Learning Outcomes

This article outlines statutory filing and disclosure duties under the Companies Act 2006 for private companies and unlisted public companies, including:

- Core statutory filing duties under the Companies Act 2006 for private companies and unlisted public companies

- Annual accounts requirements at a high level: contents, preparation, circulation and filing timing, and the effect of company size on content and audit requirements

- Deadlines for first accounts and subsequent financial years, and changes to the accounting reference date

- Purpose, timing and content of the annual confirmation statement, and its interaction with event‑driven updates and PSC information

- Key event‑driven filings, statutory time limits, and applicable forms (appointments/terminations of directors, changes of particulars, registered office moves, allotments of shares, creation of charges, changes to the articles or name)

- Statutory registers to be maintained, permitted locations (registered office or SAIL), and entries that may be kept on the central register at Companies House

- Practical aspects of the PSC regime: meaning of “significant control”, duty to investigate, register and filing time limits, and actions where PSC information is not provided

- Public nature of the Companies House register and the corporate governance rationale for disclosure

- Principal consequences of non‑compliance: civil penalties, criminal offences for officers in default, status of unregistered charges, and striking‑off

SQE1 Syllabus

For SQE1, you are required to understand statutory filing and disclosure requirements under the Companies Act 2006 for private companies and unlisted public companies, with a focus on the following syllabus points:

- Annual accounts and reports: preparation, circulation to members, filing deadlines (including “first accounts”), audit exemptions for small companies and micro‑entities, and content at a high level (directors’ report, strategic report for larger companies).

- The confirmation statement (CS01): purpose, review period, deadline, and core content (registered office, directors, statement of capital, SIC codes, shareholders, PSC).

- Event‑driven filings: what must be notified (directors/secretaries appointments/cessations and changes, registered office, allotments of shares, creation of charges, changes to articles/name, authority to allot/disapplication of pre‑emption), forms to use, and time limits.

- Statutory registers: register of members, directors, directors’ residential addresses, secretaries, PSC register; where to keep them (registered office or SAIL), inspection, and the option to use the central register.

- PSC regime: who is registrable (individual PSCs and relevant legal entities), the five statutory conditions for significant control, and steps to investigate and update.

- Companies House: the public nature of filed information and the policy rationale (transparency for creditors and members as the “price” of limited liability).

- Consequences of non‑compliance: escalating late‑filing penalties for accounts, criminal offences for failures to file or maintain registers, director disqualification risk, striking‑off, and the effect of non‑registration of charges within 21 days.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Within what period must a private company typically file its annual accounts with Companies House after its accounting reference date?

- a) 3 months

- b) 6 months

- c) 9 months

- d) 12 months

-

Which of the following events generally triggers an immediate filing requirement at Companies House (within 14 or 21 days)?

- a) Holding an annual general meeting.

- b) Appointing a new director.

- c) Declaring an interim dividend.

- d) Entering into a major commercial contract.

-

What is the primary purpose of the confirmation statement?

- a) To report the company's annual profits and losses.

- b) To confirm the accuracy of information held by Companies House about the company.

- c) To register new charges created by the company.

- d) To provide details of resolutions passed by the shareholders.

Introduction

Compliance with statutory filing and disclosure requirements is a basis of corporate governance for companies registered in England and Wales. The Companies Act 2006 (CA 2006) imposes various obligations on companies to file specific information and documentation with the Registrar of Companies at Companies House, and to maintain certain internal registers. These requirements ensure transparency and accountability, allowing shareholders, creditors, and the public access to key information about a company's management, control, and financial standing. Failure to comply can lead to penalties for the company and its officers. This article details the main statutory obligations regarding filing and disclosure.

Statutory filing and disclosure requirements for UK companies, including annual accounts, confirmation statements, event-driven filings, statutory registers, and consequences of non-compliance.

Key Term: Accounting Reference Date (ARD)

The date to which a company's annual accounts must be made up. Usually, this is the anniversary of the last day of the month in which the company was incorporated (s 391 CA 2006). Companies can change their ARD by filing the appropriate form. Key Term: Single Alternative Inspection Location (SAIL)

An address (within the same jurisdiction of incorporation) notified to Companies House where certain company records may be kept and inspected as an alternative to the registered office. Use form AD02 to notify a SAIL, AD03 to move records to the SAIL, and AD04 to move them back.Test Tip: In SQE-style questions on Statutory filing and disclosure requirements, identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

