Learning Outcomes

This article outlines UK income tax calculation and collection, including:

- Chargeable persons for UK income tax and distinction from entities liable to corporation tax

- Classification of total income into non-savings, savings, and dividend components, and the correct order of taxation

- Step-by-step computation under ITA 2007 s 23, including sequencing of reliefs, personal allowance, and rate bands

- Adjusted net income, tapering of the personal allowance for high earners, and effects of pension contributions and Gift Aid on bands and allowances

- Starting rate for savings, personal savings allowance, and treatment of the dividend allowance as 0% rate bands

- Interaction of multiple 0% rates and resulting marginal rate effects (including the 60% effective rate in the taper zone)

- Collection mechanisms (PAYE and self-assessment), payments on account, and balancing payments

- High Income Child Benefit Charge and its incorporation in the final liability

- Taxation of partnerships and basics of trust income taxation and its intersection with inheritance tax

- GAAR and targeted anti-avoidance measures, and distinction between legitimate planning and abusive arrangements

SQE1 Syllabus

For SQE1, you are required to understand UK income tax calculation and collection, with a focus on the following syllabus points:

- identifying who is liable to pay income tax and the relevant taxable entities

- distinguishing between non-savings, savings, and dividend income

- applying the correct steps to calculate income tax liability, including allowances, reliefs, and 0% rate bands

- understanding the main methods of income tax collection (PAYE and self-assessment), including payments on account

- recognising the operation of anti-avoidance rules (including GAAR and the Ramsay approach)

- outlining the taxation of trusts and the interaction with inheritance tax

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What are the three main categories of income for UK income tax purposes, and how are they taxed?

- How is the personal allowance applied when calculating an individual's income tax liability?

- What is the General Anti-Abuse Rule (GAAR) and when does it apply?

- Who is responsible for paying income tax on partnership profits?

- How does the UK tax system collect income tax from employees compared to self-employed individuals?

Introduction

Income tax is a central part of the UK tax system and a key topic for SQE1. It is charged on the income of individuals, partners, trustees, and certain other entities. Understanding how to identify taxable income, apply allowances and reliefs, and calculate the correct tax due is essential for advising clients and answering SQE1 questions. While the framework is stable, rates and bands are set for each tax year; always check current figures. From 2024/25, for example, the dividend allowance is £500, and the High Income Child Benefit Charge threshold increased (see below).

Key Term: income tax

A tax charged on the income of individuals, partners, trustees, and certain other entities, according to UK law.Test Tip: In SQE-style questions on Calculation and collection of tax, identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

Who Pays Income Tax?

Income tax is charged on the income of:

- individuals (including employees, sole traders, and partners)

- trustees (on trust income)

- personal representatives (on estate income during administration)

Key Term: partnership

An unincorporated business in which two or more persons carry on a business in common with a view to profit. For income tax, each partner is assessed on their share of the partnership profits.

Companies do not pay income tax; instead, they pay corporation tax on their profits. Scottish taxpayers face devolved rates for non-savings, non-dividend income only; savings and dividend income remain subject to UK-wide rates.

Types of Taxable Income

Income tax applies to several categories of income. For calculation purposes, these are separated into:

- Non-savings, non-dividend income (NSNDI): e.g. employment income (including benefits), self-employment profits, rental income, most pensions.

- Savings income: e.g. bank and building society interest, certain bonds.

- Dividend income: e.g. dividends from UK and overseas companies.

Key Term: non-savings, non-dividend income (NSNDI)

Income from employment, self-employment, property, and most pensions, excluding savings and dividend income. Key Term: savings income

Income from interest on bank accounts, savings bonds, and similar sources. Key Term: dividend income

Income received as dividends from shares in companies.

Steps in Calculating Income Tax

Calculating income tax liability involves a series of steps. Each must be applied in the correct order. The statutory framework is ITA 2007 s 23.

