Learning Outcomes

This article outlines the principal categories of income subject to UK income tax and explains how each category is assessed in the context of the SQE1 FLK1 examination. It expands the rules for employment income (including PAYE operation, common taxable benefits and the strict test for allowable deductions), trading income (allowable expenses, capital allowances and the tax-year basis of assessment), property income (identifying allowable expenditure, the finance cost relief restriction, replacement of domestic items relief, rent-a-room relief and the property allowance), savings income (ordering rules, Personal Savings Allowance and the starting rate for savings), dividend income (application of the Dividend Allowance, dividend rate bands and dividends as the top slice of income), and foreign income (residence and domicile, arising vs remittance basis and double tax relief). It also illustrates how to combine these income sources to compute taxable income, apply personal allowances and rate bands, and identify when 0% savings and dividend bands are available. Worked examples reinforce calculation technique and highlight common exam traps, such as mixed sources of savings income, interactions between finance cost relief and other allowances, and the treatment of foreign tax credits.

SQE1 Syllabus

For SQE1, you are required to understand the main categories of income subject to UK income tax and how they are calculated and assessed, with a focus on the following syllabus points:

- The main categories of income subject to UK income tax: employment, trading, property, savings and dividend income; foreign income overview.

- Employment income calculation, PAYE, taxable benefits in kind, and the strict test for allowable deductions.

- Trading income principles: identifying a trade using the Badges of Trade, allowable expenses, and capital allowances (AIA/WDA).

- Basis of assessment for unincorporated trading businesses on the tax-year basis, including overlap profits and transitional rules.

- Property income computation, including repairs vs improvements, replacement of domestic items relief, finance cost relief restriction and the property allowance.

- Savings income ordering rules, the Personal Savings Allowance (PSA) and the starting rate for savings.

- Dividend income ordering rules, the Dividend Allowance and rate bands; dividends as the top slice of income.

- Foreign income: residence/domicile, arising vs remittance basis, and double taxation relief.

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- Which system is typically used to deduct income tax from employment income?

- What are the "Badges of Trade" used for?

- True or false? Mortgage interest paid by a landlord on a residential letting property is fully deductible against rental income when calculating taxable profit.

- What is the standard Personal Allowance for income tax in the current tax year?

