Learning Outcomes

This article provides an overview of the decision-making processes within companies, focusing on board meetings and general meetings. It outlines the procedures for calling and conducting meetings, the types of resolutions passed, and the associated administrative requirements. For the SQE1 assessments, you need to understand how directors and shareholders make decisions, the rules governing meetings and resolutions (including ordinary and special resolutions, and written resolutions), and the importance of complying with the Companies Act 2006 and the company's articles. This knowledge will enable you to apply these principles to SQE1-style multiple-choice questions.

In addition, you should be comfortable distinguishing directors’ collective decision-making under the Model Articles (including notice, quorum, voting and conflicts rules), recognising when shareholder approval is required by statute or the articles, and applying the resolution thresholds and procedures (general meetings, written resolutions, and where applicable special notice). Understanding practical points such as short notice, deemed service, poll demands, proxies and corporate representatives, and the filing and record-keeping obligations will allow you to validate meeting outcomes. You should also be aware of the role of the articles in allocating powers (MA 3 and MA 4), directors’ delegation (MA 5), and how unanimous shareholder assent can sometimes substitute for formal procedures (Duomatic principle), ensuring decisions are valid and enforceable.

SQE1 Syllabus

For SQE1, you are required to understand the core principles of corporate governance and compliance relating to decision-making processes. This involves knowing the procedures for board and general meetings, including notice, quorum, and voting requirements, and the distinction between different types of resolutions. Your understanding of company administration and filing requirements is also assessed, with a focus on the following syllabus points:

- the division of decision-making powers between directors and shareholders

- the procedures for calling and conducting valid board meetings (BMs)

- the requirements for calling and conducting valid general meetings (GMs)

- the difference between ordinary resolutions (ORs) and special resolutions (SRs), including the majorities required

- the procedure for passing written resolutions (WRs) in private companies

- the administrative and filing requirements associated with company resolutions and meetings.

- members’ requisition rights to require directors to call a GM and timelines (ss 303–305 CA 2006)

- short notice and special notice, deemed delivery rules, and poll demands

- directors’ conflicts: declaration duties (ss 177, 182 CA 2006) and the effect of MA 14

- shareholder approvals required for specific director-related transactions (e.g. substantial property transactions, loans, long-term service contracts)

- the role of the company’s articles (including MA 3, MA 4, MA 5, MA 7–15) and any amendments impacting decision-making.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

What is the default quorum required for a valid board meeting under the Model Articles for private companies?

- a) One director

- b) Two directors

- c) A majority of the directors

- d) All directors.

-

Which type of resolution requires a majority of 75% or more of the votes cast to be passed?

- a) Board resolution

- b) Ordinary resolution

- c) Special resolution

- d) Written resolution.

-

A private company wishes to call a general meeting. What is the minimum notice period required under the Companies Act 2006, assuming no agreement to short notice?

- a) 7 clear days

- b) 14 days

- c) 14 clear days

- d) 21 clear days.

-

Which of the following decisions typically requires a special resolution?

- a) Appointing a director

- b) Declaring a dividend

- c) Removing a director

- d) Amending the articles of association.

Introduction

Effective decision-making is fundamental to the proper functioning and governance of a company. The Companies Act 2006 (CA 2006), along with a company's articles of association, establishes the framework for how decisions are made. Power is typically divided between the directors, who manage the company's day-to-day business, and the shareholders (members), who own the company and vote on significant matters. Directors usually make decisions collectively at board meetings (BMs), while shareholders make decisions by passing resolutions, either at general meetings (GMs) or via written resolutions (for private companies). Understanding these distinct processes and the rules governing them is essential for compliance and for advising clients.