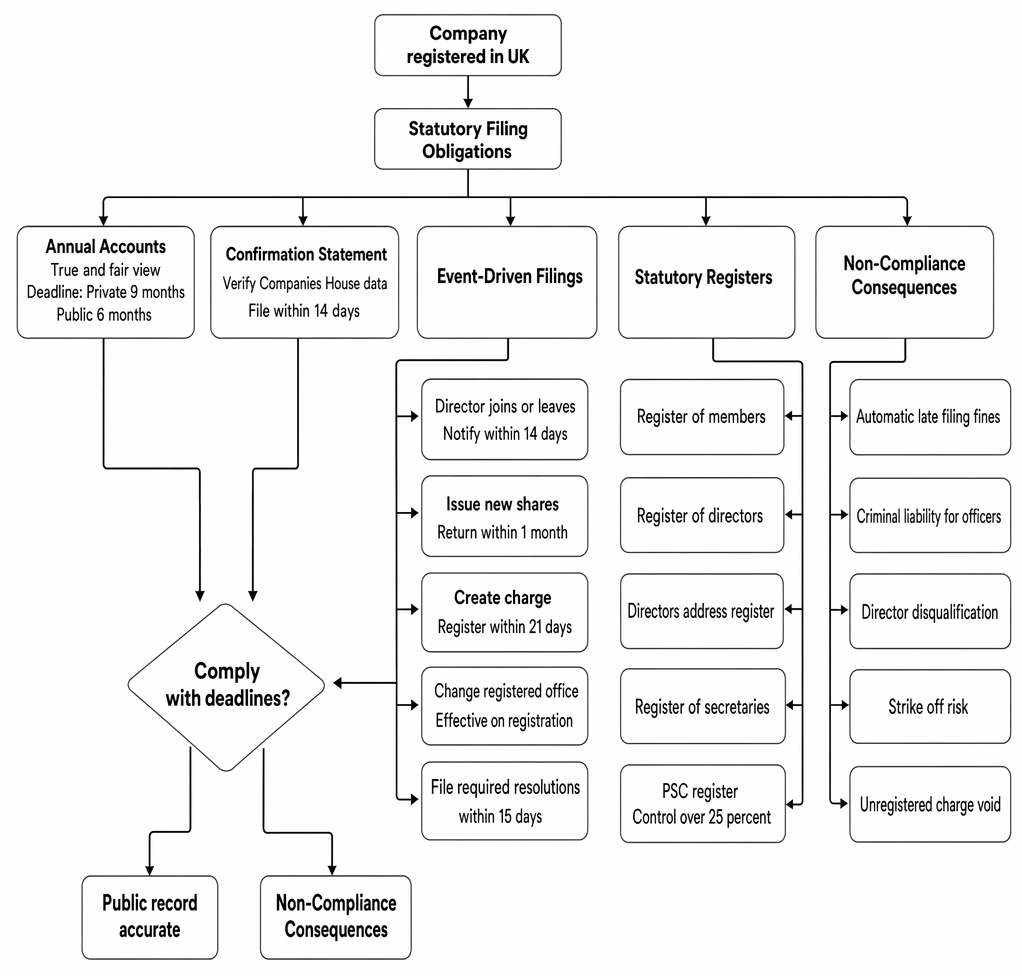

Statutory Filing Requirements

Companies must submit regular and event-driven filings to Companies House. These ensure the public record is accurate and up-to-date. The main filings include annual accounts and the confirmation statement.

Annual Accounts

Most companies are required to prepare and file annual accounts for each financial year (s 394 CA 2006). These accounts must provide a “true and fair view” of the company’s financial position and performance (s 393 CA 2006). Directors are responsible for ensuring adequate accounting records are kept (s 386) and for approving and signing the accounts (s 414), which must then be circulated to members and, where required, audited.

The accounts typically include:

- A balance sheet, signed on behalf of the board.

- A profit and loss account (income statement).

- Notes to the accounts (including a statement of capital and reserves).

- A directors’ report (s 415), unless the company qualifies as small or a micro‑entity.

- A strategic report for certain larger companies (s 414A), with non‑financial information for quoted and other qualifying companies.

- An auditor’s report where an audit is required.

Company size affects the extent of reporting and audit obligations:

- Small companies and micro‑entities may prepare simplified accounts and often claim exemption from audit if they meet the thresholds. As indicative thresholds: a small company generally does not exceed two of the following—turnover £10.2m; balance sheet total £5.1m; average employees 50. Micro‑entities are smaller again (e.g. turnover £632k; balance sheet total £316k; average employees 10). Check the current thresholds and associated accounting standards (e.g. FRS 102/105).

