Learning Outcomes

This article examines the corporation tax and company law treatment of company distributions to shareholders, including:

- The corporation tax treatment of company distributions and the precise statutory terminology used to distinguish distributions from deductible business expenses, with emphasis on exam-standard wording.

- The classification of income distributions versus capital transactions, the availability of deductions and exemptions for corporation tax, and how these classifications feed through to shareholders’ income tax and CGT positions.

- The company law requirements for lawful distributions, including preparation and use of relevant accounts, identification of distributable reserves, and the consequences and potential remedies where an unlawful distribution is made.

- The detailed tax implications of dividends, share buybacks, and loans to shareholders (including section 455 loans), together with key anti-avoidance provisions such as “bed and breakfasting” on loans, commercial purpose tests on buybacks, and rules countering value extraction disguised as capital.

- SQE1-style scenario analysis of alternative distribution methods for both companies and different categories of shareholders, highlighting frequent exam traps, required computations, and the interaction between corporation tax, income tax, and capital gains tax in problem-style questions.

SQE1 Syllabus

For SQE1, you are required to understand the corporation tax and company law treatment of company distributions to shareholders, with a focus on the following syllabus points:

- The corporation tax consequences of paying dividends to shareholders, including the general dividend exemption for corporate recipients

- The legal and tax requirements for share buybacks (purchase of own shares) and redemptions, including classification of proceeds as income distributions or capital disposals

- The statutory conditions for capital treatment on a buyback (purchase of own shares relief) and the role of HMRC clearance

- The tax rules for loans to participators in close companies, including section 455 charge, repayment rules, and anti-avoidance

- The interaction between company law (Companies Act 2006) and tax law (CTA 2010/CTA 2009) in determining lawful and tax-efficient distributions

- Practical implications of distribution methods for companies and shareholders, including relevant accounts, distributable profits, stamp duty on buybacks, and benefit-in-kind rules for director loans

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

-

Which of the following is deductible for corporation tax purposes?

- a) Dividends paid to shareholders

- b) Salaries paid to employees

- c) Share buyback payments

- d) Section 455 tax charge

-

When can the proceeds of a share buyback be treated as a capital gain for the shareholder rather than as income?

- a) Always

- b) Only if the company is a close company

- c) Only if specific statutory conditions are met

- d) Never

-

What is the main purpose of the section 455 charge in relation to loans to shareholders?