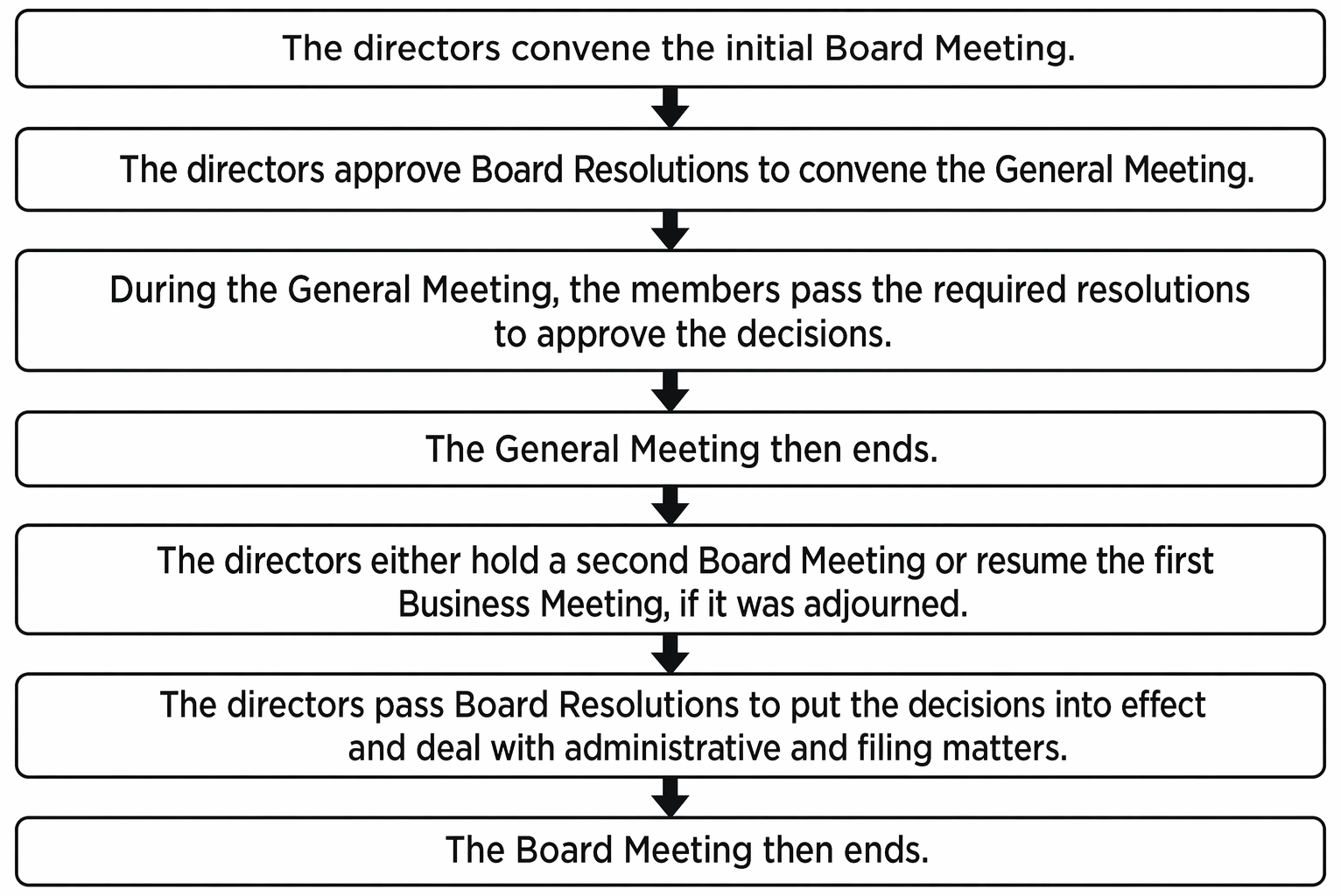

Steps for board decision-making, covering notice, quorum, disclosure of directors’ interests, member approval, and Companies House filings.

Under the Model Articles for private companies limited by shares, directors have authority to manage the company’s business (MA 3) and may delegate their powers (MA 5) to committees, individual directors or employees as appropriate. Members retain control over certain major matters by statute (e.g. amending the articles, changing the company name) or the articles. Notably, members may by special resolution direct the directors to take, or refrain from taking, specified action (MA 4), underscoring the ultimate authority members possess over the company’s constitution and strategic direction. Some shareholder decisions simply authorise the board to proceed with transactions where conflicts or risks exist (for example, substantial property transactions with directors), while other shareholder decisions directly alter the company’s constitution or structure.

Key Term: Quorum

The minimum number of directors (or members, for a general meeting) who must be present for valid decisions to be taken at a meeting.Test Tip: In SQE-style questions on Decision-making processes (board meetings, general meetings), identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

Directors' Decision-Making: Board Meetings

The directors are responsible for the management of the company's business and typically exercise their powers collectively through board meetings (BMs).

Calling Board Meetings

Under the Model Articles for private companies (MAs), any director may call a board meeting (MA 9(1)). Notice must be given to every director, wherever they are (MA 9(1)). The notice does not need to be in writing (MA 9(3)). What constitutes sufficient notice depends on what is reasonable in the circumstances (Browne v La Trinidad; Re Homer District Consolidated Gold Mines, ex p Smith). Reasonable notice varies with the company’s size, complexity and geography: a small, co-located board might accept very short notice; a board with directors in multiple time zones will require longer. The notice must indicate the proposed date, time, and place of the meeting, and how directors participating remotely can communicate (MA 9(2), MA 10(2)). If a director is omitted from notice, they may require that the meeting be re-held with them present, though a director can waive the irregularity within seven days of becoming aware (MA 9(4)).