Introduction

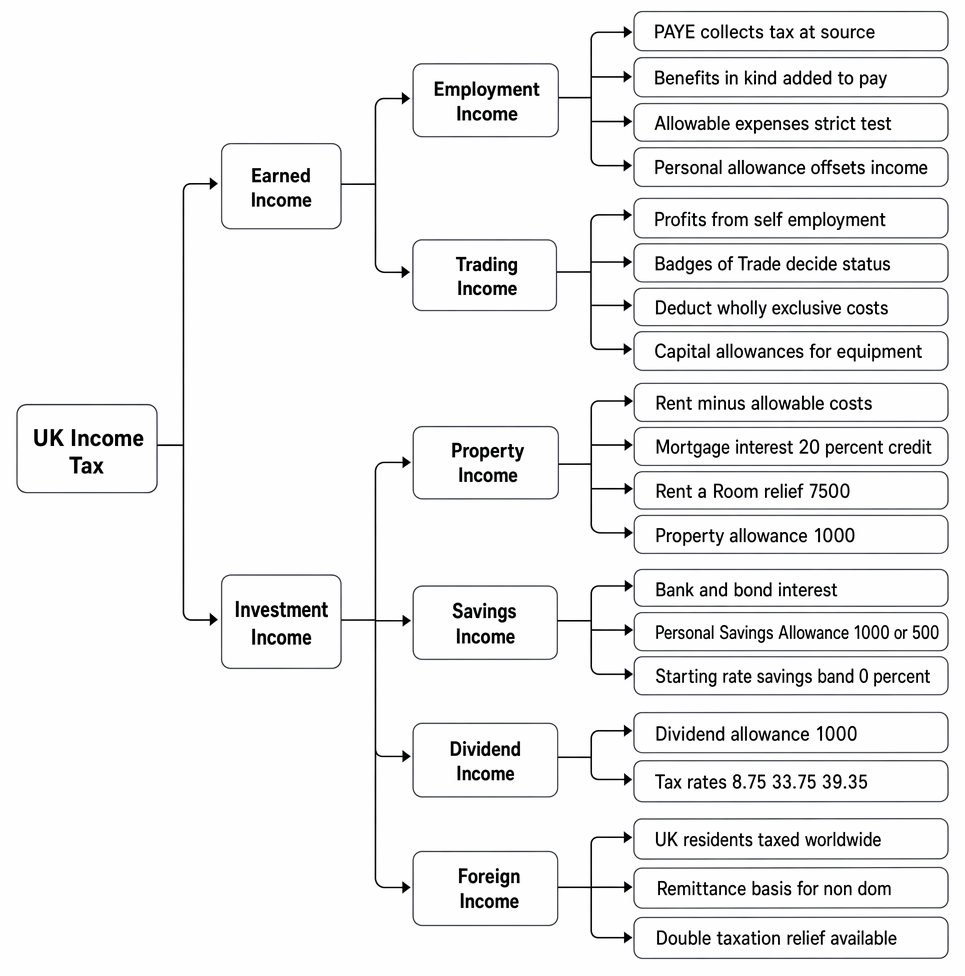

Income tax is levied on the total income of individuals, trustees, and personal representatives for each tax year, which runs from 6 April to 5 April. Different types of income are subject to specific rules regarding their calculation and the reliefs or allowances that can be applied. Understanding these distinctions is fundamental to determining an individual's overall income tax liability. This article focuses on the main types of income encountered in practice: employment income, trading income, property income, savings income, and dividend income. Foreign income is also briefly considered.

The principal categories of income chargeable to UK income tax and the main rules affecting their assessment.

Key Term: Income Tax Year

The period from 6 April in one year to 5 April in the next, used for assessing income tax liability. It is named after the two calendar years it spans (e.g., 2023/24).Test Tip: In SQE-style questions on Types of income, identify the legal test, the triggering fact, and the consequence before choosing between similar answer options.

Exam Warning: Do not rely on a familiar phrase from Types of income alone; check whether the facts satisfy every condition, exception, and timing requirement.

Employment Income

This category covers earnings derived from holding an office or employment.

Key Term: Employment Income

Income received from employment under a contract of service. This includes salary, wages, bonuses, commissions, and taxable benefits in kind.

Employment income is primarily governed by the Income Tax (Earnings and Pensions) Act 2003 (ITEPA). Tax is usually collected at source via the Pay As You Earn (PAYE) system, where the employer deducts income tax and National Insurance contributions before paying the employee their net salary.

Benefits in Kind

Many employees receive non-cash benefits, such as company cars or private medical insurance. These are known as benefits in kind and are generally taxable. Their value, calculated according to specific rules, is added to the employee's cash earnings to determine total taxable employment income.

Key Term: Benefits in Kind

Non-cash benefits provided by an employer (e.g., a company car for private use, private medical insurance). The taxable value is normally the cost to the employer or, for certain benefits (such as company cars), a figure determined by statutory formula.

Typical taxable benefits include:

- Company cars available for private use (benefit depends on list price and CO2 emissions).

- Private medical insurance (taxable at the employer’s cost).

- Beneficial loans above the statutory de minimis threshold.

- Assets transferred to employees.

Common exemptions include:

- Trivial benefits meeting HMRC conditions (not cash/vouchers, cost does not exceed the trivial benefit threshold per benefit, and not provided in recognition of services).

- One mobile phone per employee.

- Certain welfare counselling and workplace parking.

Benefits are reported via P11D (where applicable) or processed through payroll if the employer operates payrolling of benefits.

