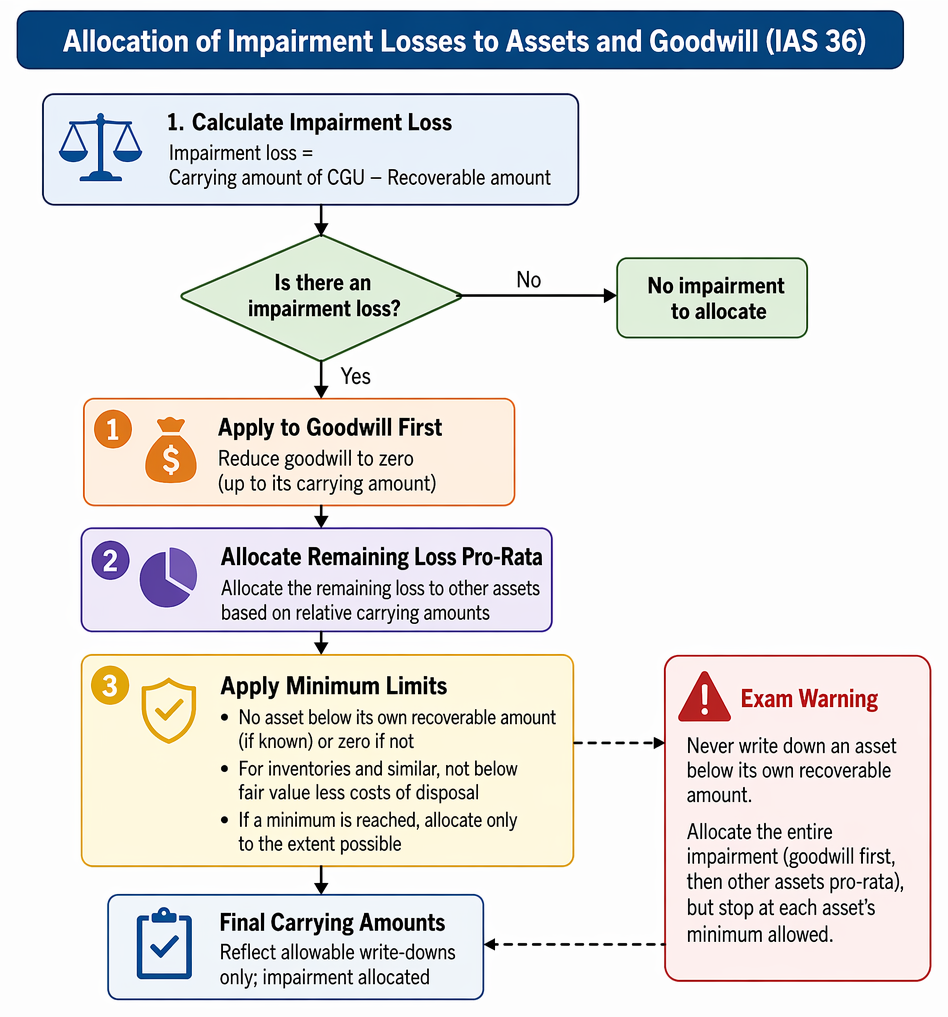

The Impairment Test: Allocation of Losses to Assets and Goodwill

An impairment loss for a CGU is determined by comparing its total carrying amount with its recoverable amount (the higher of value in use and fair value less costs of disposal).

CGU impairment is measured and allocated first to goodwill, then pro rata to other assets, without breaching recoverable amount constraints.

- If the carrying amount > recoverable amount, the unit is impaired.

- The impairment loss must be allocated:

- First, to reduce goodwill allocated to the CGU to zero.

- Then, pro rata to the carrying amounts of other assets in the unit based on their relative carrying values.

- However, no asset can be written down below its individual recoverable amount (if known) or zero if not, nor below fair value less costs of disposal for specifically measurable assets such as inventories.

Key Term: recoverable amount

The higher of an asset’s or CGU’s fair value less costs of disposal and its value in use. Key Term: impairment loss

The amount by which the carrying amount of an asset or CGU exceeds its recoverable amount.