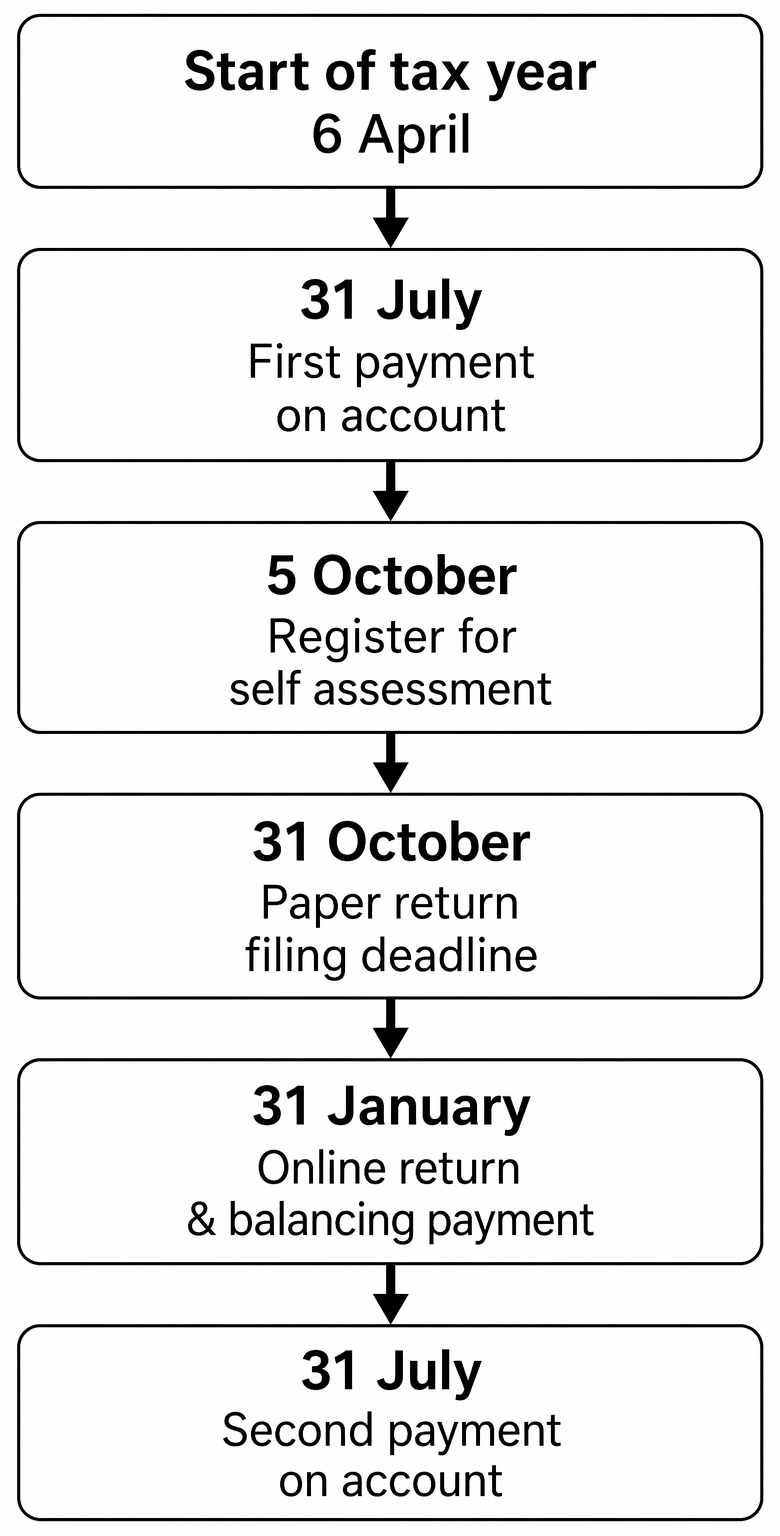

Principal dates in the UK self assessment timetable for income tax, including registration, return filing, balancing payment, and payments on account.

Step 1: Identify Total Income

Add together all sources of income for the tax year (6 April to 5 April), identifying the components: NSNDI, savings, and dividends. Keep components separate as different rules and rates apply to each.

Typical items include:

- NSNDI: salary and benefits, self-employment profits, property income, state and private pensions

- Savings: bank interest (usually paid gross), government and corporate bond interest

- Dividends: distributions from UK and overseas companies (no tax credits since 2016/17)

Step 2: Deduct Allowable Reliefs

Certain reliefs may be deducted from total income before allowances are applied (so-called “reliefs above the line” under s 24 ITA 2007). These reduce “total income” to “net income”.

Common examples include:

- Grossed-up pension contributions under relief-at-source schemes (basic rate added by provider; higher/additional rate claimed via self-assessment)

- Gift Aid donations (grossed up; extend basic and higher rate limits and reduce adjusted net income)

- Qualifying loan interest (e.g. to buy shares in a close company or to invest in a partnership)

- Trade losses and certain property losses (subject to the statutory regime)

Key Term: allowable relief

A deduction permitted by law from total income before calculating taxable income.