Board meetings can be held with directors in different locations, provided each can communicate to the others any information or opinions they have on the business of the meeting (MA 10(1)(b)). Modern practice includes telephone or video conferencing, or other real-time communication platforms.

Quorum

For a BM to be valid, a minimum number of directors must be present. This minimum number is known as the quorum.

Under the MAs, the quorum for BMs is two directors (MA 11(2)), unless the company only has one director (MA 7(2)) or the articles specify a different number. Quorum must be maintained throughout the meeting. If the number of directors falls below the quorum requirement, the remaining director(s) can only act to appoint further directors or call a general meeting to enable member appointment of directors (MA 11(3)). Directors do not need to be physically in the same place, provided they can communicate with each other (MA 10). If a director cannot be counted in the quorum due to a conflict (see MA 14), the board must still have a quorum of eligible, non-conflicted directors.

A practical consequence in smaller boards is that MA 14 can render the board inquorate when a conflicted matter is under consideration. In such companies, it is common to amend the articles to relax MA 14’s restrictions (see below), or to ensure there are enough independent directors to form a quorum when conflicts arise.

Voting at Board Meetings

Decisions at BMs are usually taken by a majority vote on a show of hands (MA 7(1)). Each director typically has one vote. The articles may grant the chairperson a casting vote in the event of a tie (MA 13(1)), though companies sometimes disapply the casting vote to facilitate consensus. The chair’s casting vote will only operate if the chair personally supports the resolution; a tied vote where the chair opposes the resolution means the resolution fails.

Directors with a personal interest in a matter being discussed may be precluded from voting or counting towards the quorum under the company's articles (e.g., MA 14), although exceptions exist (MA 14(3), (4)). Typical exceptions include matters relating to the director’s own service contract terms considered by the board, transactions with a wholly-owned subsidiary, or arrangements that do not present a conflict reasonably likely to arise. Separate and independent from MA 14, directors must declare the nature and extent of any interest in a proposed transaction or arrangement with the company (s 177 CA 2006), and for existing transactions (s 182 CA 2006), subject to statutory exceptions (e.g., where the interest is not reasonably likely to give rise to a conflict or where the other directors are already aware of the interest). Disapplying MA 14 in the articles does not disapply the statutory duty to declare interests.

Unanimous Decisions

Directors can also make decisions without a formal BM if all eligible directors indicate to each other that they share a common view on a matter (MA 8(1)). This allows for flexibility, particularly in smaller companies, where decisions can be documented through a directors' written resolution signed by all eligible directors, or by unanimous agreement evidenced in other ways. The key is unanimity among eligible directors; if one director dissents, the decision must be taken at a properly convened meeting.

Record Keeping

Companies must keep records of all board proceedings (minutes) for at least ten years (s 248 CA 2006, MA 15). Minutes should be retained at the registered office or any Single Alternative Inspection Location (SAIL), and companies can opt to keep certain statutory registers on the central register at Companies House. Failure to keep minutes is a criminal offence committed by the company and every officer in default.

Worked Example 1.1

TechStart Ltd has three directors: Alice, Ben, and Chloe. Its articles incorporate MA 11 and MA 14 without amendment. A board meeting is called to approve a contract with a supplier company in which Ben has a significant personal financial interest. Alice and Chloe attend the meeting, but Ben is travelling and cannot attend. Can the remaining directors approve the contract?

Answer:

Yes. The quorum required is two directors (MA 11(2)). Alice and Chloe constitute a quorum. Ben has a personal interest and would not have been able to vote or count in the quorum under MA 14 had he attended. Provided Alice and Chloe both vote in favour (a majority of those present and eligible to vote), the resolution to approve the contract can be validly passed. Ben must still declare his interest under s 177 CA 2006.

Shareholders' Decision-Making: General Meetings and Resolutions

While directors handle day-to-day management, certain key decisions are reserved for the shareholders (members), either by statute or the articles. Shareholders exercise their power by passing resolutions.