Deadlines for filing annual accounts are strict:

- Private companies: 9 months after the ARD (s 442 CA 2006).

- Public companies: 6 months after the ARD (s 442 CA 2006).

Special rule for first accounts: the filing deadline is 21 months from the date of incorporation for a private company (18 months for a public company), unless the ARD is changed. Directors can shorten the accounting reference period as often as they wish and can lengthen it once every five years (subject to exceptions), by filing form AA01.

Practical points frequently tested in scenarios:

- The accounts filing deadline differs from the deadline to circulate accounts to members; companies must circulate in good time for any general meeting or decision as required.

- Where an audit exemption is claimed, the balance sheet must include the required statutory statement acknowledging the exemption and stating that members have not required an audit.

Failure to file accounts on time results in automatic civil late-filing penalties for the company, which escalate with the length of delay and are doubled if accounts are late in two successive financial years. Persistent default can also lead to prosecution of officers in default and, ultimately, strike‑off action.

Confirmation Statement

Every company must deliver an annual confirmation statement to Companies House (s 853A CA 2006).

Key Term: Confirmation Statement

An annual filing confirming that the information Companies House holds about the company (e.g., registered office, directors, statement of capital, PSC information) is correct as at the confirmation date. Changes should be reported either before or at the same time as the confirmation statement. Key Term: Review Period (Confirmation Statement)

The 12‑month period for which a confirmation statement must be made. It begins on the date of incorporation or the day after the end of the previous review period. The statement must be filed within 14 days of the end of the review period.

The statement must be delivered at least once every 12 months. The due date is the end of each review period, and the filing window is 14 days thereafter. A fee is payable per 12‑month period (not per statement, if more than one statement is filed in the period).

Information covered or updated by the confirmation statement includes:

- Registered office address and SAIL (if used).

- Directors (and secretary, if any) and their service addresses.

- The company’s principal business activities (SIC codes).

- The statement of capital and prescribed shareholder information.

- PSC information—any changes should be notified as they occur and, in any event, must be up to date at the confirmation date.

Failure to file the confirmation statement is a criminal offence committed by the company and every officer in default. Persistent failure can lead to the company being struck off the register.

Event-Driven Filings

Beyond annual requirements, certain events trigger obligations to notify Companies House, typically within 14 or 21 days. This ensures the public register reflects significant changes promptly. Key examples include:

-

Change of Registered Office Address (s 87 CA 2006): Notify on form AD01. The change is only effective upon registration by Companies House.

-

Appointment/Termination of Directors or Secretaries (ss 167, 276 CA 2006):

- Appoint a director on form AP01 (AP02 for a corporate director, where permitted).

- Terminate a director on form TM01.

- Appoint a secretary on form AP03/AP04 (if the company has one).

- Terminate a secretary on form TM02.

- File changes in directors’ particulars (e.g., service address) on form CH01. These must be delivered within 14 days of the event.

-

Change of Directors’ Residential Addresses: The separate register of directors’ residential addresses must be kept and updated (s 165), but residential addresses are not generally public. Notify protected information as required.

-

Allotment of Shares (s 555 CA 2006): File a return of allotment (Form SH01), including an updated statement of capital, within one month of the allotment. Consider whether authority to allot (s 551) and pre‑emption rights (s 561) apply, and file any relevant resolutions within 15 days.

-

Creation of Charges (ss 859A–859Q CA 2006): Register most charges within 21 days beginning with the day after the charge is created, using form MR01 and a certified copy of the instrument. Failure renders the charge void against a liquidator, administrator and creditors (s 859H), and the secured sum becomes immediately payable.

-

Resolutions and Agreements (ss 29, 30 CA 2006): File copies of special resolutions and any other resolutions or agreements affecting the company’s constitution within 15 days. Common examples include:

- Special resolutions changing the articles (s 21) or changing the company name (ss 77–79; file NM01).

- Ordinary resolutions authorising directors to allot shares (s 551) and special resolutions disapplying pre‑emption rights (ss 569–571).

- Resolutions approving a substantial property transaction (s 190) or loans to directors (s 197) where required.

-

Change of Accounting Reference Date (s 392): File AA01 to shorten or lengthen the accounting reference period (subject to restrictions).

-

Single Alternative Inspection Location (SAIL): Notify the creation of a SAIL (AD02) and movement of company records (AD03/AD04).

Routine corporate actions do not always require filings. For example, share transfers do not trigger an immediate Companies House filing (they must be entered in the register of members, and changes will be reflected in the next confirmation statement through the statement of capital/shareholder information).