Step 3: Deduct Personal Allowance

Every individual is entitled to a personal allowance (currently £12,570), reducing the amount of income subject to tax. The allowance is reduced by £1 for every £2 of adjusted net income above £100,000 and is fully withdrawn once adjusted net income reaches £125,140.

Key Term: personal allowance

The amount of income an individual can receive each tax year before paying income tax. Key Term: adjusted net income

Broadly total income less certain deductions (notably grossed-up Gift Aid and pension contributions, and trade losses). It determines the tapering of the personal allowance and the High Income Child Benefit Charge.

Personal allowance is set against income in the following order:

- first against NSNDI

- then savings income

- then dividend income

Correct ordering matters for the availability of the starting rate for savings and the personal savings allowance.

Step 4: Apply Tax Rates to Each Income Type

Taxable income is divided into NSNDI, savings, and dividend income. Each is taxed at different rates and in a specific order:

- NSNDI is taxed first, using the basic, higher and additional rate bands.

- Savings income is taxed next, with possible application of the starting rate for savings and the personal savings allowance.

- Dividend income is taxed last, with a dividend allowance applied as a 0% rate band.

Key Term: starting rate for savings

A 0% rate on up to £5,000 of savings income, available only where taxable NSNDI (after personal allowance) does not fully use this band. It tapers away £1 for every £1 of NSNDI above the personal allowance. Key Term: personal savings allowance

An amount of savings income taxed at 0% (£1,000 for basic rate, £500 for higher rate, none for additional rate taxpayers). Key Term: dividend allowance

An amount of dividend income taxed at 0% (£1,000 for 2023/24; £500 for 2024/25). It does not reduce taxable income but uses up rate band.

The main UK-wide income tax rates for 2024/25 (non-savings, non-dividend and savings) are:

- Basic rate (20%): up to £37,700 of taxable income (after personal allowance)

- Higher rate (40%): £37,701 to £125,140

- Additional rate (45%): over £125,140

Dividend income is taxed at 8.75% (basic), 33.75% (higher), and 39.35% (additional) after applying the dividend allowance at 0%. Scottish taxpayers have different NSNDI rates but the UK-wide savings and dividend regimes still apply.

Ordering of savings reliefs within Step 4:

- Apply the starting rate for savings first (if available)

- Then apply the personal savings allowance

- Any remaining savings income is taxed at the appropriate marginal rates

Ordering for dividends:

- Apply the dividend allowance (0% band), then

- Tax any remaining dividends at dividend rates within the relevant remaining bands

Step 5: Calculate Total Tax Due

Add together the tax due on each slice of income to find the total income tax liability, before any reductions or additional charges.

Step 6: Deduct Any Tax Reductions

Apply any reductions against the computed tax (ITTOIA/ITA provisions), such as:

- Marriage allowance (transferrable 10% of personal allowance from a non-taxpayer to a basic rate spouse/civil partner)

- Relief for venture capital schemes

- Certain pension scheme charges/reliefs and social investment tax relief

- Top-slicing relief (for chargeable event gains; outside core scope here)

Step 7: Add Any Additional Charges

Add charges such as the High Income Child Benefit Charge (HICBC) or pension annual allowance charges. From 2024/25, HICBC applies if your adjusted net income exceeds £60,000; it is 1% of the child benefit received for every £200 of adjusted net income between £60,000 and £80,000 (fully extinguishing at £80,000).

The result after Steps 1–7 is the taxpayer’s liability to income tax for the tax year.

Worked Example 1.1

Question: Jamie has employment income of £35,000, bank interest of £1,200, and dividend income of £2,500. Jamie makes a pension contribution of £2,000. What is Jamie's income tax liability for 2023/24?

Answer:

- Total income: £35,000 + £1,200 + £2,500 = £38,700

- Deduct reliefs: gross pension (relief at source) £2,000 extends bands and reduces adjusted net income. Net income becomes £36,700.

- Deduct personal allowance: £36,700 - £12,570 = £24,130

- NSNDI taxed first: £24,130 at 20% = £4,826 Savings: £1,200 – personal savings allowance (basic rate: £1,000 at 0%), remaining £200 at 20% = £40 Dividends: £2,500 – dividend allowance (£1,000 at 0%) leaves £1,500 at 8.75% = £131.25

- Total tax: £4,826 + £40 + £131.25 = £4,997.25

Note: For 2024/25 the dividend allowance is £500, increasing the dividend tax in otherwise similar facts.

Worked Example 1.2

Question: Priya has taxable NSNDI of £2,000 after personal allowance, savings interest of £4,000, and no dividends. Calculate tax on the savings assuming 2024/25 rates.