Some shareholder decisions authorise directors to proceed with transactions involving directors (e.g., loans, substantial property transactions), while others change the constitution or structure (e.g., amending the articles, changing the company name). Under MA 4, members may by special resolution direct the directors to take specified action. Typical ordinary resolutions under the Model Articles or statute include authorising loans to directors (s 197), approving substantial property transactions (s 190), ratification of a director’s breach of duty (s 239), removing a director (s 168), removing an auditor (s 510) and authorising buybacks (ss 694–696). Typical special resolutions include changing the company name (s 77), amending the articles (s 21), disapplying statutory pre-emption rights (s 569) and approving certain payments out of capital.

Types of Resolution

There are two main types of shareholder resolution:

Key Term: Ordinary Resolution

A resolution passed by a simple majority (more than 50%) of the votes cast by members entitled to vote (s 282 CA 2006). This is the default resolution unless statute or the articles require a special resolution. Key Term: Special Resolution

A resolution passed by a majority of not less than 75% of the votes cast by members entitled to vote (s 283 CA 2006). Required for more significant decisions, such as changing the company name (s 77) or amending the articles (s 21).

Methods of Passing Resolutions

Shareholders can pass resolutions either at general meetings (GMs) or, for private companies, by using the written resolution procedure. There is also a recognised common law route for unanimous shareholder assent.

Key Term: Duomatic Principle

Where all shareholders entitled to vote unanimously and fully informally assent to a matter that could be carried into effect at a general meeting, that assent is as effective as a resolution passed at a properly convened meeting. It requires genuine, unanimous consent by all eligible members.

General Meetings (GMs)

Key Term: General Meeting

A formal meeting of the company's members (shareholders) where they vote on resolutions.

Public companies must hold an Annual General Meeting (AGM) within six months of their financial year-end (s 336 CA 2006). Private companies are not required to hold AGMs unless their articles specify. Any other meeting of members is simply a General Meeting (GM). In practice, private companies often use written resolutions to avoid convening GMs unless statute requires a meeting (e.g., removal of a director or an auditor, which cannot be done by written resolution: s 288(2)).

Calling General Meetings

GMs are usually called by the directors (s 302 CA 2006). However, members holding at least 5% of the paid-up voting share capital (or, in companies limited by guarantee, 5% of total voting rights) can require the directors to call a GM (s 303 CA 2006). The request must state the general nature of the business to be dealt with at the meeting (s 303(4)(a)) and may include a resolution to be moved. Once a valid request is received, the directors must call a GM within 21 days (s 304(1)(a)), to be held on a date not more than 28 days after the notice convening the meeting is given (s 304(1)(b)). This timeline prevents directors frustrating the requisition by undue delay. If the directors fail to call the meeting, the requisitioning members (or members representing more than 50% of the total voting rights of the requisitionists) may call the meeting themselves (s 305 CA 2006). The court also has the power to order a meeting (s 306 CA 2006).

Directors normally control the agenda by settling the notice and supporting materials, and within their fiduciary duties may circulate materials at the company’s expense encouraging support for the board’s position. Members can counterbalance this by requiring the company to circulate a statement of up to 1,000 words relating to proposed resolutions or other business of the meeting, if statutory thresholds are met (s 314 CA 2006). In practice, requisitioning and member statements are valuable tools when shareholders wish to remove a director or press for governance changes.

Notice of General Meetings

Proper notice is essential for a valid GM (s 301 CA 2006).

- Period: At least 14 clear days' notice is required (s 307(1) CA 2006).

Key Term: Clear Days

A period excluding the day the notice is given (or deemed given) and the day of the meeting itself (s 360 CA 2006).

When notice is sent by post or electronically, it is deemed received 48 hours after sending (s 1147(2) CA 2006). This adds two days onto the minimum timetable before counting the 14 clear days. Public company AGMs require 21 clear days' notice (s 307(2)).

-

Short Notice: A GM can be held on shorter notice if agreed by a majority in number of members who together hold at least 90% of the nominal value of the voting shares (95% for PLCs) (s 307(5),(6) CA 2006). Short notice cannot be used to circumvent statutory special notice requirements (see below).

-

Special Notice: Some resolutions require special notice of at least 28 clear days before the meeting (s 312 CA 2006), notably resolutions to remove a director (s 168; s 312 for special notice; s 169 rights of representation) and to remove an auditor (s 510; special notice requirement in s 511). Special notice ensures the affected officeholder has time to make representations. If after special notice has been given, a meeting is called for a date fewer than 28 days after that notice, the special notice is deemed properly given (s 312(4)).

Key Term: Special Notice

A statutory requirement that certain resolutions (e.g., removing a director or auditor) be notified to the company at least 28 clear days before the meeting at which they are proposed, enabling the officeholder to respond and members to receive appropriate information.