- a) To provide a tax deduction for the company

- b) To prevent avoidance of income tax on distributions

- c) To encourage companies to pay more dividends

- d) To reduce the company’s corporation tax rate

Introduction

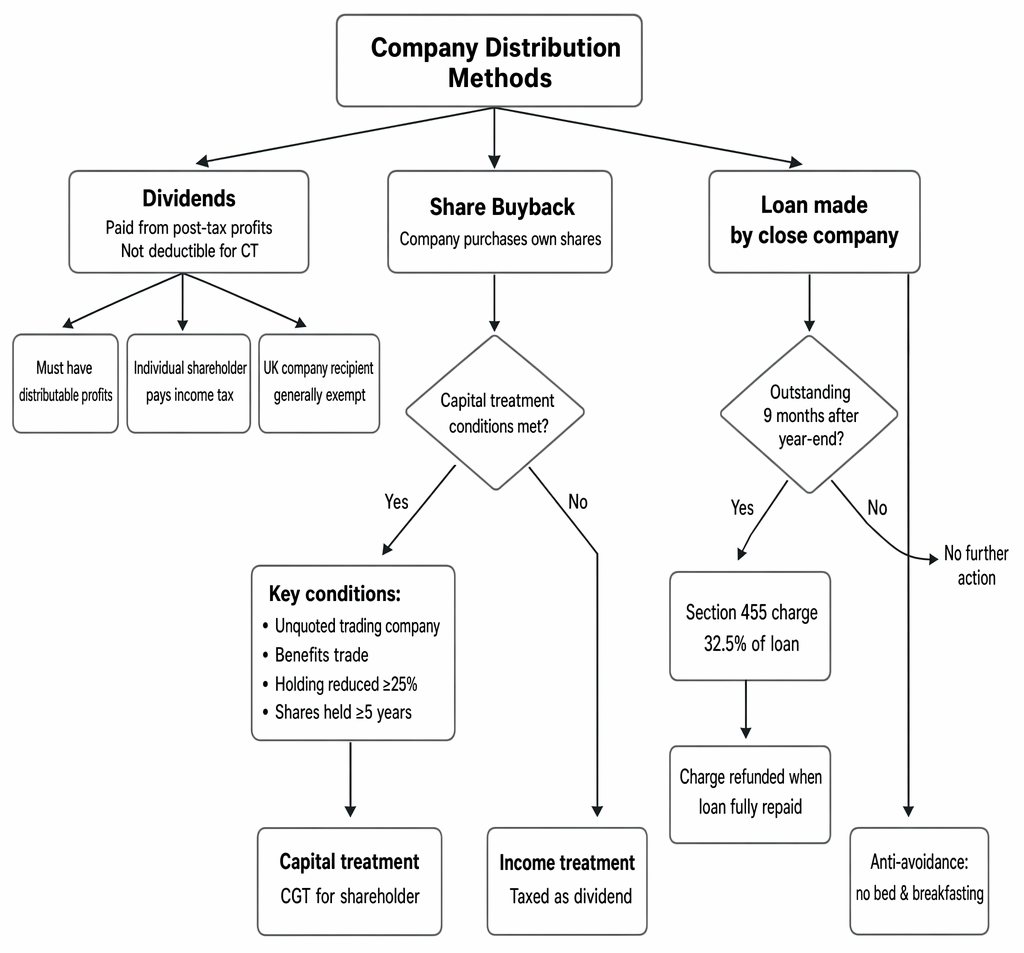

Company distributions are amounts a company returns to its members (shareholders) in their capacity as members. For corporation tax, a “distribution” is defined by statute and includes dividends and most other value transfers to shareholders (such as certain purchase-of-own-shares payments). The correct classification determines both the company’s corporation tax position and the shareholder’s income or capital tax consequences.

Dividends, share buybacks and close company loans to shareholders, including dividend, CGT and s 455 outcomes.

Key Term: distribution

A statutory concept covering value transferred by a company to shareholders in their capacity as members. It includes dividends and, in many cases, amounts paid on a purchase of own shares; it does not include normal commercial payments to suppliers or employees.

The three core routes are:

- Dividends (declared out of distributable profits)

- Share buybacks/redemptions (purchase/redeem own shares)

- Loans or advances to shareholders (participators) by close companies

Across all methods, account for the interaction with company law: a distribution is only lawful if permitted by the Companies Act 2006 and the company’s articles, and supported by “relevant accounts” evidencing sufficient distributable reserves. Tax anti-avoidance rules aim to prevent extraction of value in forms that sidestep income taxation.

Test Tip: In SQE-style questions on Tax treatment of company distributions to shareholders, identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

Exam Warning: Do not rely on a familiar phrase from Tax treatment of company distributions to shareholders alone; check whether the facts satisfy every condition, exception, and timing requirement.

Dividends: Corporation Tax and Legal Requirements

Dividends are the most common way for companies to return profits to shareholders. The tax and legal treatment of dividends is central to SQE1.

Key Term: dividend

A distribution of post-tax profits by a company to its shareholders, usually in cash, but sometimes in shares or other assets.

Dividends are paid out of profits after corporation tax. For corporation tax purposes, dividends are not deductible expenses. This means that paying a dividend does not reduce the company’s taxable profits. For company law, dividends can only be paid out of distributable profits and must be justified by “relevant accounts” (usually the latest annual accounts, or interim accounts prepared to the statutory standard). Directors must ensure the company has sufficient distributable profits before declaring a dividend; failure risks an unlawful distribution and potential personal liability.