Allowable Expenses

Employees can claim tax relief for expenses incurred 'wholly, exclusively and necessarily' in performing their employment duties. This is a strict test, meaning few expenses qualify. Common examples include professional subscriptions to approved bodies or travel costs for business purposes (but not ordinary commuting between home and the permanent workplace). Where an employee works from home, relief is limited to additional costs incurred solely because of the duties of employment, following HMRC rules.

Trading Income

This includes profits generated from carrying on a trade, profession, or vocation as a sole trader or partner.

Key Term: Trading Income

Profits arising from self-employment or business activities undertaken with a view to profit.

The determination of whether an activity constitutes a trade is based on case law principles known as the 'Badges of Trade'.

Key Term: Badges of Trade

A set of factors derived from case law used by HMRC and courts to determine if an activity amounts to a trade for tax purposes. Factors include frequency of transactions, profit motive, nature of the asset, and method of acquisition/disposal.

Taxable trading profits are calculated by deducting allowable expenses and capital allowances from the business's chargeable receipts for the accounting period.

Allowable Expenses (Trading Income)

Expenses are deductible if incurred 'wholly and exclusively' for the purposes of the trade. Non-deductible items include drawings, fines, and client entertainment. Depreciation is not deductible; instead, relief for capital expenditure on plant and machinery is given through capital allowances.

Key Term: Capital Allowances (AIA/WDA)

Tax reliefs that recognise the decline in value of qualifying plant and machinery. The Annual Investment Allowance (AIA) provides 100% relief up to the statutory cap for most plant and machinery (excluding cars). Writing Down Allowances (WDA) give ongoing relief at set rates for expenditure not covered by AIA or for pooled assets.

Key points:

- AIA (currently set at a long-term level of £1,000,000) grants full deduction for qualifying plant and machinery up to the cap per year (exclusions apply, e.g., cars).

- Expenditure exceeding AIA or not qualifying is typically added to a pool and relieved via WDA (main pool rate applies; certain assets may go to special rate pool).

- Cars do not qualify for AIA; relief depends on emissions (allocated to the appropriate pool with relevant rates).

Other trading points:

- Use of home for business: apportion costs on a reasonable basis.

- Pre-trading expenditure: certain expenses incurred up to seven years before commencement may be treated as incurred on day one of trading if they would have been allowable had the trade already commenced.

For very small trading or miscellaneous receipts, a separate trading allowance may simplify the computation. If gross trading or miscellaneous income is within the allowance, no tax is due on it; if gross income exceeds the allowance, the taxpayer can elect to deduct the allowance instead of actual expenses, but cannot use both.

Basis of Assessment (Tax-Year Basis)

From 2024/25, unincorporated trading businesses are assessed on profits arising in the income tax year (the tax-year basis). The transitional year was 2023/24, during which overlap profits could be relieved. Under the tax-year basis:

- The profits taxed for a tax year are those that arise in that tax year (apportioning accounting periods that straddle tax years).

- Historic overlap profits created under the old current-year basis are relieved (transitional spreading rules applied in 2023/24).

Practical consequences:

- Businesses with non-31 March/5 April year ends apportion profits across tax years based on days in each tax year.

- Accounting date changes are optional but can simplify apportionments (e.g., adopting 31 March or 5 April).

Worked Example 1.1

A sole trader has an accounting period 1 July 2024 to 30 June 2025. The profit for that period is £60,000. What profit is assessable in the 2024/25 tax year under the tax-year basis?

Answer:

Under the tax-year basis, apportion the accounting period that overlaps the tax year 6 April 2024–5 April 2025. The period 1 July 2024–5 April 2025 is 279 days out of the 365-day accounting period (assume 365). Assessable profit in 2024/25 = £60,000 × (279/365) ≈ £45,918. The balance (86 days, 6 April–30 June 2025) is assessable in 2025/26.

Property Income

This category covers income arising from land and property owned by the taxpayer in the UK.

Key Term: Property Income

Income derived from letting property, such as rental income from houses, flats, or commercial buildings.