Worked Example 1.1

Tech Innovate Ltd, a private company incorporated on 10th March 2023, appoints a new director, Sarah, on 1st June 2024. The company secretary forgets to file the notification form until 20th June 2024. What is the consequence?

Answer:

The company and its officers (including the secretary and potentially the directors) have committed a criminal offence under s 167 CA 2006 because the notification (Form AP01) was not filed within 14 days of Sarah's appointment (i.e., by 15th June 2024). They could face fines.

Worked Example 1.2

Alpha Holdings Ltd has three shareholders: Shareholder A (30%), Shareholder B (30%), and Shareholder C (40%). All are individuals. Who should be listed on Alpha Holdings Ltd's PSC register?

Answer:

All three shareholders (A, B, and C) should be listed on the PSC register. Each holds more than 25% of the shares/voting rights, meeting one of the conditions for significant control under the CA 2006.

Worked Example 1.3

Beta Retail Ltd was incorporated on 5 January 2024 with an ARD of 31 January. When are its first accounts due at Companies House if it does not change its ARD?

Answer:

For a private company’s first accounts, the filing deadline is 21 months from incorporation. Beta Retail Ltd must file by 5 October 2025 (unless it changes its ARD). Thereafter, accounts are due 9 months after each ARD.

Worked Example 1.4

Gamma Engineering plc creates a debenture including a floating charge on Monday 1 July (executed that day). By when must the charge be registered and what is the effect if it is not?

Answer:

The charge must be registered within 21 days beginning with the day after creation—i.e., by Monday 22 July—using MR01 with a certified copy of the instrument. If not registered in time, the charge is void against an administrator, liquidator and creditors, and the secured amount becomes immediately payable.

Worked Example 1.5

Delta Foods Ltd passes a special resolution on 10 February to adopt bespoke articles. By when must the special resolution and new articles be filed?

Answer:

A copy of the special resolution and the amended articles must be filed at Companies House within 15 days of passing the resolution (ss 29–30 and s 26 CA 2006). Delta Foods Ltd must file by 25 February (allowing for “clear days” calculation does not apply here—use the statutory 15-day period).

Worked Example 1.6

Epsilon Services Ltd’s review period for the confirmation statement ends on 30 June. It filed its last statement on 15 July the previous year. By what date must it file its next confirmation statement?

Answer:

The confirmation statement must be delivered within 14 days after the end of the review period, i.e., by 14 July. The 12‑month review period runs to 30 June, and the company has until 14 July to file.

Statutory Registers

In addition to filings at Companies House, companies must maintain several statutory registers, keeping them updated and typically available for inspection at the registered office or a Single Alternative Inspection Location (SAIL). Alternatively, private companies can elect to keep certain information solely on the public register at Companies House.

Key Term: Statutory Registers

Internal records required by the CA 2006, detailing key aspects of the company's structure and governance, such as membership, directors, and charges.

Key registers include:

- Register of Members (s 113 CA 2006): The definitive record of who owns the company's shares. It should be updated promptly for allotments and transfers and is prima facie evidence of legal title.

- Register of Directors (s 162 CA 2006): Details of current directors; the company must also keep a separate register of directors’ residential addresses (s 165) which is not generally available for public inspection.

- Register of Secretaries (s 275 CA 2006): Required only if the company chooses to have a secretary.

- Register of People with Significant Control (PSC Register) (s 790M CA 2006): Records individuals or relevant legal entities (RLEs) who meet specific conditions relating to share ownership, voting rights, or influence over the company.

Companies may keep certain information on the central register at Companies House instead of maintaining their own register of directors, secretaries, and PSCs. Regardless of where records are kept, companies must ensure they are accurate and up to date and that inspection rights are respected.

Key Term: PSC Register

A register identifying individuals and relevant legal entities with significant control over the company, typically holding more than 25% of shares or voting rights, or the right to appoint/remove a majority of directors.

The five statutory PSC conditions cover:

- Ownership of more than 25% of shares.

- Control of more than 25% of voting rights.

- The right to appoint or remove a majority of the board.

- Significant influence or control over the company.

- Significant influence or control over a trust or firm (not a legal person) which itself satisfies one of the above conditions.

Companies must take reasonable steps to identify PSCs, serve notices if needed, record the required particulars, and keep the PSC register up to date. Time limits are tight: update the PSC register within 14 days of becoming aware of a change, then file the update at Companies House within a further 14 days. If a PSC (or registrable RLE) fails to respond to notices, the company can issue restrictions notices over the relevant shares pending compliance.

Failure to maintain these registers accurately is an offence.