Answer:

- Starting rate for savings: maximum £5,000 less NSNDI after personal allowance (£2,000) = £3,000 at 0%

- Personal savings allowance (basic rate): £1,000 at 0%

- Savings interest £4,000: first £3,000 at 0% (starting rate); next £1,000 at 0% (PSA); no savings taxed.

- Total tax on savings: £0

Worked Example 1.3

Question: Alex has employment income £120,000 (no other income). Alex makes a gross personal pension contribution of £10,000 and Gift Aid donations of £2,000 (gross) in 2024/25. Compute whether the personal allowance is tapered and the impact on tax.

Answer:

- Adjusted net income starts at £120,000. Deduct grossed-up pension (£10,000) and gross Gift Aid (£2,000) = £108,000.

- Personal allowance taper applies only above £100,000. Excess = £8,000 → taper = £4,000.

- Personal allowance = £12,570 – £4,000 = £8,570 (not fully withdrawn because reliefs reduced adjusted net income).

- The pension and Gift Aid also extend the basic rate band by their gross amounts, pushing less income into higher rates.

- Result: significant reduction in the effective marginal rate compared to no reliefs, and partial restoration of the personal allowance.

Worked Example 1.4

Question: Lee’s adjusted net income is £70,000 in 2024/25. Lee and partner received child benefit of £2,212 for the year. Compute the High Income Child Benefit Charge (HICBC).

Answer:

- Threshold: £60,000. Excess = £10,000.

- HICBC = 1% of child benefit for each £200 of excess. £10,000/£200 = 50%.

- Charge = 50% × £2,212 = £1,106.

- Add £1,106 to the income tax computation at Step 7.

Methods of Tax Collection

Income tax is collected in different ways depending on the taxpayer's circumstances.

Pay-As-You-Earn (PAYE)

Employees have income tax deducted from their salary by their employer before payment. National Insurance contributions are also collected via payroll. HMRC issues tax codes to employers that reflect an employee’s allowances and adjustments (e.g. benefits-in-kind). End-of-year and leaver forms (e.g. P60, P45) summarise pay and tax deducted; benefits may be reported and processed through payroll or by forms such as P11D.

Key Term: PAYE

The system by which employers deduct income tax and National Insurance from employees' pay and send it directly to HMRC.

Key practical points:

- changes to circumstances (new job, benefits, etc.) can trigger a code change within the year

- underpayments/overpayments are often reconciled through coding or self-assessment responses

Self-Assessment

Self-employed individuals, partners, landlords, and others with untaxed income must complete a self-assessment tax return and pay tax directly to HMRC. Returns are normally filed online by 31 January following the tax year. Payment is usually in two payments on account and a balancing payment.

Key Term: self-assessment

The process by which individuals report income and pay tax directly to HMRC, typically used by the self-employed and those with complex tax affairs.

Payments timetable:

- First payment on account: 31 January in the tax year

- Second payment on account: 31 July following the tax year

- Balancing payment (and any HICBC etc.): 31 January following the tax year

Payments on account are each typically half of the prior year’s income tax (excluding certain items like capital gains). They are not required if the prior year’s liability was small (broadly under £1,000) or most tax was already collected at source (generally ≥80%).

Taxation of Partnerships

Partnerships are not separate taxable entities. Each partner is taxed individually on their share of the partnership profits.

From 2024/25, unincorporated businesses use a tax-year basis of assessment; partnership profits are apportioned by reference to the tax year. Partners include their share of profits on their own returns and pay any tax due via PAYE (if they have employment income) or self-assessment.

Taxation of Trusts

Trusts are taxed as separate entities for income tax, often at higher rates. The type of trust determines the rates and allowances:

- Interest in possession (IIP) trusts: generally, the income is treated as belonging to the life tenant and taxed accordingly. In practice, trustees may account for basic rate on some income, with the beneficiary receiving credit.

- Discretionary trusts: trustees pay the “rate applicable to trusts” on most income at 45% (and 39.35% for dividends) after a small standard rate band (usually up to £1,000, split between trusts created by the same settlor). Income distributions carry a tax credit reflecting the tax paid by trustees.

Key Term: trust

A legal arrangement where trustees hold assets for the benefit of beneficiaries, with specific tax rules applying to trust income.

Worked Example 1.5

Question: A partnership earns £60,000 profit. There are two equal partners. How is income tax paid?