Taxable property income is the gross rent received less allowable expenses. The property business is computed on an accruals basis unless a specific alternative (e.g., the £1,000 property allowance election) is made.

Allowable expenses include:

- Repairs (not improvements), maintenance and redecorations.

- Insurance, letting agent fees and management charges.

- Ground rent, service charges and council tax (if paid by the landlord).

- Replacement of domestic items in residential lettings (see below).

Expenses that improve the property’s value or extend its useful life are capital (not revenue) and are not deductible against rental income; they may feature in capital gains computations on disposal.

Key Term: Replacement of Domestic Items Relief

Relief for the cost of replacing domestic items (e.g., sofas, beds, fridges) in a residential property. Deduct the cost of the replacement item (subject to adjustments for any proceeds or improvements), not the initial purchase cost.

Points on the relief:

- Applies to unfurnished, part-furnished, and fully furnished residential lettings.

- Relief is for replacement only; improvements (e.g., upgrading to a superior item) require a restriction to the equivalent of a like-for-like replacement.

- Any sale proceeds or reimbursements reduce the relief.

Allowable Expenses (Property Income)

Expenses incurred wholly and exclusively for the property business are deductible. Examples include repairs (not improvements), insurance, letting agent fees, and ground rent.

Finance Cost Relief Restriction

For residential properties, relief for finance costs (like mortgage interest) is restricted. Landlords cannot deduct these costs directly from rental income but instead receive a basic rate (20%) tax reduction based on the finance costs incurred. The restriction applies to individuals and certain partnerships/trust arrangements, not to companies (which may deduct interest in computing profits for corporation tax).

How the restriction works:

- Compute rental profit without deducting interest.

- Compute the tax reduction at 20% of the restricted finance costs (subject to limits, including where there are property losses or non-savings/non-dividend income below allowances).

- The reduction cannot create a repayment; it reduces tax liability down to zero only.

Rent-a-Room Relief

Individuals renting out a furnished room in their main residence can receive up to £7,500 per year tax-free under this scheme (halved to £3,750 each if jointly elected by two people). Where gross receipts exceed the threshold, the taxpayer can either:

- Elect into the scheme, being taxed on gross receipts minus the allowance; or

- Opt out and compute actual profits (receipts less allowable expenses).

Property Allowance

Individuals with gross property income of £1,000 or less do not need to declare or pay tax on it. If gross income exceeds £1,000, they can choose to deduct the £1,000 allowance instead of actual expenses (but cannot use both). The property allowance cannot be combined with rent-a-room relief for the same income.

Worked Example 1.2

Sam is a basic rate taxpayer with a single residential let. For the tax year:

- Gross rent: £12,000

- Repairs and agent fees: £2,000

- Mortgage interest: £3,600

Compute Sam’s taxable property income and the finance cost tax reduction.

Answer:

Taxable rental profit (before finance costs) = £12,000 − £2,000 = £10,000. Mortgage interest is not deducted; instead, Sam receives a tax reducer: 20% × £3,600 = £720. The £10,000 profit is added to Sam’s other income. The £720 reduces Sam’s total income tax liability.

Savings Income

This includes interest received from bank and building society accounts, corporate bonds, and government gilts.

Key Term: Savings Income

Income derived from interest-bearing accounts and investments.

Savings income is taxed with specific ordering rules and allowances. It is important to separate savings income from non-savings/non-dividend income (NSNDI) and dividend income for the rate calculations.

Key Term: Personal Savings Allowance (PSA)

An amount of savings interest taxed at 0%. The PSA is £1,000 for basic rate taxpayers, £500 for higher rate taxpayers, and £0 for additional rate taxpayers. Key Term: Starting Rate for Savings

A 0% band of up to £5,000 for savings income where NSNDI (after personal allowance) is low. The band is reduced £1-for-£1 by NSNDI above the personal allowance; where NSNDI exceeds the personal allowance by £5,000, no starting rate band remains.

Ordering rules for savings income:

- Identify total income and deduct the Personal Allowance to arrive at taxable income.