-

Method: Notice may be given in hard copy, electronically, or via a website, subject to statutory and article requirements (s 308 CA 2006). If using a website, members must be notified of the availability and the address.

-

Content: Notice must state the time, date, place, and general nature of the business (s 311 CA 2006). It must include the full text of any proposed SR (s 283(6)) and inform members of their right to appoint a proxy (s 325). For removal of a director or auditor, the company must notify the officeholder forthwith and circulate any written representations if practicable (s 169(3); s 511(3)).

-

Recipients: Notice must go to all members, directors, and auditors (s 310, s 502 CA 2006).

Quorum at General Meetings

The default quorum for a GM is two qualifying persons (members or their proxies/corporate representatives), unless the company has only one member (quorum is one) or the articles specify otherwise (s 318 CA 2006). A “qualifying person” includes a member, a proxy, or a corporate representative (s 318(3)). If the meeting is not quorate within the timeframe set by the articles (commonly 30 minutes), it must be adjourned or cannot transact business. The chair’s role and adjournment process will be governed by the company’s articles; in the Model Articles, adjourned meetings typically proceed with the members then present.

Voting at General Meetings

Voting is typically by a show of hands (one vote per member present), unless a poll vote is demanded (MA 42). A poll vote means votes are counted according to the number of shares held (one vote per share). A poll can be demanded by the chair, directors, two or more members with voting rights, or members holding at least 10% of the total voting rights (MA 44). Polls are preferred when the shareholdings are unequal, as they reflect economic ownership. Members have a right to appoint proxies to attend, speak and vote (s 324–325 CA 2006), and corporate members may appoint authorised representatives (s 323).

Be alert to statutory vote-disregard rules that override ordinary voting mechanics. For approval of an off-market buyback contract, votes attached to the shares being bought back are ignored (s 695 CA 2006). For ratification of a director’s negligence, default, breach of duty or breach of trust under s 239 CA 2006, the votes of the director in question and any connected members are disregarded.

Worked Example 1.2

A private company with unamended MAs has 100 issued £1 ordinary shares. Shareholder A holds 60 shares, Shareholder B holds 30 shares, and Shareholder C holds 10 shares. An ordinary resolution is proposed at a GM attended by all three shareholders. How will the resolution pass on a show of hands versus a poll vote?

Answer:

On a show of hands, each shareholder has one vote. To pass an OR, more than 50% must vote in favour. This means at least two shareholders must vote yes. A and B voting yes would pass it (2/3 votes). B and C voting yes would pass it (2/3 votes). A and C voting yes would pass it (2/3 votes). On a poll vote, votes are per share. A has 60 votes, B has 30, C has 10. Total votes = 100. An OR needs >50 votes. A can pass the resolution alone (60 votes). B and C together cannot pass it (40 votes).

Written Resolutions (WRs)

Private companies can use written resolutions as an alternative to holding a GM (s 288 CA 2006), except for resolutions to remove a director or auditor (s 288(2)).

Key Term: Written Resolution

A resolution passed by the members of a private company in writing, rather than at a general meeting.

Procedure

-

Proposal: Can be proposed by directors or members holding at least 5% of voting rights (s 292 CA 2006). The articles may reduce this percentage (s 292(5)).

-

Circulation: Must be sent to all eligible members (s 291). The document must explain how to signify agreement and specify the deadline (lapse date) (s 291(4)).

-

Voting: Members signify agreement in writing. It requires the same majority as a resolution at a GM (>50% for OR, 75%+ for SR), but calculated based on the total voting rights of all eligible members, not just those who respond (s 282(2), s 283(2)). This means abstentions (non-responses) effectively count against the resolution.

-

Lapse Date: Usually 28 days from circulation, unless the articles specify otherwise (s 297). The resolution passes as soon as the required majority is reached (s 296(4)). Circulation by post or email does not affect the 28-day calculation.

Members holding at least 5% can require the company to circulate their proposed written resolution together with a statement of up to 1,000 words (s 292(3)), but must pay the company’s reasonable expenses for circulation (s 294). This is often used when seeking to authorise director-related transactions or constitutional changes without convening a meeting.

Worked Example 1.3

Notice of a GM is posted to members on Monday 1 March. What is the earliest valid meeting date on minimum notice?