Key Term: distributable profits

Profits available for distribution to shareholders, calculated under company law and accounting standards, evidenced by relevant accounts, and after corporation tax has been paid. Key Term: unlawful dividend

A dividend paid when the company does not have sufficient distributable profits or without relevant accounts, in breach of company law. Directors who authorised it may be liable, and shareholders may have to repay if they knew or had reasonable grounds to believe it was unlawful.

Legal mechanics:

- Final dividends are recommended by directors and approved by shareholders.

- Interim dividends may be declared solely by directors (subject to articles), provided relevant accounts show sufficient reserves.

- Dividend waivers must be properly documented and should not be used to create artificial income splits.

Dividends paid to individual shareholders are subject to income tax in the recipient’s hands, under the dividend rates and allowance applicable for the tax year. UK-resident corporate shareholders are generally exempt from corporation tax on dividends received from other companies due to the corporate dividend exemption regime (with limited exceptions). This prevents double taxation within corporate groups.

Key Term: relevant accounts

Accounts relied upon to demonstrate available distributable profits for a distribution under the Companies Act 2006. Typically the last annual accounts; for interim distributions, up-to-date interim accounts prepared to the necessary standard.

Worked Example 1.1

A company has post-tax profits of £100,000. It pays a dividend of £30,000 to its shareholders. Is the dividend deductible for corporation tax purposes?

Answer:

No. The dividend is paid out of post-tax profits and does not reduce the company’s taxable profits. It is not deductible for corporation tax.

Worked Example 1.2

Company A (UK-resident) receives a £200,000 dividend from its wholly-owned UK trading subsidiary. Is Company A generally subject to corporation tax on the dividend?

Answer:

Generally no. Most dividends received by UK-resident companies are exempt from corporation tax under the corporate dividend exemption regime. The exemption helps prevent double taxation of the same profits within a group.

Share Buybacks: Tax Classification and Conditions

A share buyback (purchase of own shares) occurs when a company purchases its own shares from shareholders. The tax treatment of the proceeds depends on whether the payment is classified as income (a distribution) or capital (a disposal for capital gains tax for individuals or chargeable gains for companies).

Key Term: share buyback

A transaction where a company purchases its own shares from shareholders, reducing the number of shares in issue. Often used to facilitate an exit of a shareholder or tidy up the capital structure.

By default, amounts paid by a company to purchase its own shares are treated as income distributions for the vendor shareholder. However, if specific statutory conditions are met, the proceeds may be treated as a capital gain for the shareholder (commonly referred to as “purchase of own shares relief”). Broadly, the key conditions include:

- The company must be an unquoted trading company (or the holding company of a trading group)

- The buyback must benefit the company’s trade (e.g. to remove a dissenting or retiring shareholder obstructing the business)

- The shareholder’s interest must be substantially reduced (usually at least a 25% reduction in their shareholding)

- The shareholder must have held the shares for at least five years (with some limited relaxations for shares acquired from a spouse/civil partner)

- The shareholder must not be “connected” with the company after the buyback (typically tested by reference to 30% thresholds)

- The transaction must be for genuine commercial reasons and not part of a tax avoidance scheme

When these conditions are satisfied, the payment is treated as capital proceeds, and the vendor may be liable to capital gains tax (CGT) rather than dividend income tax. The capital gain may, in appropriate cases, qualify for reliefs such as Business Asset Disposal Relief if the separate conditions for that relief are met.

Practical company law points:

- A buyback out of distributable profits requires an ordinary resolution approving the buyback contract (votes of the selling shareholder are ignored) and compliance with the statutory process.

- A buyback out of capital (private companies only) requires a directors’ solvency statement, an auditor’s report, a special resolution, and statutory publicity (Gazette notice and creditor notifications) with a waiting period to allow creditor applications.