- Separate NSNDI, savings and dividend components.

- Savings income is taxed after NSNDI, applying:

- Starting rate for savings (where available) at 0%.

- PSA at 0%.

- Remaining savings income at the appropriate basic/higher/additional rate.

Personal Savings Allowance (PSA)

Most taxpayers receive a PSA, allowing them to earn some interest tax-free.

- Basic rate taxpayers: £1,000 PSA.

- Higher rate taxpayers: £500 PSA.

- Additional rate taxpayers: £0 PSA.

Interest within the PSA is taxed at a 0% rate.

Starting Rate for Savings

Individuals with low levels of NSNDI may qualify for the starting rate for savings. This allows up to £5,000 of savings income to be taxed at 0%. However, this £5,000 band is reduced by £1 for every £1 of NSNDI above the personal allowance.

Worked Example 1.3

Pat has employment income (NSNDI) of £11,000, savings interest of £4,200, and no dividend income. The Personal Allowance is £12,570. How much of Pat’s savings interest is taxed at 0%?

Answer:

Pat’s NSNDI (£11,000) is below the Personal Allowance, so none of the Personal Allowance is used by NSNDI. The available starting rate for savings is the full £5,000 band, but it is capped by the actual savings interest (£4,200). Therefore, the entire £4,200 is at 0% under the starting rate. PSA is technically available, but as all savings interest is already at 0%, PSA doesn’t bite. No tax is due on the savings interest.

Dividend Income

This refers to distributions of profit paid by companies to their shareholders.

Key Term: Dividend Income

Income received by shareholders from companies in the form of dividends.

Dividends are subject to specific tax rates and allowances.

Key Term: Dividend Allowance

A 0% rate band for dividend income. For 2026/27 the allowance is £500. It is applied before charging the remaining dividends at the applicable dividend rates.

Dividend income is always treated as the top slice of income when determining the applicable rate band. After applying the dividend allowance (taxed at 0%), the balance is taxed at:

- Dividend ordinary rate in the basic rate band.

- Dividend upper rate in the higher rate band.

- Dividend additional rate in the additional rate band.

Dividend Allowance

All taxpayers receive a Dividend Allowance. For 2026/27, this is £500. Dividend income within this allowance is taxed at 0%. The allowance is applied after other income components have used up the basic/higher rate bands.

Dividend Tax Rates

Dividends received above the Dividend Allowance are taxed at specific rates, which are lower than the main income tax rates:

- Basic rate band: 10.75%

- Higher rate band: 35.75%

- Additional rate band: 39.35%

Dividends are treated as the top slice of income when determining the applicable tax rate.

Worked Example 1.4

Anya has a salary of £45,000 and receives dividends of £3,500 in the 2026/27 tax year. She has no other income. How is her dividend income taxed? (Assume Personal Allowance is £12,570 and the basic rate band ends at £37,700 taxable income).

Answer:

Anya's taxable salary is £45,000 - £12,570 = £32,430. This income uses up £32,430 of her basic rate band (£37,700). She receives £3,500 in dividends. The first £500 is covered by the Dividend Allowance and is taxed at 0%. The remaining £3,000 of dividends fall within her remaining basic rate band (£37,700 - £32,430 = £5,270 available). Therefore, the £3,000 is taxed at the dividend ordinary rate of 10.75%. Tax payable on dividends = £3,000 x 10.75% = £322.50.

Foreign Income

Income arising from overseas sources (e.g., foreign employment, rental income from property abroad, interest from overseas bank accounts) is also potentially subject to UK income tax for UK residents. The treatment depends on the individual's residence and domicile status and the applicability of any Double Taxation Agreements. Taxpayers may be taxed on the 'arising basis' (taxed on worldwide income as it arises) or, if non-domiciled, potentially on the 'remittance basis' (taxed only on foreign income brought into the UK), subject to remittance basis charges for long-term UK residents. Relief is usually available for foreign tax already paid on the same income through UK double taxation relief (up to the UK tax attributable to that income).