Answer:

Posted notices are deemed received 48 hours after posting (s 1147(2) CA 2006), so deemed receipt is Wednesday 3 March. The 14 clear days run from Thursday 4 March to Wednesday 17 March (excluding the day of deemed receipt and the meeting day). The earliest valid meeting date is Thursday 18 March.

Worked Example 1.4

A private company has 100 issued ordinary shares. A written special resolution is circulated to all eligible members. Shareholder X holds 74 shares and votes in favour. Shareholder Y holds 26 shares and does not respond. Does the special resolution pass?

Answer:

No. For a written SR, at least 75% of the total voting rights of eligible members must agree (s 283(2)). X’s 74% is below the 75% threshold, and Y’s non-response counts against the resolution. The SR will not pass unless at least one further vote is obtained to reach 75%.

Worked Example 1.5

Members holding 3,000 shares in a company with 100,000 issued ordinary shares instruct the board to call a GM to discuss concerns. Can they require the board to call the GM?

Answer:

No. Members must represent at least 5% of the issued voting rights to require the board to call a GM (s 303 CA 2006). 3,000 out of 100,000 is 3%. They do not meet the statutory threshold.

Record-Keeping and Filing Requirements

Minutes

Companies must keep minutes of all BMs and GMs (and records of WRs) for at least 10 years (s 248, s 355 CA 2006). These are usually kept at the registered office or SAIL address. Minutes serve both as evidence of decisions and as part of the company’s compliance framework. Companies may elect to keep certain statutory registers at Companies House’s central register, but minutes themselves remain internal records.

Filing Resolutions

Copies of all special resolutions must be filed with Companies House within 15 days of being passed (s 29, s 30 CA 2006). Certain ordinary resolutions also require filing, notably an OR under s 551 CA 2006 granting directors authority to allot shares, and resolutions approving buybacks or payments out of capital where filing obligations arise under the relevant provisions. Failure to file is a criminal offence committed by the company and every officer in default and may invalidate subsequent actions that depend on the filed resolution.

Additional filings may be required depending on the decision taken (for example, amending the articles or changing the company name). Companies must also maintain internal statutory registers (e.g. register of members, register of directors) and ensure any changes following member or board decisions are properly recorded and, where necessary, notified to the Registrar.

Exam Warning: Be careful to distinguish between the requirements for board meetings and general meetings. Notice periods, quorum rules, and voting thresholds differ significantly. Also, remember that written resolutions are only available to private companies and cannot be used for all types of decisions.

Practical pitfalls include miscalculating clear days when using postal or electronic service, omitting the exact wording of a special resolution in the notice, failing to inform members of their proxy rights, and overlooking special notice requirements for removing directors or auditors. Conflicts at board level under MA 14 can also invalidate decisions if quorum rules are not respected. When using written resolutions, remember that the majority is calculated on total eligible votes, so non-responses reduce the likelihood of passage.

Key Point Checklist

This article has covered the following key knowledge points:

- Decisions in a company are made by directors (at BMs) or shareholders (at GMs or by WRs).

- Directors manage the company's day-to-day business (MA 3) and may delegate (MA 5).

- BMs require reasonable notice and a quorum (usually two directors under MAs). Decisions are by majority vote; the chair may have a casting vote if provided (MA 13).

- Directors’ conflicts must be declared (ss 177, 182 CA 2006). Under MA 14, conflicted directors may be excluded from quorum and voting unless the articles disapply the restriction.

- Shareholders vote on significant matters via ordinary resolutions (ORs >50%) or special resolutions (SRs 75%+).

- GMs require 14 clear days' notice (longer for public AGMs), unless short notice is agreed (90%+ for private companies). Quorum is usually two qualifying persons (or one in a single-member company).

- Some resolutions require special notice (28 clear days), such as removal of directors or auditors.

- Voting at GMs is usually by show of hands unless a poll is demanded. On a poll, votes align with shareholdings.

- Private companies can use written resolutions (WRs) instead of GMs for most decisions, requiring the same majorities based on total eligible votes. WRs cannot be used to remove directors or auditors.

- Members holding at least 5% of voting rights can require the directors to call a GM (s 303), with statutory timelines for calling and holding the meeting (ss 304–305).

- Minutes of all meetings must be kept, and SRs (and some ORs) must be filed at Companies House within statutory deadlines.

- Unanimous shareholder assent (Duomatic principle) can validate decisions that could have been passed at a GM, provided all eligible members consent on a fully informed basis.

Key Terms and Concepts

- Quorum

- Ordinary Resolution

- Special Resolution

- General Meeting

- Clear Days

- Written Resolution

- Duomatic Principle

- Special Notice