- Stamp duty at 0.5% is generally payable by the company on the buyback consideration.

- Bought-back shares are usually cancelled and the company’s capital and reserves adjusted accordingly.

Key Term: purchase of own shares relief

The regime allowing capital treatment for payments on a purchase of own shares where statutory conditions are met (unquoted trading company, benefit of trade, significant reduction in holding, five-year ownership, not connected post-transaction, genuine commercial reasons).

Worked Example 1.3

A shareholder sells half of their shares back to the company. Their holding falls from 40% to 20%. The company is an unquoted trading company and the buyback is for the benefit of the trade. Will the proceeds be taxed as a capital gain or as income?

Answer:

The proceeds will be taxed as a capital gain, provided all other statutory conditions are met (including that the shareholder is not connected post-transaction and the five-year ownership test). The shareholder’s interest has been substantially reduced and the company is unquoted and trading.

Worked Example 1.4

A founder has held shares for 10 years in an unquoted trading company. The company buys back enough shares to reduce the founder’s stake from 35% to 12%. The purpose is to remove shareholder deadlock and improve access to bank finance. Post-buyback, the founder has under 30% of votes. How is the payment treated for tax?

Answer:

On these facts, capital treatment is likely to apply. The company is an unquoted trading company; the buyback benefits the trade; the founder’s shareholding has been substantially reduced; the five-year holding condition is met; and the founder is not connected post-buyback (below 30%). The gain will be subject to CGT, with potential further reliefs if their separate conditions are satisfied. If capital treatment is not available (e.g. insufficient reduction in interest, continued connection post-buyback, or no genuine trade benefit), the payment is treated as an income distribution and taxed as a dividend in the shareholder’s hands.

From a corporation tax standpoint, buyback payments are not deductible by the company. The accounting entry reduces reserves and share capital as prescribed; tax follows the distribution classification without creating a corporation tax deduction.

Loans to Shareholders: Section 455 Charge

Loans to shareholders (or their associates) by close companies are subject to special anti-avoidance rules. The main rule is the section 455 charge.

Key Term: close company

A company controlled by five or fewer shareholders (participators), or by any number of directors who are also shareholders. Many owner-managed companies are close companies. Key Term: section 455 charge

A corporation tax charge on loans made by a close company to a participator (shareholder) or their associate, calculated at 33.75% of the loan amount remaining outstanding nine months after the end of the accounting period. The charge is repayable when the loan is repaid, written off and taxed appropriately, or released.

The section 455 charge is designed to prevent shareholders from extracting value from the company by way of loans instead of dividends. Key practical points:

- Timing: If the loan remains outstanding nine months after the end of the accounting period, the section 455 charge is due at 33.75% of the outstanding amount (aligned to the higher dividend rate).

- Repayment credit: When the loan is repaid, written off (and appropriately taxed as a distribution), or released, the company can claim a repayment of the section 455 tax.

- Anti-avoidance: “Bed and breakfasting” rules prevent repaying a loan shortly before the nine-month date and re-borrowing soon after to avoid the charge; broadly, repayments followed by new loans within 30 days can be matched to negate the avoidance.

- Benefit-in-kind: Where the borrower is also a director/employee, interest-free or low-interest loans can create a taxable employment benefit if above the statutory thresholds.

- Write-offs: If a shareholder loan is written off, the amount is usually taxed as a distribution (dividend) in the shareholder’s hands rather than employment income.

Worked Example 1.5

A close company lends £40,000 to a shareholder. The loan is still outstanding nine months after the end of the accounting period. What is the section 455 charge?

Answer:

The company must pay a section 455 charge of £13,500 (33.75% of £40,000). If the loan is repaid later, the company can claim a refund of the section 455 tax.

Worked Example 1.6

A shareholder repays a £50,000 loan on 25 March. On 10 April, the company makes a new £48,000 loan to the same shareholder. The year-end is 31 December. How do anti-avoidance rules affect the section 455 position?