Key Term: Statement of Capital

A snapshot of a company’s issued share capital, showing the total number of shares, aggregate nominal value, amounts paid and unpaid, and rights attached to each class. It accompanies allotment returns (SH01), the confirmation statement, and certain other filings.

Corporate Governance and Disclosure

Statutory filing and disclosure requirements are essential to the UK's corporate governance framework. They provide the baseline transparency upon which codes like the UK Corporate Governance Code (for premium listed companies) build. While the detailed requirements of the UK Corporate Governance Code are beyond the scope of this article's focus on statutory duties, it is important to recognise that public disclosures mandated by the CA 2006 (like accounts and director details) enable stakeholders to monitor the company's governance and performance.

Larger companies, particularly quoted companies, face additional statutory disclosure requirements, such as preparing a detailed Directors' Remuneration Report and a Strategic Report containing non-financial information (ss 414A, 420 CA 2006). These improve accountability and provide a fuller picture of the company's operations and strategy.

The UK Corporate Governance Code applies to companies with a premium listing and operates via principles that must be reported against, and provisions that operate on a comply‑or‑explain basis through the annual report. Large private companies may also report against the Wates Corporate Governance Principles, reflecting growing expectations of transparency even outside the listed sector. The Companies (Miscellaneous Reporting) Regulations 2018 require certain large private companies to include a statement of corporate governance arrangements within the directors’ report.

Key Term: Special Resolution

A shareholder resolution passed by a majority of not less than 75% of votes cast. It is required for certain fundamental changes such as amending the articles or changing the company’s name. A copy must be filed with Companies House within 15 days.

Consequences of Non-Compliance

Failure to comply with statutory filing and disclosure requirements can have serious consequences for both the company and its officers (directors and the secretary, if appointed).

- Financial Penalties: Late filing of annual accounts attracts automatic civil penalties from Companies House, which increase with the length of delay and are doubled for consecutive late filings.

- Criminal Offences: Many breaches (e.g., failure to file the confirmation statement, failure to maintain registers, failure to notify director changes) are criminal offences, potentially leading to fines for the company and its officers. Persistent non‑compliance can lead to prosecution of officers in default.

- Director Disqualification: Persistent breaches of filing requirements can lead to directors being disqualified under the Company Directors Disqualification Act 1986.

- Striking Off: Companies House may strike the company off the register for failure to file documents like the confirmation statement or accounts, leading to the company ceasing to exist and its assets passing to the Crown (bona vacantia).

- Loss of Validity of Security: Failure to register charges within 21 days makes the security void against insolvency practitioners and creditors. The secured debt becomes immediately payable.

- Reputational and Commercial Impact: Failure to maintain a compliant public record may affect credit ratings and counterparties’ willingness to do business.

Exam Warning: Compliance with filing deadlines is critical. SQE1 questions might test your ability to identify the correct deadline or the consequences of missing it. Remember that failure is often an offence committed by both the company and its officers.

Key Point Checklist

This article has covered the following key knowledge points:

- Companies must file annual accounts with Companies House, typically within 9 months (private) or 6 months (public) of the ARD; first accounts have extended deadlines (21 months private; 18 months public).

- Accounts must give a true and fair view and, dependent on size, include a directors’ report, strategic report (for larger companies), and an auditor’s report unless an exemption applies.

- The confirmation statement (CS01) must be filed at least once every 12 months, within 14 days of the end of the review period, confirming the company data on the public record.

- Event-driven filings include changes to directors and secretaries, registered office and SAIL, share allotments (SH01), creation of charges (MR01), and filing of resolutions and amendments to articles, usually within 14 or 21 days.

- The PSC regime requires companies to identify, record and file details of persons (or registrable relevant legal entities) with significant control and to keep the PSC register current within tight time limits.

- Companies must maintain statutory registers—members, directors, directors’ residential addresses, secretaries (if any), and PSC—kept at the registered office or SAIL, or on the central register where permitted.

- Failure to comply can result in civil penalties, criminal liability for officers, potential director disqualification, striking‑off, and (for charges) invalidity of the security against insolvency office‑holders and creditors.

- Special resolutions and other constitutional changes must be filed within 15 days; a change of company name takes effect only on issue of the new certificate of incorporation.

- A change of registered office is effective only upon registration by Companies House.

Key Terms and Concepts

- Accounting Reference Date (ARD)

- Single Alternative Inspection Location (SAIL)

- Confirmation Statement

- Review Period (Confirmation Statement)

- Statutory Registers

- PSC Register

- Statement of Capital

- Special Resolution