Answer:

Each partner is taxed on £30,000 as part of their personal income. Each calculates their own tax liability, applying their personal allowance and tax rates, and pays any tax due through self-assessment (subject to PAYE on any employment income they may also have).

Anti-Avoidance Rules

The UK tax system includes measures to prevent tax avoidance.

General Anti-Abuse Rule (GAAR)

The GAAR targets arrangements that are abusive and seek to exploit loopholes in tax law. It applies across the main direct taxes (including income tax, capital gains tax, and corporation tax) and stamp taxes. HMRC can counteract the tax advantage on a just and reasonable basis. The GAAR Advisory Panel may opine on whether arrangements are “double-reasonably” viewed as a reasonable course of action.

Key Term: General Anti-Abuse Rule (GAAR)

A statutory rule allowing HMRC to counteract tax advantages from arrangements deemed abusive of tax legislation.

Ramsay Approach and Specific Anti-Avoidance Provisions

Courts adopt a purposive approach to tax legislation and consider the overall effect of composite transactions (the Ramsay principle). Alongside GAAR, there are targeted rules to prevent known avoidance, such as:

- disguised remuneration (including “loan charge” rules for certain historic schemes)

- settlements legislation (attributing income of some “arrangements” back to the settlor)

- transfer of assets abroad provisions

- targeted anti-avoidance in loss relief and property businesses

Exam Warning: For SQE1, be able to distinguish between legitimate tax planning (e.g. pensions and Gift Aid) and arrangements that may be challenged under GAAR or specific anti-avoidance rules.

Trusts and Inheritance Tax

Trusts are subject to special income tax rules and may also trigger inheritance tax (IHT) charges.

- Interest in possession trusts: Income is taxed on the beneficiary (life tenant), often with tax accounted for by trustees on some sources.

- Discretionary trusts: Trustees pay income tax at the trust rates (currently 45% on most income; 39.35% on dividends) after a small standard rate band.

- IHT: Transfers into many trusts (relevant property trusts) can be immediately chargeable to IHT at lifetime rates, and periodic (ten-year) and exit charges may apply. Transfers to IIP trusts for spouses and certain disabled trusts may be treated differently.

Key Term: inheritance tax (IHT)

A tax on the transfer of assets on death or certain transfers into trusts, subject to exemptions and thresholds.

Additional Practical Points and Marginal Effects

- The personal allowance taper creates an effective marginal rate of 60% on NSNDI in the band £100,000–£125,140 (before considering savings/dividends). Pension contributions and Gift Aid reduce adjusted net income and can restore personal allowance and extend basic rate band.

- Starting rate for savings is only available if NSNDI (after personal allowance) is low enough.

- The dividend allowance and personal savings allowance are 0% rate bands that still use up the basic/higher rate bands.

- For Scottish taxpayers, NSNDI rates and bands differ; however, the UK-wide savings and dividend regimes and allowances apply uniformly, and personal allowance is UK-wide.

Key Point Checklist

This article has covered the following key knowledge points:

- Income tax is charged on the income of individuals, partners, and trustees, but not companies.

- Taxable income is divided into non-savings, savings, and dividend income; the order of taxation is NSNDI, then savings, then dividends.

- Reliefs under ITA 2007 s 24 are deducted before allowances; personal allowance is then set off in the order NSNDI, savings, dividends.

- The personal allowance is reduced by £1 for every £2 of adjusted net income over £100,000.

- The starting rate for savings (0% up to £5,000) applies only where NSNDI after personal allowance is low; then apply the personal savings allowance.

- Dividend income benefits from a 0% dividend allowance (2024/25: £500), after which dividend rates apply.

- HICBC applies from adjusted net income above £60,000 (2024/25), tapering to £80,000.

- Income tax is collected via PAYE for employees and via self-assessment for those with untaxed income; payments on account may be required.

- Partnerships are transparent for tax; each partner is taxed on their share. From 2024/25, a tax-year basis applies to unincorporated businesses.

- Trusts are taxed at beneficiary or trustee level depending on type; discretionary trusts pay at the trust rates, and IHT periodic/exit charges may apply.

- Anti-avoidance rules, including GAAR and targeted provisions, counteract abusive arrangements.

Key Terms and Concepts

- income tax

- partnership

- non-savings, non-dividend income (NSNDI)

- savings income

- dividend income

- allowable relief

- personal allowance

- adjusted net income

- starting rate for savings

- personal savings allowance

- dividend allowance

- PAYE

- self-assessment

- trust

- General Anti-Abuse Rule (GAAR)

- inheritance tax (IHT)