Answer:

The short repayment followed by a near-equivalent loan within 30 days can be matched (anti-“bed and breakfasting”). The repayment will be set against the later loan, limiting the extent to which the original loan is treated as cleared. If the net amount remains outstanding nine months after year-end, section 455 will apply to that amount.

Comparing Distribution Methods

Companies may choose between dividends, share buybacks, or loans to shareholders. Each method has different tax and legal consequences, and each has specific procedural requirements.

- Dividends: Not deductible for corporation tax; income tax charged on recipients; most dividends received by corporate shareholders are exempt from corporation tax. Must be supported by relevant accounts showing distributable profits.

- Share buyback: If capital conditions are met, vendor shareholder pays CGT on the gain; otherwise taxed as dividend income. The company cannot deduct the payment for corporation tax; stamp duty at 0.5% may apply. Company law requires ordinary resolution approving the contract; capital buybacks need solvency statement, auditor’s report, special resolution, and statutory publicity.

- Loans to shareholders: If a close company lends and the loan remains outstanding nine months after year-end, section 455 applies at 33.75%. Repayment generates a tax credit back to the company. If written off, the amount is usually taxed on the shareholder as a dividend. Benefit-in-kind charges can arise for director/employees on cheap loans.

Worked Example 1.7

A company has £50,000 of surplus cash. It can pay a dividend, buy back shares, or lend the money to its sole shareholder. What are the main tax consequences of each option?

Answer:

- Dividend: Not deductible for corporation tax; shareholder pays income tax on the dividend; lawful only if supported by relevant accounts and distributable reserves.

- Share buyback: If capital conditions are met, shareholder pays CGT; if not, taxed as a dividend. Company pays stamp duty on the buyback and cannot deduct the payment for corporation tax. Company law process must be followed.

- Loan: Section 455 charge at 33.75% applies if not repaid within nine months of year-end; no immediate income tax for the shareholder, but benefit-in-kind rules may apply if they are also a director/employee. Write-off typically taxed as a dividend on the shareholder.

Worked Example 1.6 (additional company law context)

A private company wants to buy back shares out of capital to facilitate a retiring shareholder’s exit. There are insufficient distributable reserves. What steps must it take?

Answer:

The company must follow the capital buyback process: directors’ solvency statement; auditor’s report; special resolution approving the payment out of capital within seven days of the solvency statement; statutory publicity (Gazette notice and either creditor notification or national newspaper notice); and a minimum waiting period (5–7 weeks) to allow creditor applications before completing the buyback.

Key Point Checklist

This article has covered the following key knowledge points:

- Dividends are paid from post-tax profits and are not deductible for corporation tax; corporate recipients are generally exempt from corporation tax on dividends received.

- Dividends must be paid out of distributable profits and supported by relevant accounts; unlawful dividends can result in director liability and shareholder repayment in some circumstances.

- Purchase of own shares payments are usually income distributions unless statutory conditions for capital treatment are met; capital treatment requires genuine trade benefit, substantial reduction in interest, five-year ownership, and non-connection post-buyback.

- Buybacks require strict Companies Act procedures; capital buybacks need solvency statements, auditor reports, special resolutions, and statutory publicity; stamp duty at 0.5% commonly applies.

- Loans to participators in close companies trigger the section 455 charge at 33.75% if not repaid within nine months after the period end; repayment generates a refund; anti-“bed and breakfasting” rules apply.

- Writing off shareholder loans is generally taxed as a dividend in the shareholder’s hands; cheap or interest-free director loans can create employment benefit-in-kind charges.

- Choice of distribution method affects both the company’s corporation tax position (usually no deduction) and the shareholder’s personal tax (income vs capital), and must align with company law and anti-avoidance constraints.

Key Terms and Concepts

- distribution

- dividend

- distributable profits

- relevant accounts

- unlawful dividend

- share buyback

- purchase of own shares relief

- close company

- section 455 charge