Worked Example 1.1

Scenario Delta Ltd operates a division with the following assets:

- Goodwill: $100,000

- Equipment: $200,000 (recoverable amount $190,000)

- Fixtures: $120,000 (recoverable amount $110,000)

- Inventory: $80,000 (net realisable value $80,000)

The recoverable amount of the CGU as a whole is calculated to be $420,000.

Required: Allocate the impairment loss.

Answer:

- Total carrying amount: $100,000 (Goodwill) + $200,000 (Equipment) + $120,000 (Fixtures) + $80,000 (Inventory) = $500,000

- Impairment loss = $500,000 – $420,000 = $80,000

- Step 1: Apply loss to goodwill: $100,000 (but only $80,000 is needed)

- Goodwill is reduced to $20,000; but, per IAS 36, the entire loss is first allocated to goodwill up to its carrying amount, so impair goodwill by $80,000.

- Revised balances: Goodwill = $20,000 (if more impairment remaining, would then allocate to other assets pro-rata)

- Here, no further loss remains, so only goodwill is reduced.

Worked Example 1.2

Scenario Suppose instead that the CGU's recoverable amount is only $370,000, with the same initial asset balances as above.

Answer:

- Impairment loss = $500,000 – $370,000 = $130,000

- Step 1: Allocate to goodwill: $100,000 (reduce to nil)

- Remaining loss to allocate: $30,000

- Step 2: Allocate $30,000 pro-rata to equipment and fixtures (ignore inventory as it already equals NRV).

- Pro-rata basis (equipment + fixtures): $200,000 + $120,000 = $320,000

- Equipment: $30,000 × $200,000/$320,000 = $18,750

- Fixtures: $30,000 × $120,000/$320,000 = $11,250

- Check that neither is written below its individual recoverable amount. Final carrying amounts:

- Equipment: $200,000 – $18,750 = $181,250 (cannot go below recoverable amount $190,000, so limit write-down to $10,000).

- Fixtures: $120,000 – $11,250 = $108,750 (cannot go below recoverable amount $110,000, so limit write-down to $10,000).

- If pro-rata allocations would exceed minimums, allocate only to extent possible; any unallocated impairment is left.

Exam Warning: When allocating impairment losses, never write down an asset below its own recoverable amount. The entire impairment must always be fully allocated (goodwill, then other assets pro-rata), but "stop" at the minimum allowed for each asset.

Special Restrictions—Goodwill Reversal Prohibited

Impairment losses recognised for goodwill must never be reversed in future periods, even if conditions improve. This is a strict IFRS rule, and any reversal of goodwill impairment is not allowed for FR exam purposes.

Key Term: reversal of impairment loss

Recognition of an increase in the estimated recoverable amount of an asset previously impaired, limited to the carrying amount as if impairment had never occurred. Key Term: individual asset’s recoverable amount

The recoverable amount determined for a specific asset within a CGU, used as a floor when allocating impairment.

Step Summary for Allocating Impairment in a CGU with Goodwill

-

Identify the CGU and calculate total carrying amount including goodwill.

-

Calculate recoverable amount of the CGU.

-

The impairment loss is the excess of the total carrying amount over the recoverable amount.

-

Allocate:

- First, write down goodwill, up to its carrying amount.

- Then, distribute any remaining loss pro rata among other assets, but not below their individual recoverable amounts.

-

No asset (other than goodwill) should be written below recoverable amount (or net realisable value for inventory).

-

Goodwill impairment is never reversed—other assets may have reversals if justified by IAS 36.

Summary

IAS 36 requires that when an individual asset’s recoverable amount cannot be estimated, assets must be grouped into cash-generating units (CGUs). If a CGU including goodwill is impaired, the loss is allocated first to reduce goodwill, then to other assets pro rata, but not below individual recoverable amounts. Goodwill impairment cannot be reversed in future periods, while other assets are subject to potential reversal only if certain strict criteria are met.

Key Point Checklist

This article has covered the following key knowledge points:

- Define “cash-generating unit (CGU)” and “goodwill” for FR exam purposes

- Explain why and how CGUs are used in impairment reviews

- Describe the required order for allocating impairment losses (goodwill, then other assets pro rata)

- State that goodwill impairment cannot be reversed under IFRS

- Apply the process for impairment loss allocation to worked examples

Key Terms and Concepts

- cash-generating unit (CGU)

- goodwill

- recoverable amount

- impairment loss

- reversal of impairment loss

- individual asset’s recoverable amount