Key points:

- UK tax resident individuals are generally taxed on worldwide income unless the remittance basis applies.

- Double Taxation Agreements may reduce or eliminate double tax; claim relief via self-assessment.

- Foreign interest and dividends are included in UK computations; allowances (e.g., PSA, Dividend Allowance) can still apply, subject to ordering rules.

Worked Example 1.5

Kim is UK resident and domiciled. Kim has UK salary £30,000, UK bank interest £900, and foreign bank interest £400 (foreign tax withheld £40). What UK tax is due on the savings income, assuming the PSA applies?

Answer:

Taxable NSNDI is within the basic rate band. Savings interest totals £1,300 (£900 + £400). As a basic rate taxpayer, Kim’s PSA is £1,000 at 0%. The remaining £300 savings interest falls within the basic rate band and is taxed at 20% = £60. Double tax relief is available on the foreign interest up to the UK tax on that same income. The UK tax on the foreign portion within the PSA is 0%, and on the remainder it is within the £300 charge; proportionate relief is limited to the UK tax attributable. Here, if the £300 charge relates to UK interest, the foreign DTR may be nil; if part relates to foreign interest, relief is limited to the UK tax on that foreign portion (capped at £40 actually paid).

Trading Income: Bringing it Together

Finally, bringing trading computation together with capital allowances:

Worked Example 1.5

A sole trader has chargeable receipts of £110,000. Deductible expenses (excluding depreciation) are £74,000. During the year, the trader buys qualifying plant and machinery for £35,000 and a car (not eligible for AIA) allocated to the appropriate capital allowance pool.

Compute trading profit using AIA and WDA principles (ignore detailed car pool rates; assume the car goes to a pool with WDA at the relevant rate and that no private use adjustment is needed).

Answer:

Profit before capital allowances = £110,000 − £74,000 = £36,000. AIA can be claimed on the £35,000 plant and machinery in full, reducing profit to £1,000. The car does not qualify for AIA; it is added to the appropriate pool with WDA given at the rate for that pool. The WDA reduces the pool but, where there is insufficient profit, the WDA may create or increase a loss carried forward within the trade (subject to trading loss relief rules). Here, profit remains £1,000 (assuming the car’s WDA is deferred if it would otherwise create a loss or absorbed into the computation leading to a small loss; detailed pooling rates would determine the final figure).

Key Point Checklist

This article has covered the following key knowledge points:

- Income tax is charged on different types of income, including employment, trading, property, savings, and dividend income.

- Employment income includes salary and benefits; taxable benefits in kind are added to cash pay. Allowable employment expenses are tightly restricted.

- Trading income is calculated as receipts less allowable expenses and capital allowances; AIA and WDA give relief for qualifying plant and machinery.

- From 2024/25, trading profits for unincorporated businesses are assessed on the tax-year basis (apportionment where necessary), with overlap profits relieved via transitional rules.

- Property income is rental income less allowable expenses, including repairs and replacement of domestic items. Residential property finance costs attract a 20% tax reducer rather than a deduction.

- Rent-a-room relief and the £1,000 property allowance operate as alternatives to actual expenses; they cannot be combined for the same income.

- Savings income is subject to ordering rules, the Personal Savings Allowance (0% band), and can benefit from the starting rate for savings where NSNDI is low.

- Dividend income benefits from the Dividend Allowance (0% band) and is charged at specific rates above the allowance; dividends are the top slice of income.

- Foreign income for UK residents is generally taxed on the arising basis with double taxation relief available; non-domiciled individuals may use the remittance basis subject to conditions.

Key Terms and Concepts

- Income Tax Year

- Employment Income

- Benefits in Kind

- Trading Income

- Badges of Trade

- Capital Allowances (AIA/WDA)

- Property Income

- Replacement of Domestic Items Relief

- Savings Income

- Personal Savings Allowance (PSA)

- Starting Rate for Savings

- Dividend Income

- Dividend Allowance